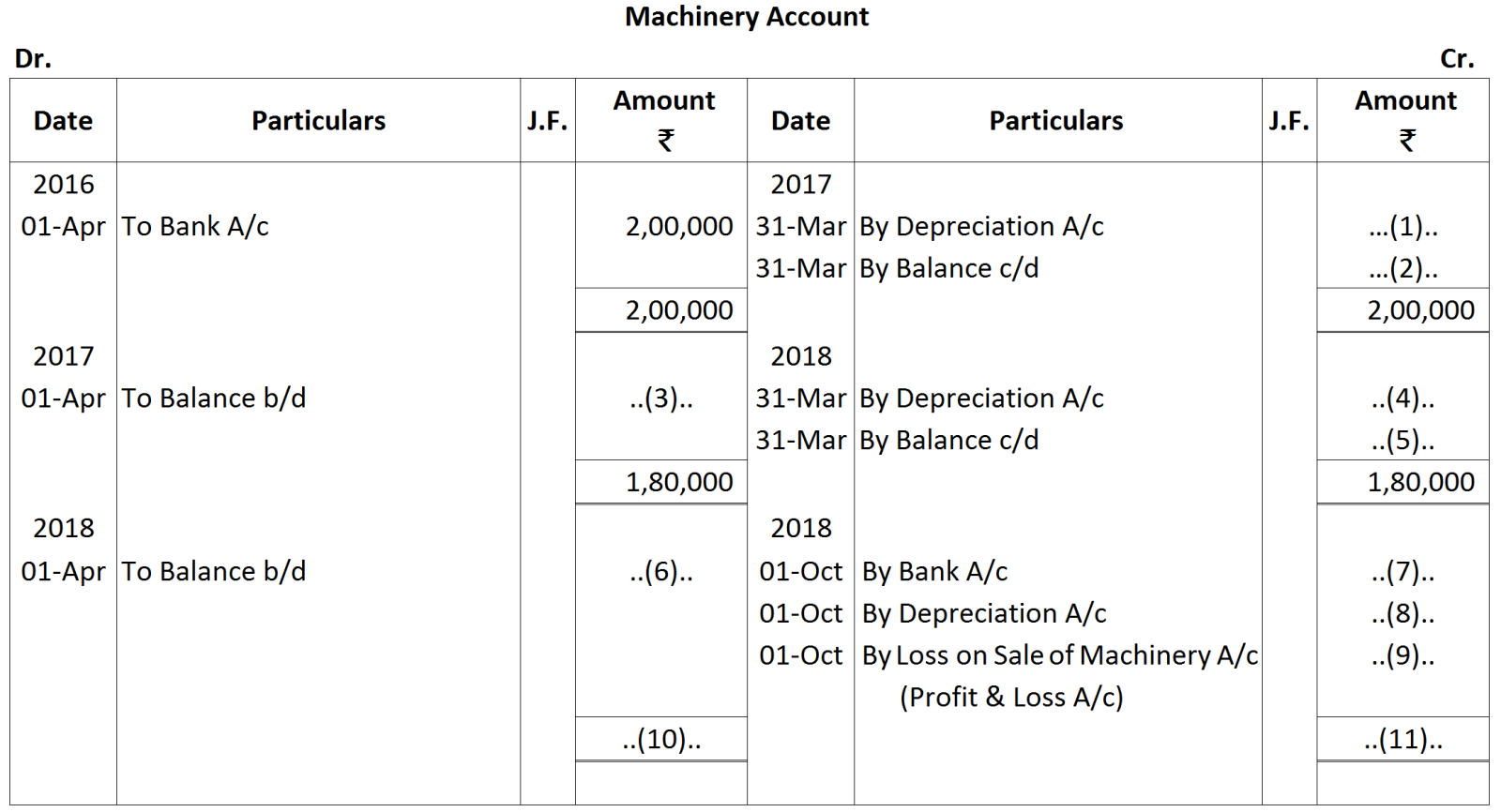

Model Paper 5 — Account STD 11 Commerce — Question

CBSE BoardEnglish MediumSTD 11 CommerceAccountModel Paper 54 Marks

Question

Explain the need for drawing up the special purpose books.

✓

Answer

Special purpose books are beneficial in: i. Accuracy: As each journal is managed by a different accountant having specific expertise, it improves accuracy and reduces defects. ii. Efficiency: Increases efficiency by dividing the workload. iii. Concise Descriptions: The journal describes the purpose of recording. For example, a record in the purchase journal will be understood by default that it is a purchase-related transaction. iv. Minimal Posting: Reduces the volume of posting as totals can be done periodically. v. Fraud Prevention: As the recording of different journals are assigned to a different individual, fraud prevention is prevented. vi. Faster process: As multiple books are handled by multiple accountants, the recording work moves faster.

Need a full question paper?

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.