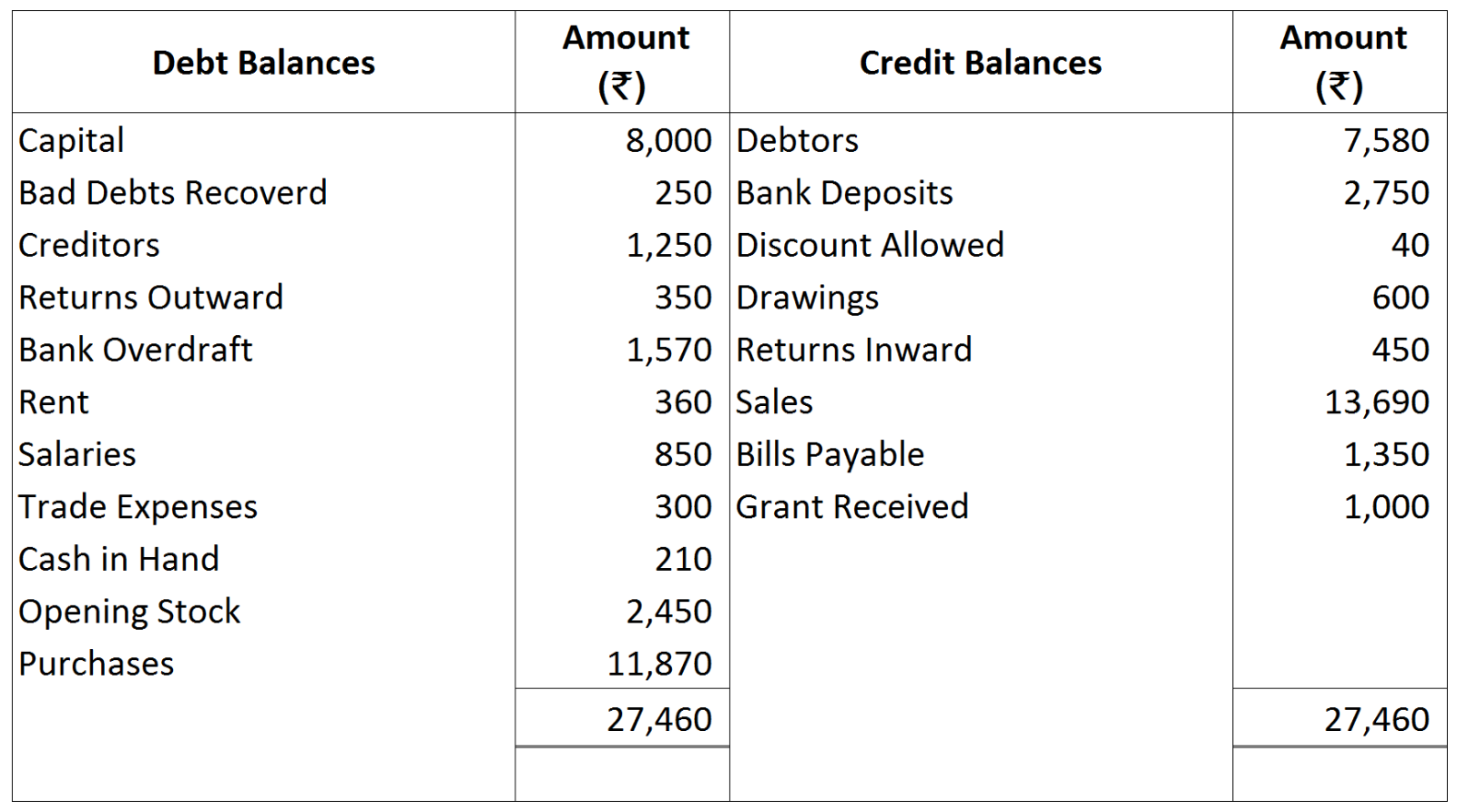

Question

Redraft correctly the Trial Balance given below:

Get the step-by-step solution for this question inside the Vidyadip app.

Get the answer in the appGenerate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

|

|

₹

|

|

(i)

|

Bank Balance as per Pass Book.

|

10,000

|

|

(ii)

|

Cheque deposited into bank but no entry was passed in Cash Book.

|

500

|

|

(iii)

|

Cheque received and entered in Cash Book but not sent to bank.

|

1,200

|

|

(iv)

|

Insurance premium paid directly by the bank.

|

800

|

|

(v)

|

Bank charges entered twice in the Cash Book.

|

20

|

|

(vi)

|

Cheque received entered twice in Cash Book.

|

1,000

|

|

(vii)

|

Bill discounted dishonoured not recorded in the cash book.

|

5,000

|