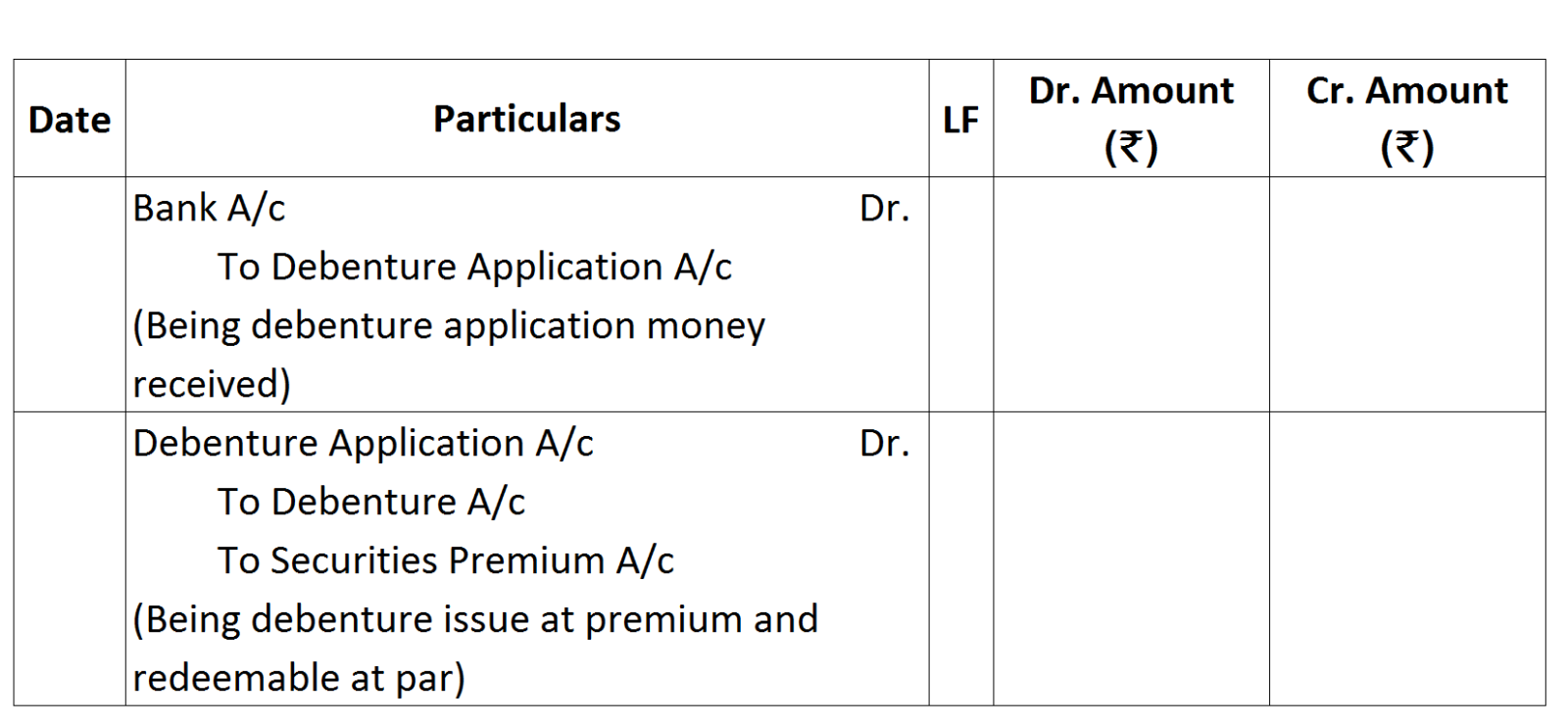

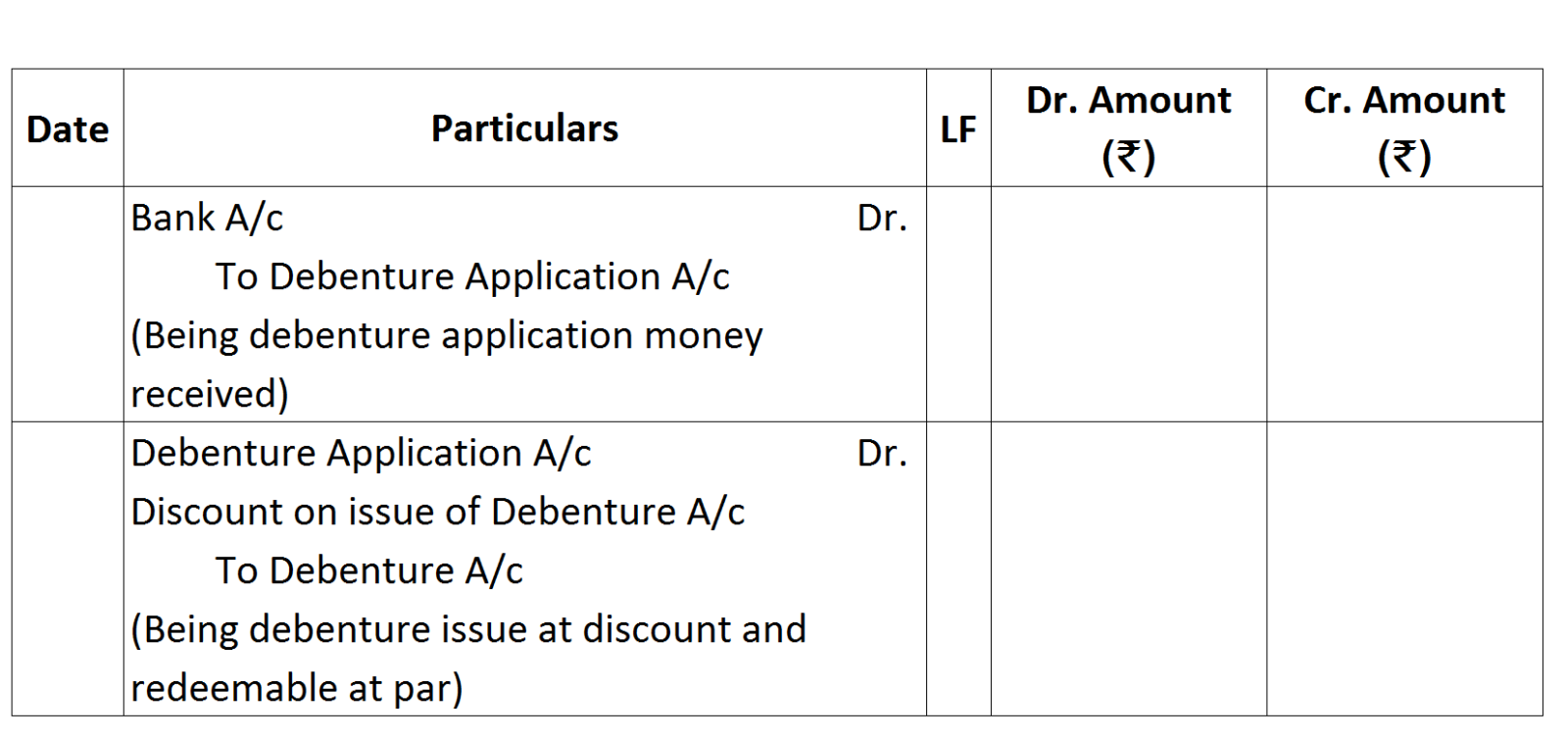

