Question 13 Marks

Write the various Assets in order of liquidity in a Balance Sheet.

Answer

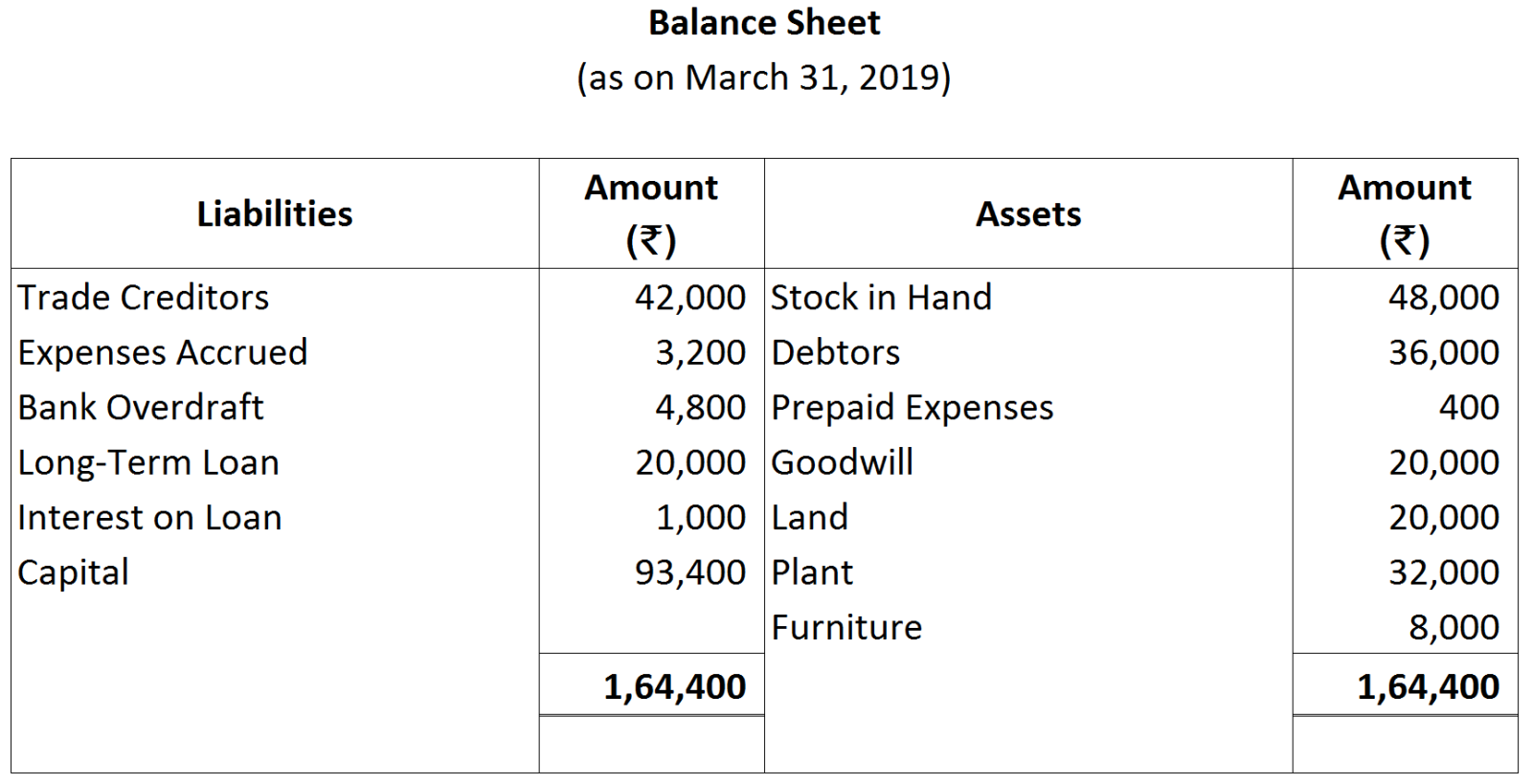

View full question & answer→In the Order of Liquidity:

Current Assets:

Non-Current Assets:-

Current Assets:

- Cash in Hand

- Cash at Bank

- Bills Receivable

- Short Term Investments

- Sundry Debtors/ Book Debts

- Closing Stock

- Prepaid Expenses

- Accrued Income

Non-Current Assets:-

- Furniture

- Loose Tools

- Motor Vehicle

- Plant and Machinery

- Land and Buildings

- Patents and Trade Marks

- Goodwill

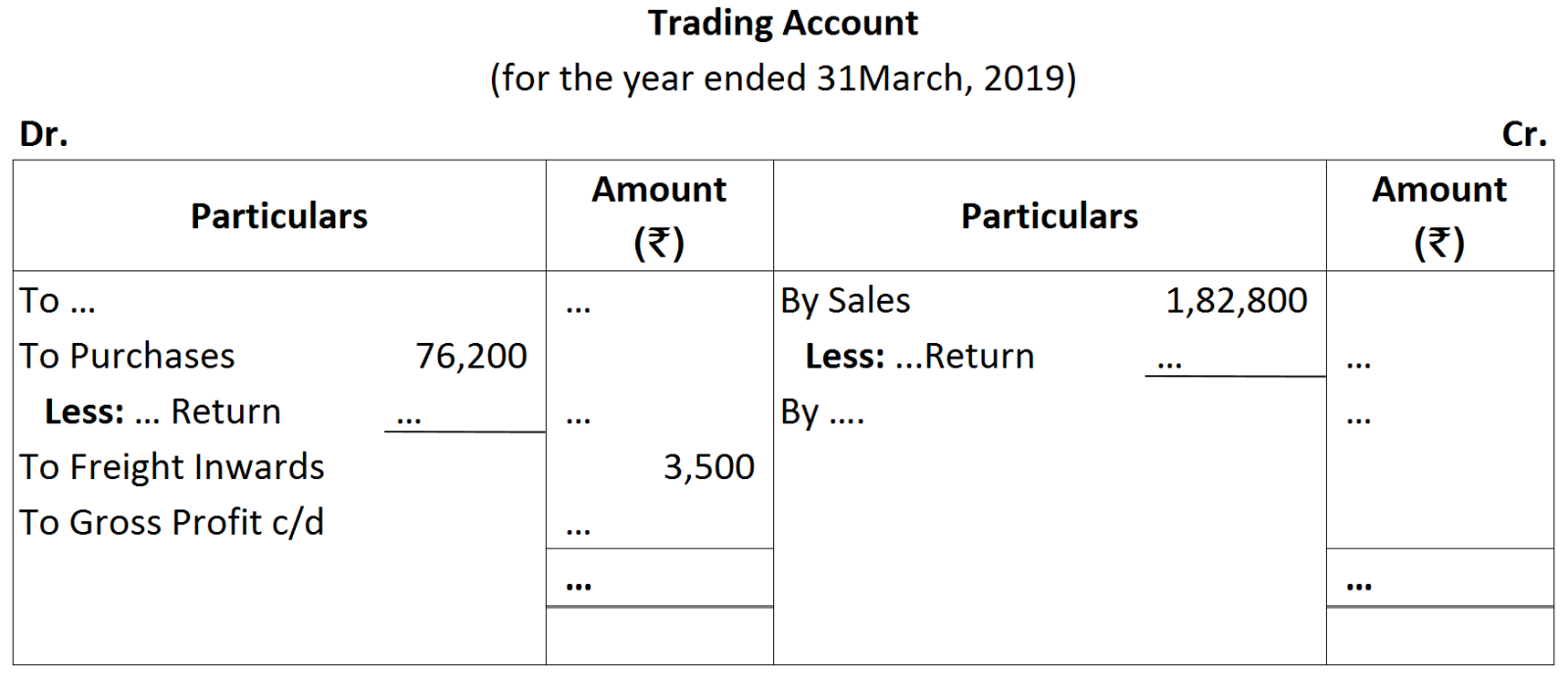

Notes:

Notes:

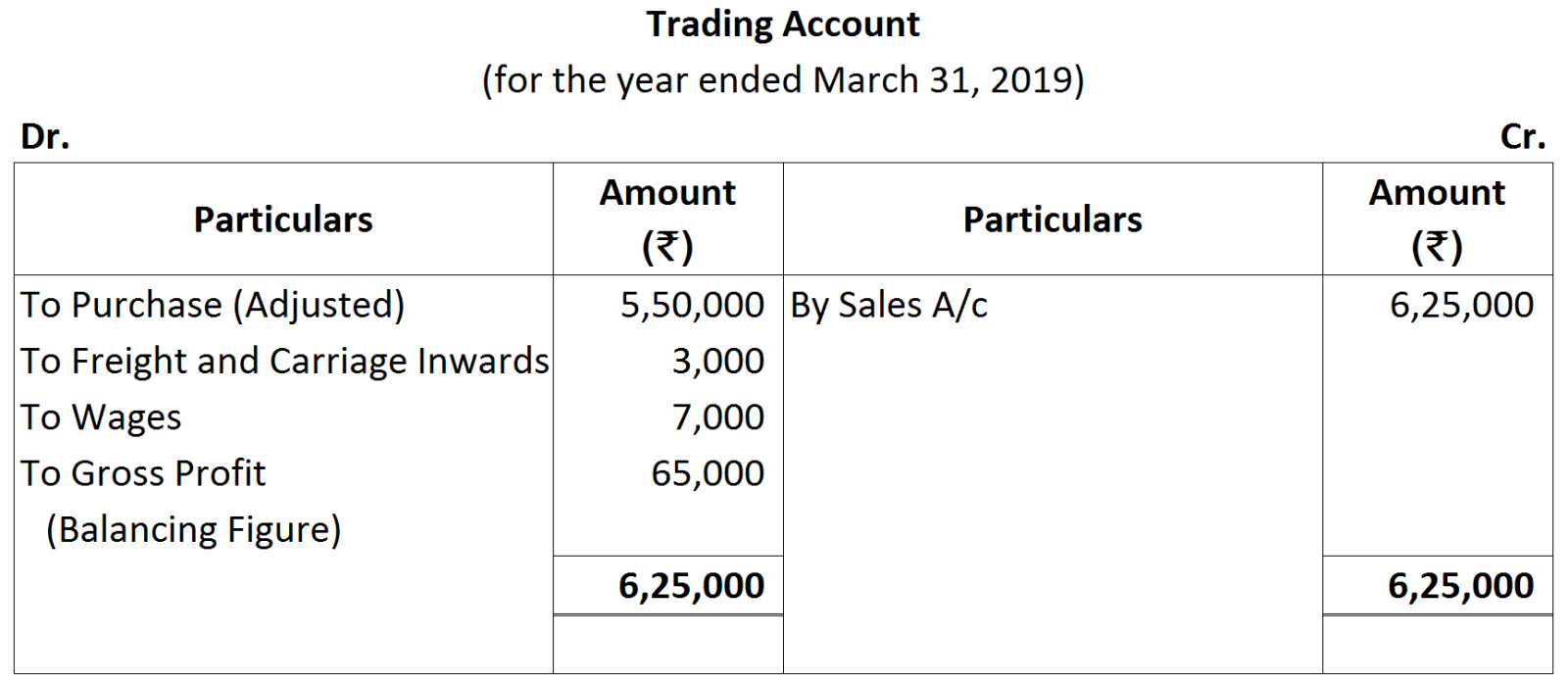

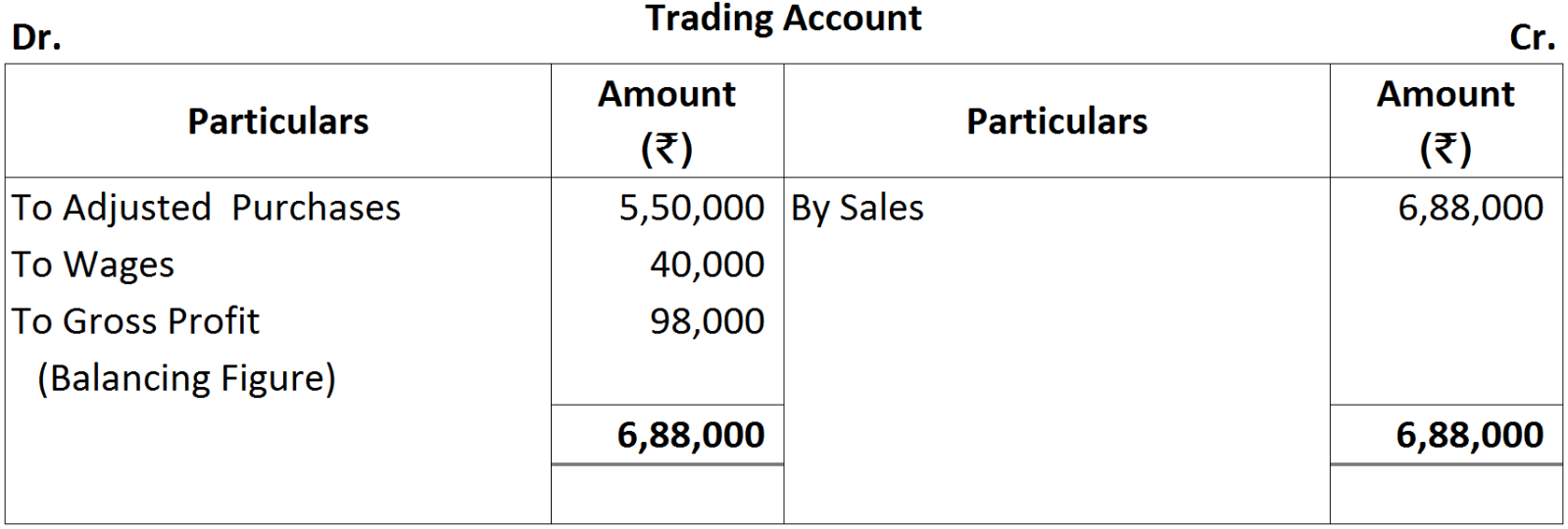

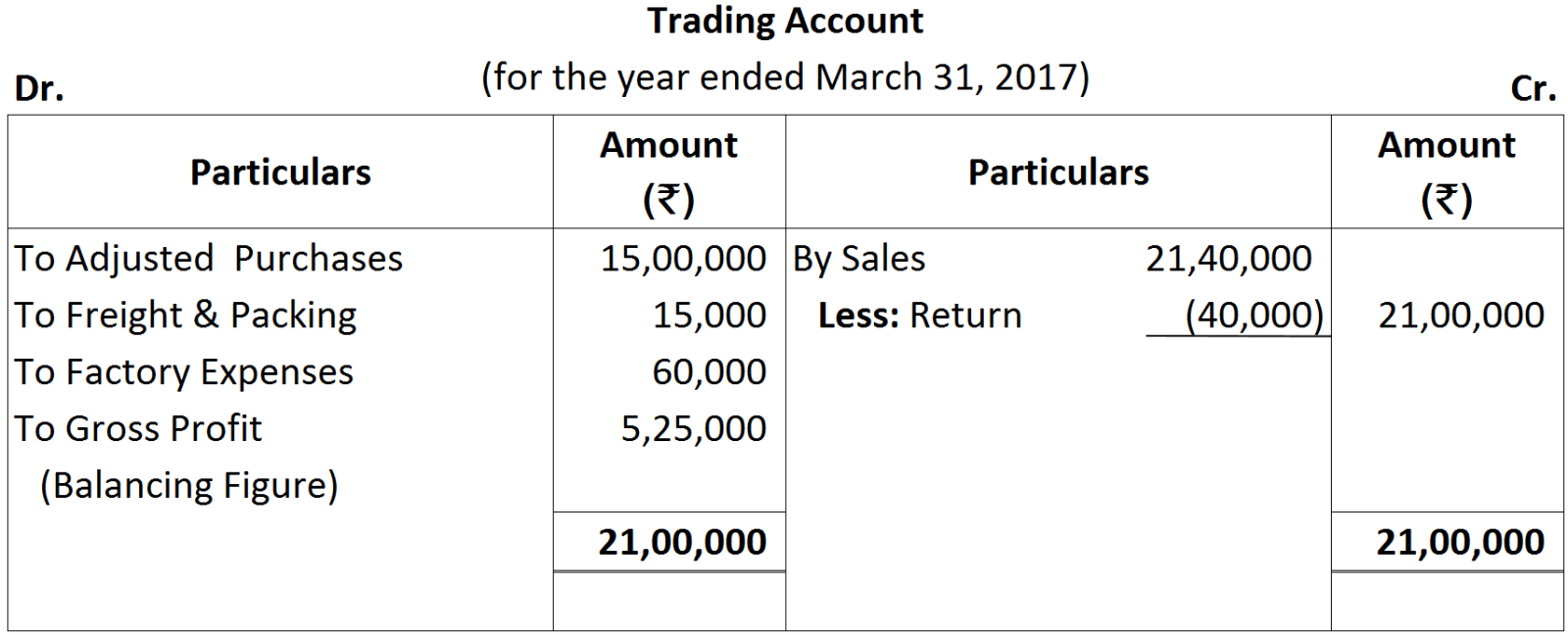

As adjusted purchases is given, it means opening and closing stock are already adjusted. So, these two stocks will not be considered while calculating Gross Profit.

As adjusted purchases is given, it means opening and closing stock are already adjusted. So, these two stocks will not be considered while calculating Gross Profit.

Note: Closing Stock will not be shown on the Credit side of Trading Account since it has already been adjusted while calculating adjusted purchases.

Note: Closing Stock will not be shown on the Credit side of Trading Account since it has already been adjusted while calculating adjusted purchases.