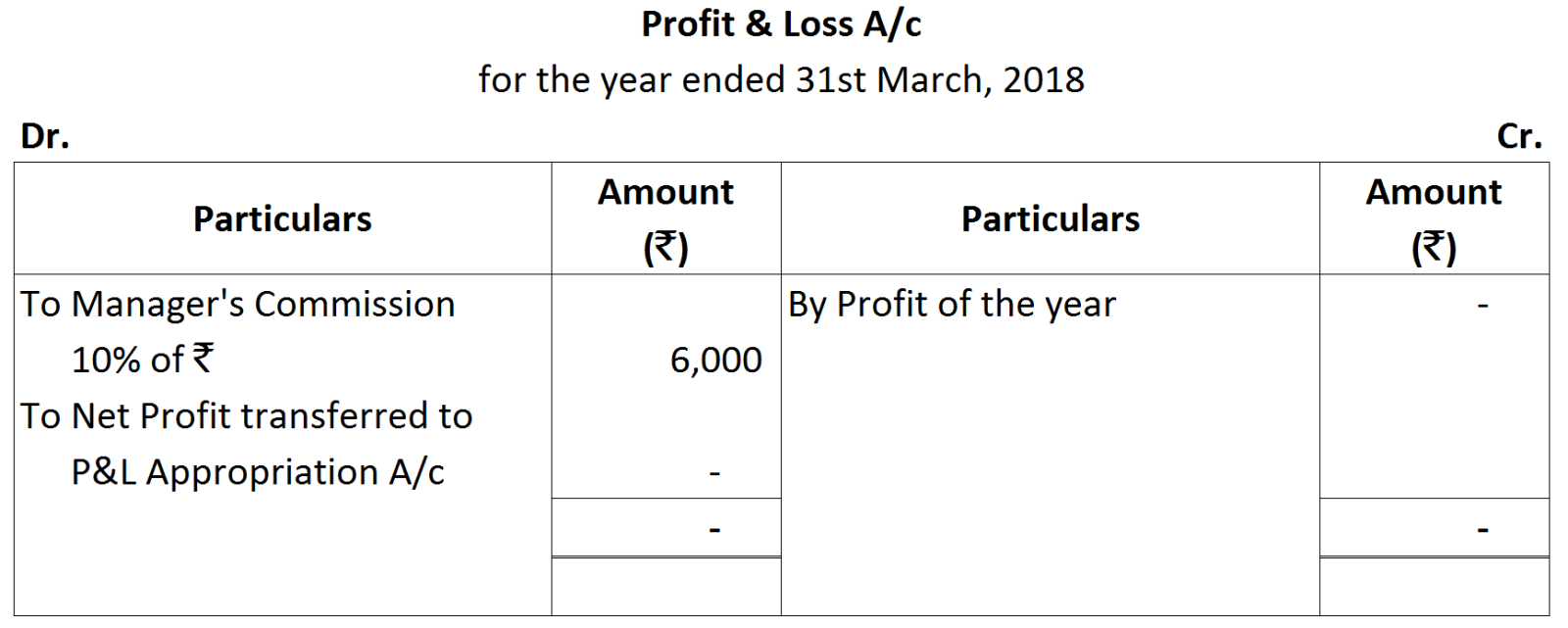

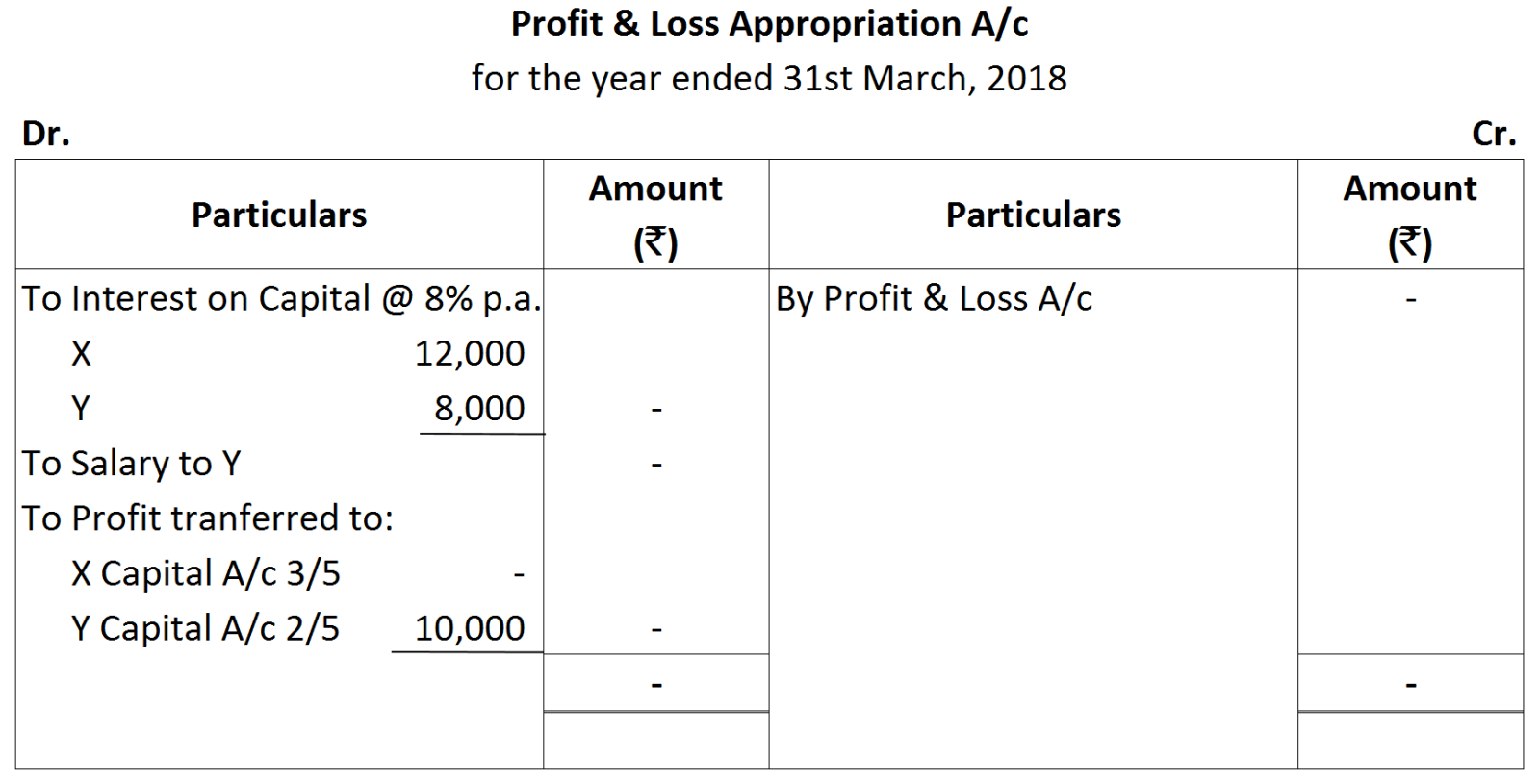

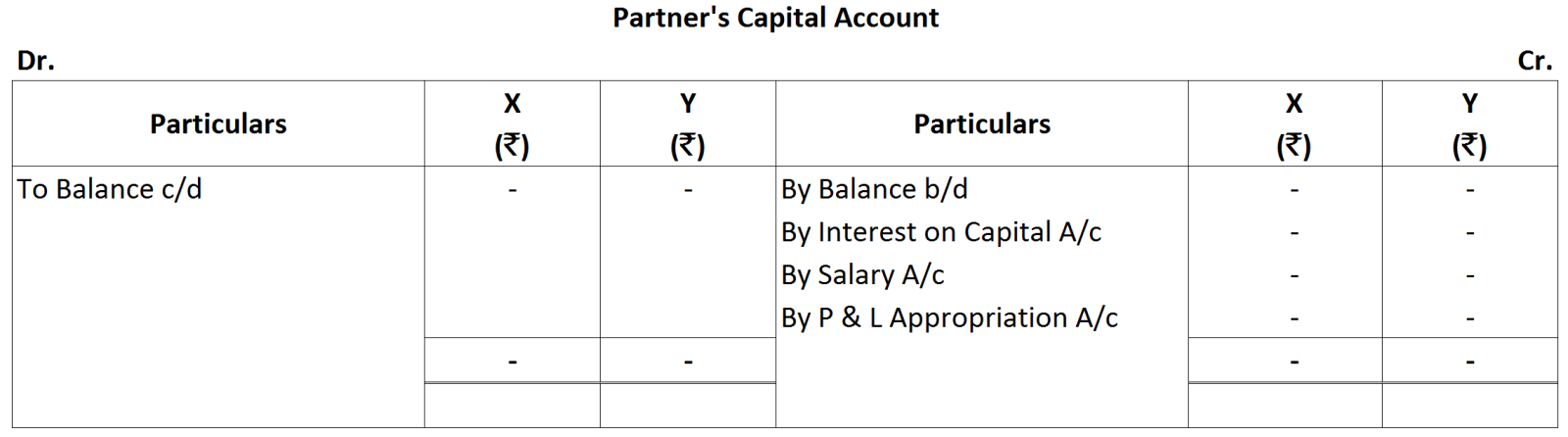

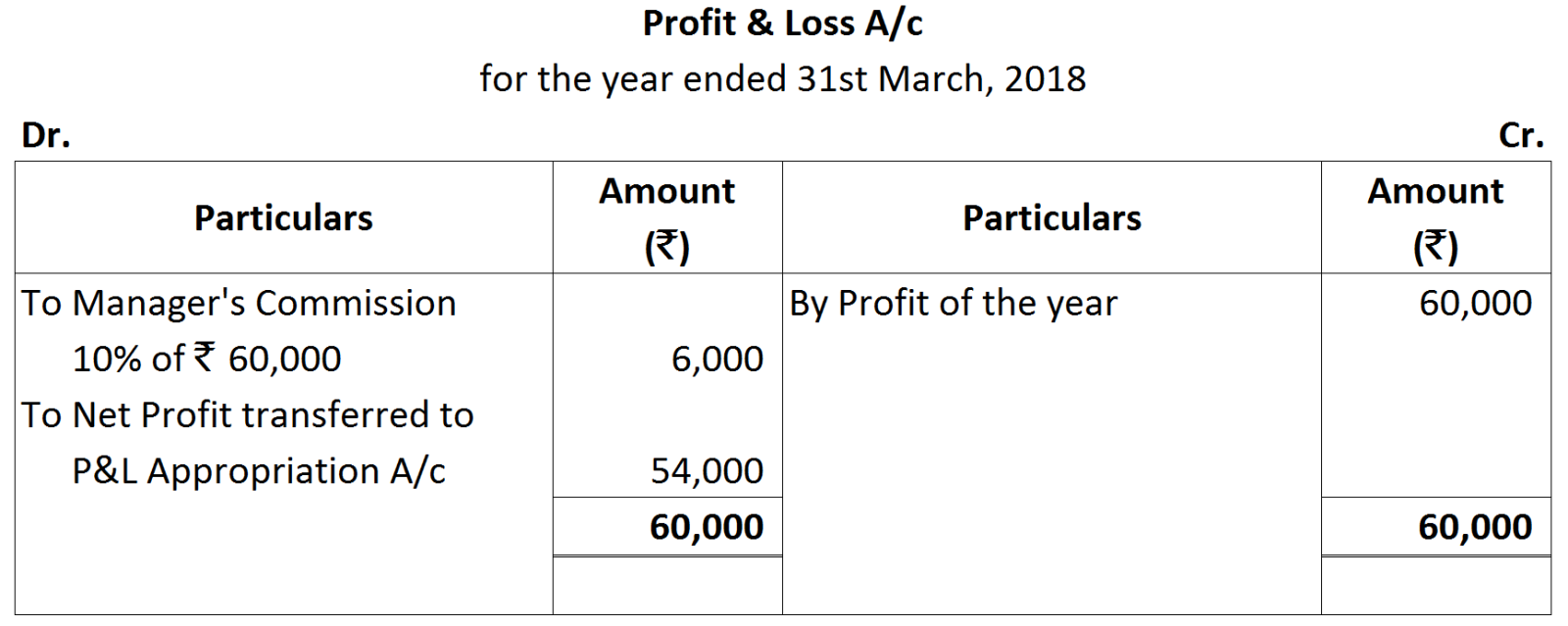

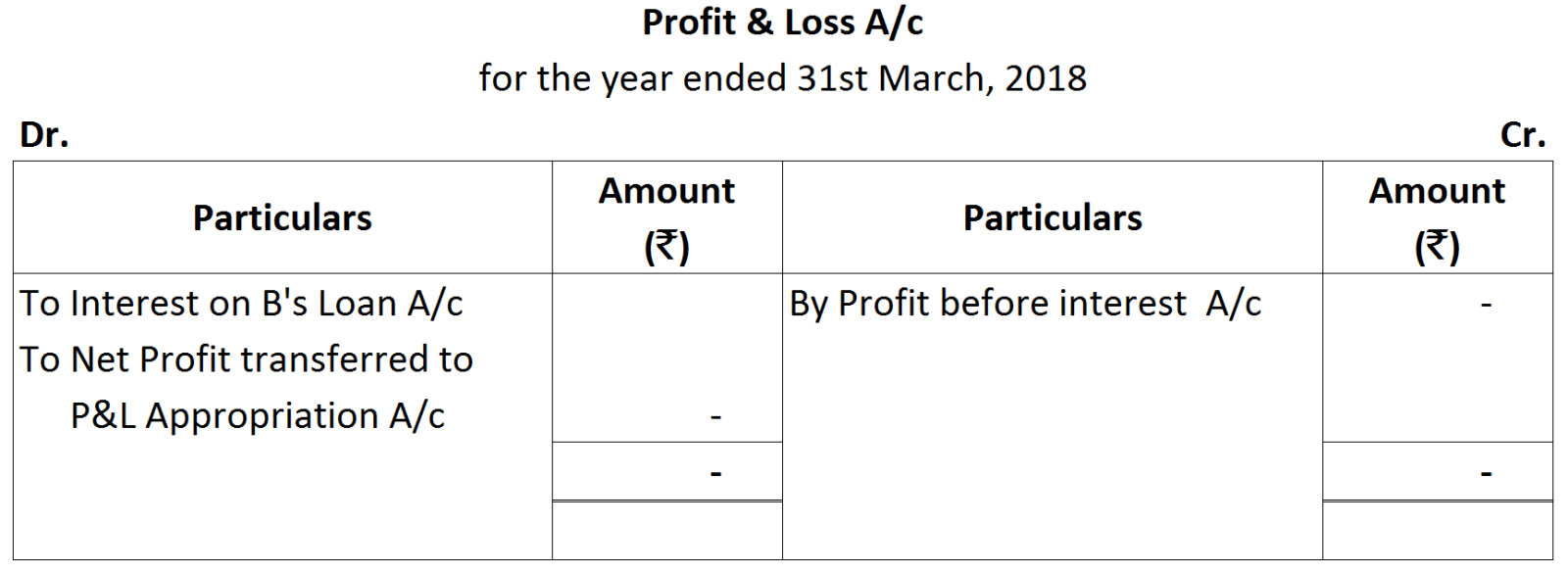