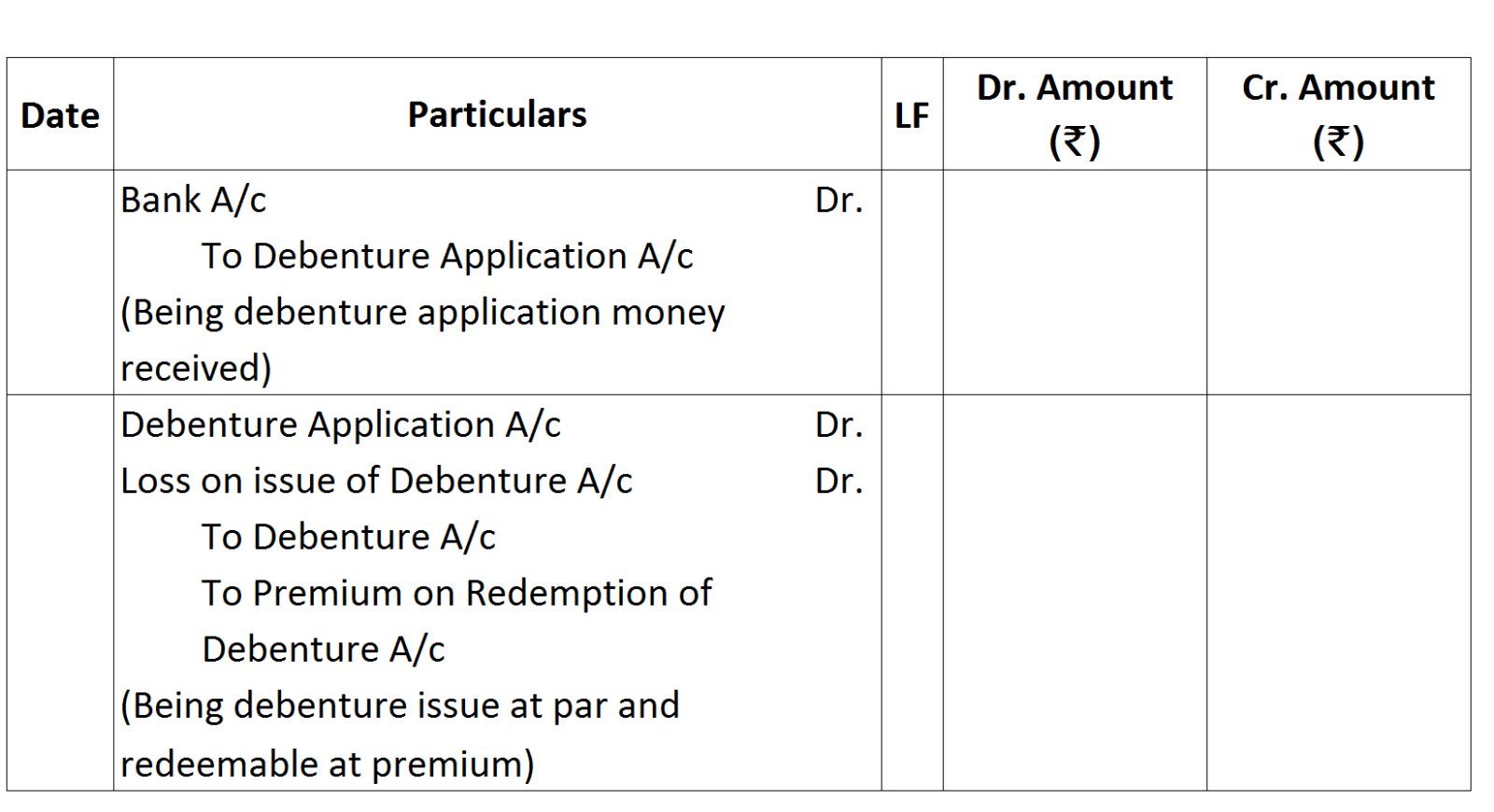

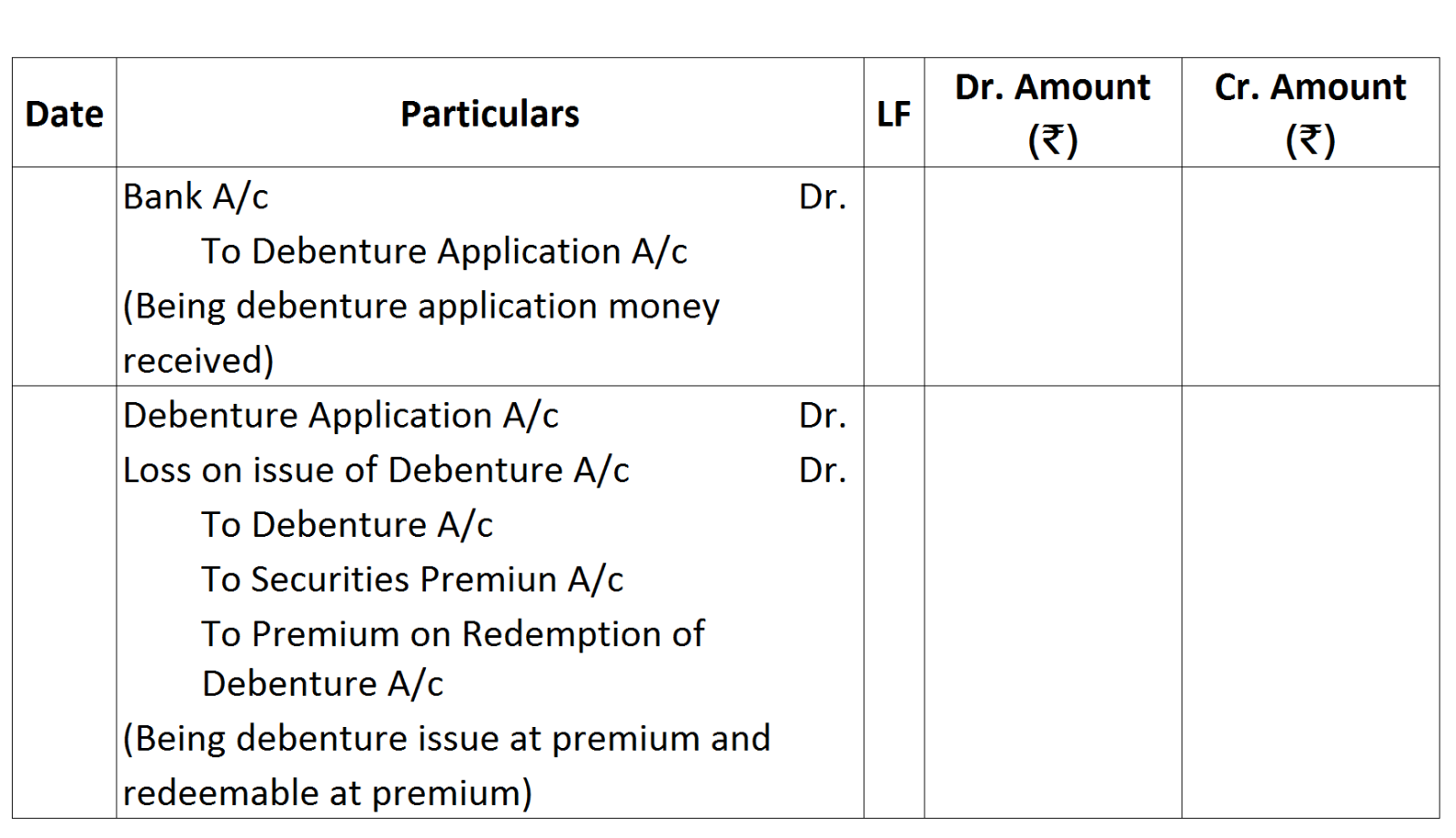

Question

