Question

Why is Balance Sheet prepared?

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

|

|

₹

|

|

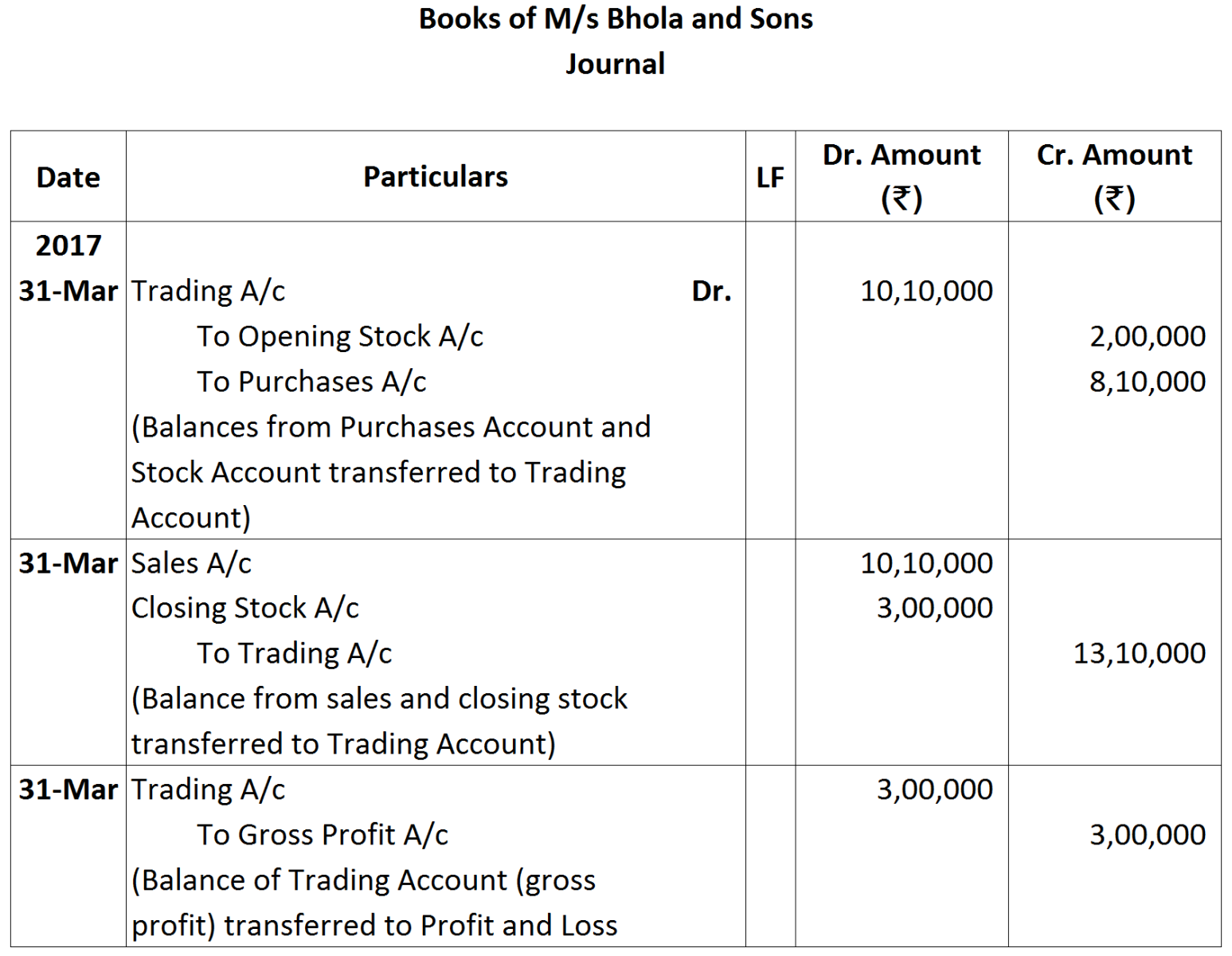

Opening Stock:

|

Raw Material

|

80,000

|

|

|

Finished Goods

|

1,40,000

|

|

Purchases

|

|

3,60,000

|

|

Sales

|

|

7,00,000

|

|

Returns:

|

Purchases

|

10,000

|

|

|

Sales

|

6,000

|

|

Wages

|

|

1,30,000

|

|

Factory Expenses

|

|

90,000

|

|

Freight:

|

Inwards

|

20,000

|

|

|

Outwards

|

30,000

|

|

At the end of the accounting period, stock was:

|

|

|

|

Raw Materials

|

|

70,000

|

|

Work-in-Process

|

|

20,000

|

|

Finished Goods

|

|

1,10,000

|

| 2019 | ₹ | |

| May 23 | Postage | 400 |

| May 24 | Casual labour | 500 |

| May 24 | Taxi hire | 600 |

| May 26 | Note pads and registers | 800 |

| May 27 | Cartage | 200 |

| May 28 | Bus fare | 300 |