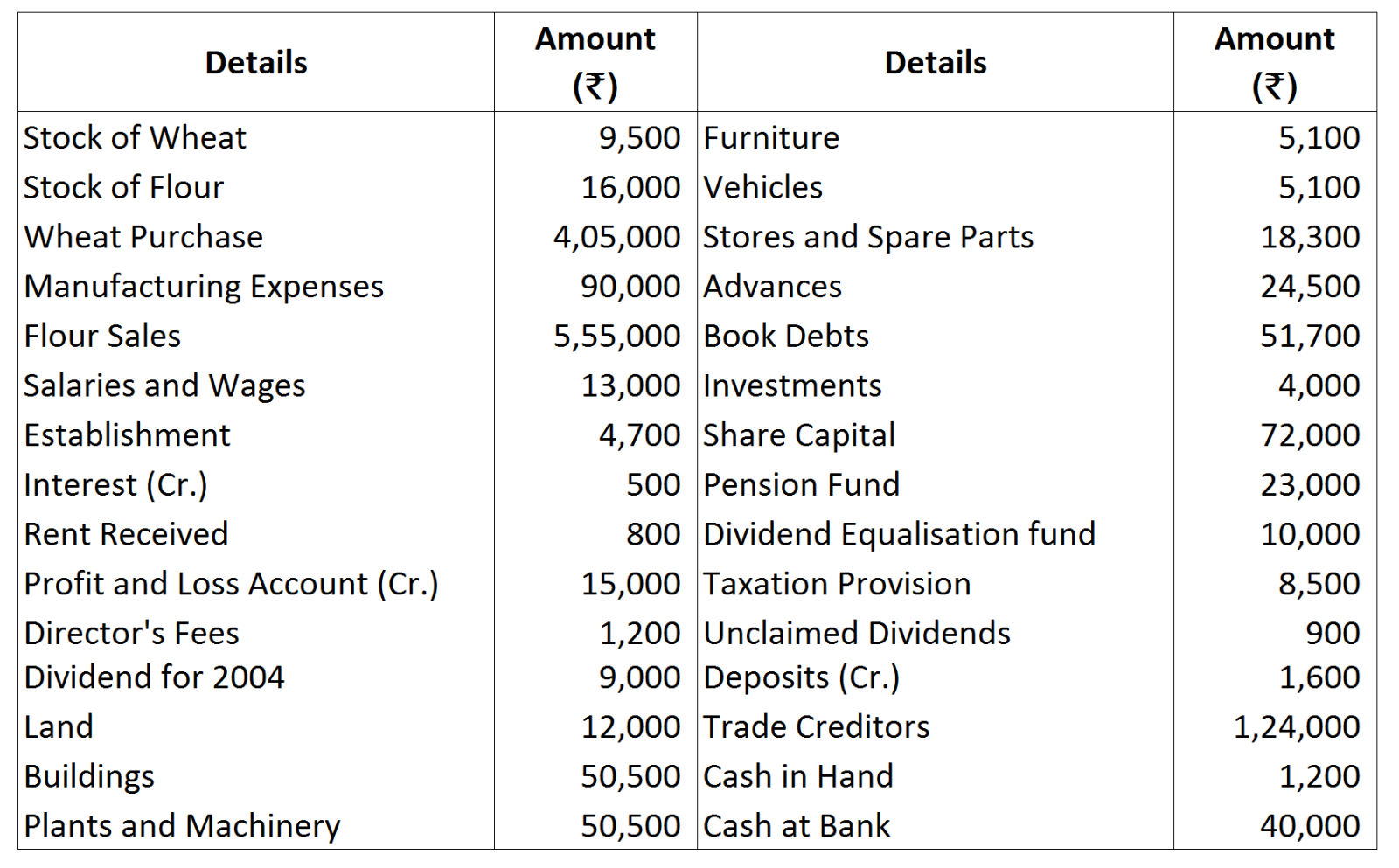

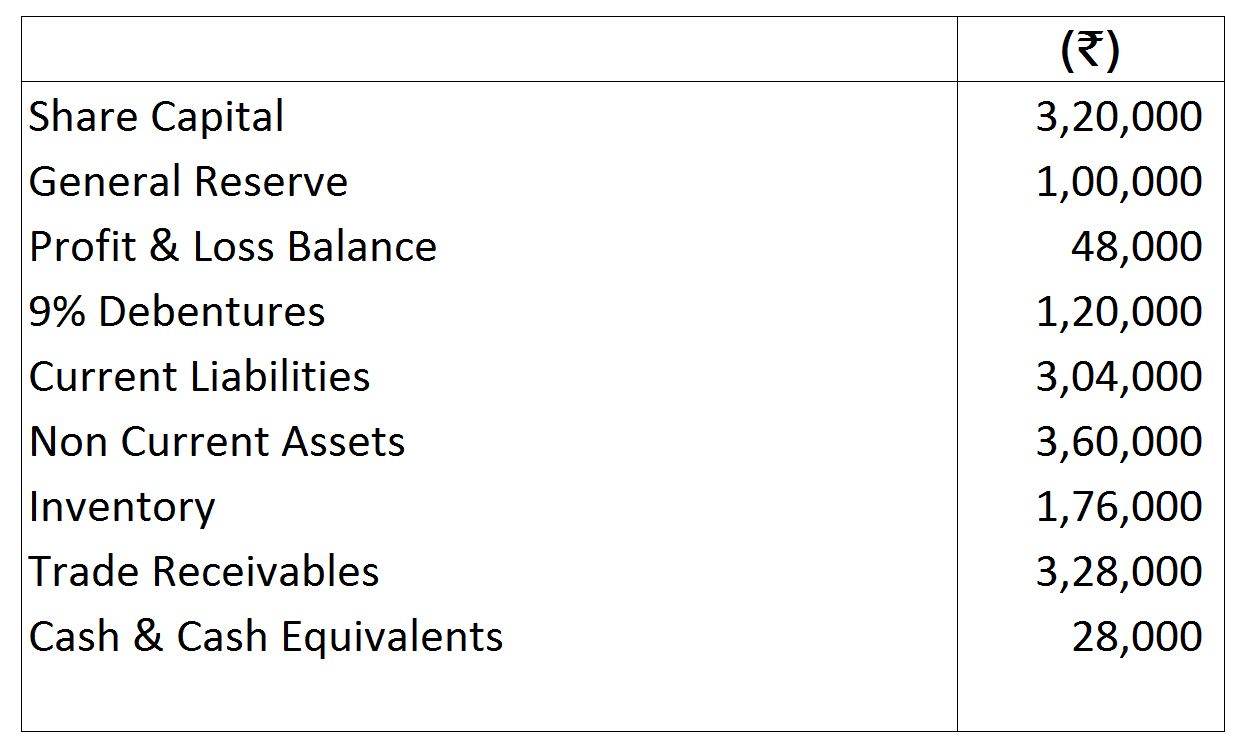

