Question 13 Marks

Write notes on the following:

- Accrued Income.

- Unearned Income.

- Provision for Doubtful Debts.

Answer

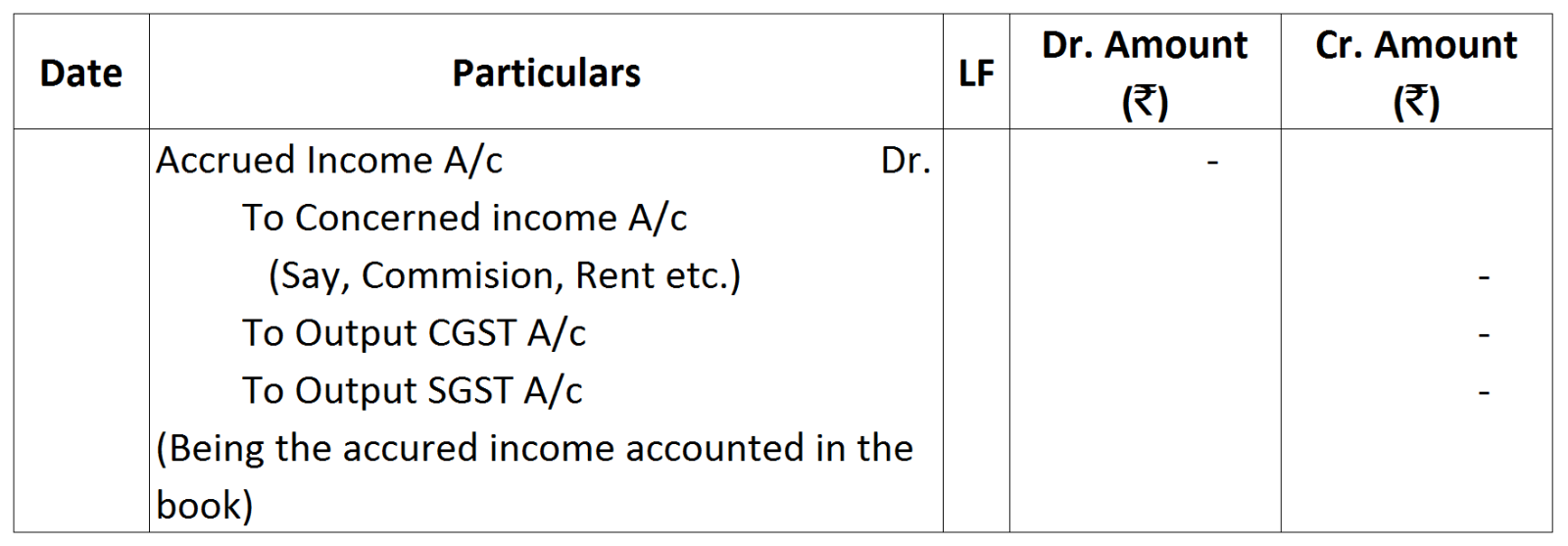

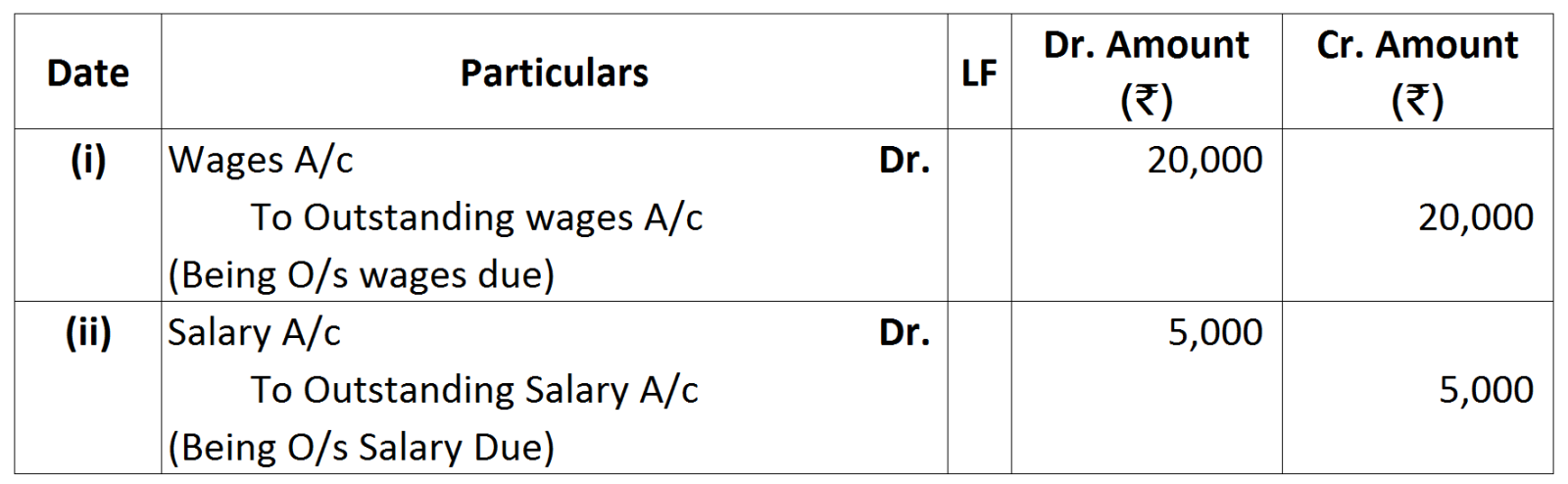

View full question & answer→- Accrued Income: It is quite common that certain items of income such as interest on securities, commission, rent etc., are earned during the current year but have not been actually received by the end of the current year.

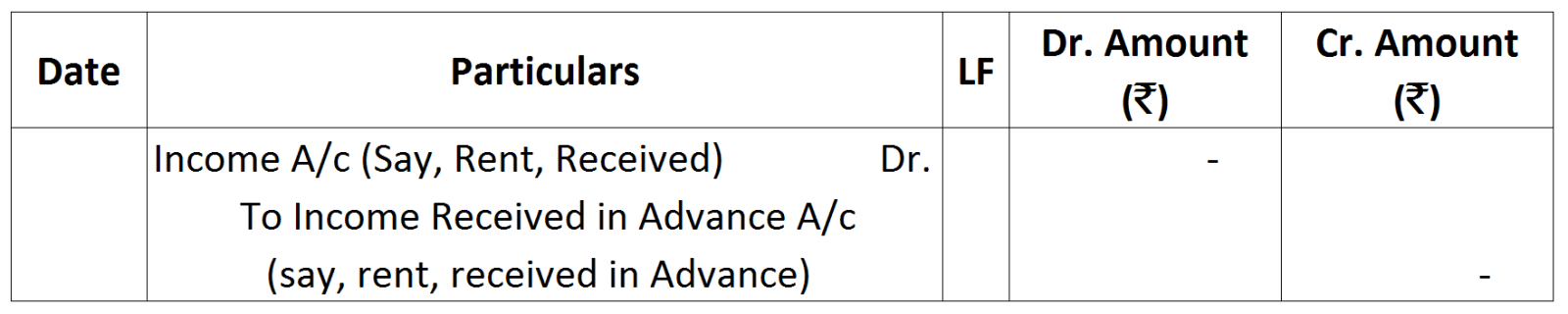

- Unearned Income: It may also happen that a certain income is received in the current year but the whole amount of it does not belong to the current year. Such portion of this income which belongs to the next year is known as 'Unearned Income' or 'Income received but not earned'.

- Provision for Doubtful Debts: Even after deducting the amount of actual bad-debts from the debtors, the list of debtors at the end of the year may include some debts which are either bad or doubtful. As the amount of actual loss on account of current year bad-debts would be known only in the next year when the amount is realised from debtors, a provision is created to cover any possible loss on account of bad-debts likely to occur in future. Such a provision is created at a fixed percentage on debtors every year and is called “Provision for Bad and Doubtful Debts'.