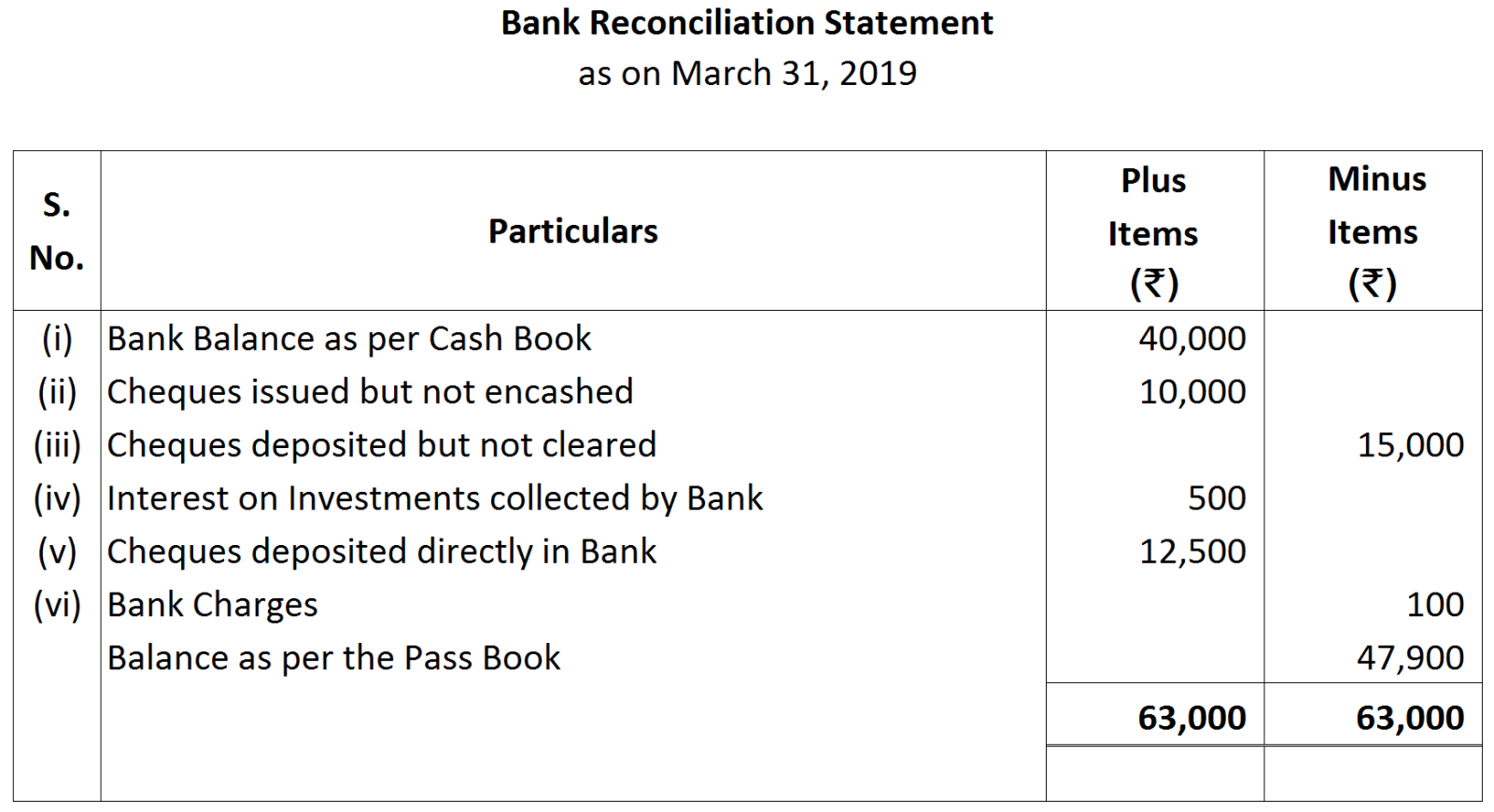

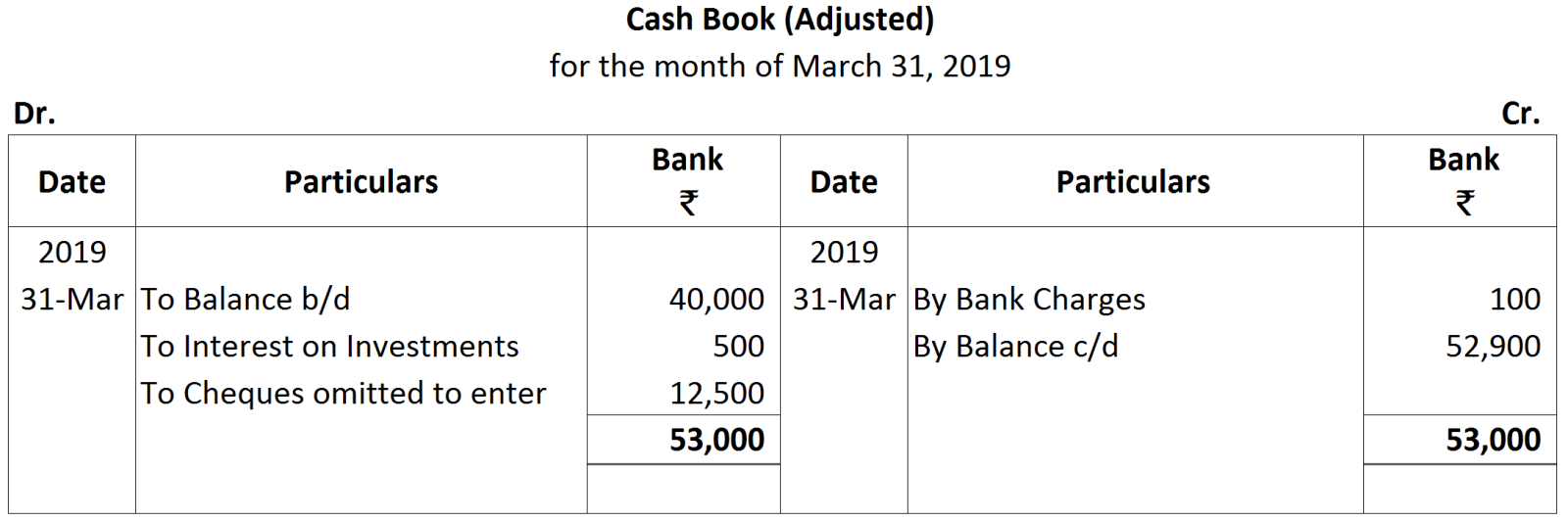

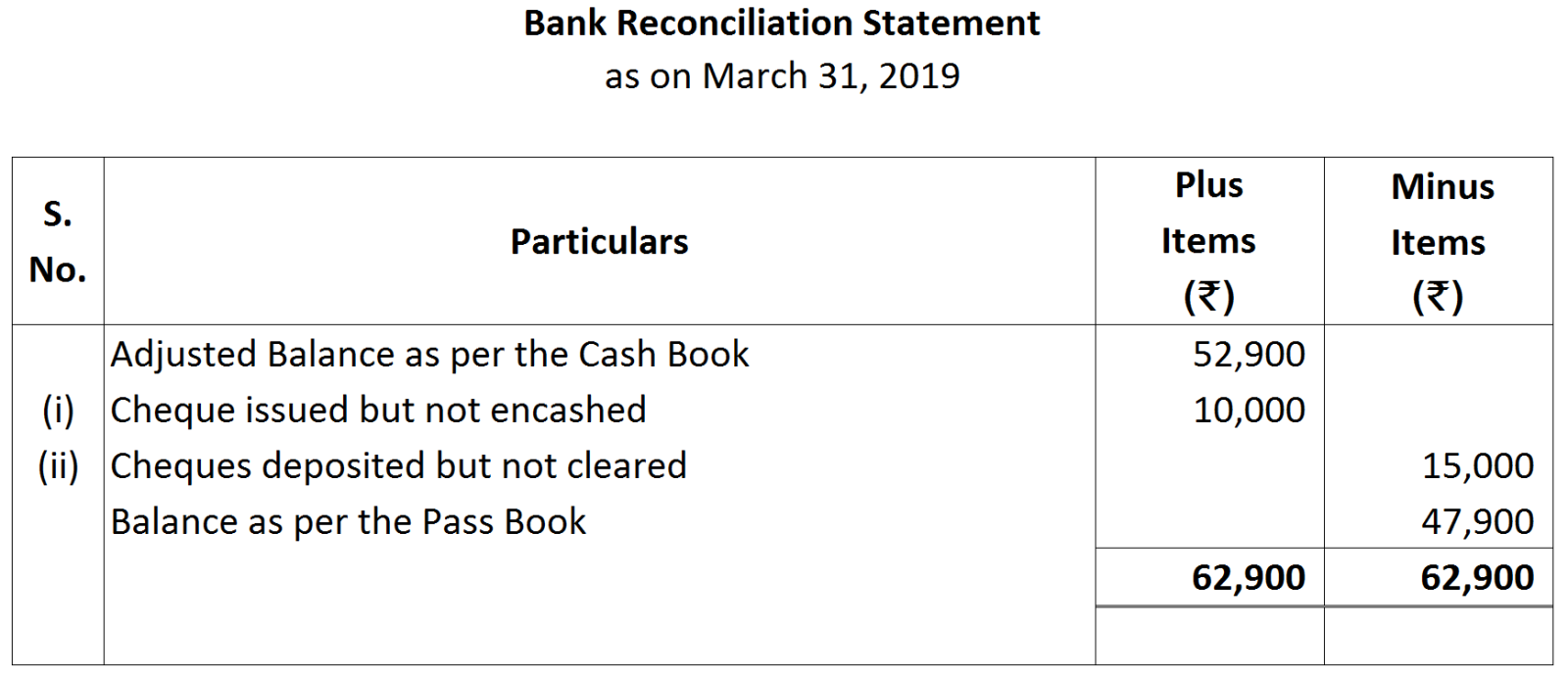

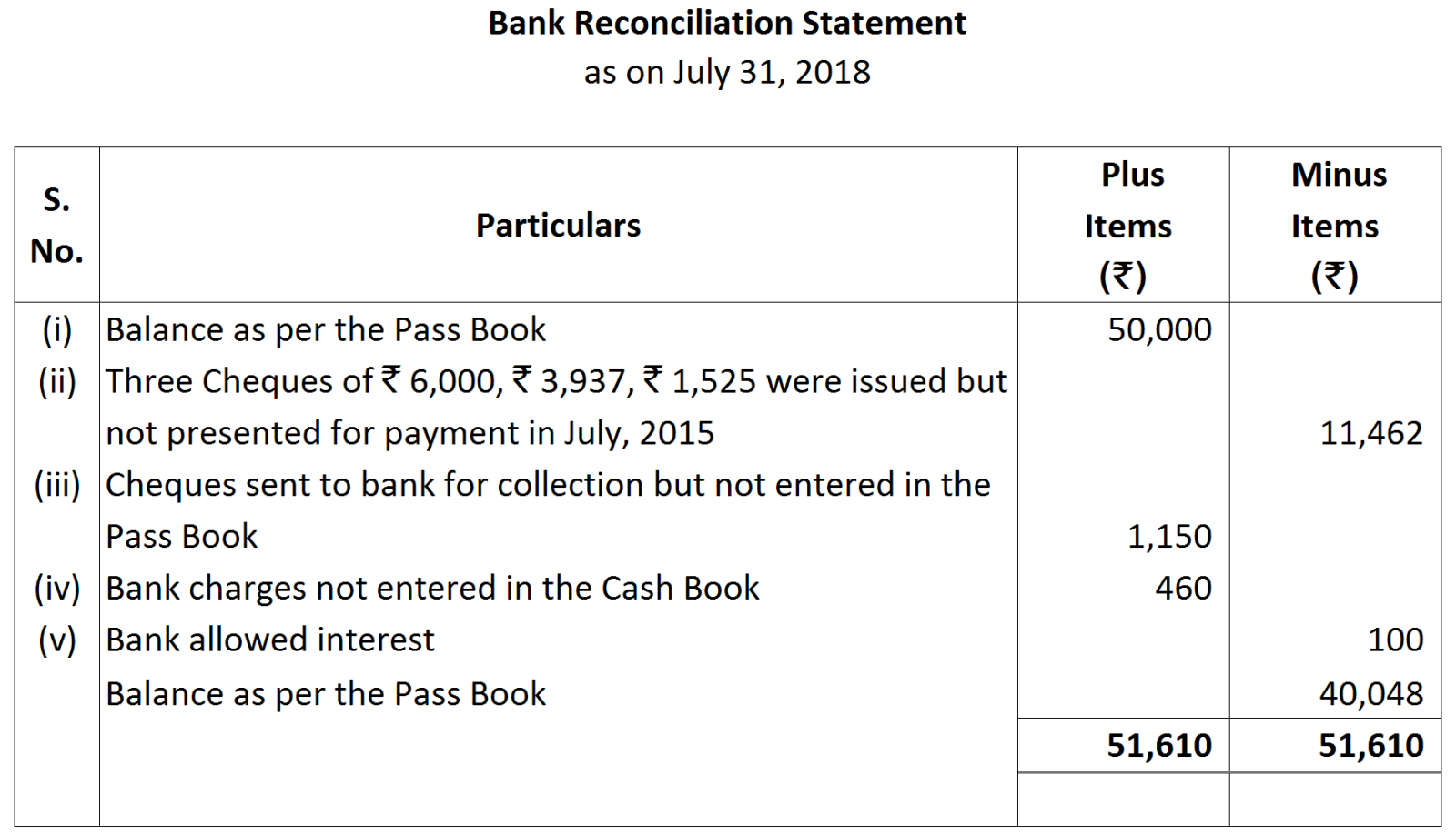

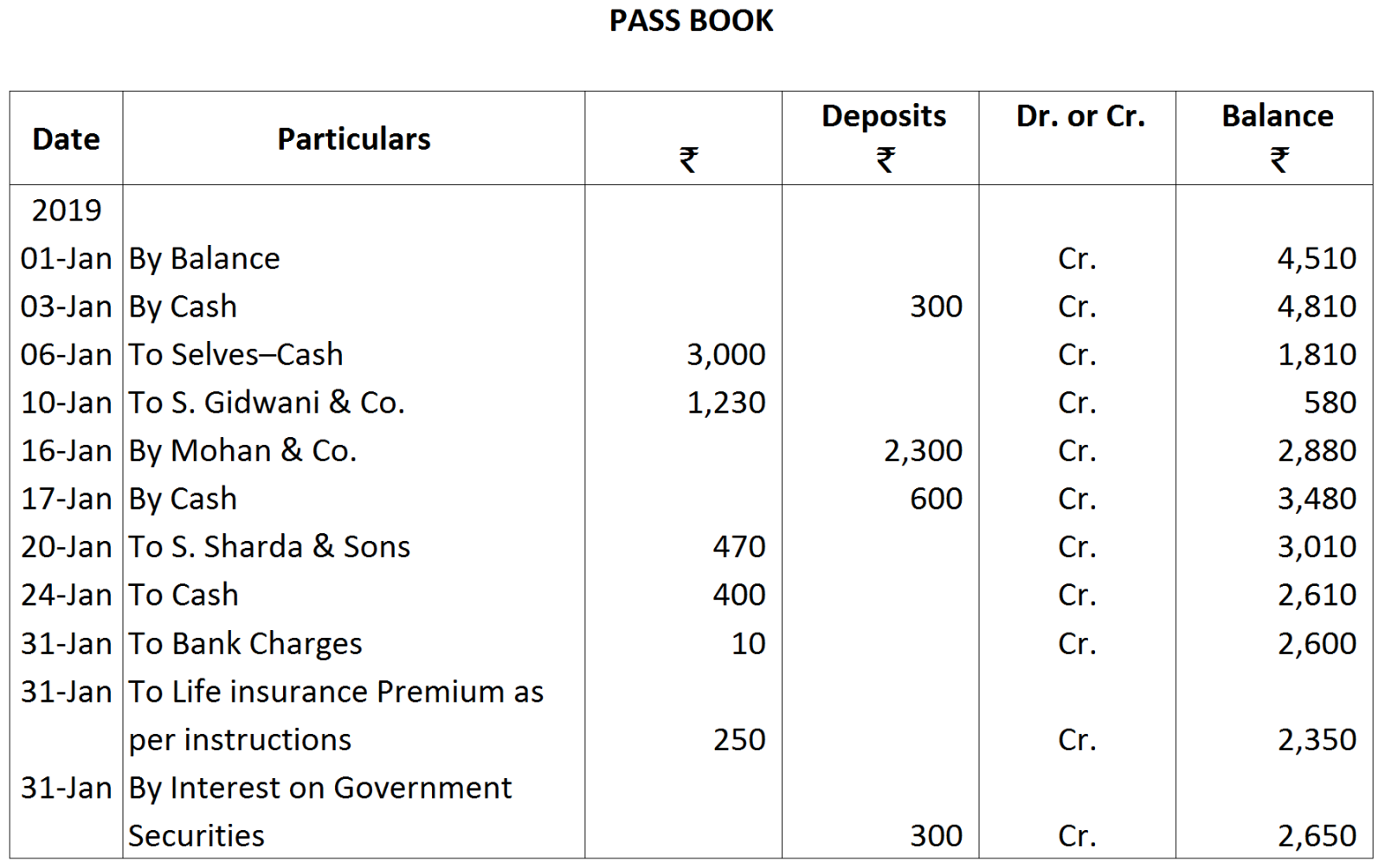

