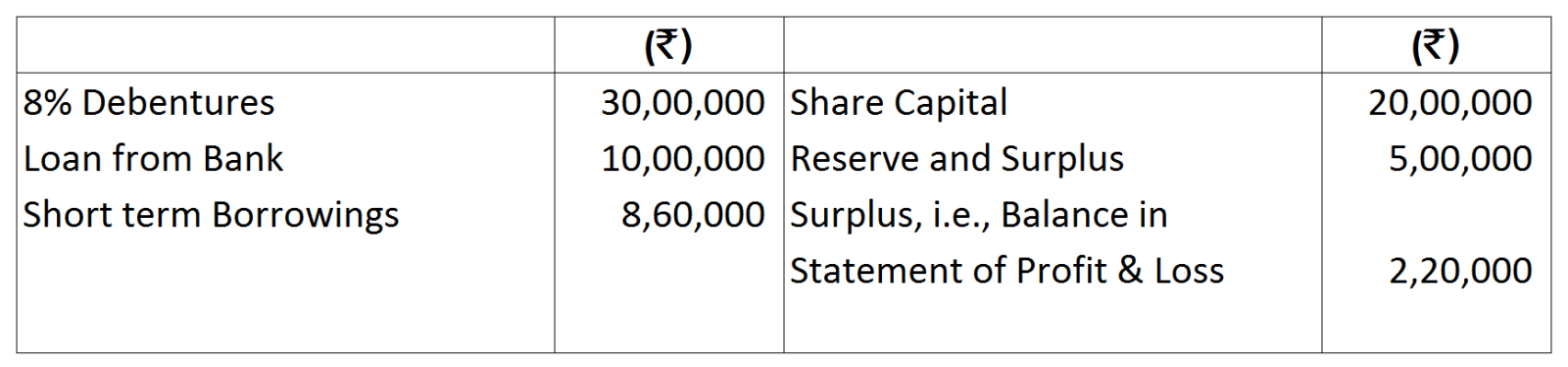

Question

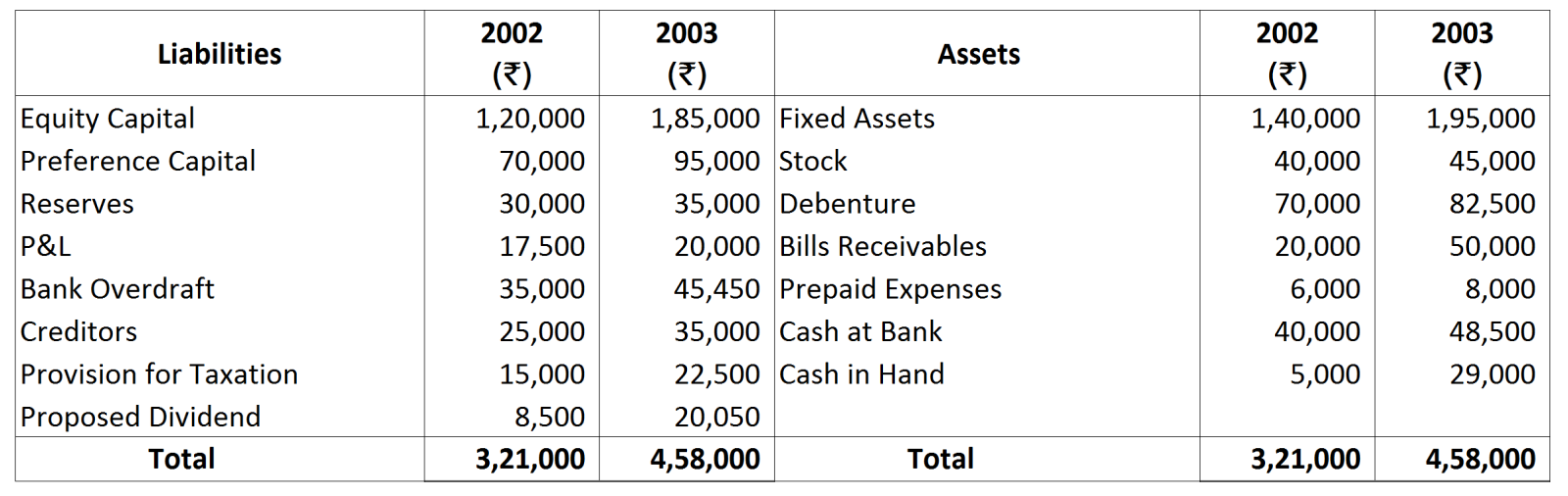

From the following information, calculate Total Assets to Debt Ratio:

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

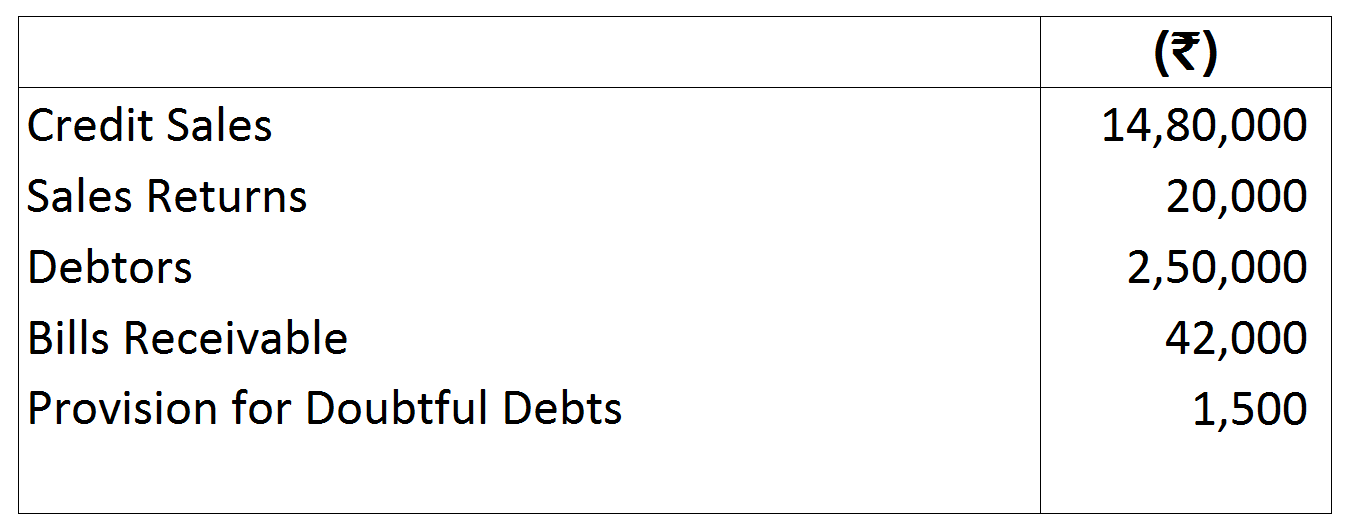

From the following information, calculate Net Profit before Tax and Extraordinary Items:

|

₹

|

|

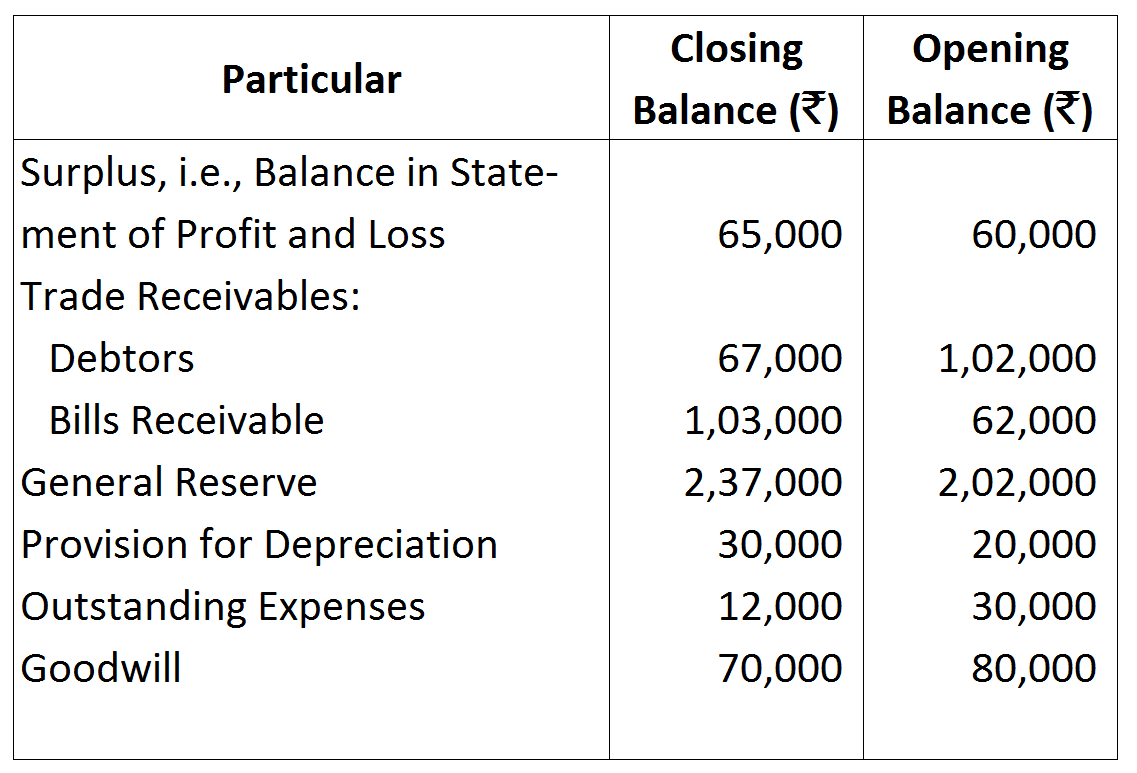

Surplus, i.e., Balance in Statement of Profit and Loss (Opening)

|

1,00,000

|

|

Surplus, i.e., Balance in Statement of Profit and Loss (Closing)

|

3,36,000

|

|

Dividend paid in the current year

|

72,000

|

|

Interim Dividend Paid during the year

|

90,000

|

|

Transfer to Reserve

|

1,00,000

|

|

Provision for Tax for the current year

|

1,50,000

|

|

Refund of Tax

|

3,000

|

|

Loss due to Earthquake

|

2,00,000

|

|

Insurance Proceeds from Earthquake disaster settlement

|

1,00,000

|