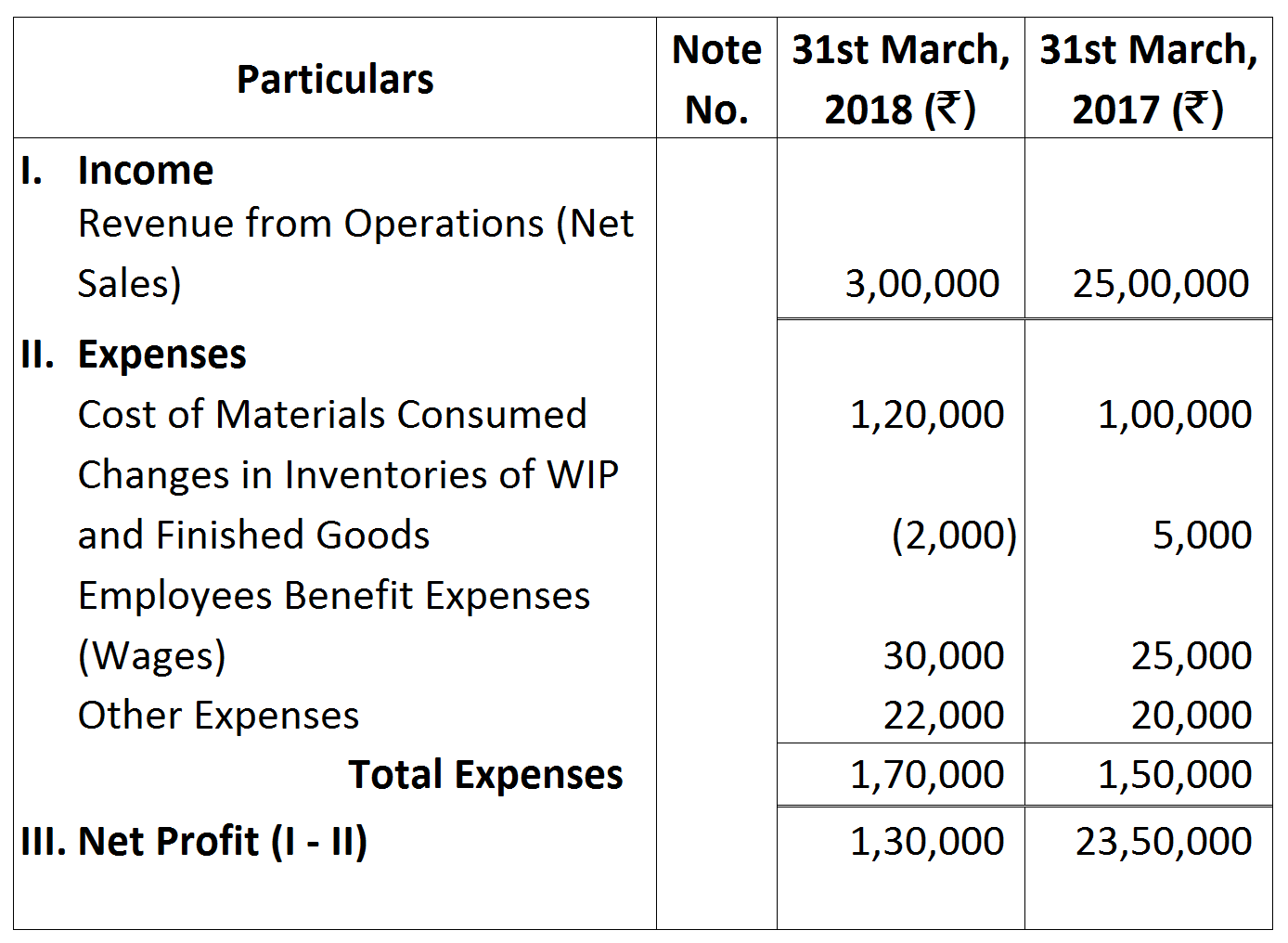

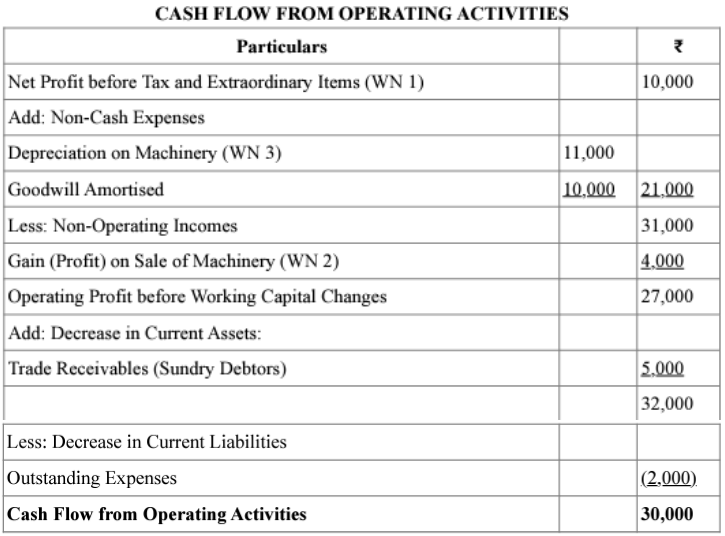

Question

Calculate Cash Flow from Operating Activities from the following information:

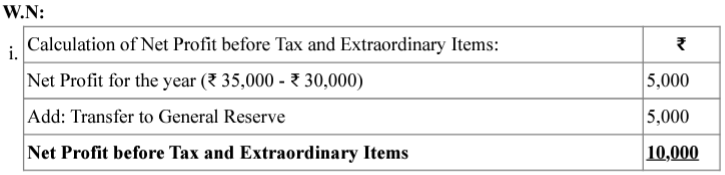

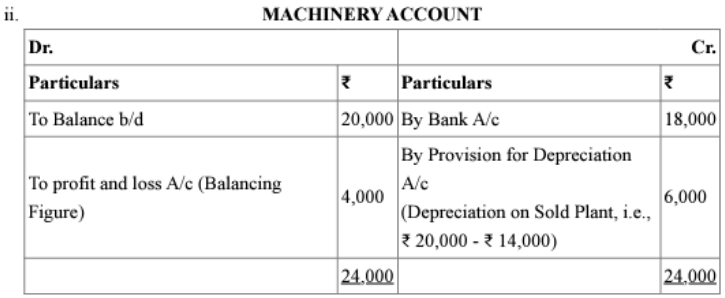

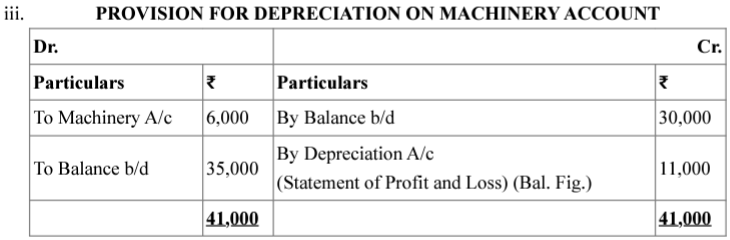

Machinery costing ₹ 20,000 having book value of ₹ 14,000 was sold for ₹ 18,000 during the year.

| Particulars | Opening Balances (₹) | Closing Balances (₹) |

| Surplus, i.e., Balance in Statement of Profit and Loss | 30,000 | 35,000 |

| General Reserve | 10,000 | 15,000 |

| Provision for Depreciation on Machinery | 30,000 | 35,000 |

| Outstanding Expenses | 5,000 | 3,000 |

| Goodwill | 20,000 | 10,000 |

| Trade Receivables (Sundry Debtors) | 40,000 | 35,000 |

10 each at a premium of ₹

10 each at a premium of ₹  5 per share. The amount was payable as follows:

5 per share. The amount was payable as follows:

3 per share (including premium ₹

3 per share (including premium ₹  1 per share)

1 per share) ₹ 5 per share (including premium

₹ 5 per share (including premium  ₹ 2 per share)

₹ 2 per share) 8 per share fully paid up. The re-issued shares included all the forfeited shares of Jeevan.

8 per share fully paid up. The re-issued shares included all the forfeited shares of Jeevan.