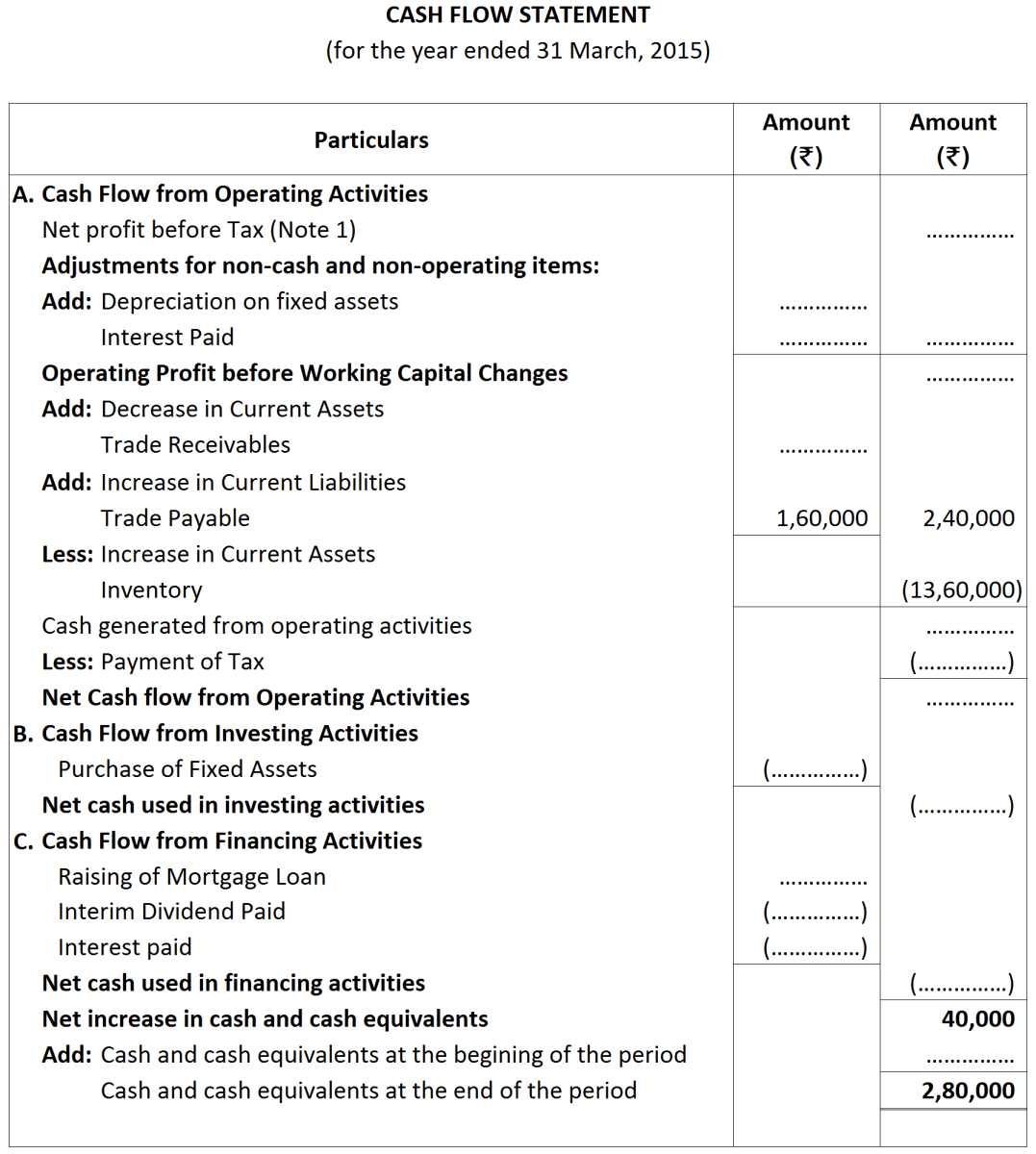

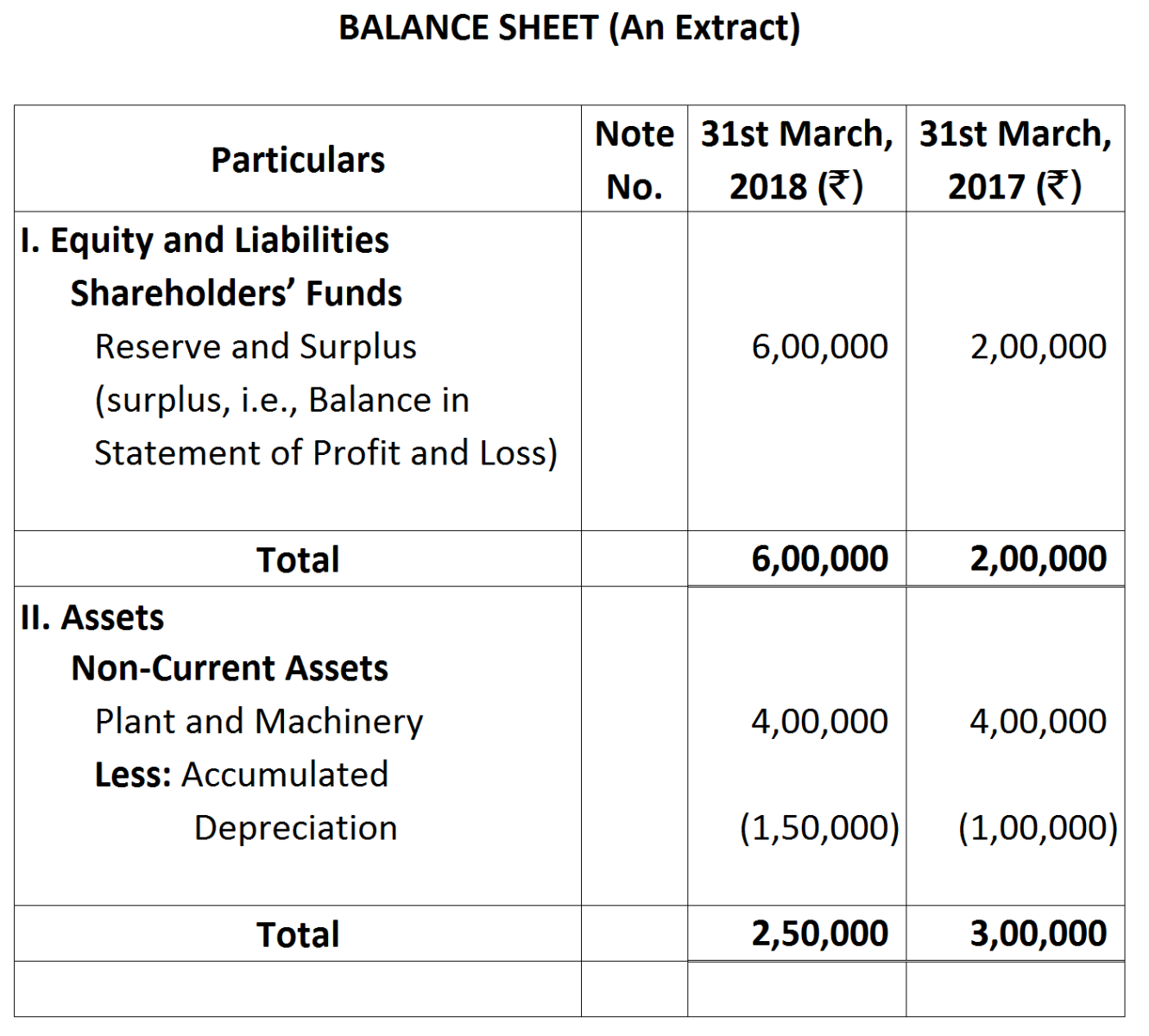

