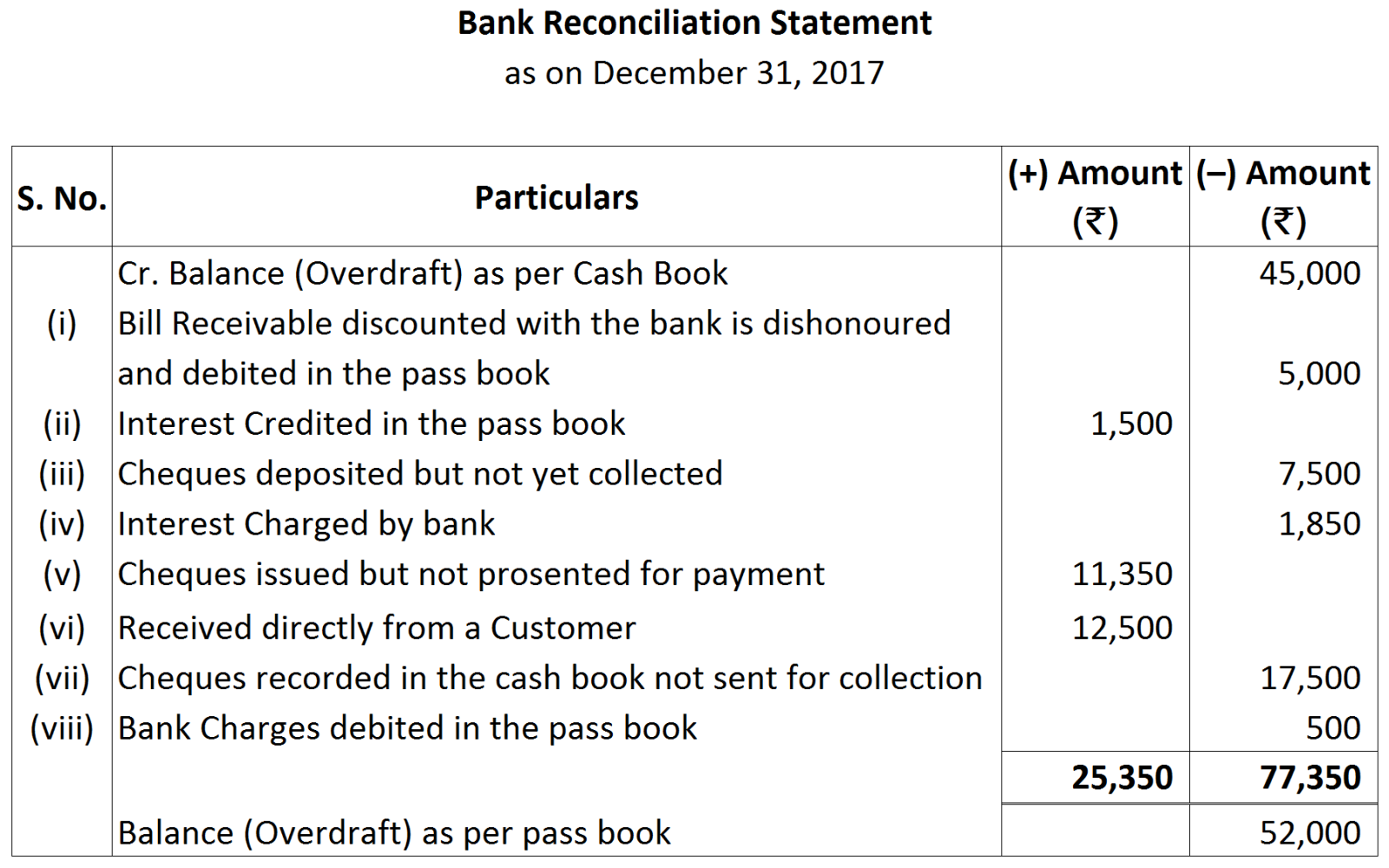

Question 11 Mark

Cheques issued but not presented for payment are recorded or not recorded in an amended cash book? Give reason for your answer.

Answer

View full question & answer→Cheques issued but not presented for payment are not recorded in an amended cash book because they will be ultimately presented for payment in the bank.