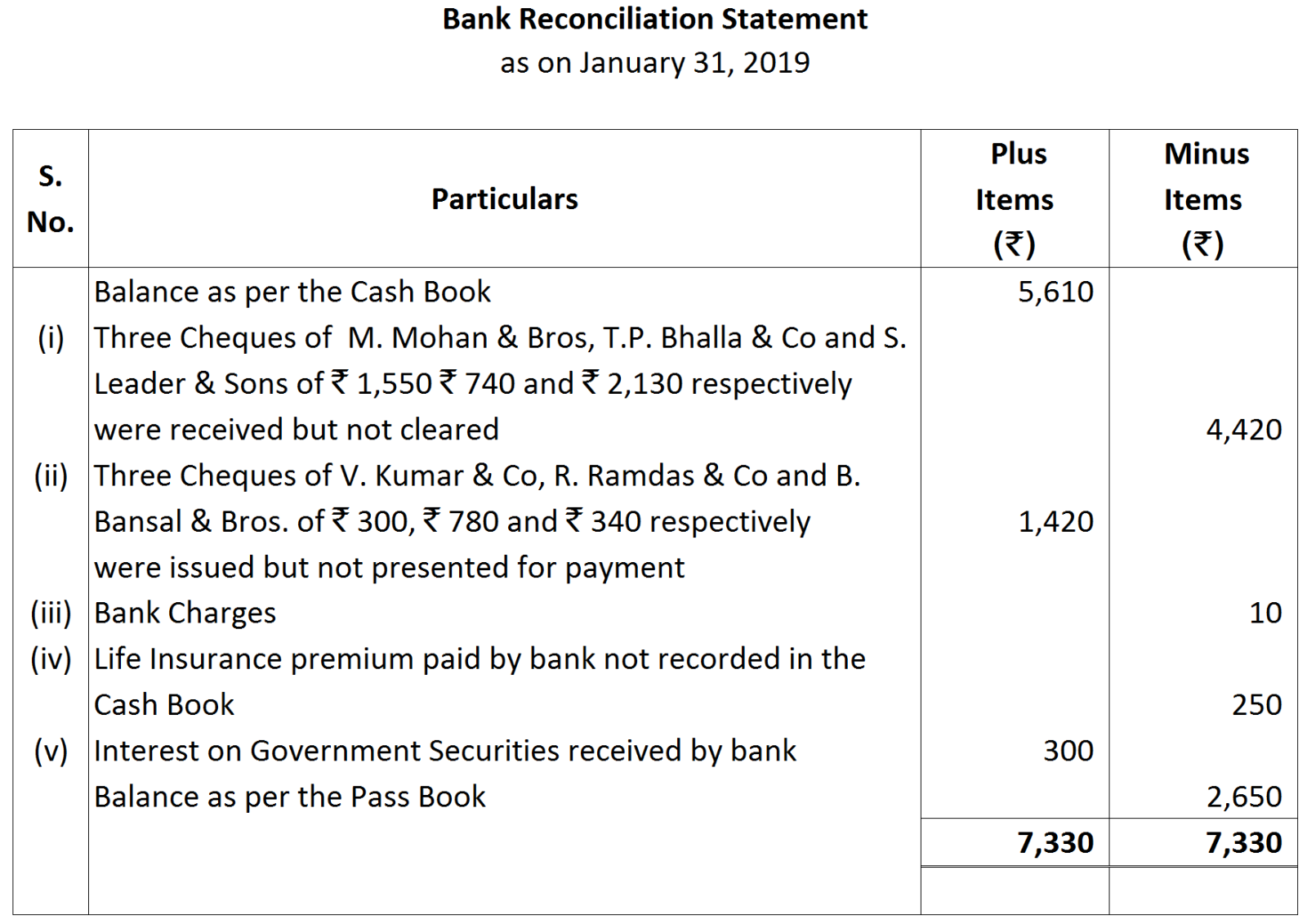

Question 16 Marks

Prepare Bank Reconciliation Statement from the following particulars on 31st July, 2018:

- Balance as per the Pass Book ₹ 50,000.

- Three cheques for ₹ 6,000, ₹ 3,937 and ₹ 1,525 issued in last week of July, 2018 were presented for payment to the bank in August, 2018.

- Two cheques of ₹ 500 and ₹ 650 sent to the bank for collection were not entered in the Pass Book by 31st July, 2018.

- The bank charged ₹ 460 for its commission and allowed interest of ₹ 100 which were not mentioned in the Bank Column of the Cash Book.

Answer

View full question & answer→Solution is as follows:

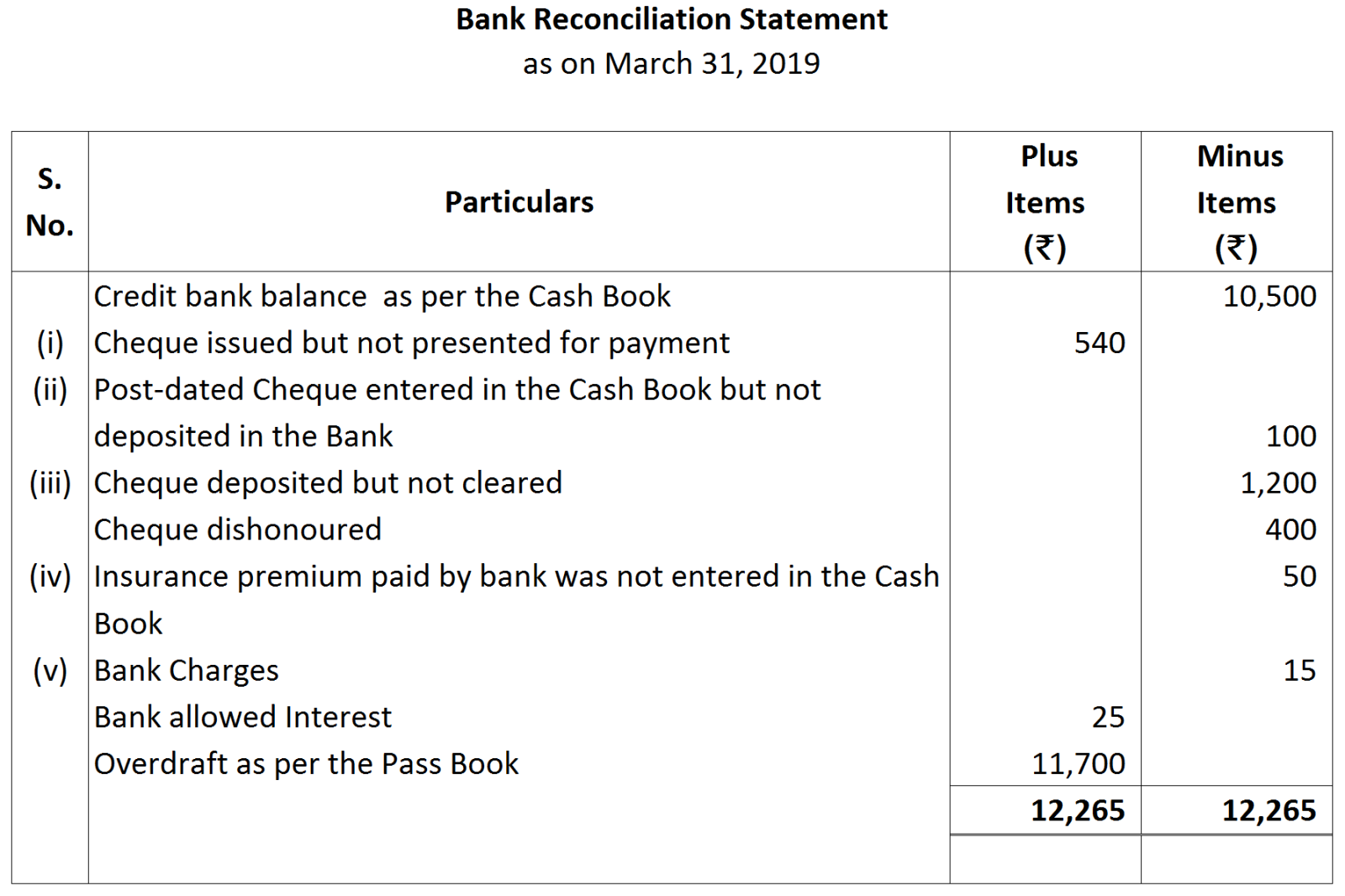

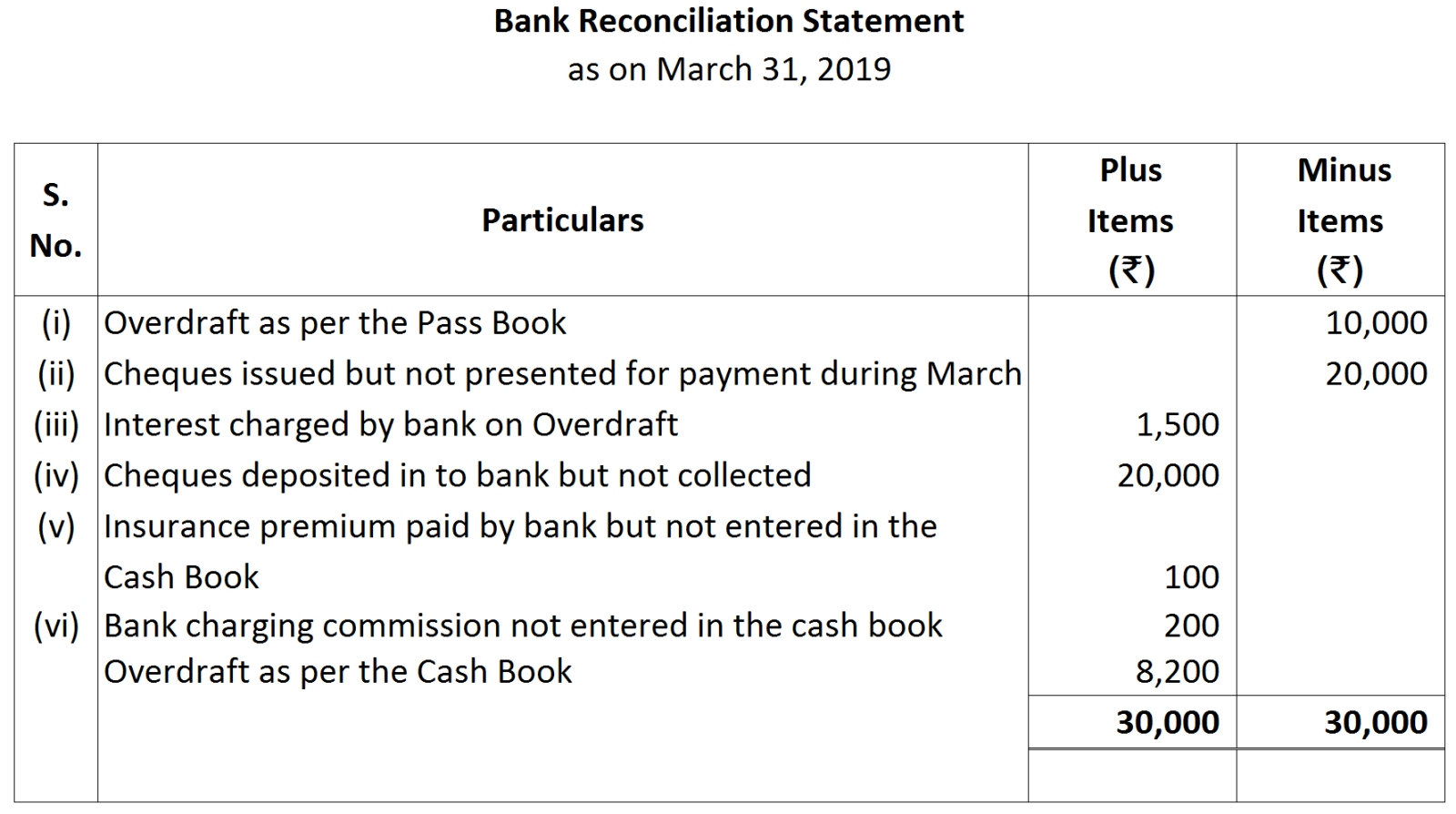

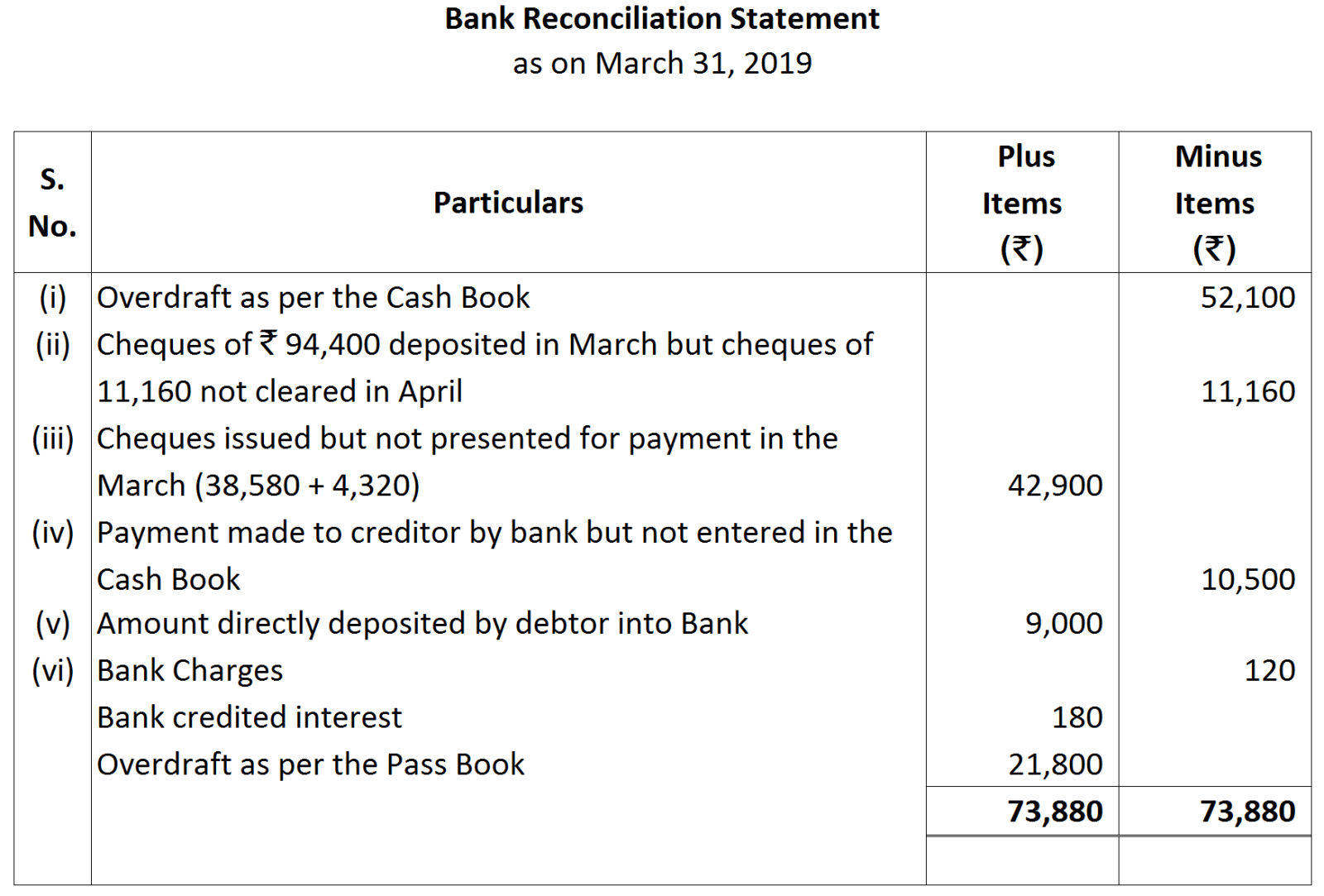

Note: Cheque dated 15th April, 2019 issued to M & Co. dishonoured will have no impact as this statement is as on 31st March 2019.

Note: Cheque dated 15th April, 2019 issued to M & Co. dishonoured will have no impact as this statement is as on 31st March 2019.

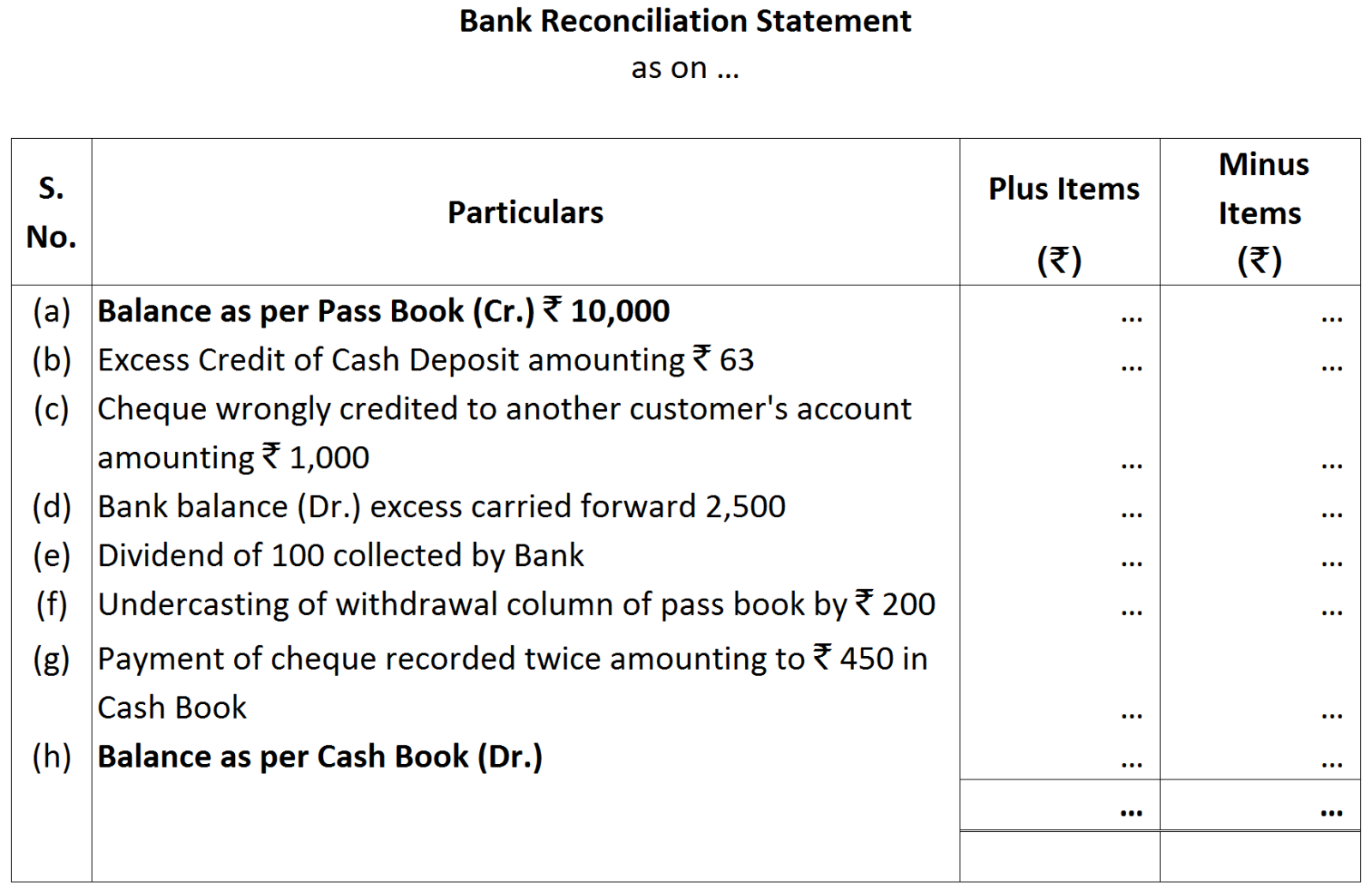

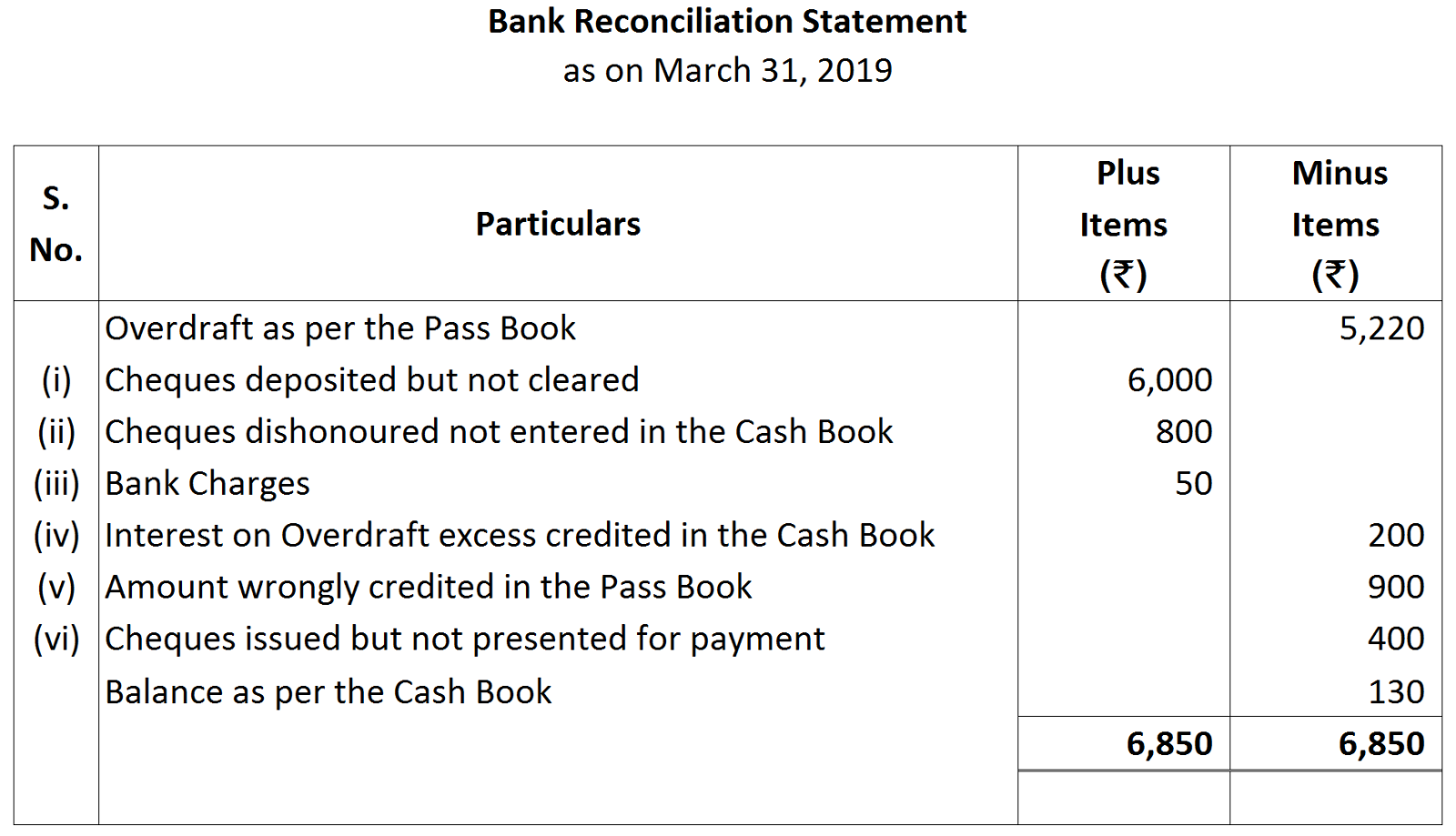

Note: In Cash Book cheque received from G. Basu & Co is debited with ₹ 1,000 and at the time of dishonour entry is reversed by crediting G. Basu & Co with ₹ 1,000. Therefore its net effect is nil in Cash Book.

Note: In Cash Book cheque received from G. Basu & Co is debited with ₹ 1,000 and at the time of dishonour entry is reversed by crediting G. Basu & Co with ₹ 1,000. Therefore its net effect is nil in Cash Book.

\