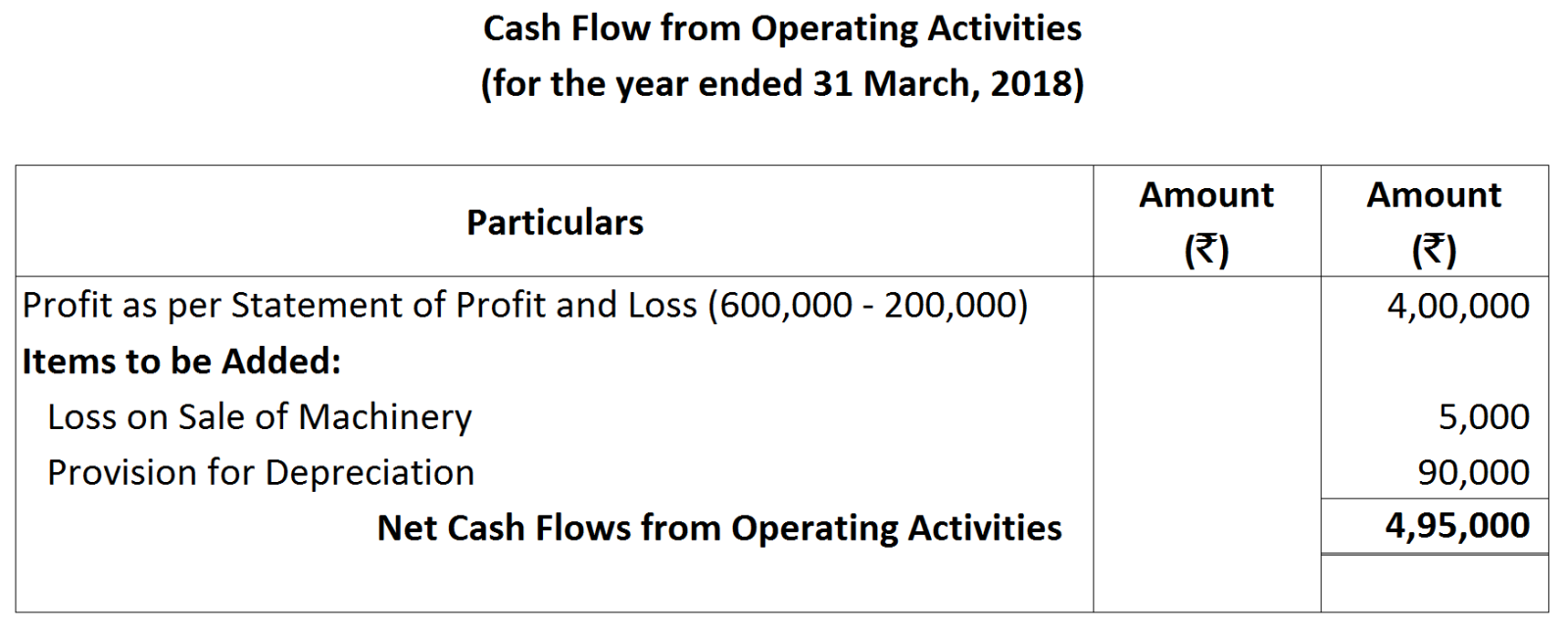

Question

Compute Cash Flow from Operating Activities from the following:

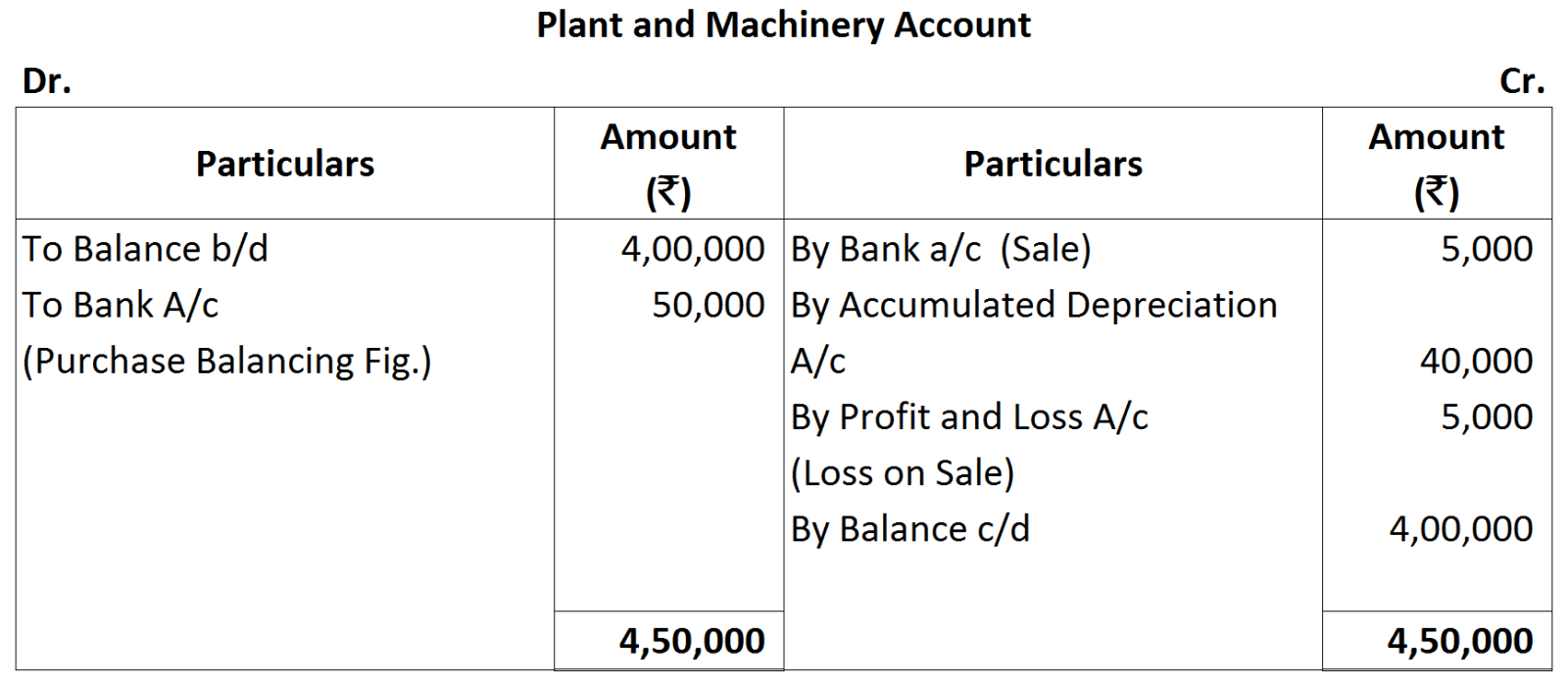

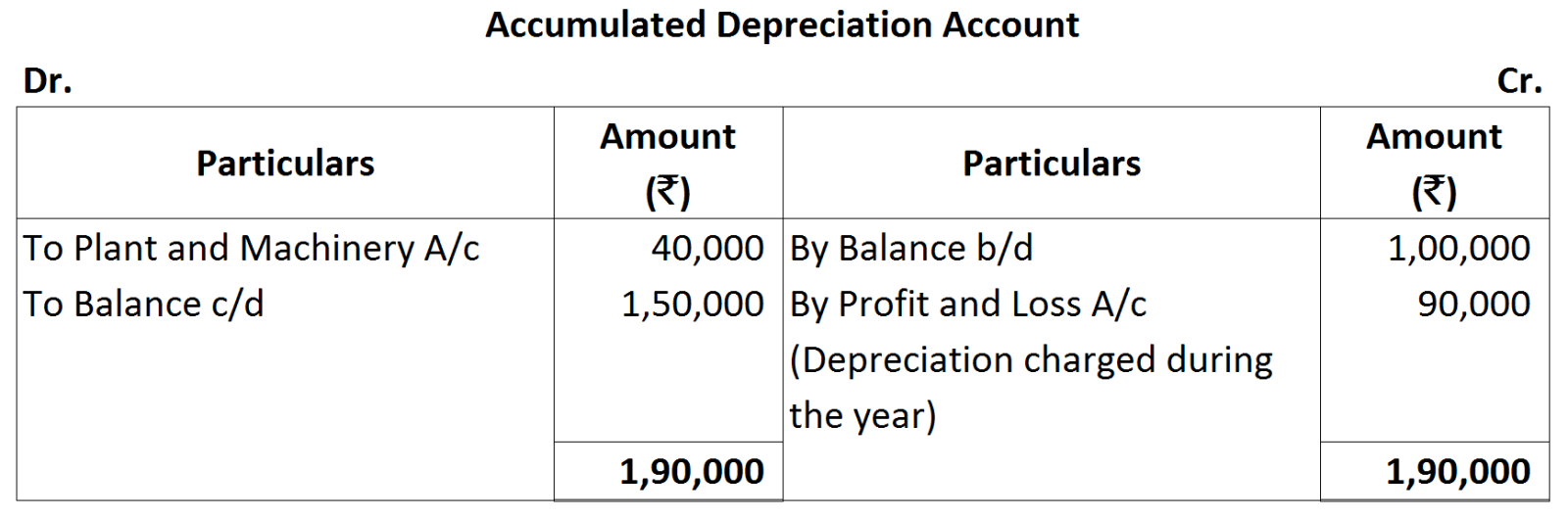

Additional information: during the year, apart of machinery ₹ 50,000 (accumulated depreciation thereon ₹ 40,000) was sold for ₹ 5,000.

