MCQ 11 Mark

The adjustment to be made for provision for doubtful debt is $........$

- A

Credit profit and loss account and deduct the provision from the debtors.

- ✓

Debit profit and loss account deduct the provision from debtors.

- C

Credit profit and loss account and add the provision to debtors.

- D

Debit profit and loss account and add the provision to debtors.

AnswerCorrect option: B. Debit profit and loss account deduct the provision from debtors.

The adjustment for the provision for doubtful debt

Adjustment $1:$ Provision for doubtful debt is debited to Profit and loss A/c.

Adjustment $2:$ Provision for doubtful debt is deducted from debtors in balance sheet.

View full question & answer→MCQ 21 Mark

Expenses paid but not accounted as expenses means $.........$

- A

- ✓

Expenses paid in advance but services yet to be enjoyed.

- C

- D

AnswerCorrect option: B. Expenses paid in advance but services yet to be enjoyed.

An accrued expense is a liability that represents an expense that has been recognized but not yet paid. Not every transaction requires an immediate exchange of cash for goods and services. Sometimes, especially when there is a prolonged history of ongoing transactions between two parties, formal invoicing and payment requirements can occur after the expense associated with the transaction has been recognized.

View full question & answer→MCQ 31 Mark

Bad debt amount should be credited to the $.......$ account.

AnswerBad debts are the amount due from the debtors which are either declared as bad or doubtful. Bad debt is a loss to the organization and should be debited to profit $\&$ loss account as indirect expenses by reducing the amount of debtors.

Accounting entry to be passed on account of bad debt is as under:

Bad Debts A/c, Dr.

To sundry Debtors

View full question & answer→MCQ 41 Mark

Expenses incurred but not yet paid are accounted because of $(c)$ Matching Principle.

View full question & answer→MCQ 51 Mark

Interest on capital is $......$ on business.

AnswerSometimes, the proprietor may like to know the profit made by the business after providing for interest on capital. In such a situation, interest is calculated at a given rate of interest on capital as at the beginning of the accounting year.

If however, any additional capital is brought during the year, the interest may also be computed on such amount from the date on which it is brought into business.

Such interest is treated as expense for the business and the following entry is recorded in the books of account:

Interest on Capital A/c Dr.

To Capital A/c

View full question & answer→MCQ 61 Mark

Provision for Discount on Debtors is provided on:

- A

Debtors that are doubtful of recovery.

- ✓

Debtors that are not doubtful of recovery.

- C

On both $(a)$ and $(b).$

- D

AnswerCorrect option: B. Debtors that are not doubtful of recovery.

View full question & answer→MCQ 71 Mark

Which of the following transactions is of capital nature?

- ✓

Purchase of a truck by a company

- B

Replacement of old types and tubes

- C

Yearly premium to insure the truck

- D

Cost of repair of the truck

AnswerCorrect option: A. Purchase of a truck by a company

Capital expenditure is a money spent by a business or organization on acquiring or maintaining fixed assets, such as land, buildings, and equipment.

Hence, Purchase of a truck by a company is a capital expenditure.

View full question & answer→MCQ 81 Mark

Business paid to Mr. A $₹ 50,000$ as salary on $25^{th}$ March, $2011$. Mr. A went to bank to deposit cheque in his account on $3^{rd}$ April, $2011.$ What is the entry to be passed in the Balance Sheet on the date of final accounts?

- ✓

- B

Bank A/c Dr. To O/s Salary A/c.

- C

Salary A/c Dr. To O/s Salary A/c.

- D

View full question & answer→MCQ 91 Mark

- ✓

Income received in advance.

- B

Income earned but not received.

- C

Income of the firm in the year of receipt.

- D

AnswerCorrect option: A. Income received in advance.

View full question & answer→MCQ 101 Mark

Goods distributed to employees free of cost is debited to:

- ✓

- B

Sales Promotion Expenses.

