Question

Explain the types of Reserves.

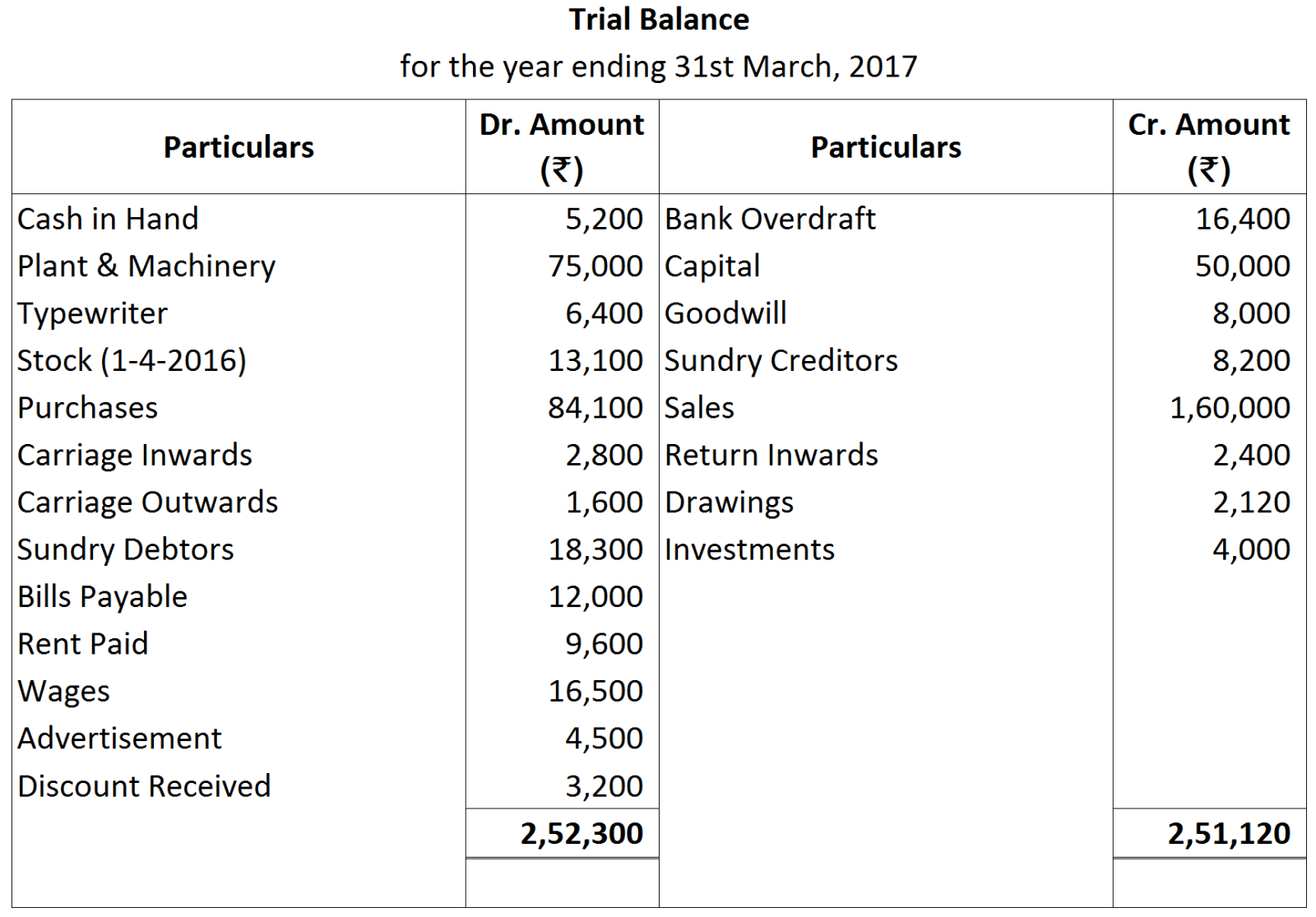

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

|

|

₹

|

|

(i)

|

Cheques issued but not yet presented for payment.

|

6,000

|

|

(ii)

|

Cheques deposited in the bank but not collected.

|

9,000

|

|

(iii)

|

Bank paid insurance premium.

|

5,000

|

|

(iv)

|

Bank charges.

|

300

|

|

(v)

|

Directly deposited by a customer.

|

8,000

|

|

(vi)

|

Interest on investment collected by bank.

|

2,000

|

|

(vii)

|

Cash discount allowed of ₹ 200 was recorded on the debit side of the Bank column.

|

|

|

2017

|

|

|

Nov. 3

|

Purchased goods from Sachdeva Furniture Store, New Delhi :

|

|

50 Chairs @ ₹ 2,000 each

|

|

|

5 Tables @ ₹ 10,000 each

|

|

|

Nov. 10

|

Purchased furniture from Mahadeva & Co., Jaipur (Rajasthan) valued ₹ 2,00,000, less $12\frac{1}{2}\%$ Trade Discount

|

|

Nov. 18

|

Purchased furniture from Fashion Furniture House, Chandigarh of the list price of ₹ 2,50,000, less 15%

|

|

Nov. 20

|

Purchased from India Furniture House, New Delhi:

|

|

100 Chairs @ ₹ 1,800 each

|

|

|

Nov. 25

|

Purchased from Mohan Lal & Sons furniture of the value of ₹ 20,000 for cash

|

|

2017

|

|

|

Jan. 10

|

Purchased goods from Ghanshyam of the list price of ₹ 50,000 at 15% trade discount.

|

|

Jan. 13

|

Returned goods to Ghanshyam of the list price of ₹ 2,000

|

|

Jan. 15

|

Paid cash to Ghanshyam ₹ 40,000 in full settlement of his account.

|

|

Jan. 20

|

Purchased goods from Raghu of the list price of ₹ 60,000 at 10% trade discount.

|

|

Jan. 22

|

Returned goods to Raghu of the list price of ₹ 5,000

|

|

Jan. 25

|

Paid cash to Raghu ₹ 49,000 in full settlement of his Account.

|

|

|

₹

|

|

Machinery A/c

|

5,00,000

|

|

Provision for Depreciation A/c

|

2,25,000

|