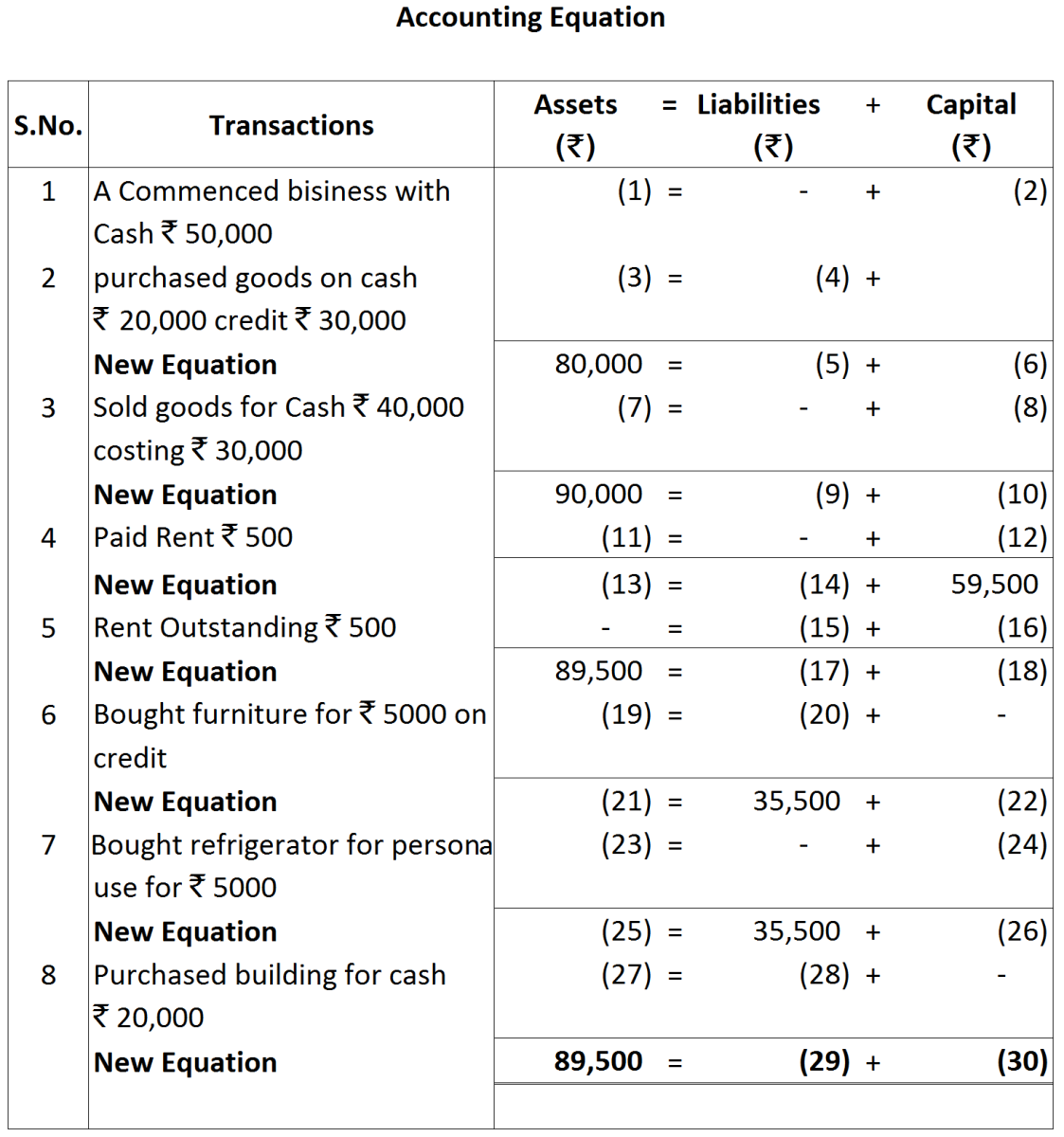

Question

State the causes of difference occurred due to time lag.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

2018

|

|

|

March 1

|

Purchased goods for ₹ 5,00,000 from Mehta Bros.

|

|

March 10

|

Sold goods for ₹ 8,00,000 to Munjal & Co.

|

|

March 15

|

Paid for advertisement ₹ 40,000 by cheque.

|

|

March 18

|

Purchased furniture for office use ₹ 50,000 and payment made by cheque.

|

|

March 25

|

Paid for printing and stationery ₹ 8,000.

|

|

March 31

|

Payment made of balance amount of GST.

|

|

2018

|

|

|

April 1

|

Purchased goods for ₹ 1,00,000 from Manoj and availed discount of ₹ 10,000

|

|

April 2

|

Paid amount due to Manoj by cheque and availed discount of ₹ 4,500

|

|

April 5

|

Cash ₹ 5,000 paid to Desai and discount allowed by him ₹ 200

|

|

April 10

|

Cash ₹ 10,000 received from Govardhan and allowed him discount ₹ 500.

|

|

April 12

|

Sold personal Car of the proprietor for ₹ 80,00 against cheque, which was deposited into the firm's bank account.

|

|

April 16

|

Sold personal Car of the proprietor for ₹ 1,50,000 against cheque, which was deposited into the proprietor's personal bank account.

|

|

April 20

|

Sold goods to Gaurav costing ₹ 1,00,000 at a profit of 40% and allowed him 10% trade discount and paid for cartage ₹ 3,000 not to be charged from him.

|

|

April 24

|

Placed an order with Rudra & Co. for supply of goods of ₹ 80,000 and a cheque for 40% amount is sent to them as an advance.

|

|

a.

|

Commenced business with cash

|

₹ 1,50.000

|

|

b.

|

Purchased machinery on credit

|

₹ 40,000

|

|

c.

|

Purchased goods for cash

|

₹ 20,500

|

|

d.

|

Purchased car for personal use

|

₹ 80,000

|

|

e.

|

Paid to creditors in full settlement

|

₹ 38,000

|

|

f.

|

Sold goods for cash costing ₹ 5,000

|

₹ 4,500

|

|

g.

|

Paid rent

|

₹ 1,000

|

|

h.

|

Commission received in advance

|

₹ 2,000

|