- C

- D

View full question & answer→Question 111 Mark

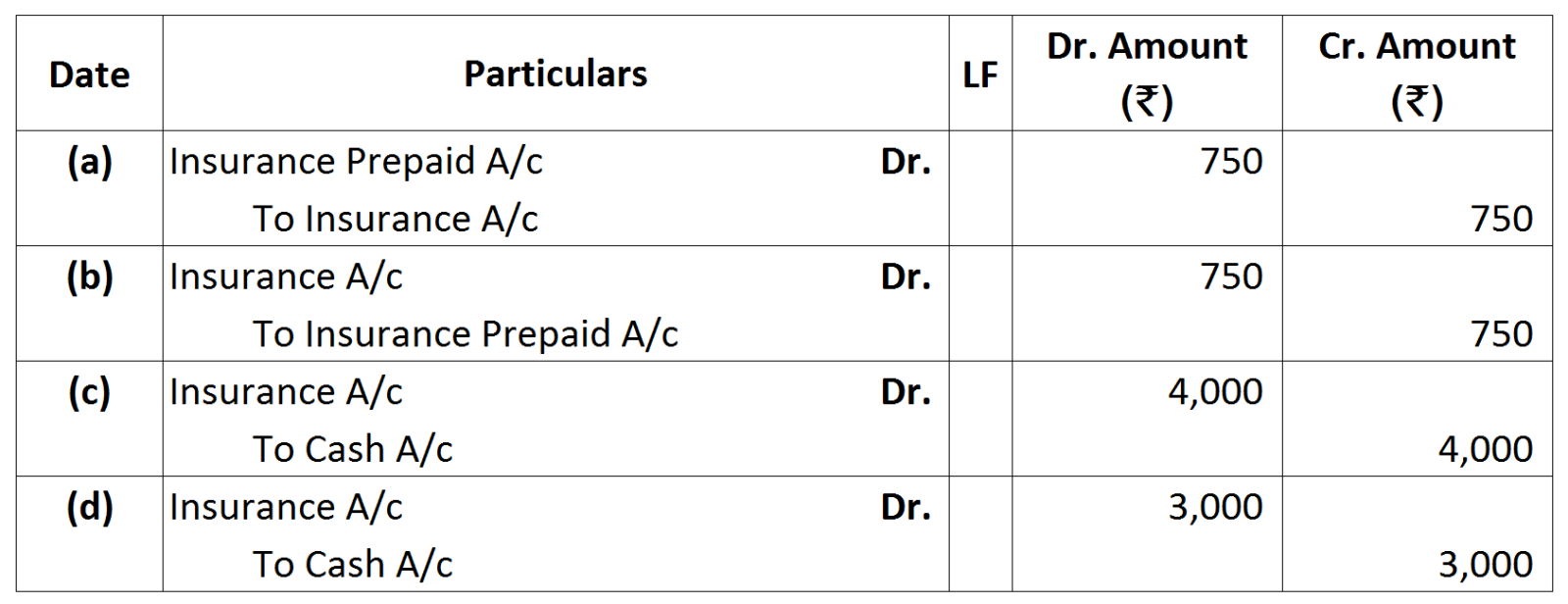

Insurance paid $₹ 4,000 ($including premium of $₹ 3,000$ per annum paid upto $30^{th}$ June, $2017)$. What will be the adjusting closing entry necessary as on $31^{st}$ March, $2017:$

View full question & answer→MCQ 121 Mark

The interest on partners capital accounts is to be credited to $..........$

- A

- B

- C

- ✓

Partner's Capital Account

AnswerCorrect option: D. Partner's Capital Account

Interest on partner's capital is an amount at an agreed rate of interest which is credited to a partner based on the amount of capital contributed by him/her.

Interest on partner's capital is an expense to the firm and hence debited to profit and loss appropriation A/c. On the other hand it is an income for partners and hence credited to partner's capital A/c.

View full question & answer→MCQ 131 Mark

Accrued income is shown $........$ of balance sheet.

AnswerAccrued income is usually listed in the current assets section of the balance sheet in an accrued receivables account.

View full question & answer→MCQ 141 Mark

AnswerCorrect option: B. Income received in advance.

View full question & answer→MCQ 151 Mark

Trading Account is prepared to know:

- ✓

- B

- C

Both $(a)$ and $(b).$

- D

View full question & answer→MCQ 161 Mark

Types of Account shown in Balance Sheet are $......$

- A

- B

- ✓

- D

Real, Nominal and Personal.

View full question & answer→MCQ 171 Mark

Non $-$ provision for outstanding bonus amounting to $Rs.50,000$ of the employees will lead to $......$

- A

Suppression of profit by $Rs.50,000.$

- ✓

Over statements of profit by $Rs.50,000.$

- C

Overvaluation of inventory

- D

AnswerCorrect option: B. Over statements of profit by $Rs.50,000.$

View full question & answer→MCQ 181 Mark

Wages paid for installation of machine is added to the cost of machine because of:

MCQ 191 Mark

New $\text{R.D.D.}$ is to be deducted from $.......$

AnswerIt is quite possible that whole of he amount of debtors may not be realised in future. However, it is not possible to accurately know the amount of such bad debts. Hence, a reasonable estimate of such loss is made and provided for the same. Such provision is called provision for bad debts and is created by debiting profit and loss account. The following journal entry is recorded as:

Profit and Loss A/c Dr.

