Question

Calculate Return on Investment from the following:

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

On Application

|

₹ 6 (including ₹ 2 premium)

|

|

On Allotment

|

₹ 6 (including ₹ 2 premium)

|

|

On First Call

|

₹ 3 (including ₹ 2 premium)

|

|

On Second & Final Call

|

₹ 3 (including ₹ 2 premium)

|

| On 6,000 shares | Full amount called, |

| On 1,250 shares | ₹ 4 per share, |

| On 500 shares | ₹ 3 per share, |

| On 250 shares | ₹ 2 per share. |

Notes:

Notes:

|

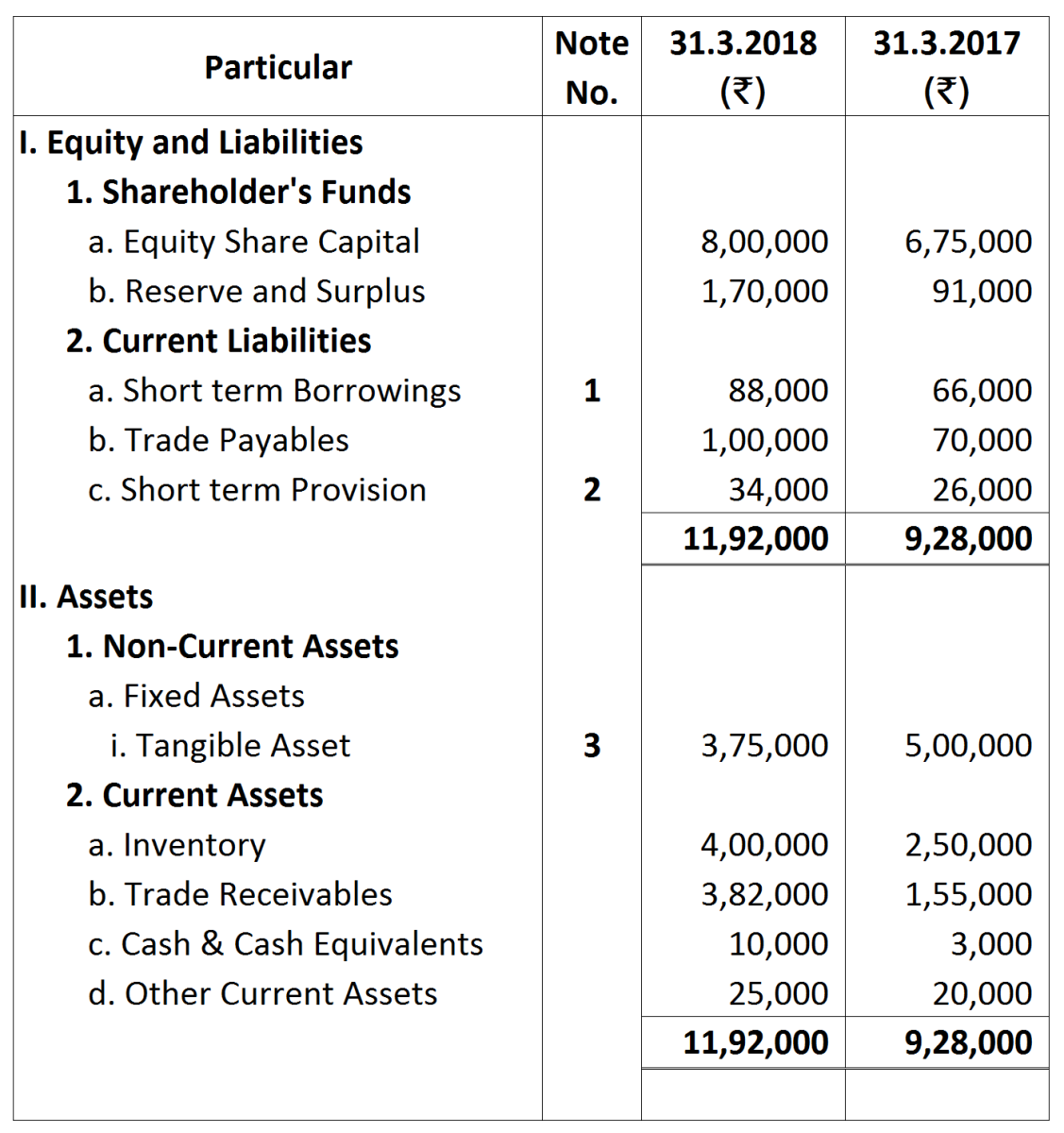

1.

|

Short-term Borrowings:

|

31.3.2018

|

31.3.2017

|

|

|

Bank Overdraft

|

88,000

|

66,000

|

|

2.

|

Short-term Provision

|

|

|

|

|

Taxation Provision

|

34,000

|

26,000

|

|

3

|

Tangible Assets:

|

|

|

|

|

Land

|

1,50,000

|

2,00,000

|

|

|

Plant

|

2,25,000

|

3,00,000

|

|

|

|

3,75,000

|

5,00,000

|