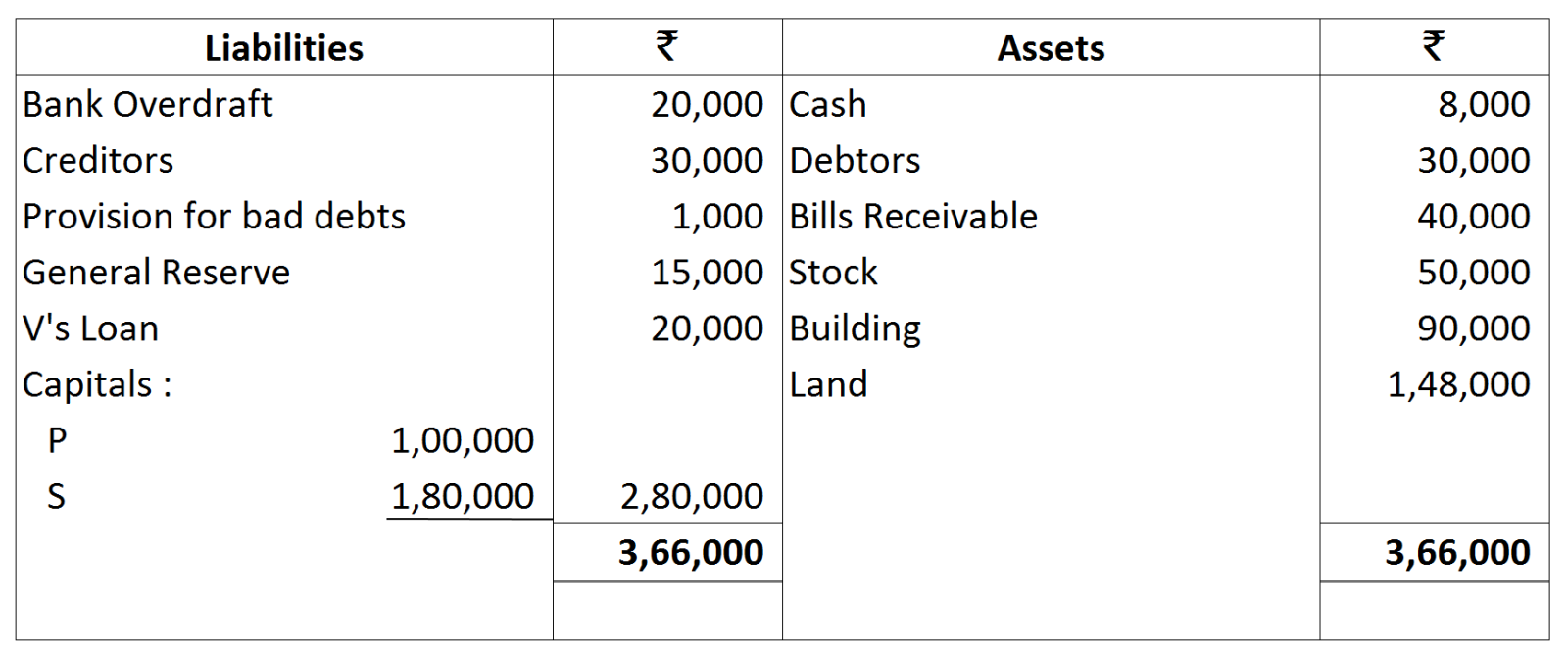

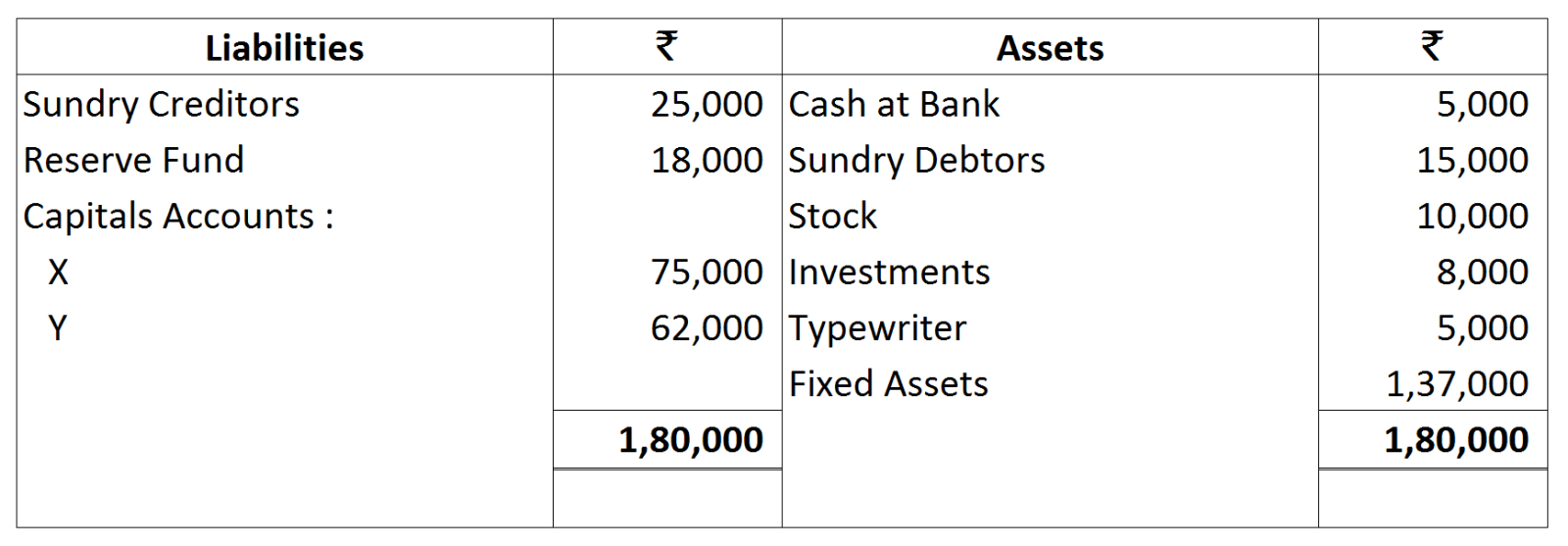