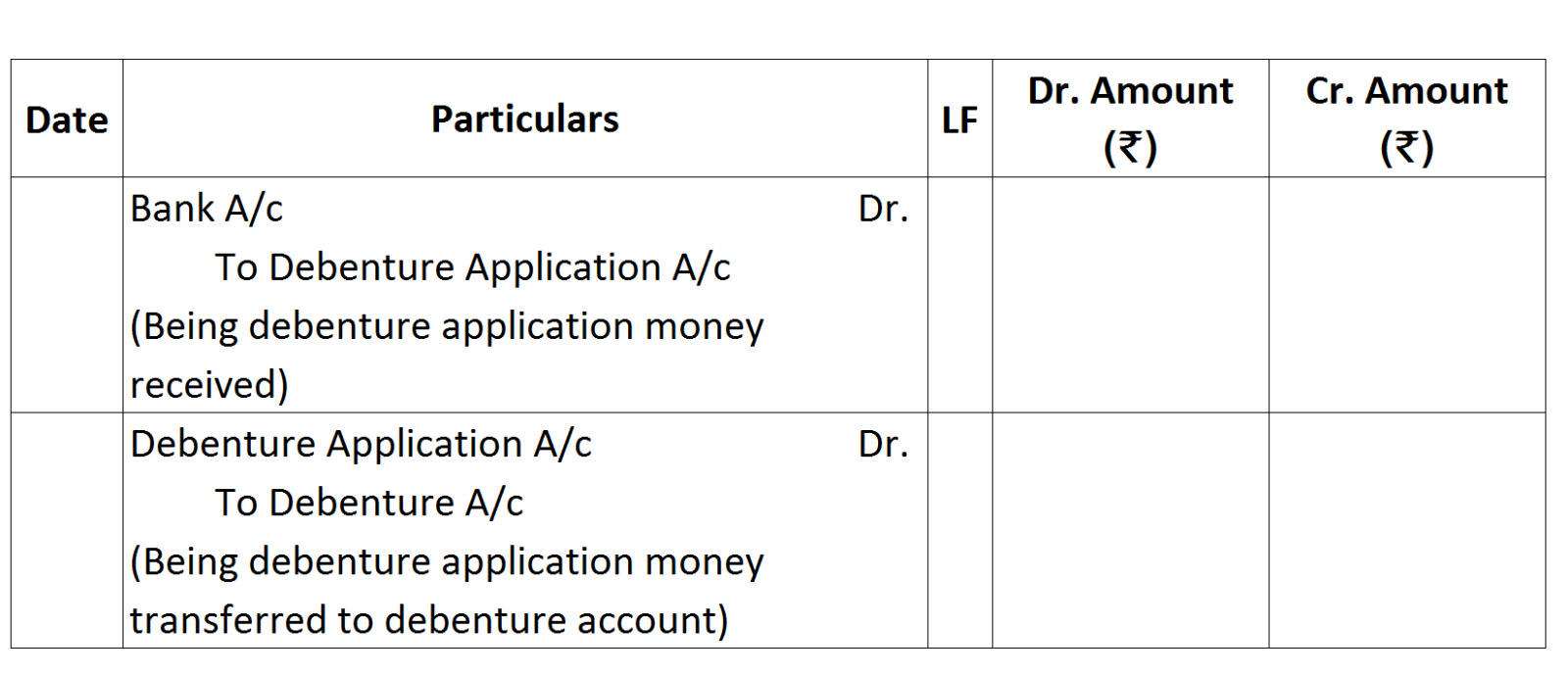

Explain the different terms for the issue of debentures with reference to their redemption.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

