Question

What is horizontal analysis of financial statements?

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

On Application

|

:

|

₹ 3 per share

|

|

On Allotment

|

:

|

₹ 3 per share (including premium)

|

|

On First Call

|

:

|

₹ 3 per share

|

|

On Second and Final Call

|

:

|

Balance amount

|

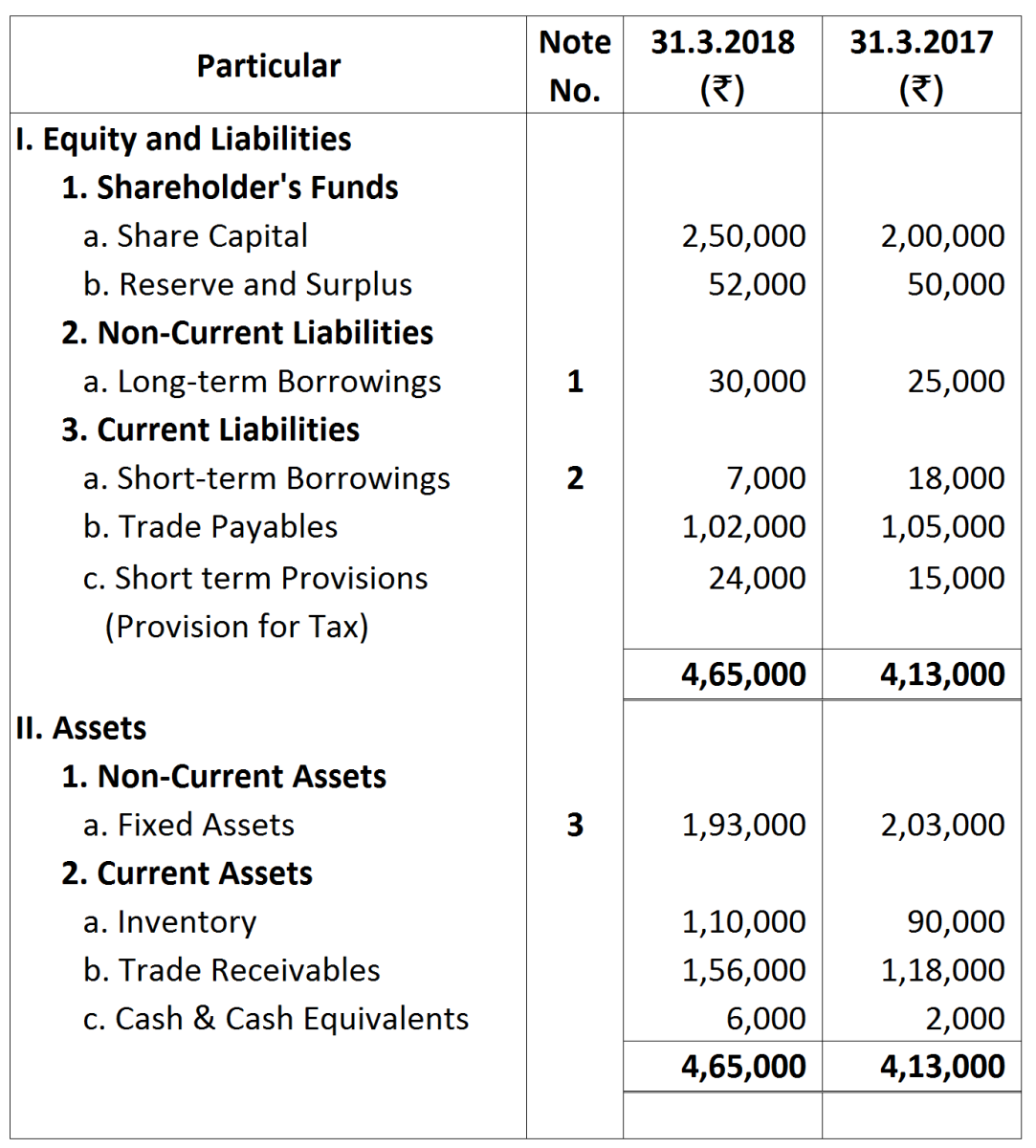

Notes:

Notes:  Additional Information:

Additional Information:

|

1.

|

Contingent Liability

|

31.3.2018

|

31.3.2017

|

|

|

|

₹

|

₹

|

|

|

Proposed Dividend

|

30,000

|

25,000

|

|

2.

|

Provision for tax made ₹ 30,000.

|

||

|

3.

|

Additional debentures amounting to ₹ 5,000 were issued on 1st Oct. 2017. Interest on debentures has been paid up-to date.

|

||