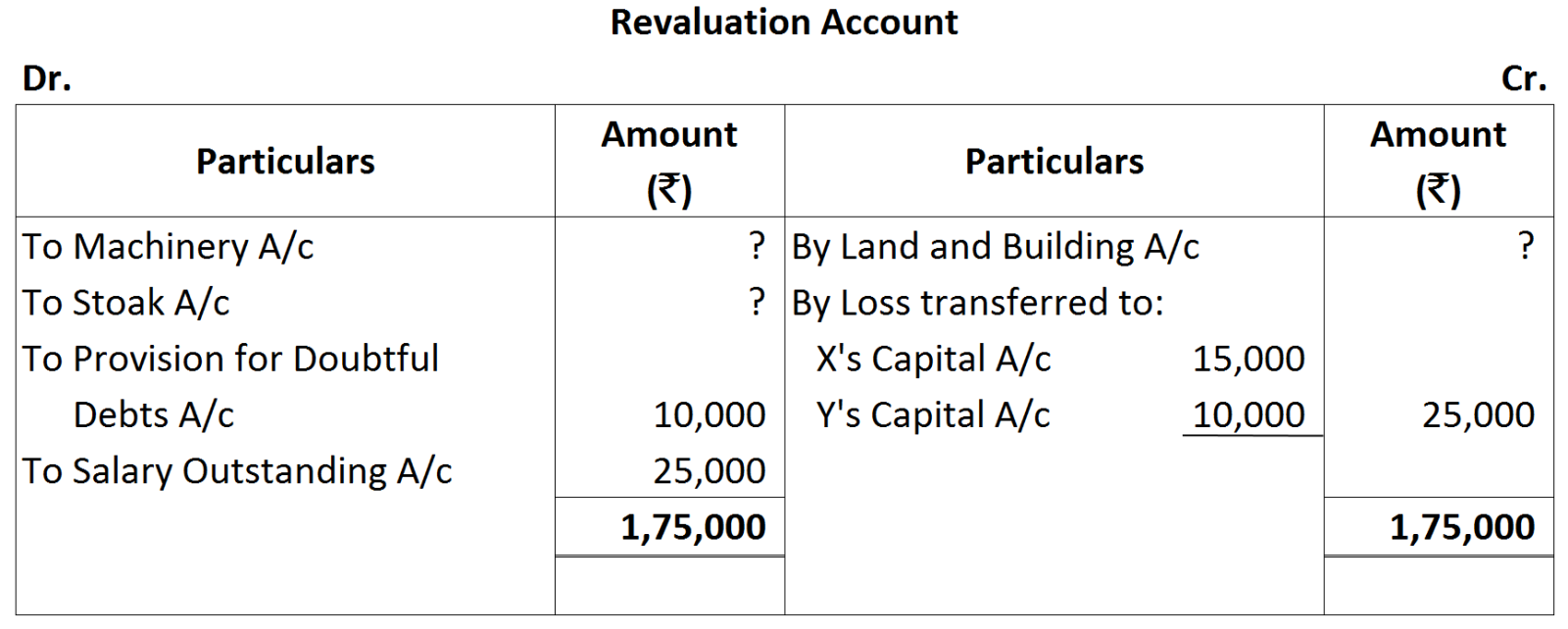

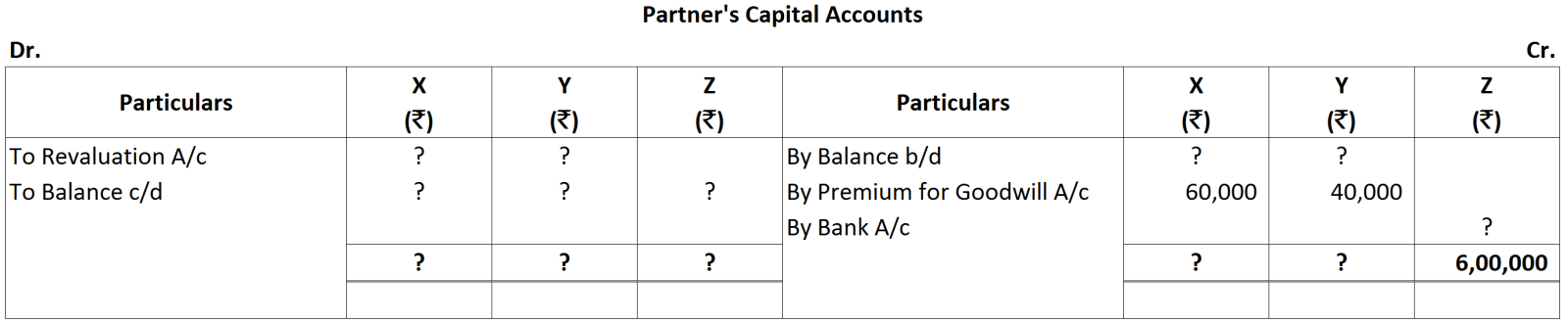

