Share capital is the capital that is built up by the company by issuing shares in the market. Share capital consist of capital that is made up of Equity shares and Preference shares.

Share capital can be classified as-

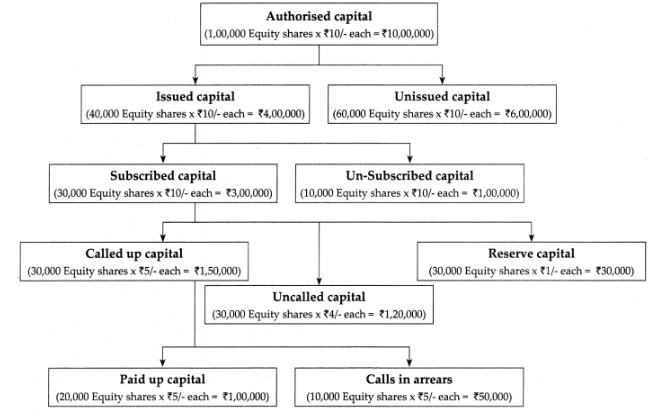

(i) Authorised or Nominal or Registered Capital

- The Authorized capital is the maximum amount of capital that a company can raise through the issue of shares to the shareholders.

- The Authorized capital of a company is also called as the Registered capital or Nominal Capital.

- Authorized capital is the maximum capital that is authorized by the company’s Memorandum of Association.

- The Authorized capital is mentioned in the Memorandum of Association of the company under the heading ‘capital clause’ and the company pays stamp duty on this amount at the time of incorporation.

- Authorized capital is also called as ‘Nominal Capital’ as usually a company never issues the entire Authorized Capital.

- A company can increase its Authorized Capital by altering its Memorandum of Association.

- The maximum limit of authorized capital is registered with the registrar of the companies.

- Example of Authorized Capital: XYZ Ltd. Company has an authorized capital of ₹ 10,00,000, then it can issue shares worth up to ₹ 10,00,000 to its shareholders and cannot issue anything beyond it.

(ii) Issued and Unissued capital:

- Issued capital is that portion of authorized shares capital that had been raised by issuing shares to the general public.

- These are the shares that the company offers to prospective investors for a subscription.

- The issued capital of a company may be equal to or less than the Authorized Capital of incorporation.

- The balance part of Authorized Capital which is not offered to the public for subscription is called ‘unissued capital’.

- Unissued capital is that capital which a Company is authorized to issue but has not issued as shares.

- Unissued capital is the balance part of Authorised capital which is not offered to the public.

- Example of Issued and Unissued Capital: XYZ Ltd Company can have issued Capital of ₹ 4,00,000 divided into 40,000

- Equity Shares at Face Value of ₹ 10/- each and the Unissued Capital 6,00,000 divided into 60,000 equity shares of ₹ 10/- each.

(iii) Subscribed and Unsubscribed Capital:

- Subscribed share capital is that part of issued share capital for which a company has positively received a subscription from the investor.

- It is a part of Issued Capital that has been subscribed by investors or purchased by the general public.

- The subscribed capital may be equal to or less than the issued capital.

- The part of the Issued Capital which is not subscribed by the investors is called as ‘Unsubscribed Capital’.

- Example of Issued and Unissued capital: If XYZ Ltd company has issued capital ₹ 4,00,000 i.e., it has issued 40,000 equity shares of ₹ 10 each and company has received subscription for 30,000 shares i.e., for 30,000 equity shares of ₹ 10/- each then its subscribed capital is ₹ 3,00,000 and unsubscribed capital will be ₹ 1,00,000 divided into 10,000 Equity shares of ₹ 10/- each.

(iv) Called up and Uncalled capital and Reserve capital:

- Called up share capital is that part of share capital that has been called by the company for payment from shareholders.

- The company collects the full value of shares in installments and each installment is called a ‘call’.

- Uncalled Capital is that part of subscribed capital that is not demanded from the shareholders.

- A company can decide to keep aside a part of its uncalled capital to be called up only at the time of winding up of a company to meet its financial requirements. Which is called a Reserve Capital.

Example of call up, uncalled and Reserve Capital.

If XYZ Ltd company is to subscribed capital is ₹ 3,00,000 i.e., 30,000 equity shares of face value of ₹ 10/- each. Out of which company made first call of ₹ 5/- per share, so company called up capital will be ₹ 1,50,000 (30,000 Equity shares × ₹ 5/- each = ₹ 1,50,000)

If the company decides to keep ₹ 1/- per share as capital to be collected at the time of the winding-up, the Reserve Capital will be 30,000 (30,000 equity shares of ₹ 10 each.)

Uncalled Capital will be ₹ 1,20,000 (30,000 equity shares were 4 per share which will be called up in the future.)

(v) Paid-up capital and calls in Arrears:

- Paid-up capital is the amount of money a company has received from shareholders in exchange for shares.

- It is the total amount of money paid up by the shareholders when the company has called up or demanded them to pay.

- The paid-up capital can be equal to or less than the authorized capital.

- Unpaid capital means any uncalled or unpaid share capital. The amount not paid to shareholders is also called as calls in Arrears.

- Every shareholder has to pay calls as and when the company demands, failure to pay the calls may lead to future forfeiture of shares (cancellation of shares).

Example of paid up capital and calls in Arrears.

‘XYZ’ Ltd Company has made a call of ₹ 5/- per share on 30,000 equity shares, so if all the shareholder have paid the calls, then paid-up capital will be ₹ 1,50,000 (30,000 equity shares of ₹ 5/- per share). But if 10,000 Equity Shareholders have not paid calls then the paid-up capital will be ₹ 1,00,000 (20,000 Equity Shares × ₹ 5/- per share) and calls in Arrears will be ₹ 50,000 (10,000 Equity Shares × ₹ 5/- per share).