To Provision for Doubtful Debts A/c

New Reserve for Doubtful Debts is deducted from the debtors on the asset side of the balance sheet.

View full question & answer→MCQ 201 Mark

Interest is calculated at a given rate of interest on capital as at the $......$ of the accounting year.

AnswerCorrect option: D. Both $A\ \&\ C$

Sometimes, the proprietor may like to know the profit made by the business after providing for interest on capital. In such a situation, interest is calculated at a given rate of interest on capital as at the beginning of the accounting year. If however, any additional capital is brought during the year, the interest may also be computed on such amount from the date on which it is brought into the business. Such interest is treated as expense for the business on debit side of profit and loss account.

View full question & answer→MCQ 211 Mark

Adjustment entries are those which are passed $........$

- A

- B

At the beginning of the year

- ✓

For adjustment of prepaid and outstanding expenses/income.

- D

AnswerCorrect option: C. For adjustment of prepaid and outstanding expenses/income.

Adjustment entries are the entries which are passed at the end of each accounting period to adjust the nominal and other accounts so that correct net profit or net loss is indicated in profit and loss account and balance sheet may also represent the true and fair view of the financial condition of the business.

View full question & answer→MCQ 221 Mark

Salaries and Wages Account is shown in:

MCQ 231 Mark

There are certain items which are not recorded on day-to-day basis such as $.........$

- A

- B

- ✓

Depreciation on fixed assets

- D

AnswerCorrect option: C. Depreciation on fixed assets

Depreciation on fixed assets, interest on capital, etc. are not recorded on day-to-day basis. These are adjusted at the time of preparing financial statements.

View full question & answer→MCQ 241 Mark

Prepaid expenses is shown under $..........$ side of balance side.

AnswerGenerally, the amount of prepaid expenses that will be used up within one year are reported on a company's balance sheet as a current asset. As the amount expires, the current asset is reduced and the amount of the reduction is reported as an expense on the income statement.

View full question & answer→MCQ 251 Mark

Rent prepaid a/c appearing in the trial balance is $.........$

- A

Shown on the liability side of balance sheet

- ✓

Shown on the assets side of the balance sheet

- C

Shown on debit side of profit and loss A/c

- D

Credited to profit and loss A/c

AnswerCorrect option: B. Shown on the assets side of the balance sheet

Rent prepaid a/c appearing in the trial balance is debit of trial balance.

Prepaid rent is an asset which is shown under the current asset of balance sheet.

View full question & answer→MCQ 261 Mark

Reserve for doubtful debts appearing in the trial balance should be $........$

AnswerCorrect option: D. Both $A$ and $C$

Reserve for doubtful debt is created on conservatism concept. Conservatism concept assumes that all the anticipated losses should be recorded in books of account to know the true profitability.

Adjustment for Reserve for doubtful debts is to be done while preparing the profit $\&$ loss account.

If the reserve is appearing in trial balance, that means an adjustment entry has already been passed in books of account. This has to be shown in credit side of profit $\&$ loss account and will appear in liability side of balance sheet.

View full question & answer→MCQ 271 Mark

Prepaid Insurance appearing in the Trial Balance is shown in the Balance Sheet on the assets side because of:

MCQ 281 Mark

Income received in advance is deducted from the income because of:

- A

Revenue Recognition Concept.

- B

- ✓

- D

View full question & answer→MCQ 291 Mark

Reserve for doubtful debts is made out of $.......$ profit.

AnswerIt is quite possible that the whole amount may not be realised in future. However, it is not possible to actually know the amount of such debts. Hence, a reasonable estimate of such loss is made and provided the same. Such provision is called provision for bad debts and is created by debiting profit and loss account. The following journal entry is recorded as:

Profit and Loss A/c Dr.

To Provision for Doubtful Debts A/c

It is shown as a deduction from the debtors on the asset side of the balance sheet. Reserve for doubtful debts is made out of revenue profit.

View full question & answer→MCQ 301 Mark

Interest on capital is calculated on $........$

AnswerCorrect option: D. Both $A\ \&\ B$

Interest on capital is to be calculated on the capitals at the beginning for the relevant period. If there is any additional capital introduced or capital withdrawn during the year, it will cause change in the capitals and interest is to be calculated proportionately on the changed capitals for the relevant period.

Interest on capital $=$ Amount of capital $\times$ Rate of interest per annum $\times$ Period of interest

View full question & answer→MCQ 311 Mark

The debts written off as bad, if subsequently recovered are credited to $.......$

AnswerA bad debt recovery is a payment received after it has been designated as uncollectible.If the original entry was instead a credit to accounts receivable and a debit to bad debt expense $($the direct write$-$off method$)$, then reverse this original entry.

View full question & answer→MCQ 321 Mark

Which of the following is an example of an adjusting entry?

- A

Recording the purchase of goods an account.

- ✓

Recording depreciation of a truck.

- C

Recording the billing of customers for services rendered.

- D

Recording the payment of wages to employees.

AnswerCorrect option: B. Recording depreciation of a truck.

Adjusting entries refers to a set of journal entries recorded at the end of the accounting period to have an updated and accurate balances of all the accounts. Adjusting entries are mere application of the accrual basis of accounting and not based on transactions. For example, accrued interest on loan, depreciation, writing off prepaid expenses, etc.

View full question & answer→MCQ 331 Mark

Which of the following statements is not true?

- A

It is not true that all partners can have limited liability in a limited partnership.

- B

Capital contributions do not have to be equal from each partner.

- C

A minor has a right to access and inspect books of accounts of partnership firm in which he is partner.

- ✓

Interest on capital is a reward for the different amounts of work partners may perform.

AnswerCorrect option: D. Interest on capital is a reward for the different amounts of work partners may perform.

Interest will be allowed to each partner on the capital contributed by him . Interest on capital of the partners is calculated for the relevant period for which the amount of capital has been used in the business. Capital introduced or withdrawn by a partner during the accounting year has to be taken for the purpose of calculation and definitely is not a reward for the partners.

View full question & answer→MCQ 341 Mark

Providing Interest on Capital $........$ net profit.

AnswerInterest on capital is a charge on the profits of a firm and it decreases the net available profit for appropriation.

View full question & answer→MCQ 351 Mark

View full question & answer→MCQ 361 Mark

An adjusting entry to accrued wages earned but not yet paid is an example of $.......$

- A

Adjusting recorded costs with the appropriate accounting periods.

- B

Adjusting recorded revenue with the appropriate accounting periods.

- ✓

Reflecting unrecorded expenses incurred during the accounting period.

- D

Reflecting unrecorded revenue earned during the accounting period.

AnswerCorrect option: C. Reflecting unrecorded expenses incurred during the accounting period.

Unpaid Wages Under the accrual basis of accounting, unpaid wages that have been earned by employees but have not yet been recorded in the accounting records should be entered or recorded through an accrual adjusting entry which will: Debit Wages Expense. Credit Wages Payable or credit Accrued Wages Payable.

View full question & answer→MCQ 371 Mark

A machine was purchased in Bihar. During transit the machine was damaged and the cost of repairs incurred is $₹ 20,000$. This expense is treated as:

- ✓

- B

- C

Deferred Revenue expense.

- D

View full question & answer→MCQ 381 Mark

Income received in advance will be deducted from $......$

AnswerCorrect option: B. Credit side of profit $\&$ loss account

Sometimes, a certain income is received but the whole amount of it does not belong to the current period. The portion of income which belongs to the next accounting period is termed as income received in advance or an Unearned Income. Income received in advance is adjusted by recording the following entry:

Concerned Income A/c Dr.

To Income Received in Advance A/c

The effect of this entry will be that the balance in the income account will be equal to the amount of income earned for the current accounting period, and the new account of income received in advance will be shown as a liability in the balance sheet. The amount of income received in advance will be deducted from the credit side of profit and loss account.

View full question & answer→MCQ 391 Mark

Financial capital is also referred to $.........$

AnswerFinancial capital is the money used to help pay for the acquisition of plants, equipment, and other items needed to build products or offer services. Hence, it can be referred to money capital.

View full question & answer→MCQ 401 Mark

Salary outstanding A/c $Rs. 5000$ appears in the trial balance along with salary A/c of $Rs. 15000$. How this will be accounted for in the books of accounts:

- ✓

Salary outstanding A/c $Rs. 5000$ to be shown in the balance sheet on the liability side.

- B

Salary A/c to be debited to profit and loss A/c by $Rs. 20,000.$

- C

Salary A/c to be debited to profit and loss A/c by $Rs. 5,000.$

- D

Salary outstanding A/c $Rs. 5000$ to be credited to profit and loss A/c.

AnswerCorrect option: A. Salary outstanding A/c $Rs. 5000$ to be shown in the balance sheet on the liability side.

As Salary outstanding A/c is appearing inside the trial balance along with salary a/c that means SalaryOutstanding have just one treatment.

Salary Outstanding is a Current Liability for the Business therefore it will appear in the Liabilities side of the Balance Sheet.

Therefore, Salary outstanding A/c $Rs. 5000$ will be to be shown in the balance sheet on the liability side.

View full question & answer→MCQ 411 Mark

The recording of wages earned but not yet paid is an example of an adjustment that $..........$

- A

Apportions revenues between two or more periods

- ✓

Recordings an accrued expense

- C

Recordings an unrecorded revenue

- D

AnswerCorrect option: B. Recordings an accrued expense

The expenses accrued but not paid is an outstanding expense and is a liability of the business.

View full question & answer→MCQ 421 Mark

If there is no partnership deed then interest on capital will be charged at $.......$ p.a.

- A

$6\%$

- B

$8\%$

- C

$9\%$

- ✓

$\text{NIL}$

AnswerCorrect option: D. $\text{NIL}$

When there is no partnership deed then interest on capital will not be charged. There will be no interest provided on the capital.

View full question & answer→MCQ 431 Mark

'A three years premium paid on a fire insurance policy' should be classified as $......$

AnswerA prepaid expense refers to an amount that a company has paid and a portion or all of it will be an expense in a later accounting period.

A prepaid expense can be recorded initially as an expense or as a current asset.

View full question & answer→MCQ 441 Mark

If prepaid rent appears in trial balance, while preparing the final accounts it will be shown in $......$

AnswerCorrect option: C. Assets side of Balance Sheet.

Prepaid Rent A/c is shown on the Assets side $($under current assets$)$ in the Balance Sheet. It reports the amount of future rent expense that was paid in advance of the rental period.

View full question & answer→MCQ 451 Mark

Accrued Income, if given in the Trial Balance is shown in:

- A

Trading Account, as addition to the income.

- B

Profit and Loss Account, as addition to the income.

- C

Profit and Loss Account, as addition to the income and in the Balance Sheet, as an asset.

- ✓

Balance Sheet as an asset.

AnswerCorrect option: D. Balance Sheet as an asset.

View full question & answer→MCQ 461 Mark

Amount earned during the current accounting year but have not been actually received by the end of the same year is known as $......$

AnswerIt may happen that certain items of income such as interest on loan, commission, rent, etc. are earned during the current accounting year but have not been actually received by the end of the same year. Such incomes are known as accrued income, outstanding income or incomes earned but not yet received. Common examples of such incomes are commission receivable, income on investments due but not yet received etc. The adjusting entry for accrued income is:

Accrued Income A/c Dr.

To Concerned Income A/c

The amount of accrued income will be added to the related income in the profit and loss account and the new account of accrued income will appear on the asset side of the balance sheet.

View full question & answer→MCQ 471 Mark

Interest on advance money provided by the Partner can be paid from $.......$

- A

- B

- ✓

Both $(a)$ and $(b)$

- D

From the money provided by Central Government

AnswerCorrect option: C. Both $(a)$ and $(b)$

View full question & answer→MCQ 481 Mark

Accrued income is also called $.........$

AnswerIt may happen that certain items of income, such as interest on loan, commission, rent, etc., are earned during the current accounting year but have not been received by the end of the same year. Such incomes are known as accrued income. It is the income that has been earned during a particular accounting period, also known as outstanding income.

Examples include accrued interest, accrued rent (to be received), etc. Accrued income is recorded in the books at the end of an accounting period to show the true numbers of a business.

View full question & answer→MCQ 491 Mark

A prepayment of insurance premium will appear in the Balance Sheet and in the Insurance Account respectively as.

- A

A liability and a debit balance

- ✓

An asset and a debit balance

- C

An asset and a credit balance

- D

AnswerCorrect option: B. An asset and a debit balance

A current asset which indicates the cost of the insurance contract $($premiums$)$ that have been paid in advance. It represents the amount that has been paid but has not yet expired as of the balance sheet date. A related account is Insurance Expense, which appears on the income statement and shown on balance sheet as asset.

View full question & answer→MCQ 501 Mark

Income received in advance, if given outside the Trial Balance is shown in:

- A

Trading Account, as deduction from the income.

- B

Profit and Loss Account, as deduction from the income.

- ✓

Profit and Loss Account, as deduction from the expense and in the Balance Sheet, as a liability.

- D

Balance Sheet as a liability.

AnswerCorrect option: C. Profit and Loss Account, as deduction from the expense and in the Balance Sheet, as a liability.

View full question & answer→