Question

What would be an effect on equilibrium price and quantity when demand and supply both increase at the same rate?

OR

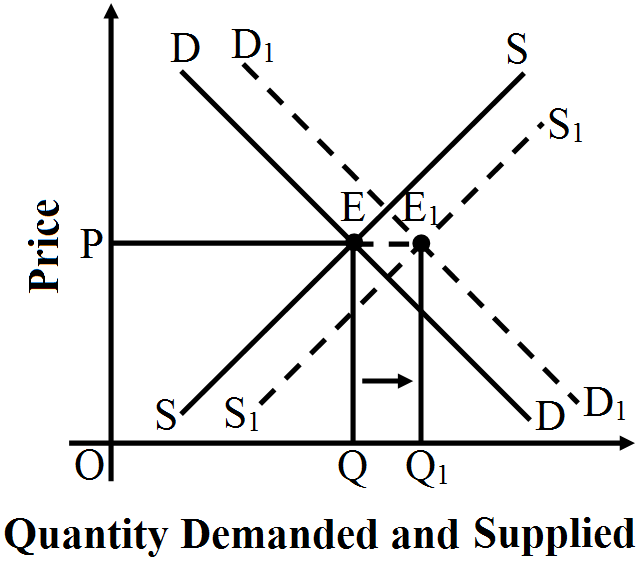

Explain with the help of a diagram a situation when demand and supply curves shift to the right but equilibrium price remains the same.

OR

Market for a good is in equilibrium. What is the effect on equilibrium price and quantity if both the market demand and the market supply of the goods increase in the same proportion? Use diagram.

OR

Explain with the help of a diagram a situation when demand and supply curves shift to the right but equilibrium price remains the same.

OR

Market for a good is in equilibrium. What is the effect on equilibrium price and quantity if both the market demand and the market supply of the goods increase in the same proportion? Use diagram.