MCQ 11 Mark

At a price below the equilibrium price, there is:

MCQ 21 Mark

The price at which quantity supplied and quantity demanded are equal is termed as:

- ✓

- B

- C

Both $(a)$ and $(b).$

- D

View full question & answer→MCQ 31 Mark

When both demand and supply decreases in the same proportion, then equilibrium price will:

MCQ 41 Mark

Imperfect competition is a type of market structure showing some but not all feature of competitive market. Which of the following is/ are imperfect competition?

- A

- B

Monopolistic competition.

- C

- ✓

Both $(a)$ and $(b).$

AnswerCorrect option: D. Both $(a)$ and $(b).$

View full question & answer→MCQ 51 Mark

Which of the following is not an essential condition of pure competition?

- A

Large number of buyers and sellers.

- B

- C

Freedom of entry and exit.

- ✓

Absence of transport cost.

AnswerCorrect option: D. Absence of transport cost.

View full question & answer→MCQ 61 Mark

An attempt to set a minimum price for a good is called a:

MCQ 71 Mark

Marginal revenue of a firm is constant throughout under:

MCQ 81 Mark

If price is forced to stay below equilibrium price $.........$

- A

- ✓

- C

either $(a)$ or $(b).$

- D

View full question & answer→MCQ 91 Mark

View full question & answer→MCQ 101 Mark

Differentiated but close substitutes exist under:

- A

- B

- ✓

Monopolistic competition.

- D

AnswerCorrect option: C. Monopolistic competition.

View full question & answer→MCQ 111 Mark

$.........$ is a situation of the market in which demand for a commodity is exactly equal to its supply corresponding to a particular price.

View full question & answer→MCQ 121 Mark

Assume that in the market for a good $Z$ there is a simultaneous increase in demand and the quantity supplied. The result will be:

- A

An increase in equilibrium price and quantity.

- B

A decrease in equilibrium price and quantity.

- ✓

An increase in equilibrium quantity and uncertain effect on equilibrium price.

- D

A decrease in equilibrium price and increase in equilibrium quantity.

AnswerCorrect option: C. An increase in equilibrium quantity and uncertain effect on equilibrium price.

View full question & answer→MCQ 131 Mark

Which is the best example of monopoly market?

MCQ 141 Mark

Under monopoly, monopolist tries to increase his profits by restricting supply of his product and fixing:

AnswerAs a price maker, a monopolist has full control over price. Thus, he charges high price to maximise the profits and can restrict supply of his product.

View full question & answer→MCQ 151 Mark

Monopolist can determine $.........$

- A

- B

- ✓

both $(a)$ and $(b).$

- D

AnswerCorrect option: C. both $(a)$ and $(b).$

View full question & answer→MCQ 161 Mark

Under what condition, equilibrium price will increase and equilibrium quantity will decrease?

AnswerDemand curve remain unchanged, if there is a decrease in supply, supply curve and equilibrium point will shift leftwards. As a result, equilibrium price will increase and equilibrium quantity will decrease

View full question & answer→MCQ 171 Mark

An increase in demand with unchanged supply leads to $.........$

- A

rise in equilibrium price and fall in equilibrium quantity.

- B

fall in both equilibrium price and quantity.

- ✓

rise in both equilibrium price and quantity.

- D

fall in equilibrium price and rise in equilibrium quantity.

AnswerCorrect option: C. rise in both equilibrium price and quantity.

View full question & answer→MCQ 181 Mark

Rent control is an example of:

MCQ 191 Mark

If in a oligopoly, the fir1ms are selling homogeneous products, then the oligopoly firm is called:

MCQ 201 Mark

From the following, in which market, there is a free entry and exit of firms?

- A

- B

Monopolistic competition and monopoly.

- C

Perfect competition and oligopoly.

- ✓

Perfect competition and monopolistic competition.

AnswerCorrect option: D. Perfect competition and monopolistic competition.

View full question & answer→MCQ 211 Mark

Under perfect competition, what is the relationship between Price $P$ , Average Revenue and Marginal Revenue?