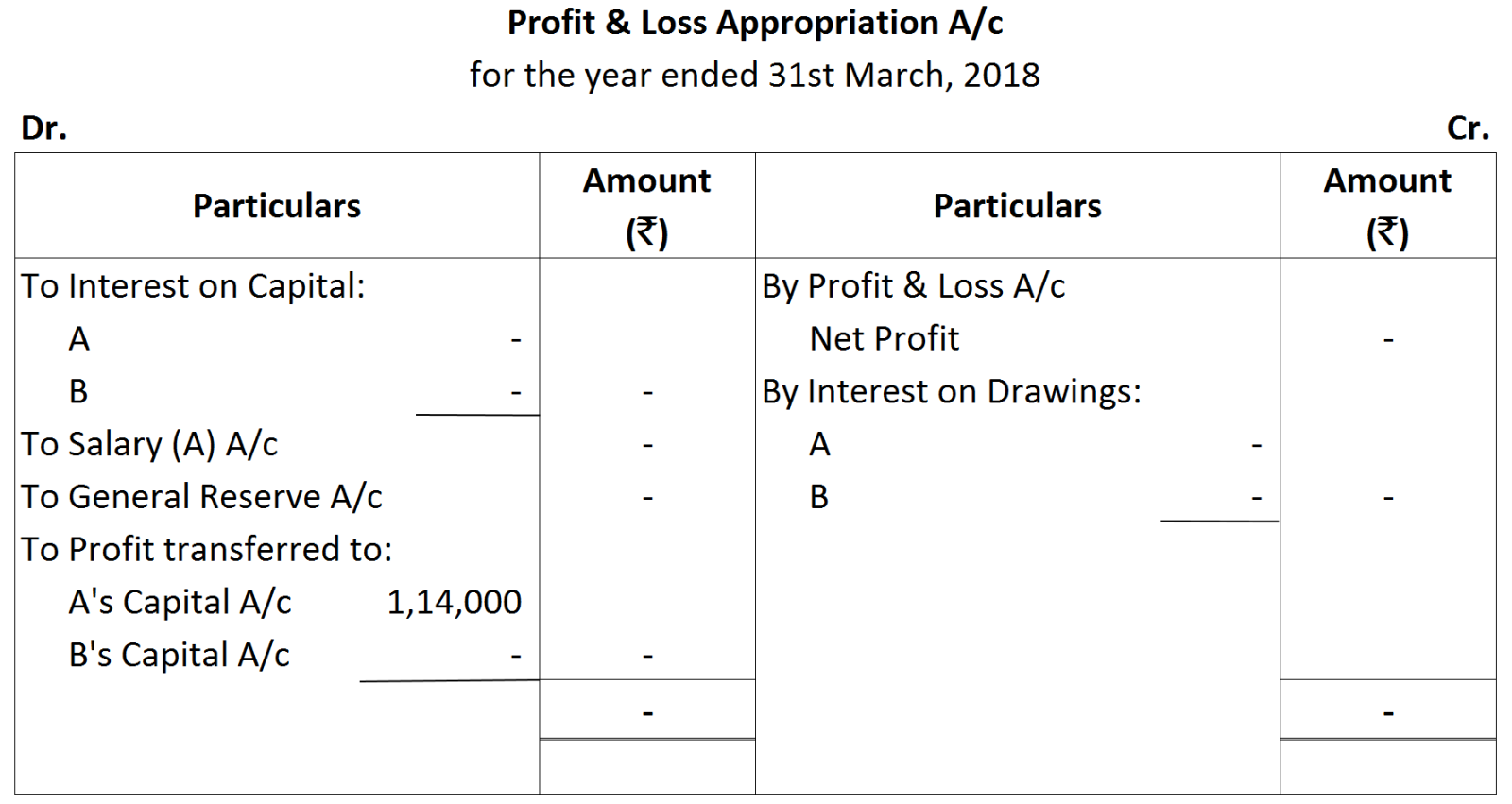

Question

Fill in the missing figures in the following Accounts:

Working Notes:

Working Notes:Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

| ₹ | |

|

1st June

|

1,000

|

|

1st August

|

750

|

|

1st October

|

1,250

|

|

1st December

|

500

|

|

1st February

|

500

|