Question 13 Marks

What is the use of Financial Statements for Potential Investors?

Answer

View full question & answer→Investors: They can assess the short-term and long-term financial soundness and earning capacity of the business with the help of financial statements. They can also study the trend of sales, trend of profits, shortcomings and the prospects of future growth of the enterprise.

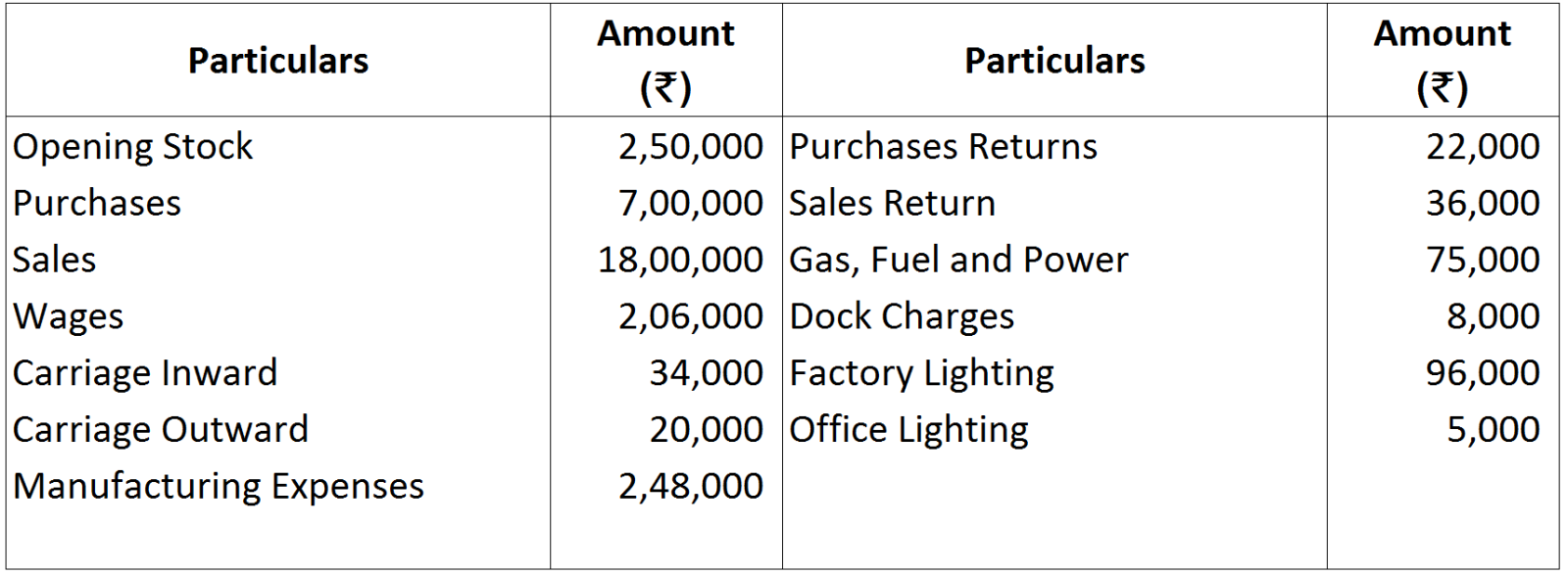

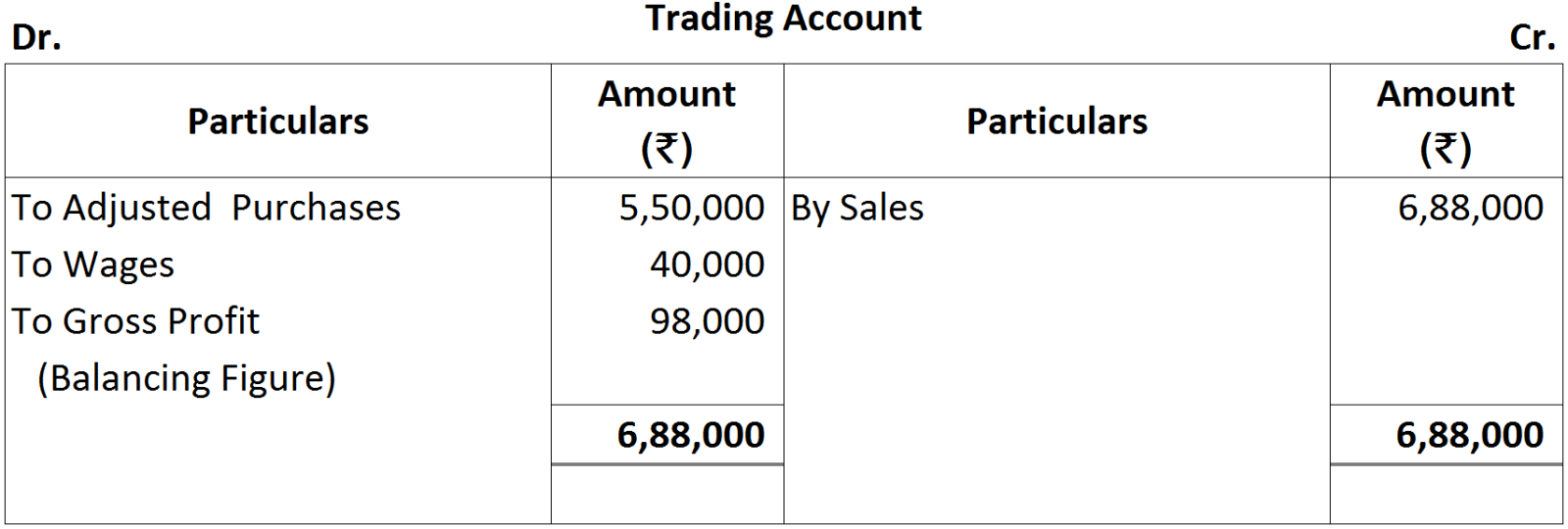

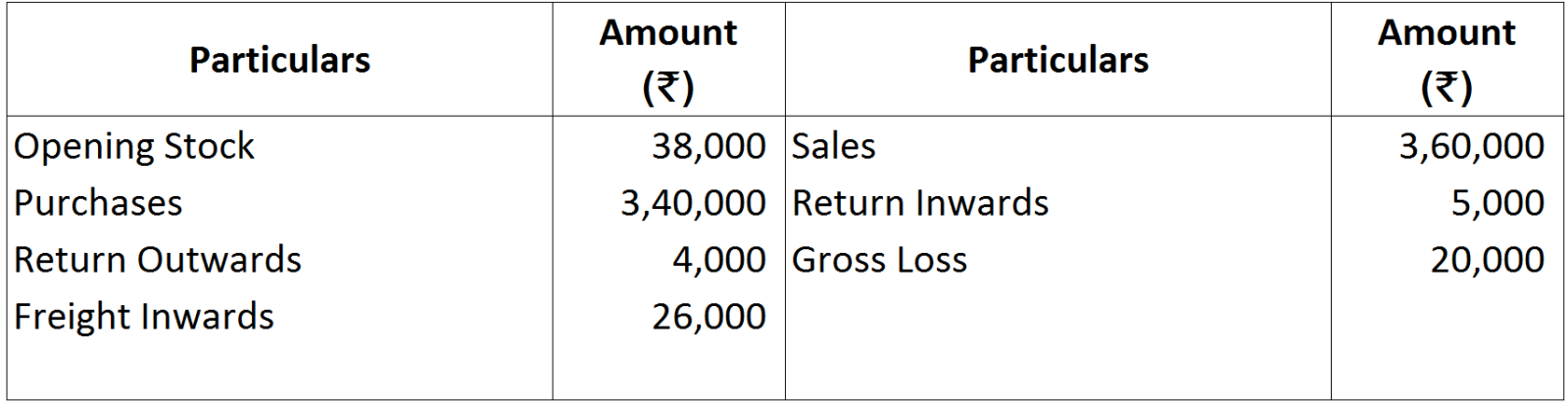

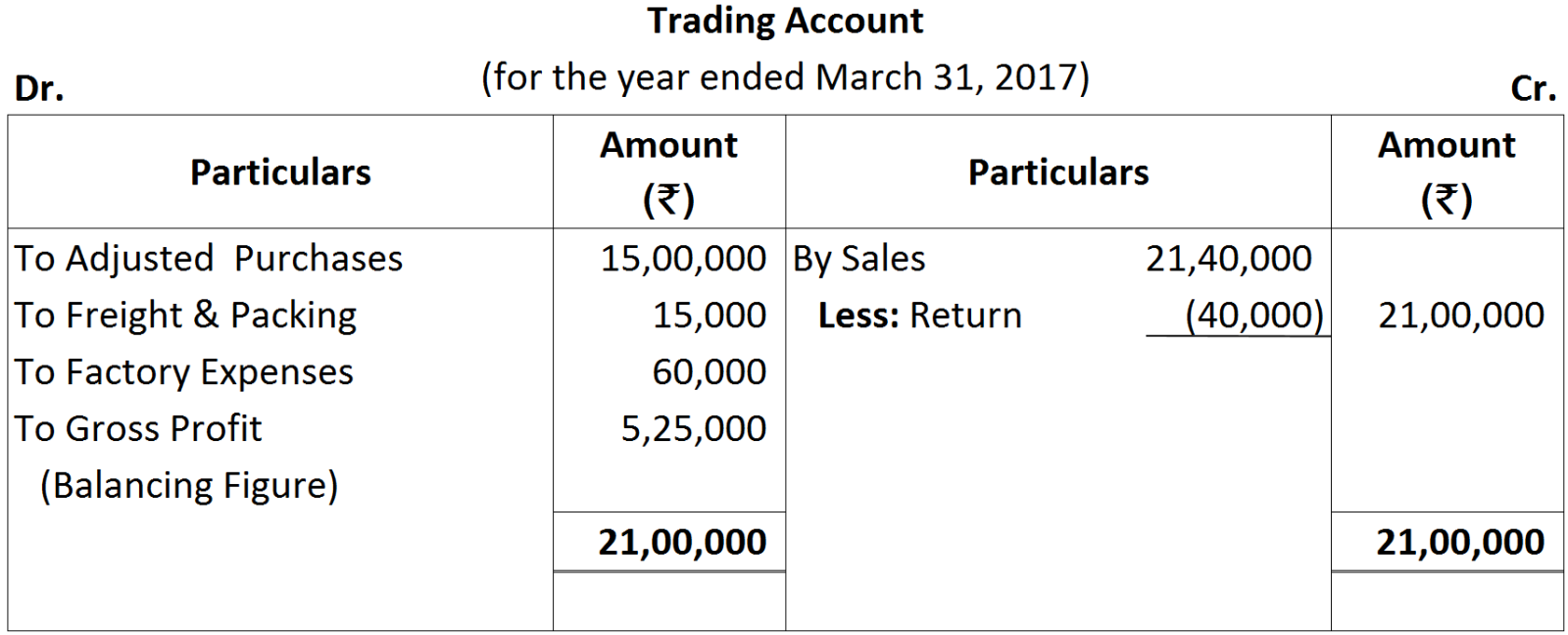

As adjusted purchases is given, it means opening and closing stock are already adjusted. So, these two stocks will not be considered while calculating Gross Profit.

As adjusted purchases is given, it means opening and closing stock are already adjusted. So, these two stocks will not be considered while calculating Gross Profit.

Note: Closing Stock will not be shown on the Credit side of Trading Account since it has already been adjusted while calculating adjusted purchases.

Note: Closing Stock will not be shown on the Credit side of Trading Account since it has already been adjusted while calculating adjusted purchases.