Additional information: during the year, apart of machinery ₹ 50,000 (accumulated depreciation thereon ₹ 40,000) was sold for ₹ 5,000.

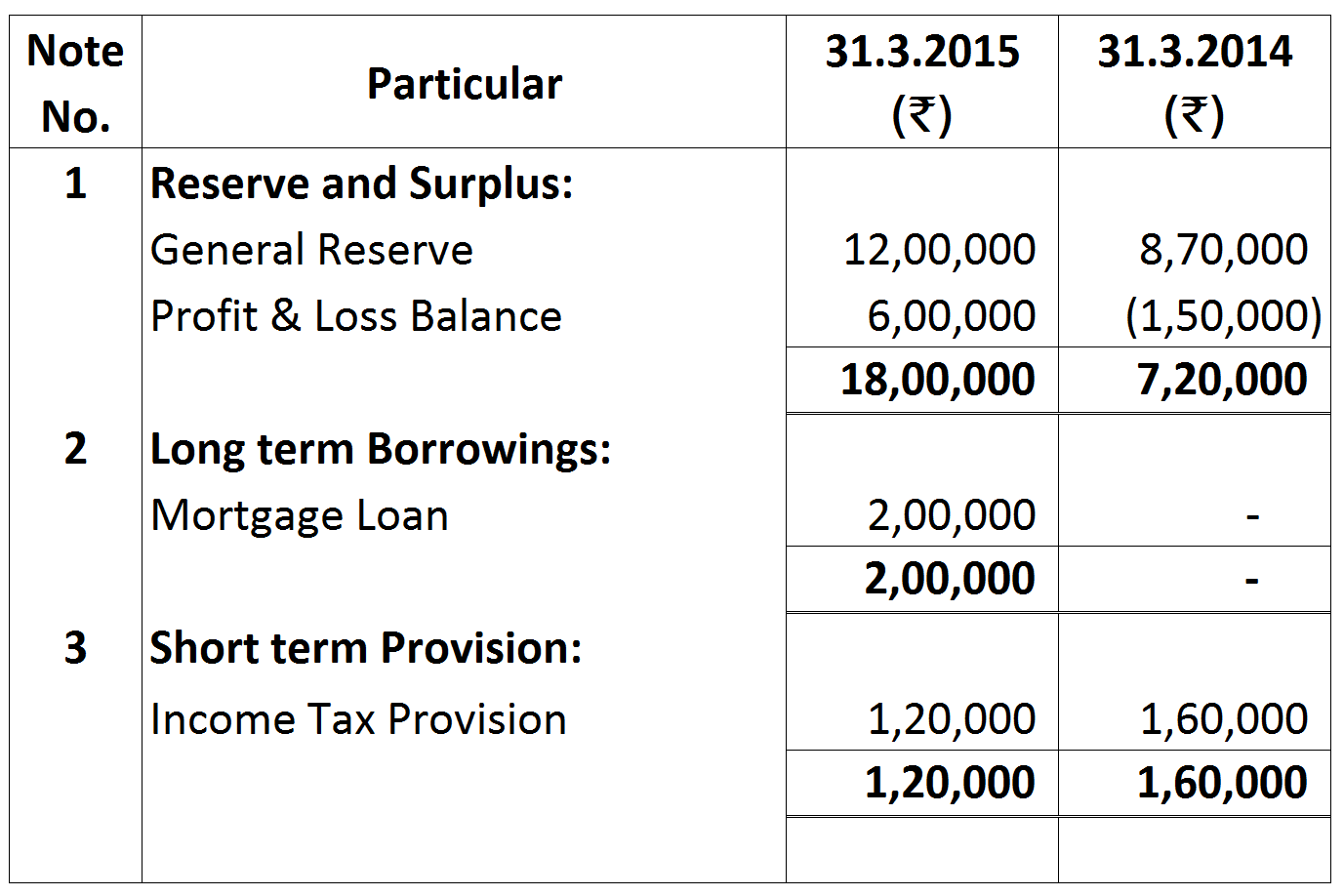

Working Notes:

Working Notes: