Question

Give the rules of Debit and Credit and explain them with imaginary examples.

Under Double Entry System of accounting each transaction has two aspects. One aspect is debit, i.e., receiving or incoming aspect. Another aspect is credit, i.e., giving or outgoing aspect. Debit and credit aspects of a transaction form the basis of Double Entry System.

Rules of Double Entry or Rules of Debit and Credit are formed on the basis of these two aspects in each of the business transactions. There are two approaches for deciding when to write on the debit side of account and when to write on the credit side of an account, i.e., which account is to be debited and which account is to be credited. The rules or: the basis of which such decision is taken are called Rules of Debit and Credit.

Rules of Debit and Credit (Traditional Classification) at a Glance:

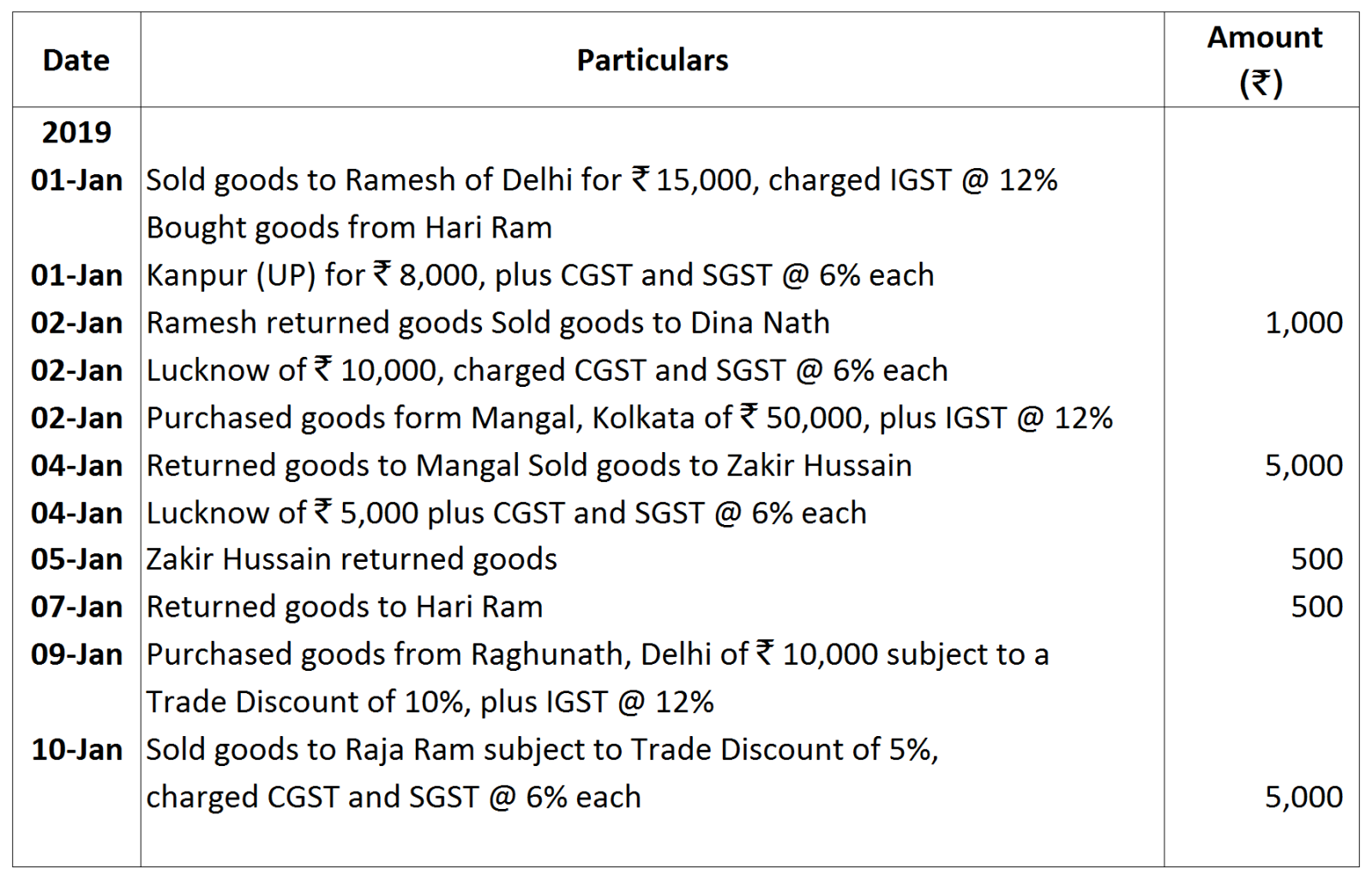

From the following transactions, state the nature of accounts and state which account will be debited and which account will be credited:

Under Double Entry System of accounting each transaction has two aspects. One aspect is debit, i.e., receiving or incoming aspect. Another aspect is credit, i.e., giving or outgoing aspect. Debit and credit aspects of a transaction form the basis of Double Entry System.

Rules of Double Entry or Rules of Debit and Credit are formed on the basis of these two aspects in each of the business transactions. There are two approaches for deciding when to write on the debit side of account and when to write on the credit side of an account, i.e., which account is to be debited and which account is to be credited. The rules or: the basis of which such decision is taken are called Rules of Debit and Credit.

Rules of Debit and Credit (Traditional Classification) at a Glance:

|

S.No

|

Types of Account

|

Account to be Debited

|

Account to be Credited

|

|

1

|

Personal Account

|

Receiver

|

Giver

|

|

2

|

Real Account

|

What comes in

|

what goes out

|

|

3

|

Nominal Account

|

Expense and Loss

|

Income and Gain

|

| S.No | ₹ | |

|

1

|

Mohan started business with cash

|

5,00,000

|

|

2

|

Purchased goods for cash

|

1,00,000

|

|

3

|

Sold goods for cash

|

1,50,000

|

|

4

|

Received interest from Ram in cash

|

500

|

|

5

|

Sold goods to Ashok

|

60,000

|

|

6

|

Purchased furniture for cash

|

50,000

|

|

7

|

Paid wages

|

20.000 |