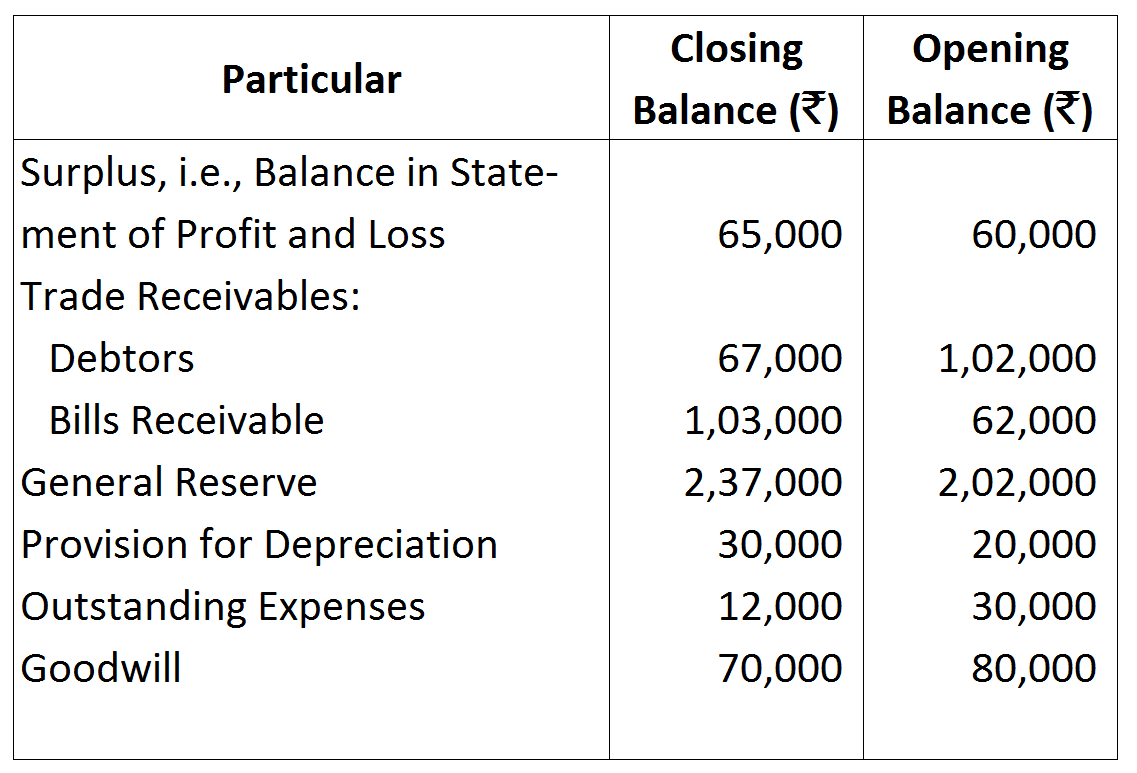

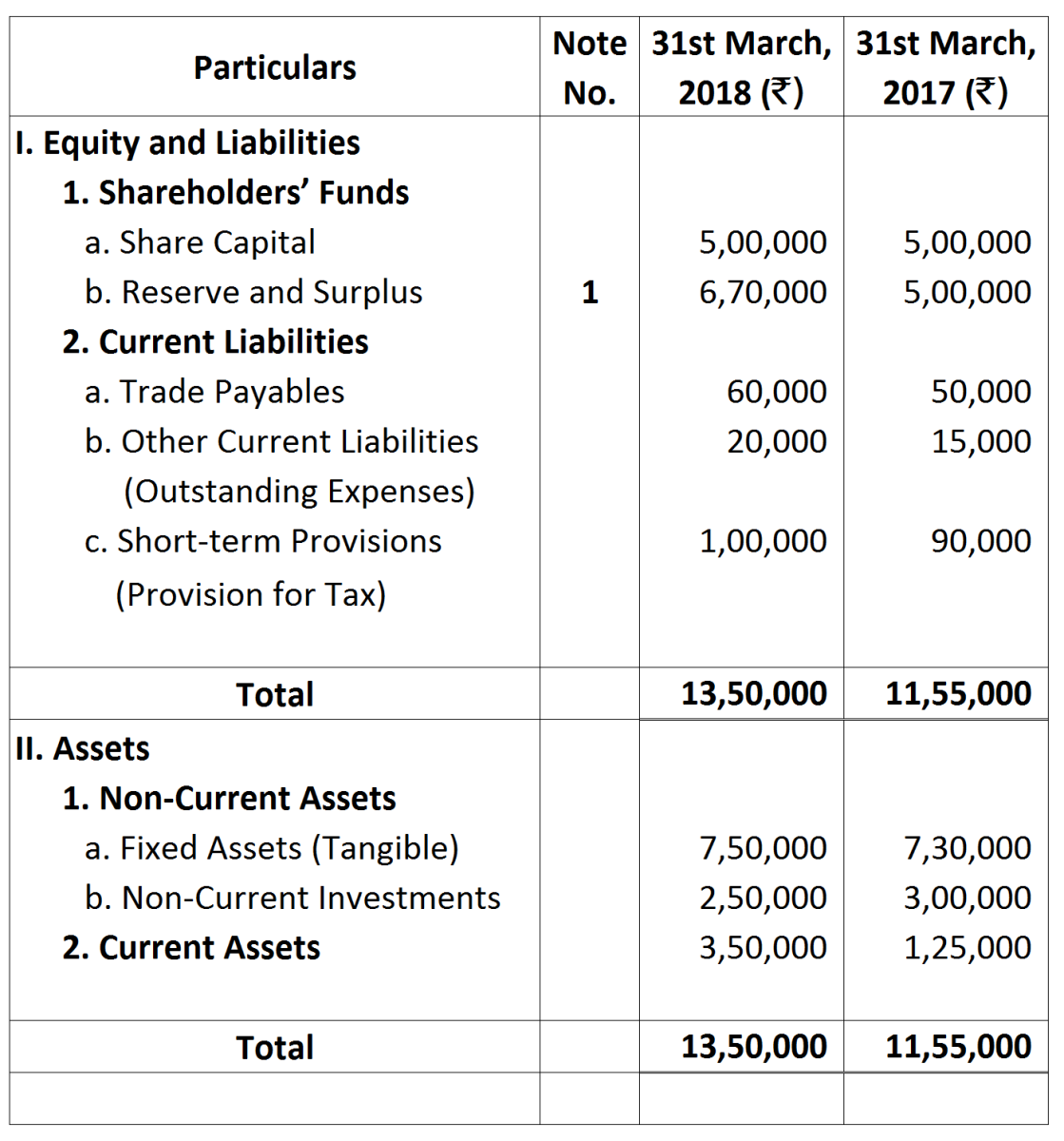

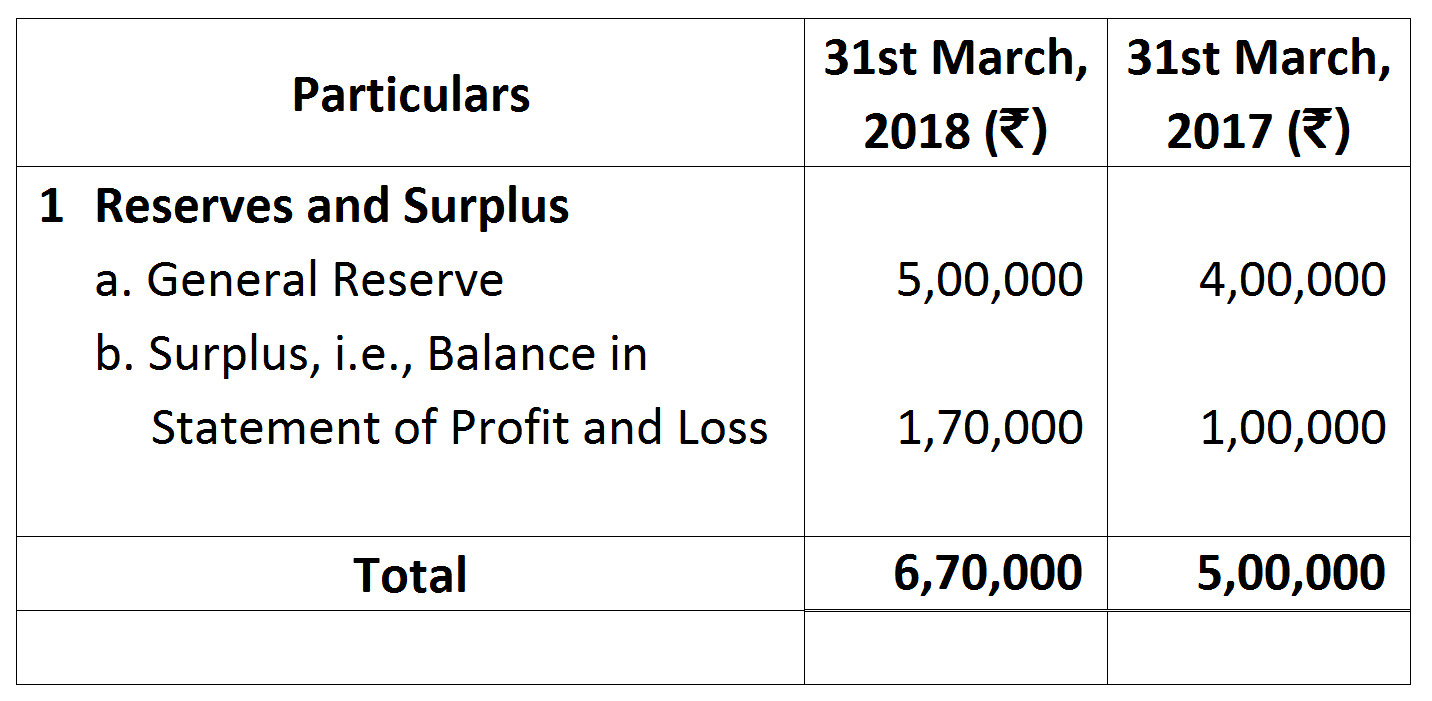

|

Particulars

|

31st March, 2018 ₹

|

31st March, 2017 ₹

|

|

Inventories

Trade Receivables

Prepaid Expenses

Trade Payables

Provision for Tax

|

1,15,000

1,50,000

20,000

1,10,000

20,000

|

1,25,000

1,10,000

6,000

80,000

15,000

|

Notes to Account:

Notes to Account: Additional Information: Depreciation for the year was ₹ 75,000.

Additional Information: Depreciation for the year was ₹ 75,000.