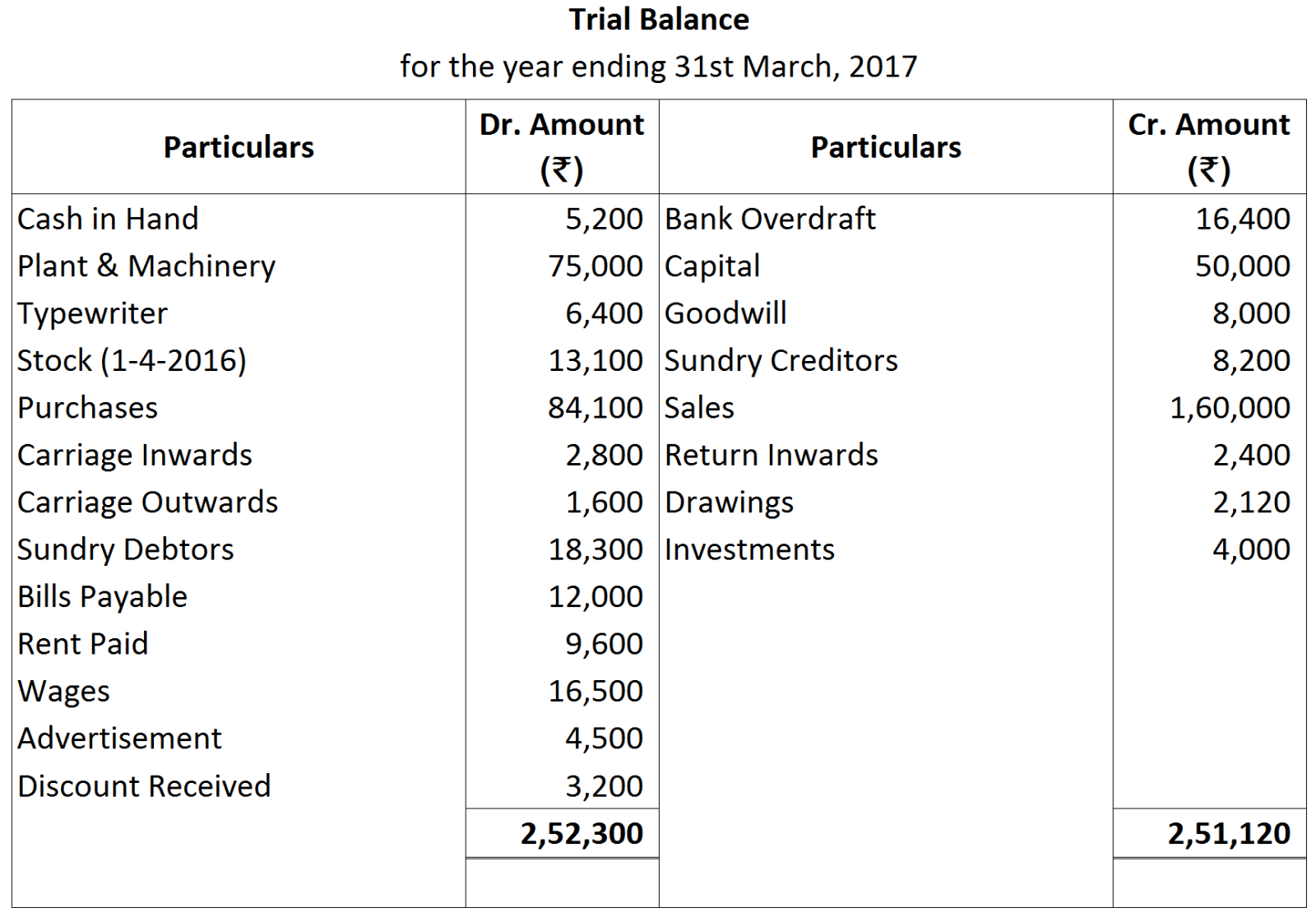

Question

“Every transaction has debit and credit aspects.” Explain.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

2019

|

|

|

June 10

|

Purchased goods from Ravichandran of Madurai of the list price of ₹ 2,00,000 at 25% trade discount at 4% cash discount on purchase price of goods. Paid CGST and SGST @ 9% each. Paid the entire amount by cheque on the same date. |

|

June 25

|

Sold goods to Ramalingam of Erode of the list price of ₹ 3,75,000 at 20% trade discount and 2% cash discount on sale price. Charged CGST and SGST @ 9% each. Full amount was received by cheque on the same date.

|

|

|

|

₹

|

|

(i)

|

Bank Balance as per Pass Book.

|

10,000

|

|

(ii)

|

Cheque deposited into bank but no entry was passed in Cash Book.

|

500

|

|

(iii)

|

Cheque received and entered in Cash Book but not sent to bank.

|

1,200

|

|

(iv)

|

Insurance premium paid directly by the bank.

|

800

|

|

(v)

|

Bank charges entered twice in the Cash Book.

|

20

|

|

(vi)

|

Cheque received entered twice in Cash Book.

|

1,000

|

|

(vii)

|

Bill discounted dishonoured not recorded in the cash book.

|

5,000

|

|

2017

|

|

|

March 1

|

Sold to Chandra Light House

|

| 50 Tubelights @ ₹ 60 each Less: 20% | |

| 20 Heaters @ ₹120 each Less: 25% | |

|

March 5

|

Purchased from Charat Ram Electric Co.

|

|

March 10

|

25 Table Fans @ ₹ 600 each |

| 20 Ceiling Fans @ ₹800 each | |

|

Chaudhary & Sons purchased from us

80 Dozen Bulbs @ ₹ 90 per Dozen

|

|

|

March 12

|

Purchased from Ram Lal & Sons one Typewriter for ₹ 6,000 on credit, for office use.

|

|

March 16

|

Sri Ram & Sons sold to us:

|

| 10 Electric Irons @ ₹ 180 each less: 10% | |

|

March 20

|

Chandra Light House returned

|

|

March 22

|

5 Tubelights sold on March 1. |

|

Sold goods to Jai Bhagwan & Co. for cash ₹ 10,000.

|

|

|

March 25

|

Returned to Sri Ram & Sons 2 Electric Irons purchased on March 16.

|