Question 16 Marks

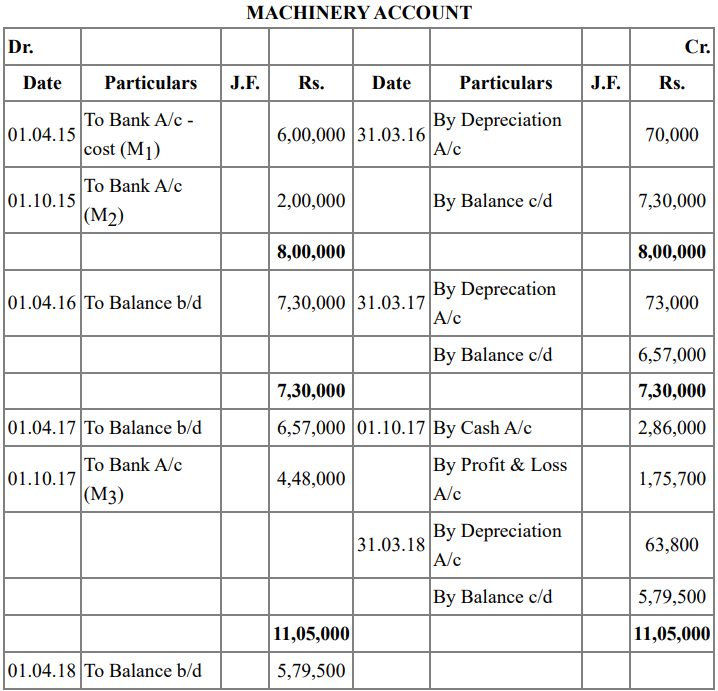

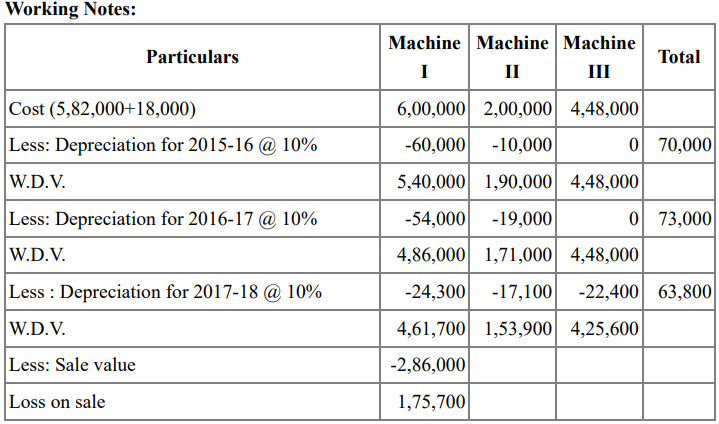

A firm purchased on 1st April 2015 certain machinery for Rs. $5,82,000$ and spent Rs. 18,000 on its installation. On 1st October 2015, additional machinery costing Rs. $2,00,000$ was purchased. On 1st October 2017, the machinery purchased on 1st April 2015 was auctioned for Rs.2,86,000 plus CGST and SGST @ $6 \%$ each and new machinery for Rs. $4,00,000$, plus IGST @ $12 \%$ was purchased on the same date. Depreciation was provided annually on 31st March at the rate of $10 \%$ on the Written Down Value Method. Prepare the Machinery Account for the three years ended 31st March 2018.

View full question & answer→