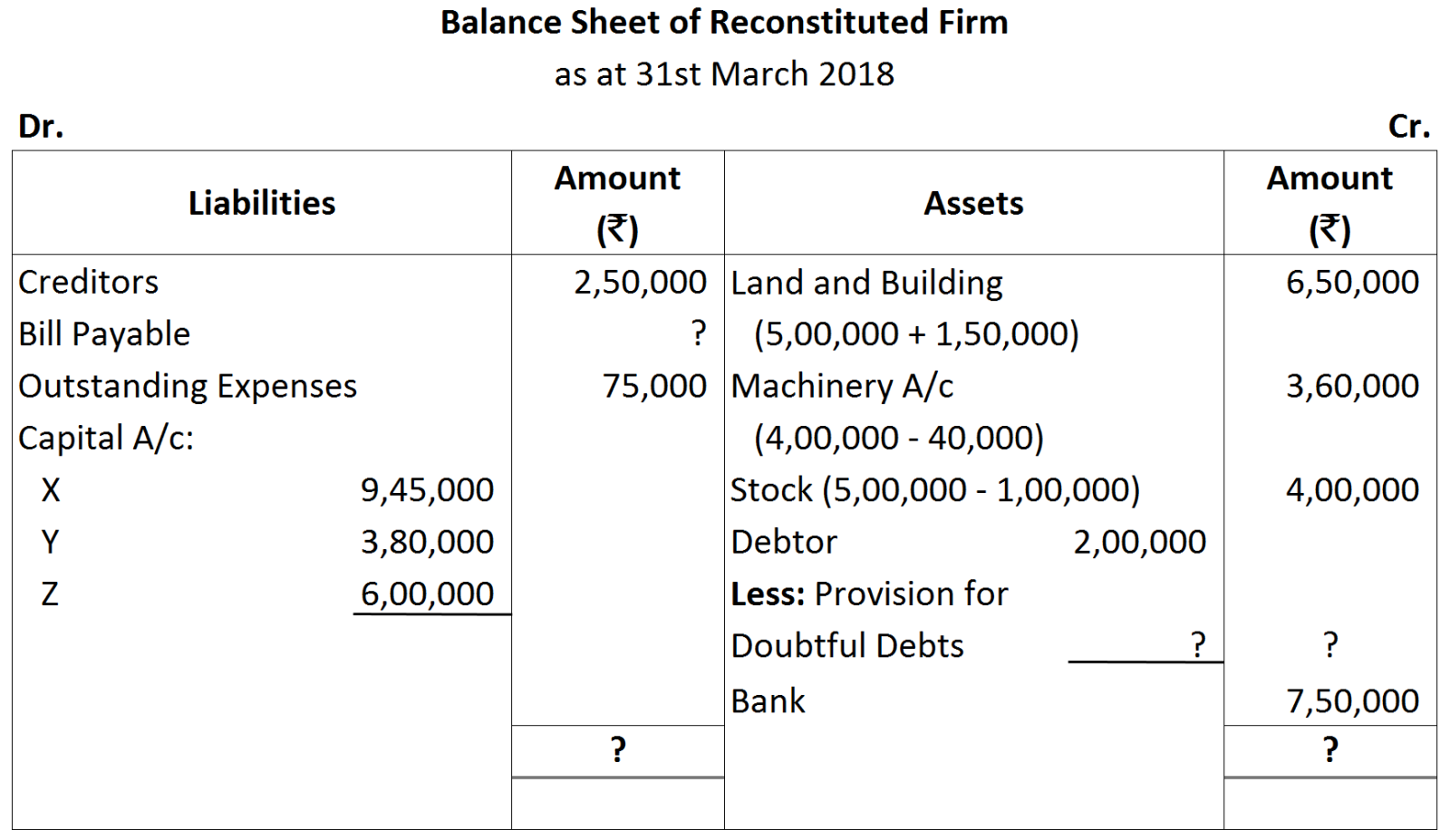

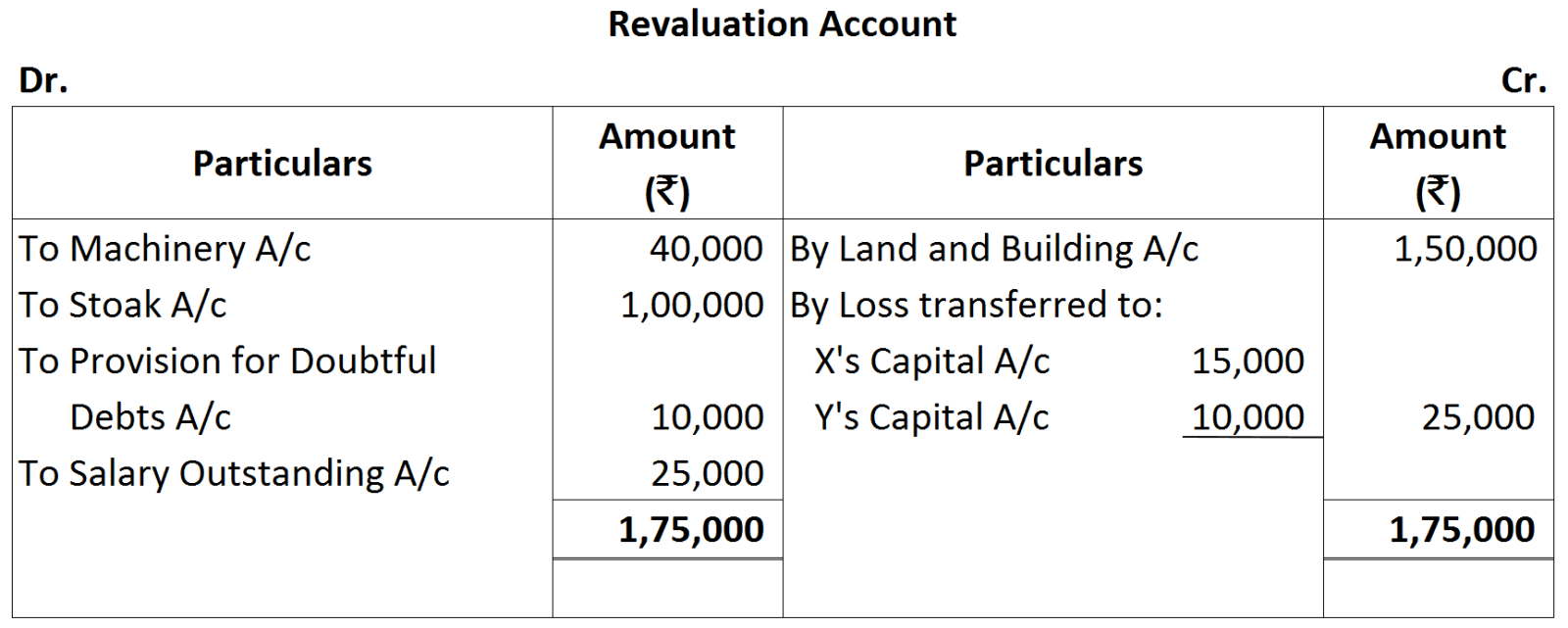

Question

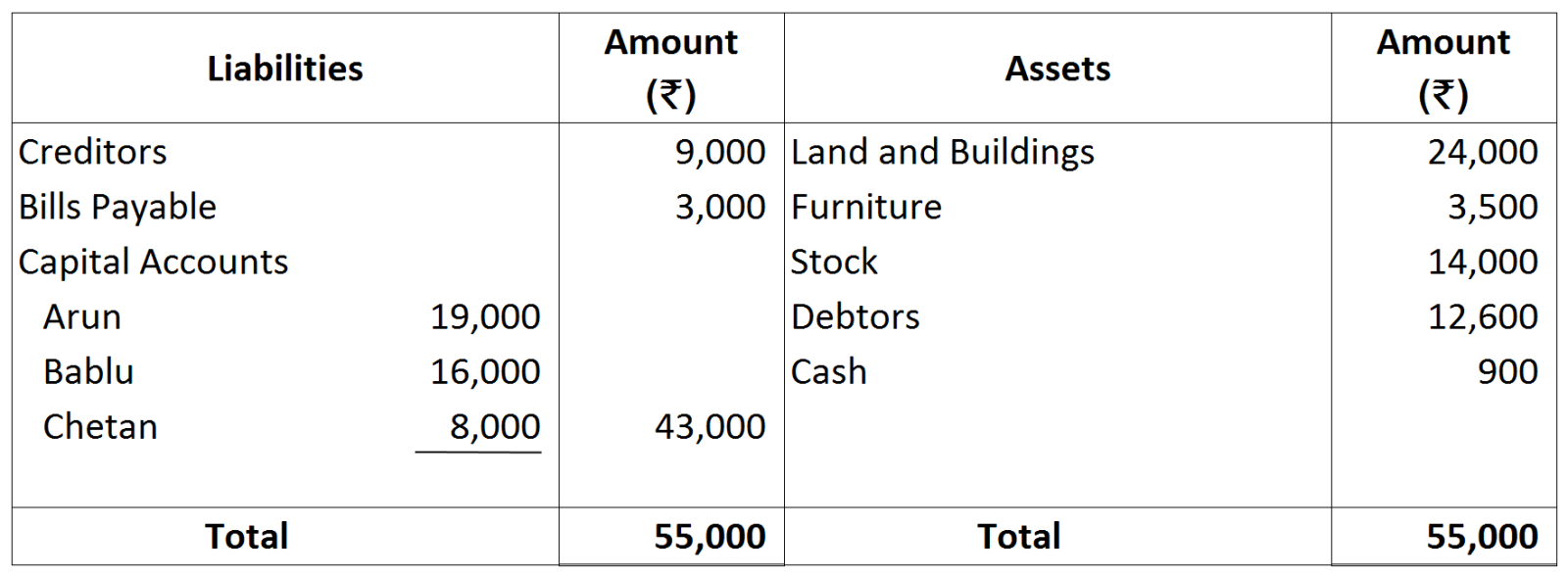

Complete the missing amounts in the following accounts:

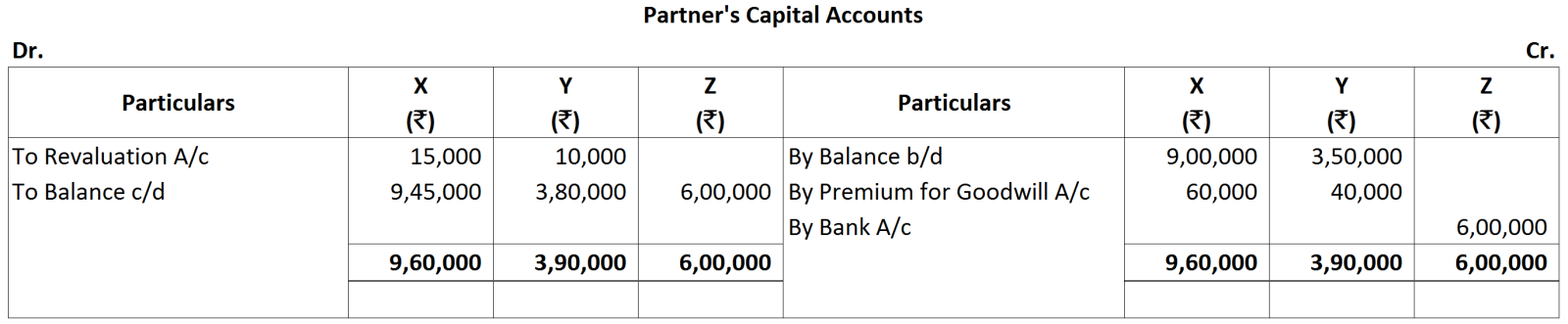

Notes:

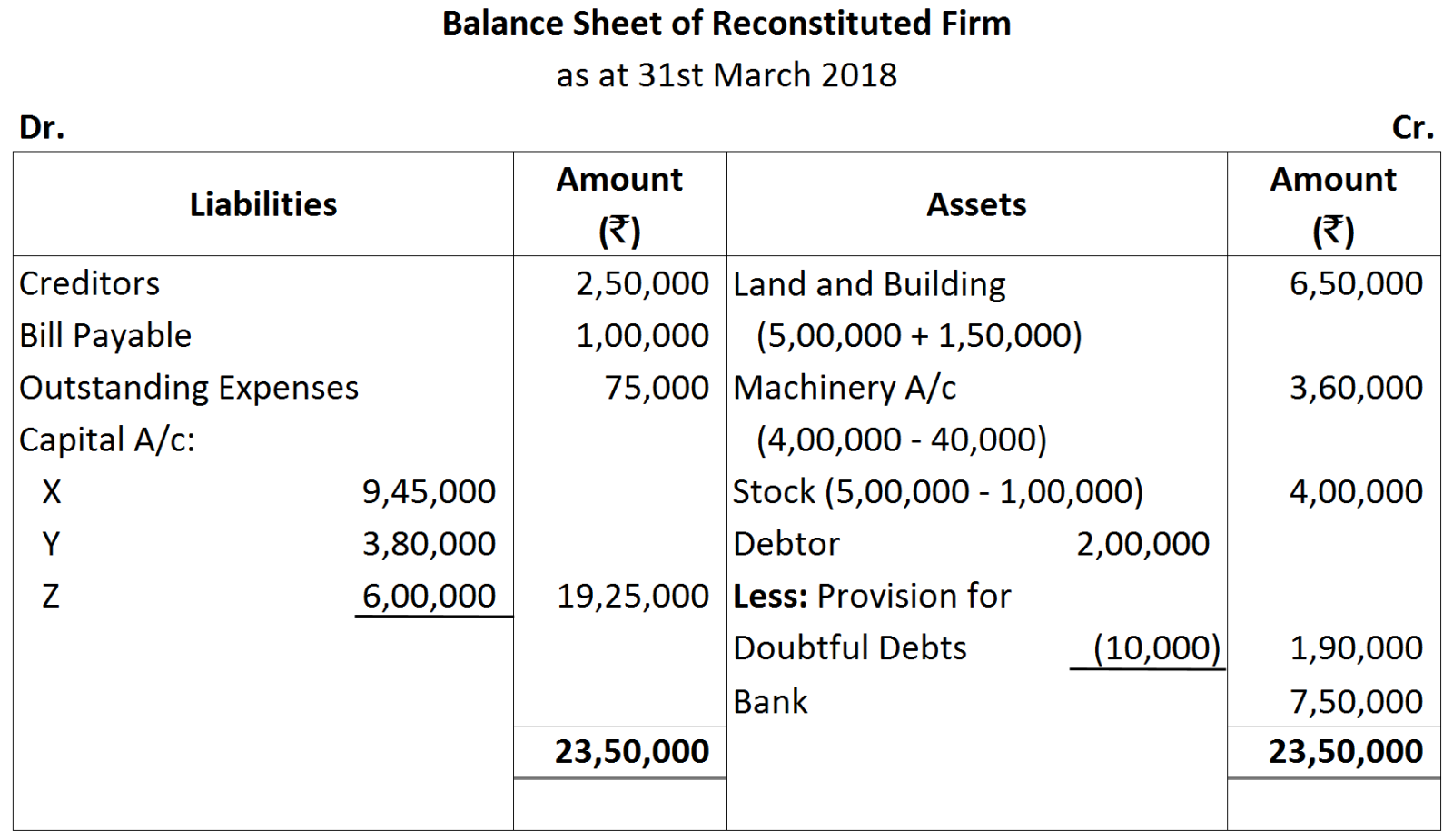

Notes:

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

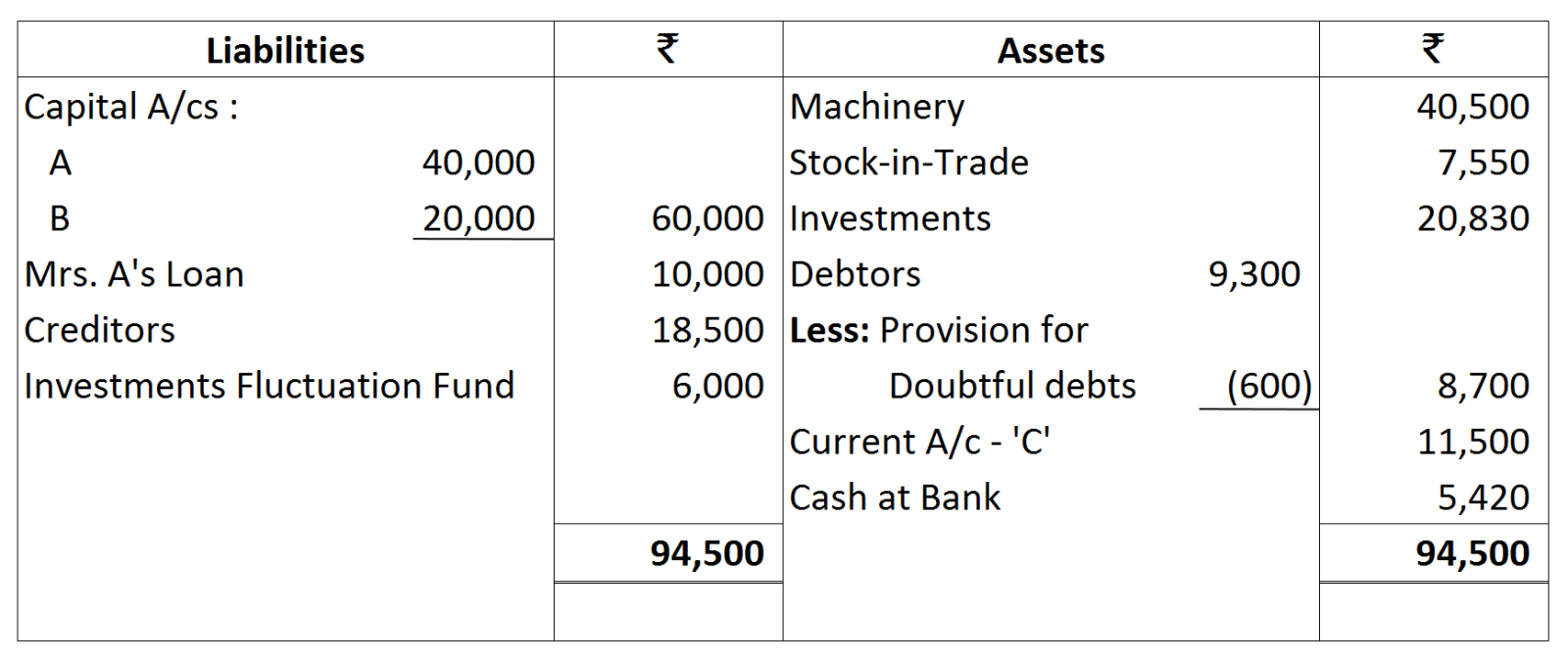

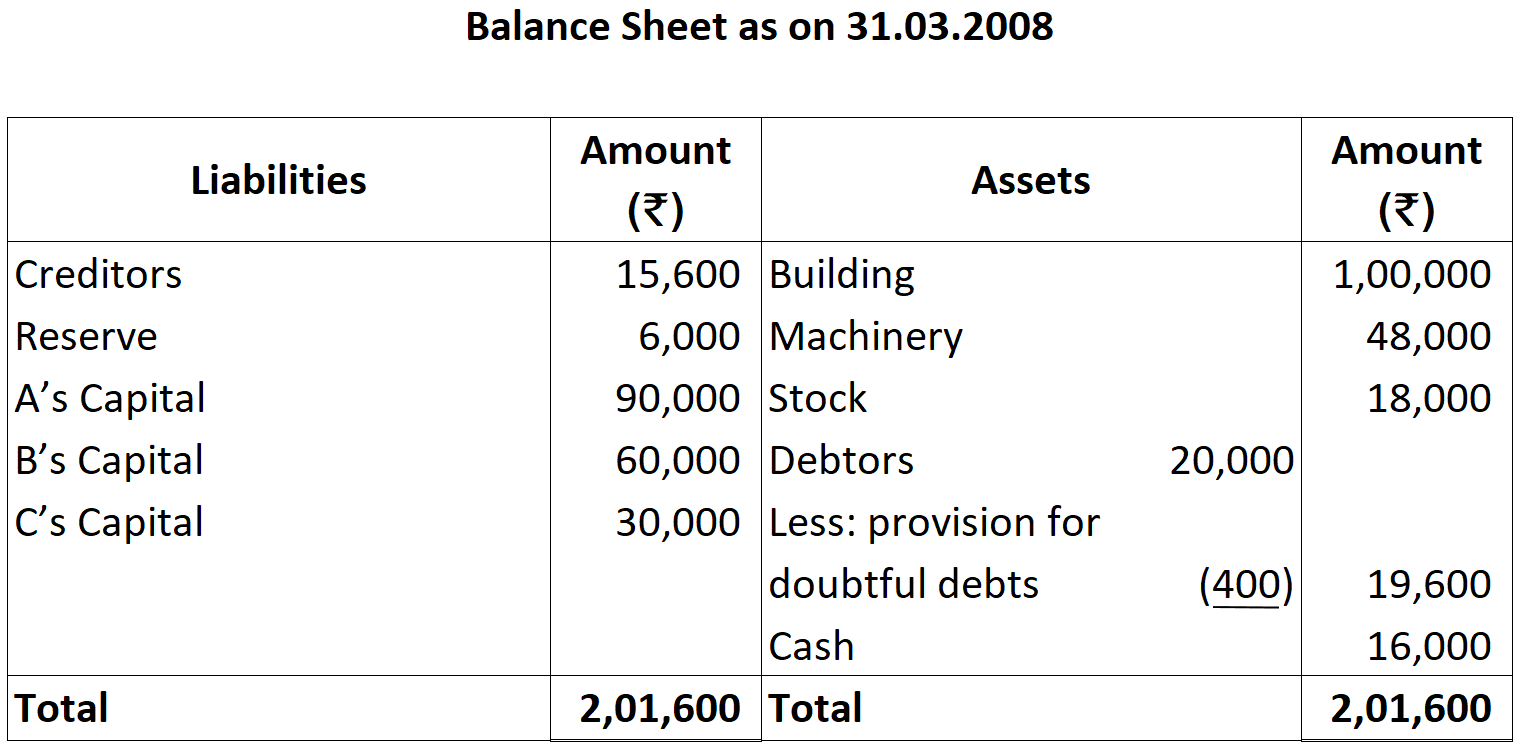

On the above date B retired owing to ill health and the following adjustments were agreed upon.

On the above date B retired owing to ill health and the following adjustments were agreed upon.

