Question

Assuming the capitals are fixed in Question give the necessary adjusting journal entry.

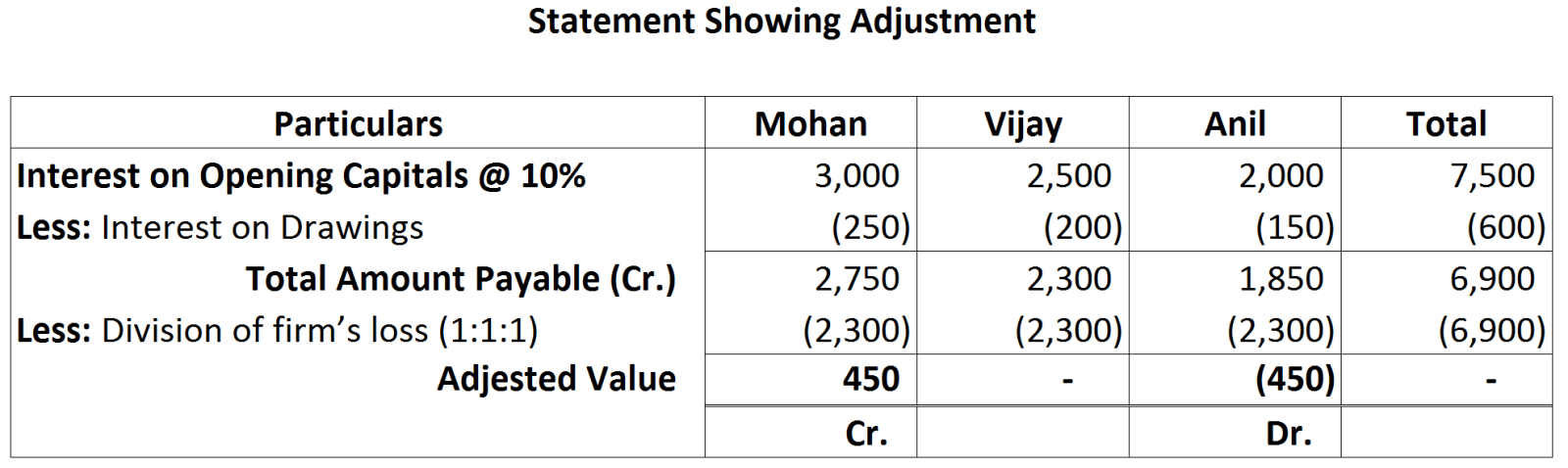

Mohan, Vijay and Anil are partners their capitals being ₹ 30,000, ₹ 25,000 and ₹ 20,000 respectively, In arriving at these figures, the profits for the year ended, 31st March, 2018 ₹ 24,000 has already been credited to the partners in the proportion in which they share profits. Their drawings were ₹ 5,000 (Mohan) ₹ 4,000 (Vijay) and ₹ 3,000 (Anil) for the year ending 31st March 2018. Subsequently the following omissions were noticed and it was decided to bring them into Account.

Mohan, Vijay and Anil are partners their capitals being ₹ 30,000, ₹ 25,000 and ₹ 20,000 respectively, In arriving at these figures, the profits for the year ended, 31st March, 2018 ₹ 24,000 has already been credited to the partners in the proportion in which they share profits. Their drawings were ₹ 5,000 (Mohan) ₹ 4,000 (Vijay) and ₹ 3,000 (Anil) for the year ending 31st March 2018. Subsequently the following omissions were noticed and it was decided to bring them into Account.

- Interest on Capital at 10% p.a.

- Interest on Drawings Mohan ₹ 250, Vijay ₹ 200 and Anil ₹ 150.