Question

What is 'Window Dressing'? Explain with the help of an example.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

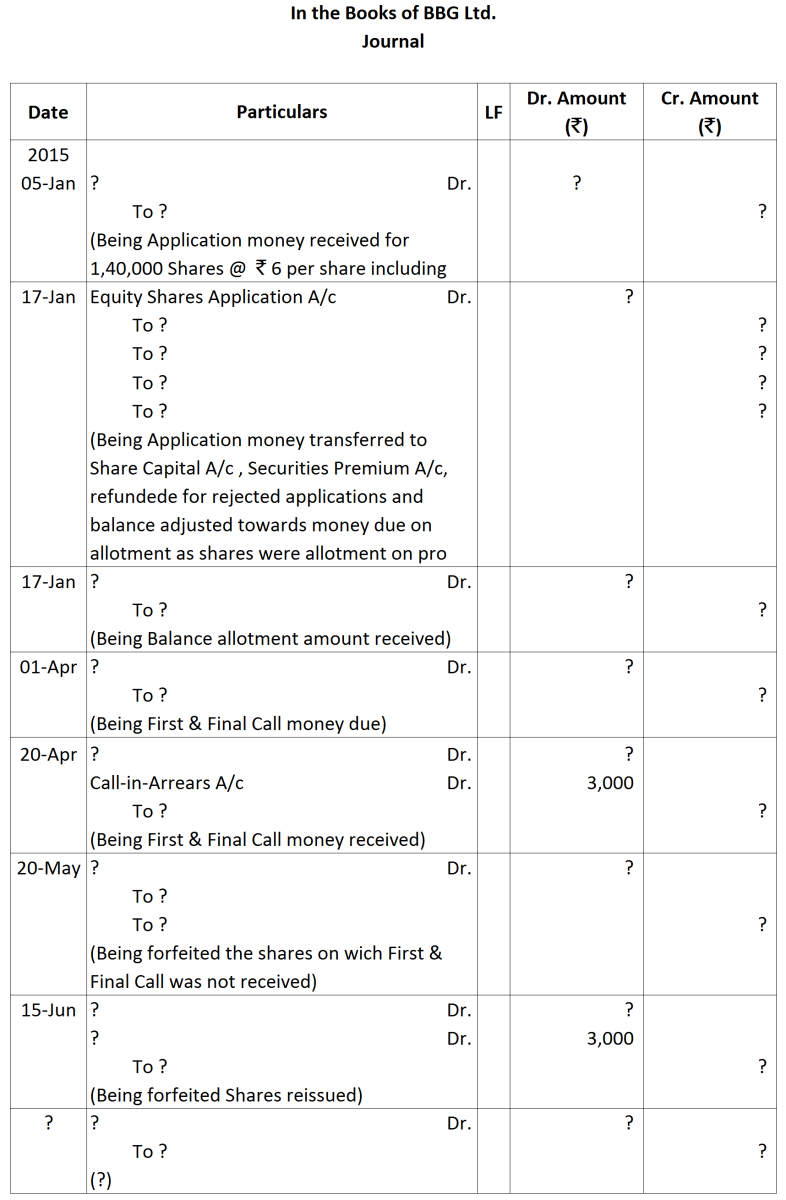

|

|

₹

|

|

On application

|

30

|

|

On allotment

|

25 (including premium)

|

|

On first call

|

20

|

|

On final call

|

30

|

| On application and allotment | - | ₹ 4 per share, |

| On first Call | - | ₹ 3 per share, |

| On second and final Call | - | balance. |