- ✓

$P = =$

- B

$P > >$

- C

$P < <$

- D

$P = >$

AnswerCorrect option: A. $P = =$

View full question & answer→MCQ 221 Mark

Firm in a monopolistic market has $.........$ control over price.

View full question & answer→MCQ 231 Mark

What is the impact of change in supply on market equilibrium when demand is perfectly inelastic?

- A

Both equilibrium price and equilibrium quantity will change.

- B

Both equilibrium price and equilibrium quantity will not change.

- C

Equilibrium price remains same and equilibrium quantity will change.

- ✓

Equilibrium price will change and equilibrium quantity remains same.

AnswerCorrect option: D. Equilibrium price will change and equilibrium quantity remains same.

In this case, quantity will remain unchanged, only price will increase with fall in supply and vice$-$versa.

View full question & answer→MCQ 241 Mark

Under what condition, both equilibrium price and equilibrium quantity will decrease?

MCQ 251 Mark

When demand decreases and there is no shift in supply, the equilibrium price $.........$ and quantity $.........$

View full question & answer→MCQ 261 Mark

A seller cannot influence the market price under:

- ✓

- B

- C

Monopolistic competition.

- D

View full question & answer→MCQ 271 Mark

When supply decreases and there is no change in demand, then equilibrium price $.........$ and quantity $.........$

View full question & answer→MCQ 281 Mark

- A

A minimum price that a firm may charge for a good or service.

- B

Usually established by the manufacturer of a product.

- ✓

The maximum price that a firm may charge for a good or service.

- D

AnswerCorrect option: C. The maximum price that a firm may charge for a good or service.

View full question & answer→MCQ 291 Mark

Homogenous product means products are:

MCQ 301 Mark

Market which has a few large firms is $.........$

- ✓

- B

- C

monopolistic competition.

- D

View full question & answer→MCQ 311 Mark

Assume that consumers' incomes and the number of sellers in the market for goods A both decrease. Based upon this information, we can conclude, with certainty, that the equilibrium $.........$

View full question & answer→MCQ 321 Mark

In which market structure, price and output solution is indeterminate?

- ✓

- B

Monopolistic competition.

- C

- D

View full question & answer→MCQ 331 Mark

When both demand and supply increases in the same proportion then equilibrium price will:

MCQ 341 Mark

When demand decreases and there is no shift in supply, the equilibrium price $.........$ and quantity $.........$

View full question & answer→MCQ 351 Mark

When increase in demand in more than increase in supply, then equilibrium quantity will:

MCQ 361 Mark

When supply increases and there is no change in demand, then equilibrium price $.........$ and quantity $.........$

View full question & answer→MCQ 371 Mark

Demand curve of a firm is perfectly elastic under:

- ✓

- B

- C

Monopolistic competition.

- D

View full question & answer→MCQ 381 Mark

When demand increases with no change in supply, equilibrium price $.........$ and quantity $.........$

View full question & answer→MCQ 391 Mark

With a given supply curve a decrease in demand causes $.........$

- A

an overall decrease in price but an increase in equilibrium quantity.

- B

an overall increase in price but a decrease in equilibrium quantity.

- ✓

an overall decrease in price and a decrease in equilibrium quantity.

- D

no change in overall price but a reduction in equilibrium quantity.

AnswerCorrect option: C. an overall decrease in price and a decrease in equilibrium quantity.

View full question & answer→MCQ 401 Mark

There is inverse relation between price and demand for the product of a firm under:

- A

- B

Monopolistic competition only.

- ✓

Both under monopoly and monopolistic competition.

- D

Perfect competition only.

AnswerCorrect option: C. Both under monopoly and monopolistic competition.

View full question & answer→MCQ 411 Mark

- A

- ✓

- C

Monopolistic competition.

- D

Both perfect and monopolistic competition.

View full question & answer→MCQ 421 Mark

A firm is able to sell any quantity of a good at a given price. The firm’s marginal revenue will be:

- A

Greater than Average Revenue.

- B

Less than Average Revenue.

- ✓

Equal to Average Revenue.

- D

AnswerCorrect option: C. Equal to Average Revenue.

View full question & answer→MCQ 431 Mark

Selling cost is insignificant under:

- ✓

- B

- C

Monopolistic competition.

- D

View full question & answer→MCQ 441 Mark

Differentiated products is a characteristic of:

- A

Monopolistic competition only.

- B

- ✓

Both monopolistic competition and oligopoly.

- D

AnswerCorrect option: C. Both monopolistic competition and oligopoly.

View full question & answer→MCQ 451 Mark

If the market supply is less than the market demand of a commodity at a given price, it is called:

MCQ 461 Mark

When there is increase in demand and decrease in supply, equilibrium price:

MCQ 471 Mark

If market price is above equilibrium price, there exists a situation of:

- ✓

- B

- C

- D

Both $(a)$ and $(c).$

View full question & answer→Question 481 Mark

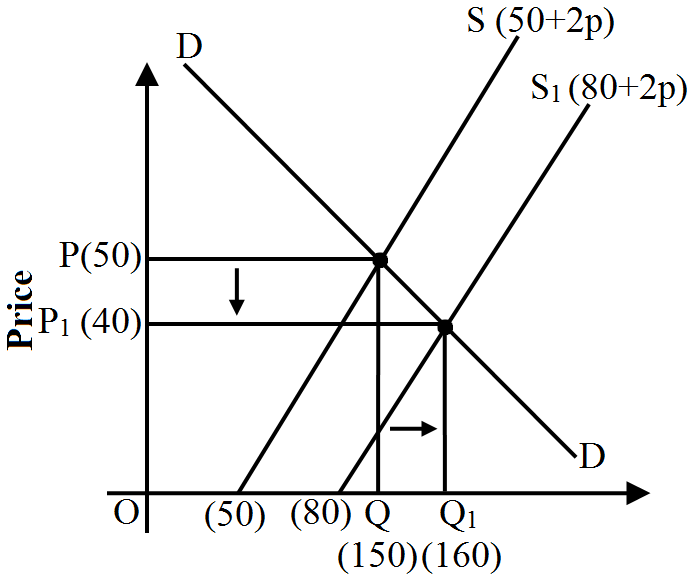

Suppose the demand and supply curve of a Commodity$-X$ is given by the following two equations simultaneously:

$Qd = 200 - p$

$Qs = 50 + 2p$

Find the equilibrium price and equilibrium quantity.

Suppose that the price of a factor of production producing the commodity has changed, resulting in the new supply curve given by the equation

$Qs' = 80 + 2p$

Analyse the new equilibrium price and new equilibrium quantity as against the original equilibrium price and equilibrium quantity.

AnswerWe know that the equilibrium price and quantity are achieved at;

$Qd = Qs$

$200 - p = 50 + 2p$

$(-) 3p = (-) 150$

Therefore, Equilibrium Price

$p = 50$

And, Equilibrium Quantity

$q = 200 - 50 = 150$ units

If the price of factor of production has changed, then under the new conditions;

$Qd = Qs$

$200 - p = 80 + 2p$

$(-) 3p = (-) 120$

Therefore, Equilibrium Price

$p = 40$

And, Equilibrium Quantity

$q = 200 - 40 = 160$ units

As, Intercept on $X-$axis of Supply equation, $Qs = 50 + 2p$ is $50 [$By Putting Price $(P) = 0]$ and Intercept on $X-$axis of supply equation, $Qs' = 80 + 2p$ is $80 [$By Putting Price $(P) = 0].$

Since, Intercept of $X-$axis Increases, Supply curve shifts Rightward as shown below:

So, equilibrium price falls from $₹ 50$ to $₹ 40$ and Equilibrium Quantity rises from $150$ units to $160$ units. View full question & answer→MCQ 491 Mark

Suppose that the supply of cameras increases due to an increase in imports. Which of the following statements will most likely occur?

- A

The equilibrium price of cameras will increase.

- B

The equilibrium quantity of cameras exchanged will decrease.

- C

The equilibrium price of camera film will decrease.

- ✓

The equilibrium quantity of camera film exchanged will increase.

AnswerCorrect option: D. The equilibrium quantity of camera film exchanged will increase.

View full question & answer→MCQ 501 Mark

In monopolistic competition, which relationship is true from the following between $AR$ and $MR?$

- A

$AR = MR.$

- B

$AR < MR.$

- ✓

$AR > MR.$

- D

AnswerCorrect option: C. $AR > MR.$

Both $AR$ and $MR$ curves are downward sloping under monopolistic competition because a firm can sell more commodity by lowering the price. The $MR$ curve is half of $AR$ curve, i.e. $AR > MR.$

View full question & answer→MCQ 511 Mark

When both demand and supply decrease in the same proportion, then the equilibrium quantity will:

MCQ 521 Mark

At a price above the equilibrium price, there is:

MCQ 531 Mark

If price is above then equilibrium Price, there is:

MCQ 541 Mark

Demand curve is inelastic under:

- A

- ✓

- C

Monopolistic competition.

- D

View full question & answer→MCQ 551 Mark

Equilibrium price may be determined through $.........$

View full question & answer→MCQ 561 Mark

Demand curve is perfectly elastic under:

- ✓

- B

- C

Monopolistic competition.

- D

View full question & answer→MCQ 571 Mark

Equilibrium price and output changes when:

- A

- B

- ✓

Both demand and supply changes.

- D

AnswerCorrect option: C. Both demand and supply changes.

View full question & answer→MCQ 581 Mark

When both demand and supply increase in the same proportion then equilibrium quantity will:

MCQ 591 Mark

An increase in supply with demand remaining the same bring about $.........$

- ✓

an increase in equilibrium quantity and decrease in equilibrium price.

- B

an increase in equilibrium price and decrease in equilibrium quantity.

- C

decrease in both equilibrium price and quantity.

- D

AnswerCorrect option: A. an increase in equilibrium quantity and decrease in equilibrium price.

View full question & answer→MCQ 601 Mark

Suppose the technology for producing personal computers improves and, at the same time, individuals discover new uses for personal computers so that there is greater utilisation of personal computers. Which of the following statements/ factors will happen to equilibrium price and equilibrium quantity?

- A

Price will increase; quantity cannot be determined.

- B

Price will decrease; quantity cannot be determined.

- ✓

Quantity will increase; price cannot be determined.

- D

Quantity will decrease; price cannot be determined.

AnswerCorrect option: C. Quantity will increase; price cannot be determined.

View full question & answer→MCQ 611 Mark

If there is shortage of certain goods, the government introduces $.........$ for distribution of commodity to consumers.

View full question & answer→MCQ 621 Mark

‘Homogenous products’ is a characteristic of:

- A

Perfect competition only.

- B

- ✓

Both $(a)$ and $(b).$

- D

AnswerCorrect option: C. Both $(a)$ and $(b).$

View full question & answer→MCQ 631 Mark

Demand curve is elastic under:

- A

- B

- ✓

Monopolistic competition.

- D

AnswerCorrect option: C. Monopolistic competition.

View full question & answer→MCQ 641 Mark

When increase in demand is more than increase in supply, then equilibrium price will:

MCQ 651 Mark

The product sold by monopolist has:

MCQ 661 Mark

Entry is restricted under:

- A

- ✓

- C

Monopolistic competition.

- D

View full question & answer→MCQ 671 Mark

There are only a few sellers under:

- A

- B

Monopolistic competition.

- ✓

- D

View full question & answer→MCQ 681 Mark

In perfect competition, as the firm is a price taker, the $.........$ curve is a horizontal straight line.

View full question & answer→MCQ 691 Mark

If in an industry, demand and supply will not intersect in positive quadrant, then it is called:

AnswerA non$-$viable industry is one which will not produce the product in an economy. It may be because cost of product is too high and consumers are not willing to pay the price.

View full question & answer→