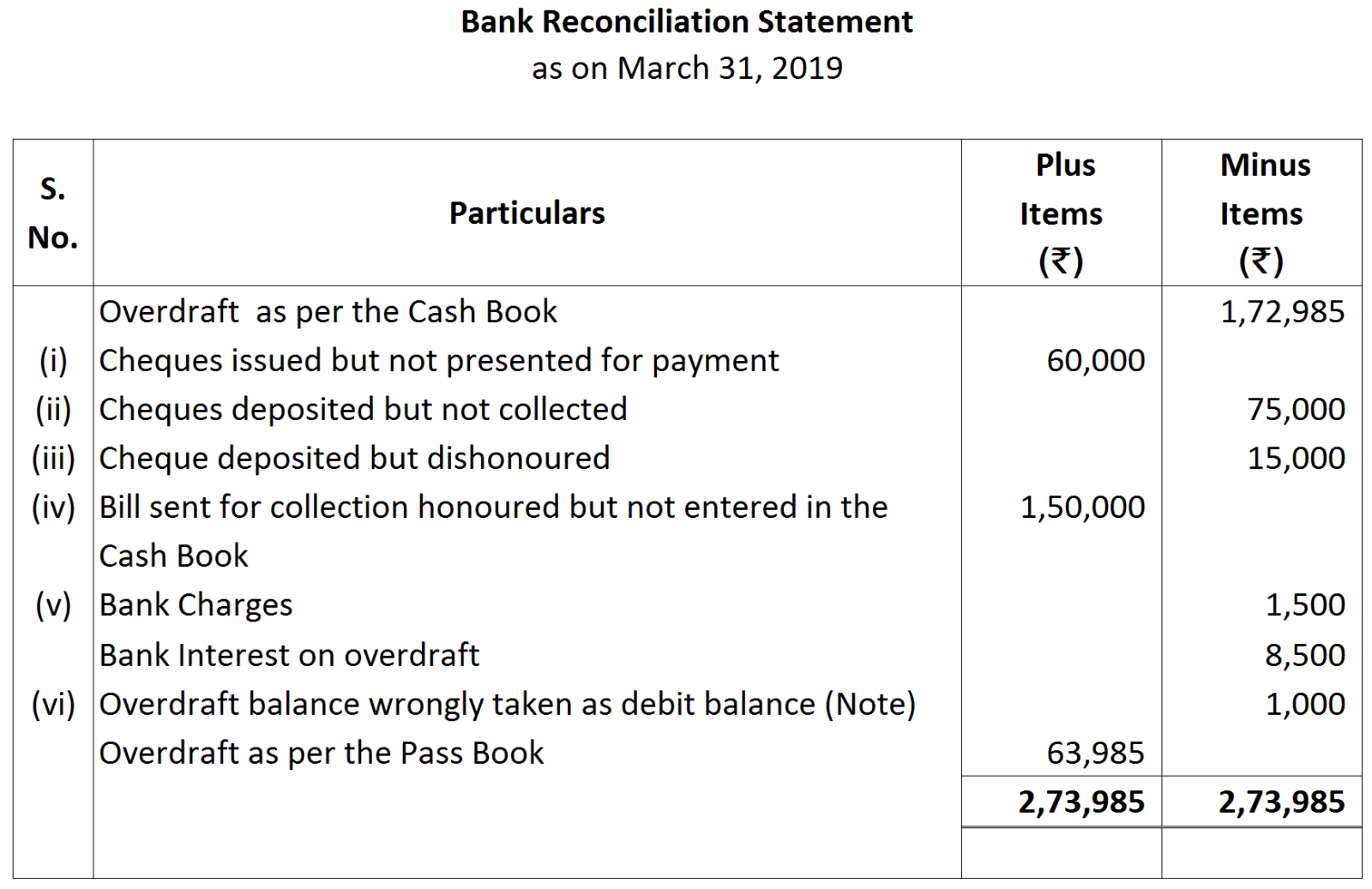

\ Note: Overdraft balance has credit balance but taken as debit balance, so to correct the error credit cash book by double amount.

Note: Overdraft balance has credit balance but taken as debit balance, so to correct the error credit cash book by double amount. Note: Point (vii) will have no affect on the statement as error in recording cash deposit entry is already rectified.

Note: Point (vii) will have no affect on the statement as error in recording cash deposit entry is already rectified.