Question

Explain the process of preparing income statement and balance sheet.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

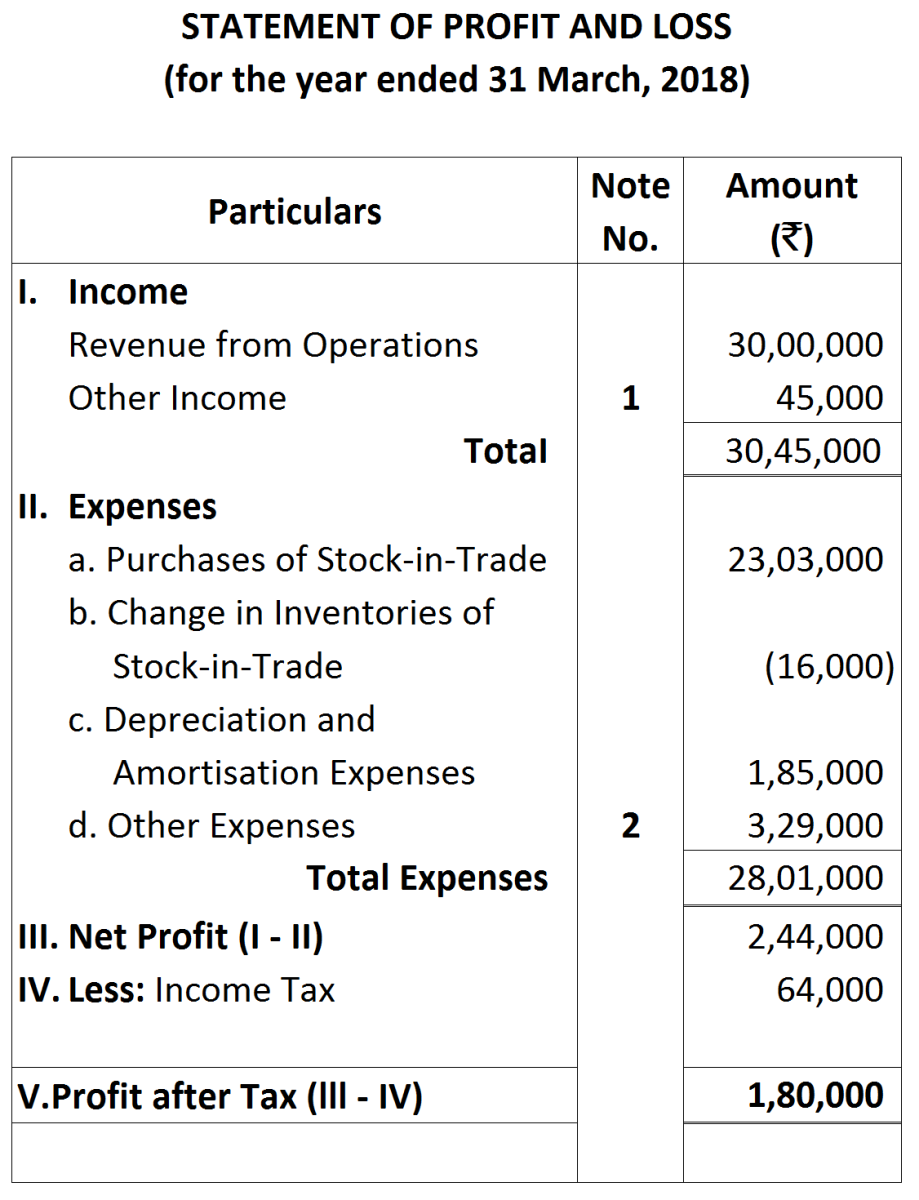

Notes to Account:

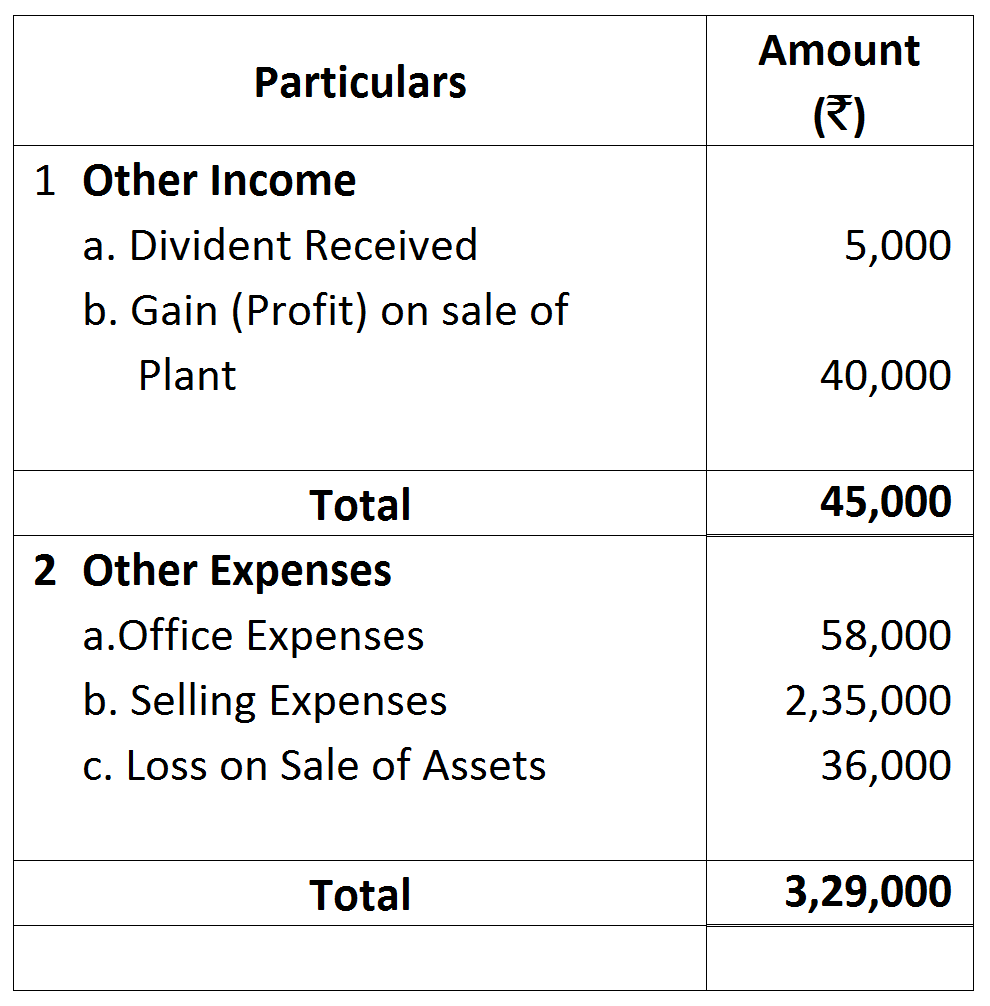

Notes to Account:

|

Other Informatiom:

|

Balance as on 31st march, 2018 (₹)

|

Balance as on 31st march, 2017 (₹)

|

|

Trade paybles

|

2,78,000

|

2,50,000

|

|

Trade receivables

|

4,52,000

|

4,15,000

|

|

inventories

|

3,00,000

|

2,84,000

|

|

Office expenses Outstanding.

|

-

|

5,000

|

|

Selling expenses Outstanding.

|

25,000

|

22,000

|