Question

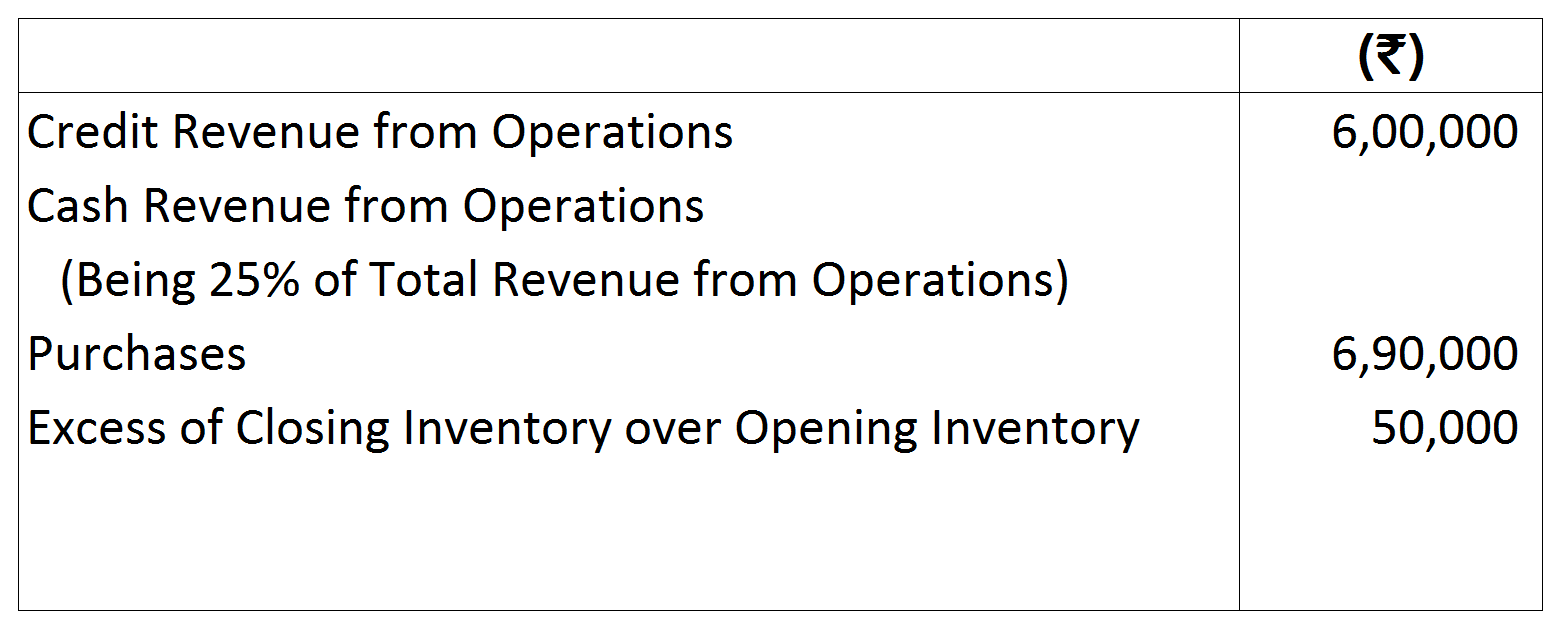

Calculate G.P. Ratio from the following:

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

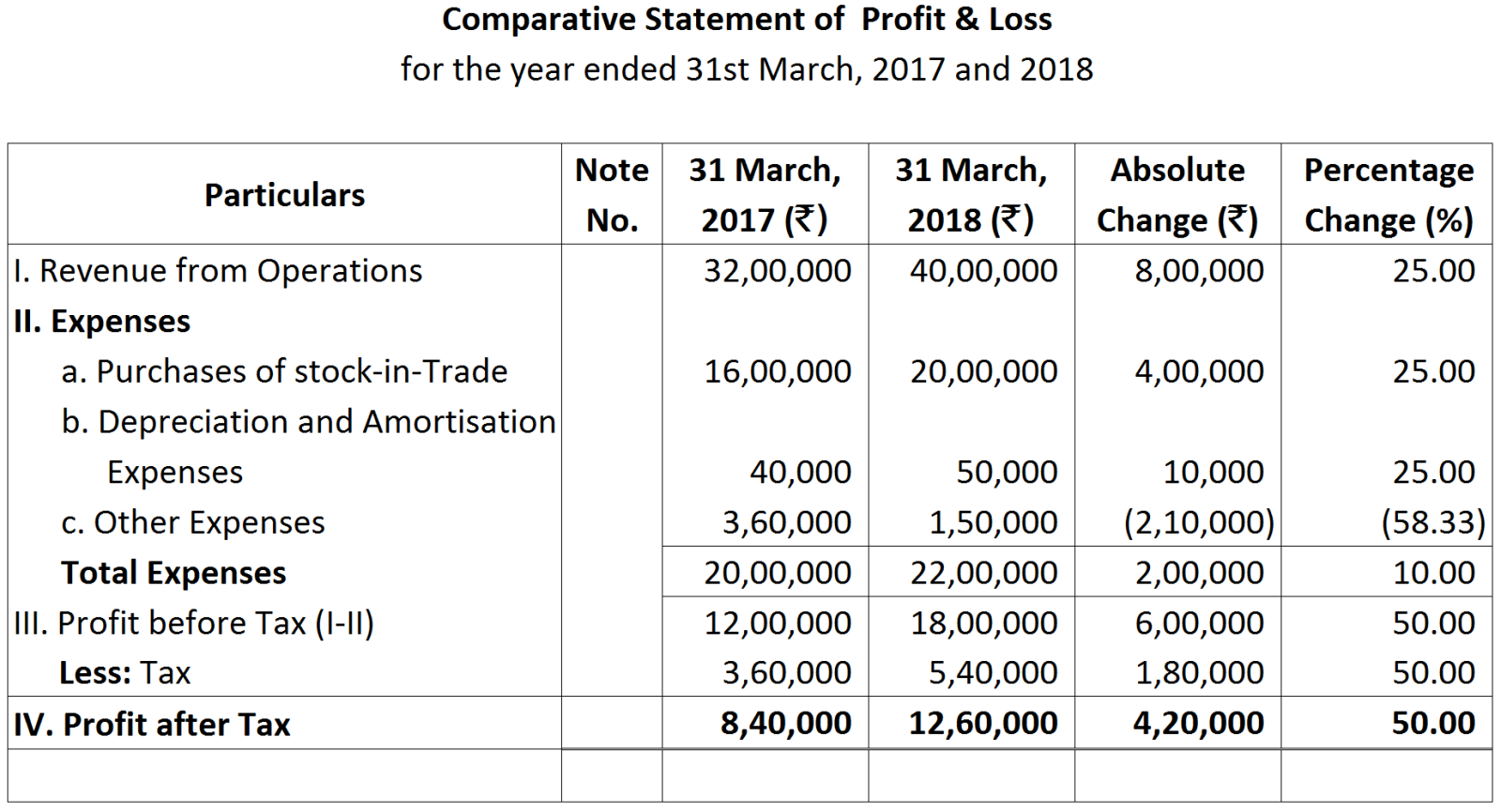

From the above Comparative Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Operating ratio.

From the above Comparative Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Operating ratio.| On application | - | ₹ 6 (including ₹ 1 premium) |

| On allotment | - | ₹ 2 (including ₹ 1 premium) |

| On first call | - | ₹ 3 (including ₹ 1 premium) |

| On second and final call | - | ₹ 3 (including ₹ 1 premium) |