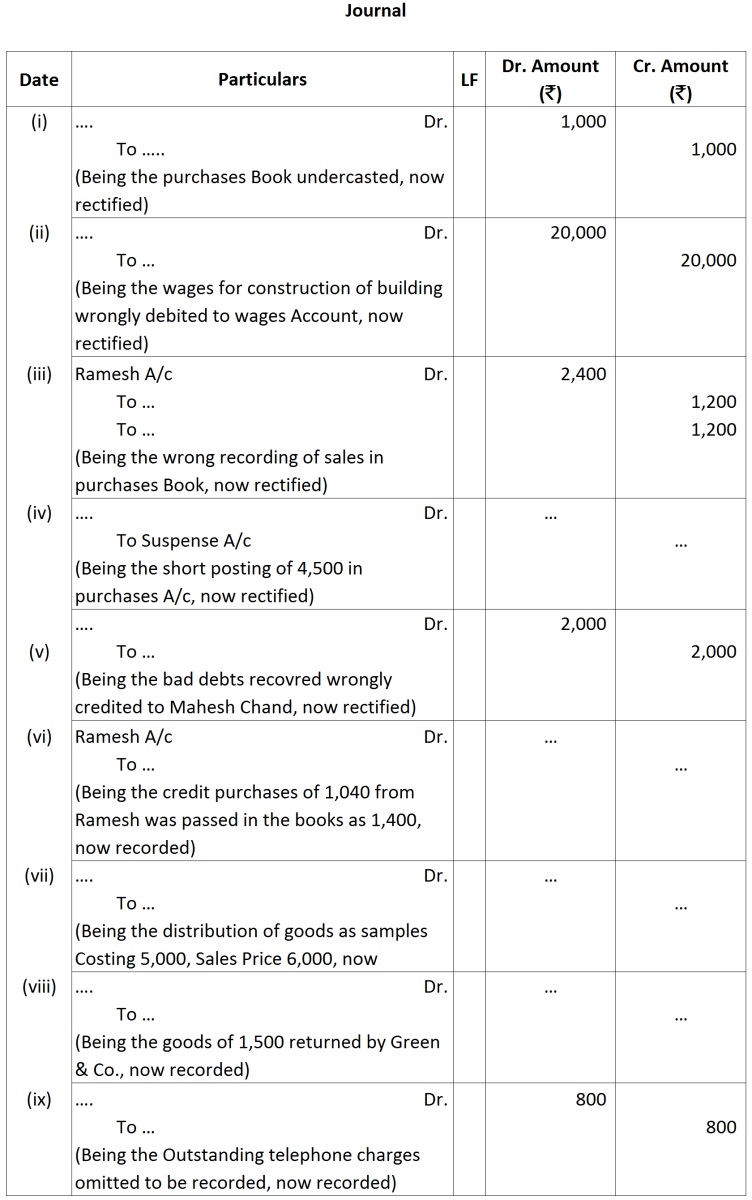

Question

Determine the missing information in the following Rectifying Journal Entries:

Get the step-by-step solution for this question inside the Vidyadip app.

Get the answer in the appGenerate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

|

₹

|

|

|

01

|

Cash in hand

|

17,500

|

|

|

Cash at bank

|

5,000

|

|

03

|

Purchased goods for cash

|

3,000

|

|

05

|

Received cheque from Jasmeet

|

10,000

|

|

08

|

Sold goods for cash

|

7,000

|

|

10

|

Jasmeet’s cheque deposited into bank

|

|

|

12

|

Purchased goods and paid by cheque

|

20,000

|

|

15

|

Paid establishment expenses through bank

|

1,000

|

|

18

|

Cash sales

|

7,000

|

|

20

|

Deposited into bank

|

10,000

|

|

24

|

Paid trade expenses

|

500

|

|

72

|

Received commission by cheque

|

6,000

|

|

29

|

Paid Rent

|

2,000

|

|

30

|

Withdrew cash for personal use

|

1,200

|

|

31

|

Salary paid

|

6,000

|

|

2018

|

|

|

March 1

|

Mahesh Chandra of Bihar purchased goods for ₹ 1,00,000 from Sunil Soren of Jharkhand and sold the same to Deepak Patnaik of Odisha for ₹ 1,50,000.

|

|

March 5

|

Deepak Patnaik sold goods to Suresh Yadav of Odisha for ₹ 1,80,000.

|

|

March 10

|

Suresh Yadav sold goods to Ravi Chakravarti of West Bengal for ₹ 2,50,000.

|

|

March 14

|

Ravi Chakravarti sold goods costing ₹ 2,50,000 to Sanjay Diwedi of West Bengal at a profit of 40% on cost.

|

|

2017

|

|

(₹)

|

|

Jan. 1

|

Petty cashier is given a monthly imprest amount of ₹ 10,000. He spent last month ₹ 9,200 and got the balance from the head cashier today.

|

|

|

Jan. 2

|

Paid for Wages

|

600

|

|

Jan. 3

|

Paid for sundry expenses

|

100

|

|

Jan. 5

|

Paid for stationery

|

700

|

|

Jan. 9

|

Paid for courier charges

|

200

|

|

Jan. 12

|

Stamps purchased

|

750

|

|

Jan. 14

|

Paid wages to casual labour

|

500

|

|

Jan. 16

|

Stationery purchased

|

400

|

|

Jan. 19

|

Paid for general expenses

|

610

|

|

Jan. 20

|

Paid for cartage

|

800

|

|

Jan. 22

|

Paid for advertising

|

900

|

|

Jan. 24

|

Paid for postage

|

400

|

|

Jan. 25

|

Paid for Taxi Fare

|

840

|

|

Jan. 27

|

Paid for entertainment

|

600

|

|

Jan. 29

|

Paid for carriage

|

500

|

|

Jan. 31

|

Paid for petty repairs

|

700

|

|

2017

|

|

|

April 1

|

Received ₹ 10,000 for Petty Cash

|

|

April 3

|

Paid Cartage ₹ 800

|

|

April 4

|

Paid Bus Fare ₹ 400; Speed Post ₹ 200

|

|

April 6

|

Paid for Stationery ₹ 700

|

|

April 7

|

Paid for Courier Services ₹ 300

|

|

April 9

|

Paid for Taxi fare ₹ 800; Wages ₹ 300

|

|

April 10

|

Paid for Wages ₹ 400; Charity ₹ 500

|

|

April 11

|

Paid for Newspaper bill ₹ 600

|

|

April 12

|

Paid for soap ₹ 320; Speed post charges ₹ 300

|

|

April 13

|

Paid for Postage ₹ 780

|

|

April 14

|

Paid for Repairs of Chairs ₹ 500

|

|

April 15

|

Paid for Refreshment to customers ₹ 900

|