Question

Rectify the following errors which were detected before preparing the Trial Balance:

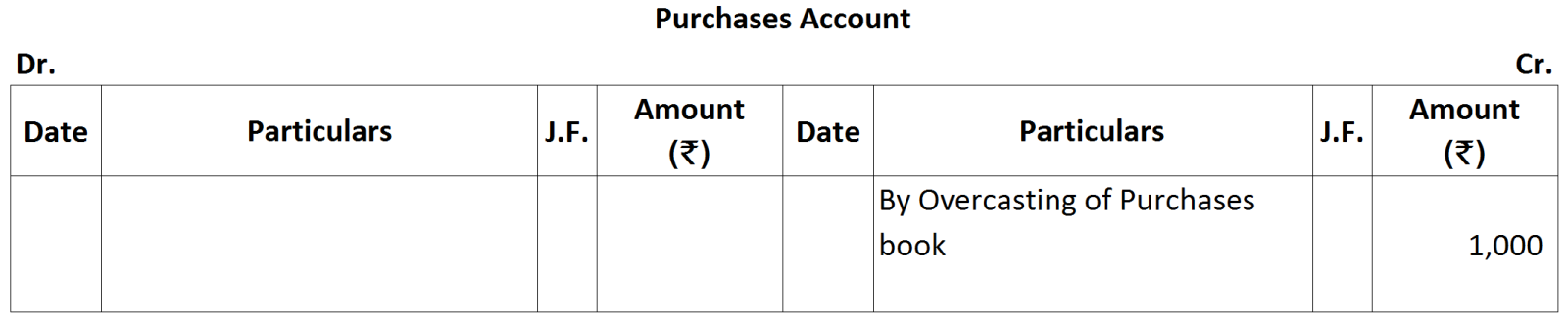

- Purchase book has been overcast by ₹ 1,000.

- Purchase from Ram ₹ 20,000 has been omitted to be posted to his account.

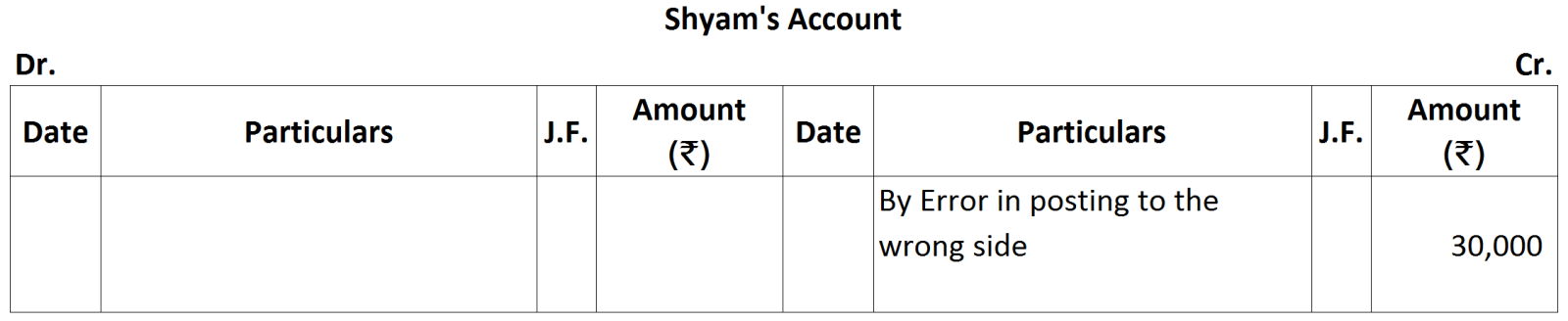

- Purchase from Shyam ₹ 15,000 has been posted to the debit side of his account.

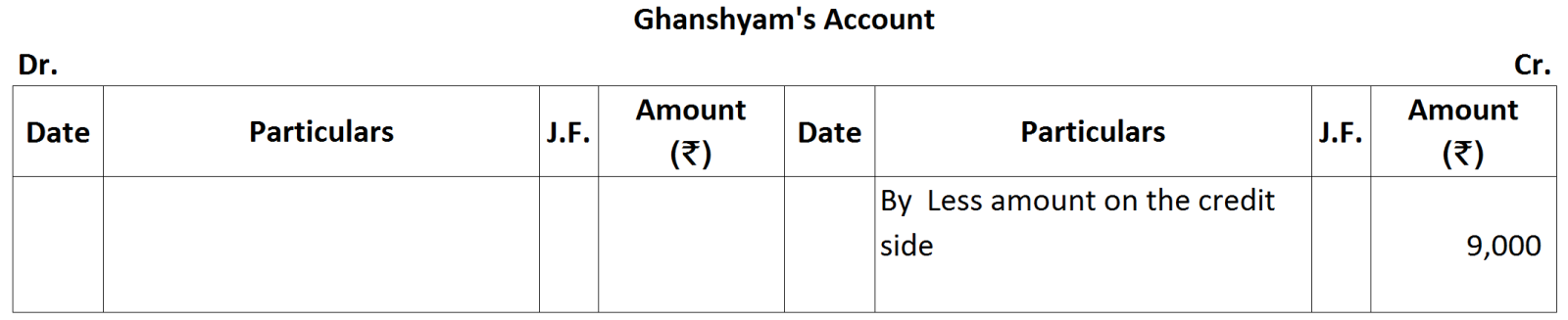

- Purchase from Ghanshyam ₹ 10,000 has been posted to his account as ₹ 1,000.

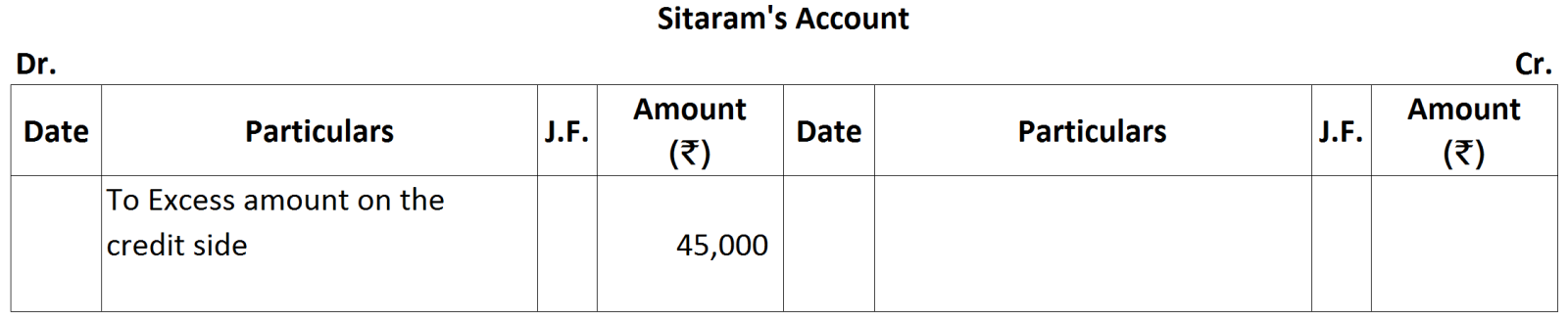

- Purchase from Sita Ram ₹ 5,000 has been posted to his account as ₹ 50,000.