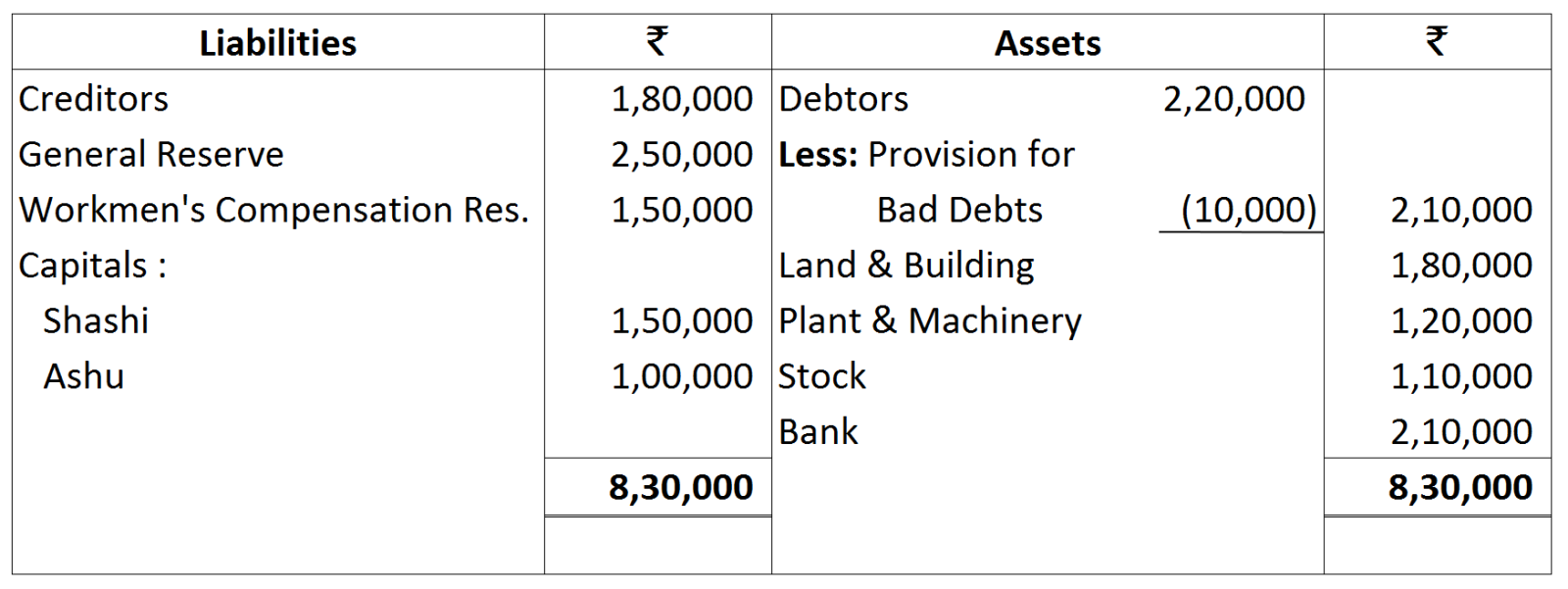

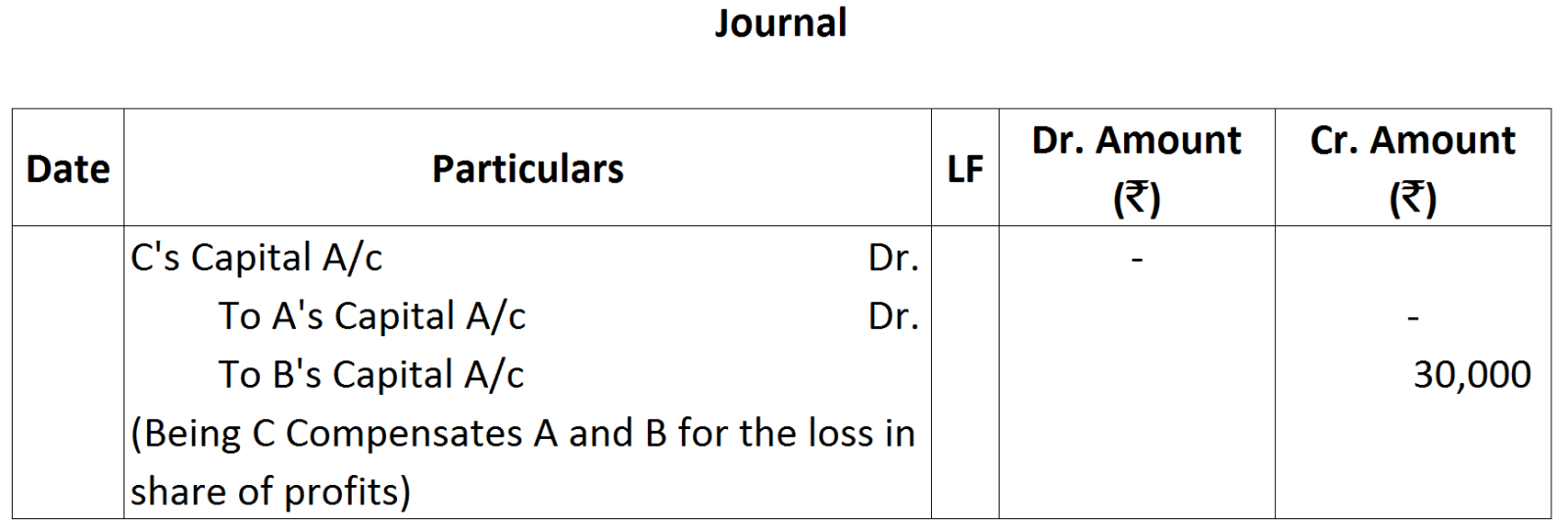

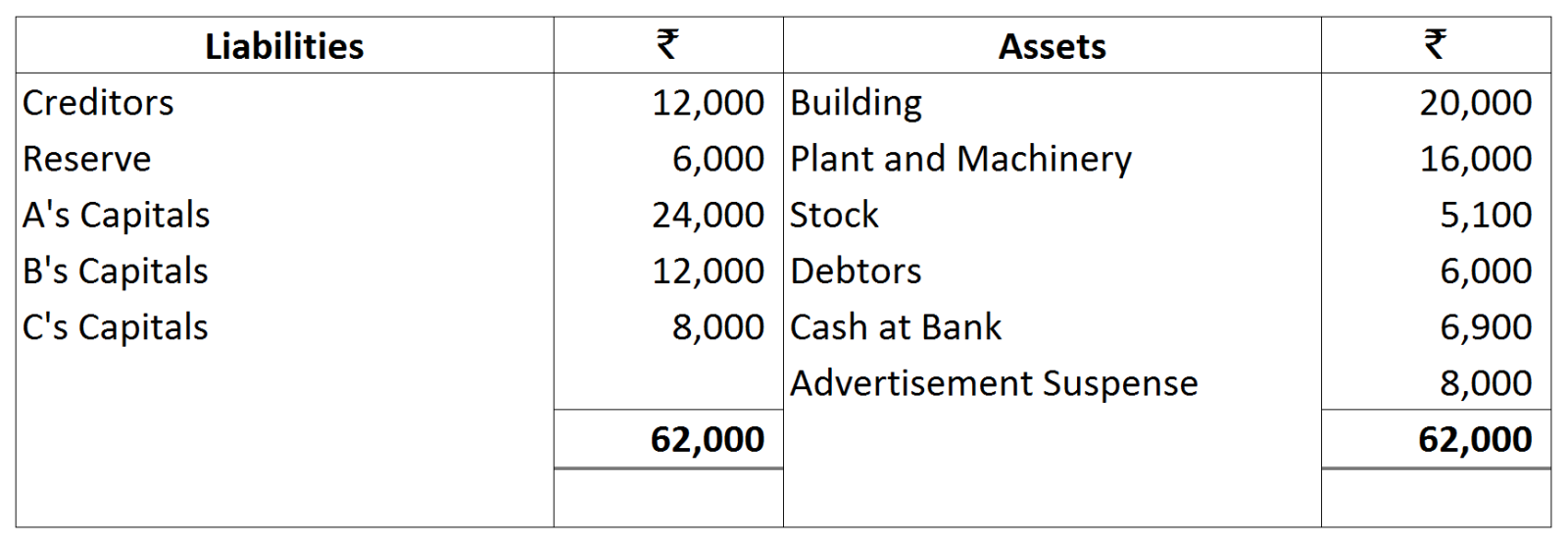

A died on 30-9-2018 and B and C decided to share future profits in the ratio of 7 : 3 Under the partnership agreement the executors of a deceased partner were entitled to:

A died on 30-9-2018 and B and C decided to share future profits in the ratio of 7 : 3 Under the partnership agreement the executors of a deceased partner were entitled to: