Question

How does ratio analysis become less effective due to price level changes?

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

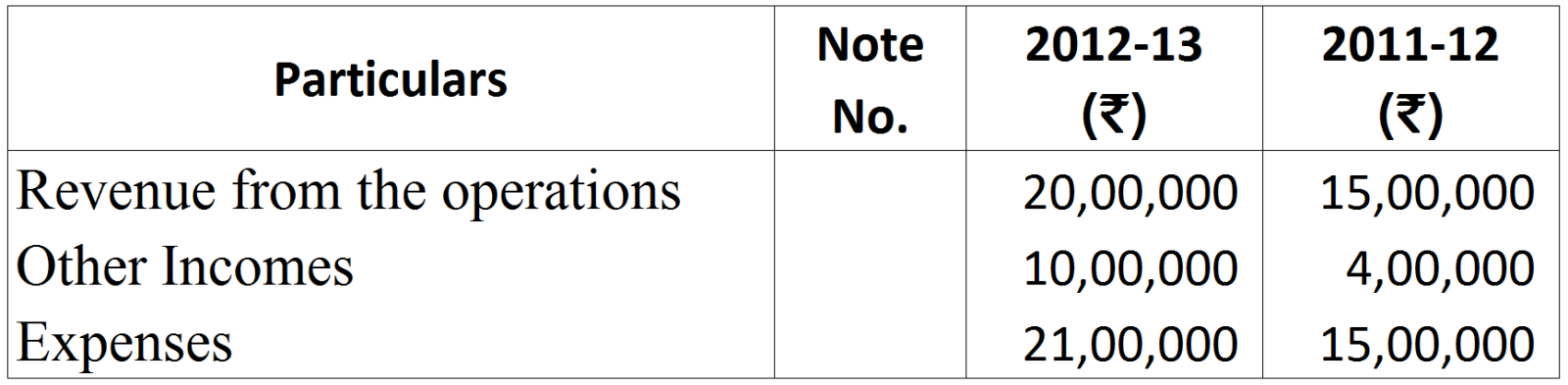

| RJ Ltd.Statement of Profit and Loss for the year ended 31st March, 2022 | |||

| Particulars | Note No. | 2021 - 22 ₹ | 2020 - 21 ₹ |

| Revenue from Operations | 20,00,000 | 15,00,000 | |

| Employee Benefit Expenses | 8,00,000 | 4,00,000 | |

| Other Expenses | 2,00,000 | 1,00,000 | |

| Tax Rate 50% | |||

|

Particulars

|

31st March, 2018 ₹

|

31st March, 2017 ₹

|

|

Investments in Land

Shares in Z Ltd.

12% Long-term Investments

Plant and Machinery

Patents

Goodwill

|

3,00,000

1,50,000

80,000

7,50,000

70,000

1,50,000

|

3,00,000

1,50,000

50,000

6,00,000

1,00,000

1,00,000

|

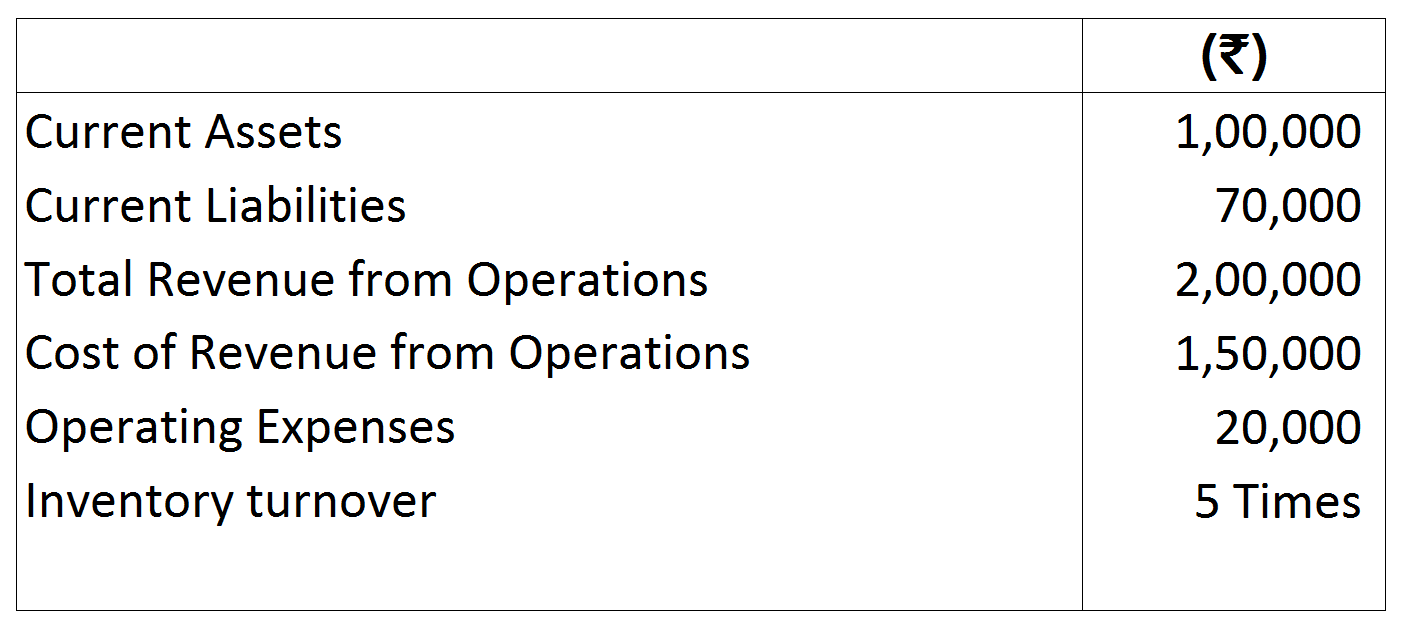

If the closing inventory is more by f4,000 than opening inventory, determine the following:

If the closing inventory is more by f4,000 than opening inventory, determine the following: