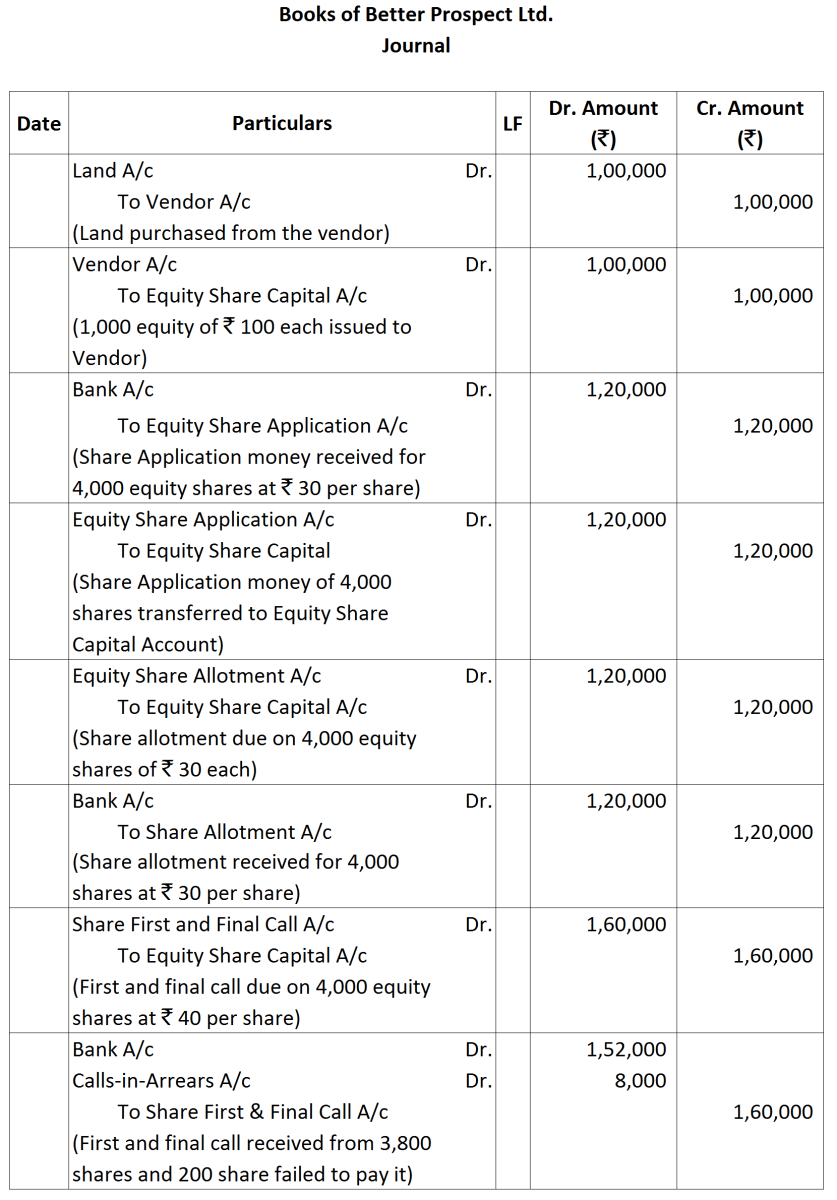

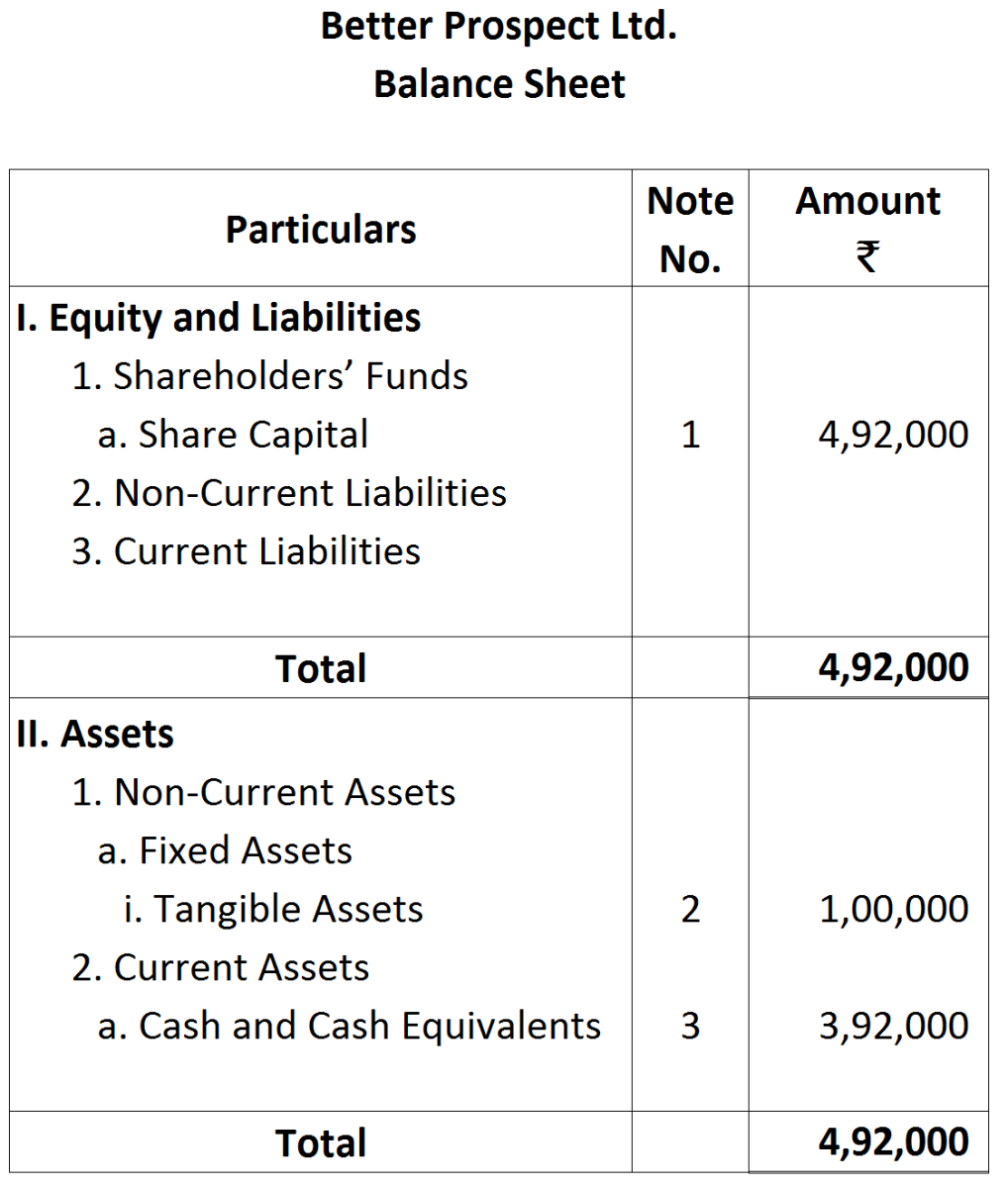

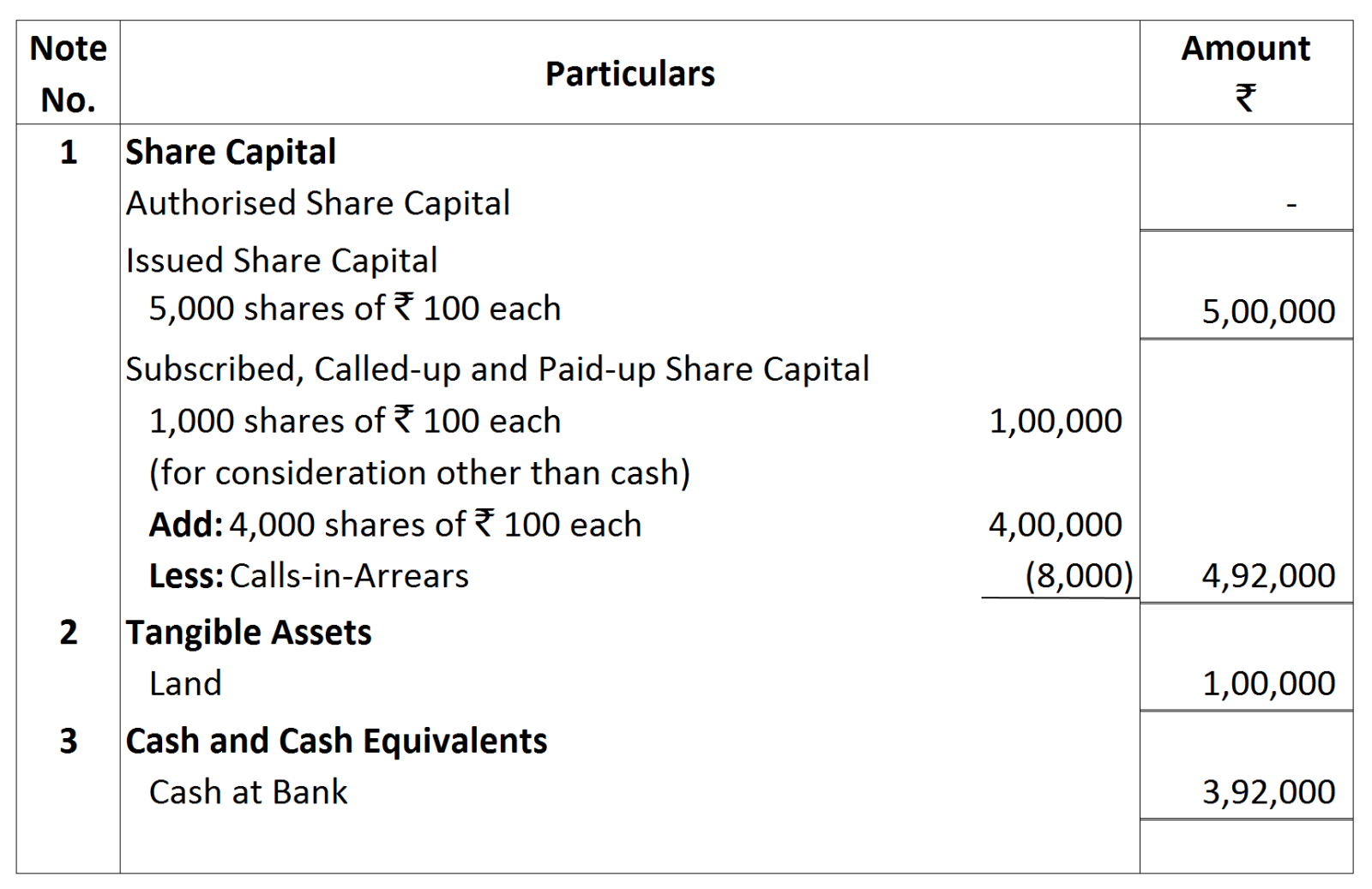

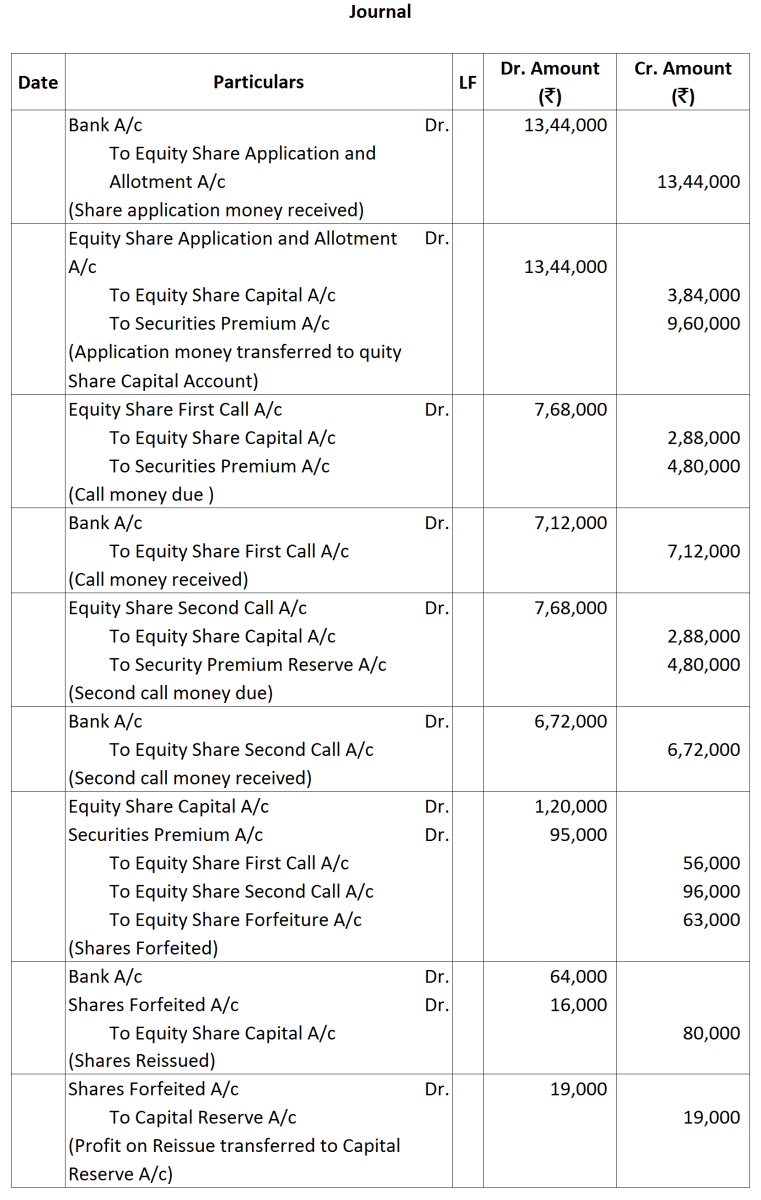

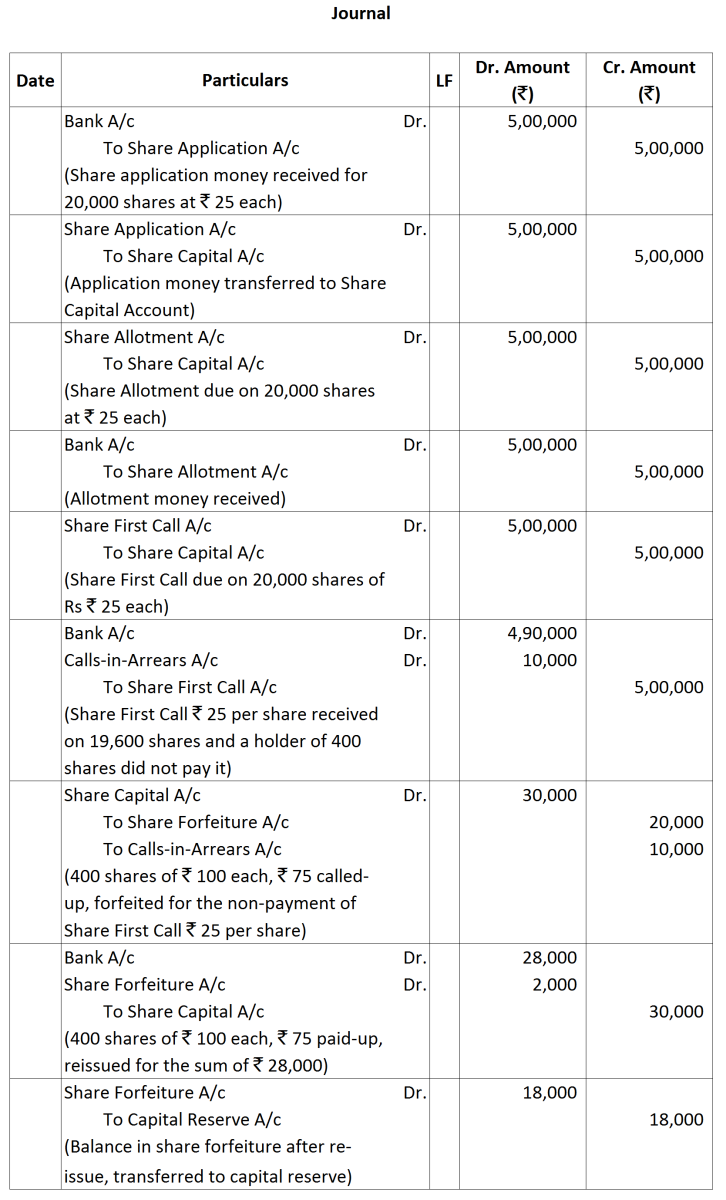

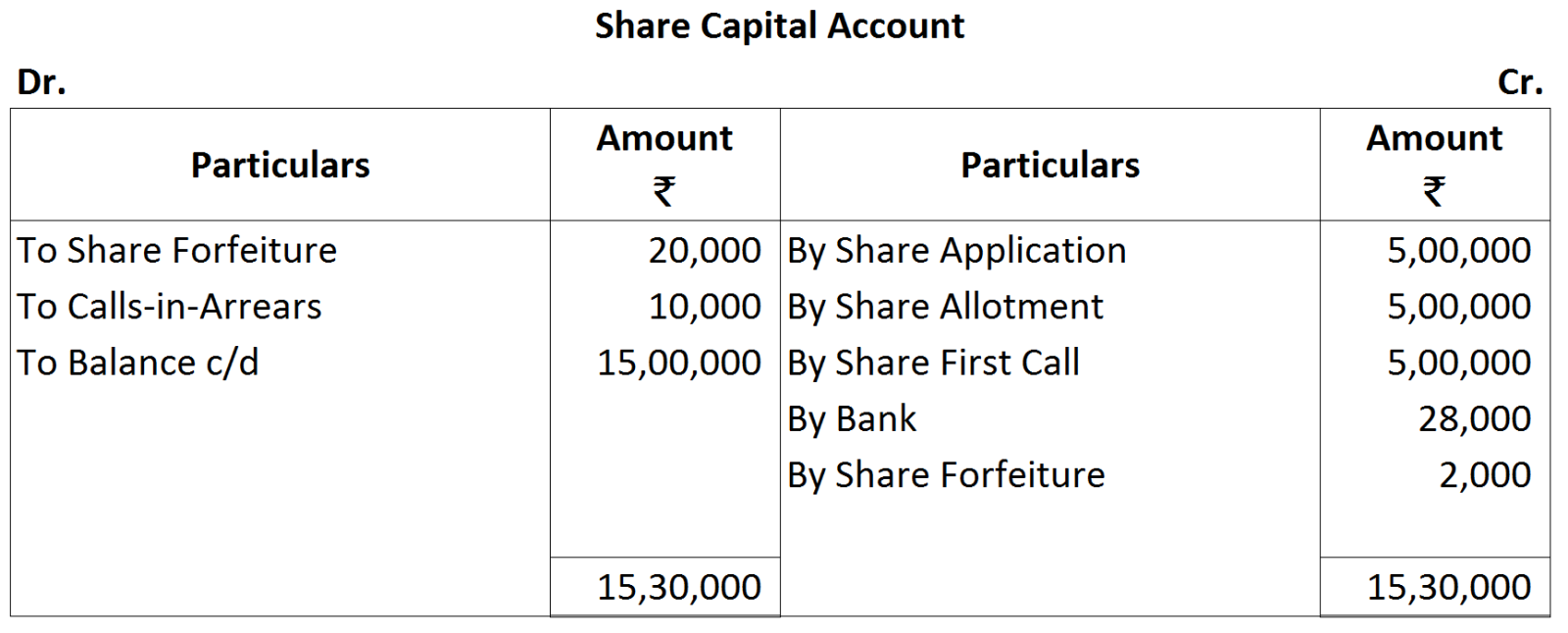

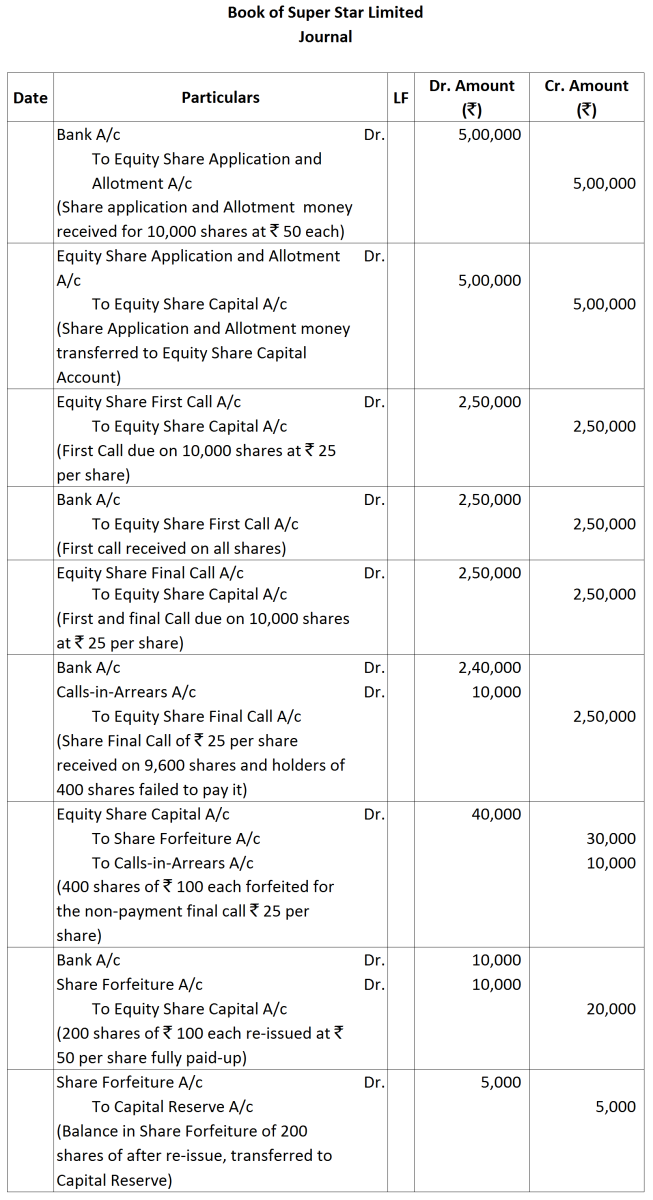

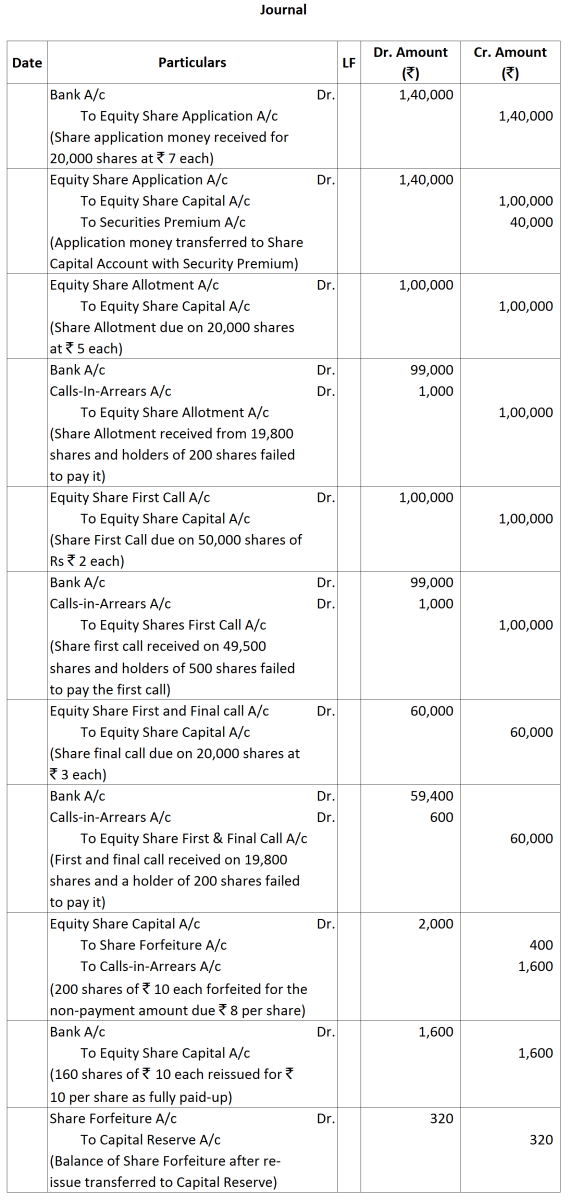

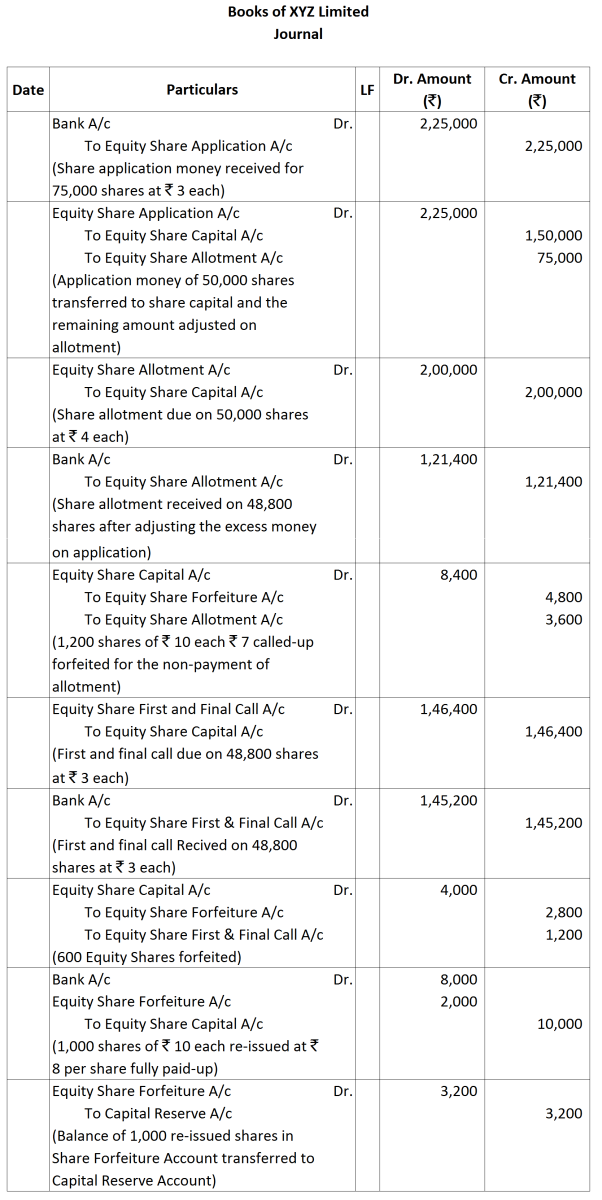

Question 16 Marks

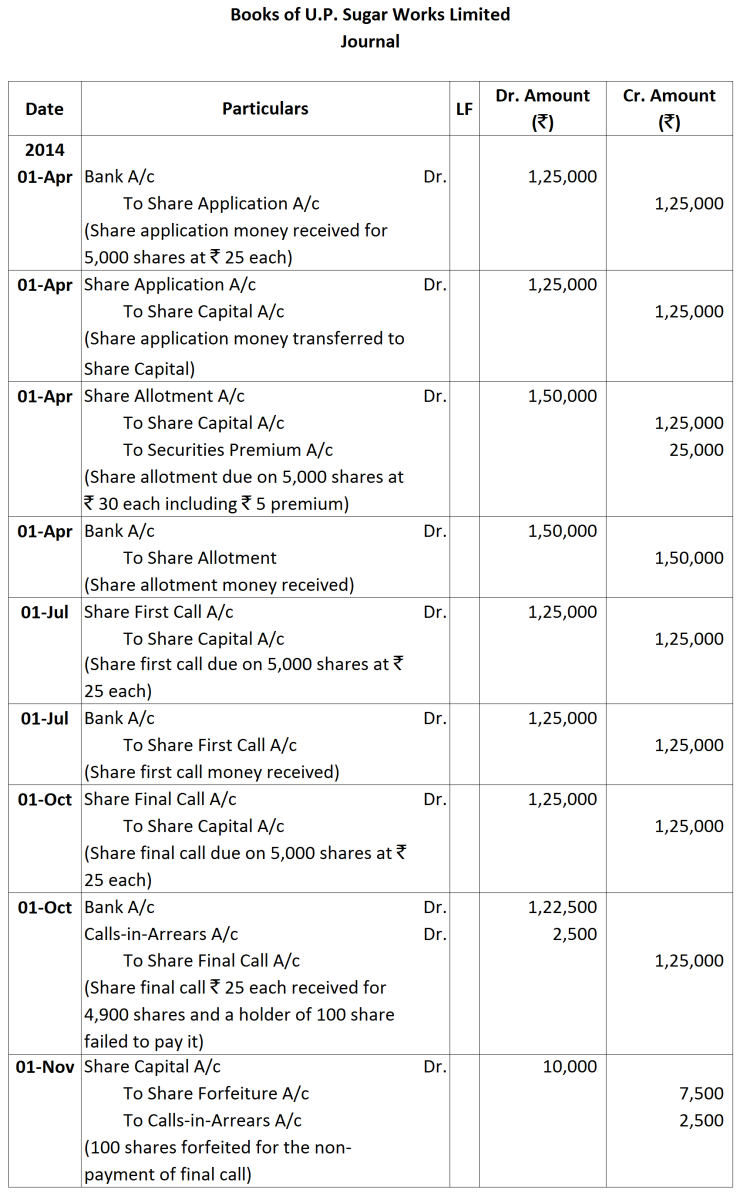

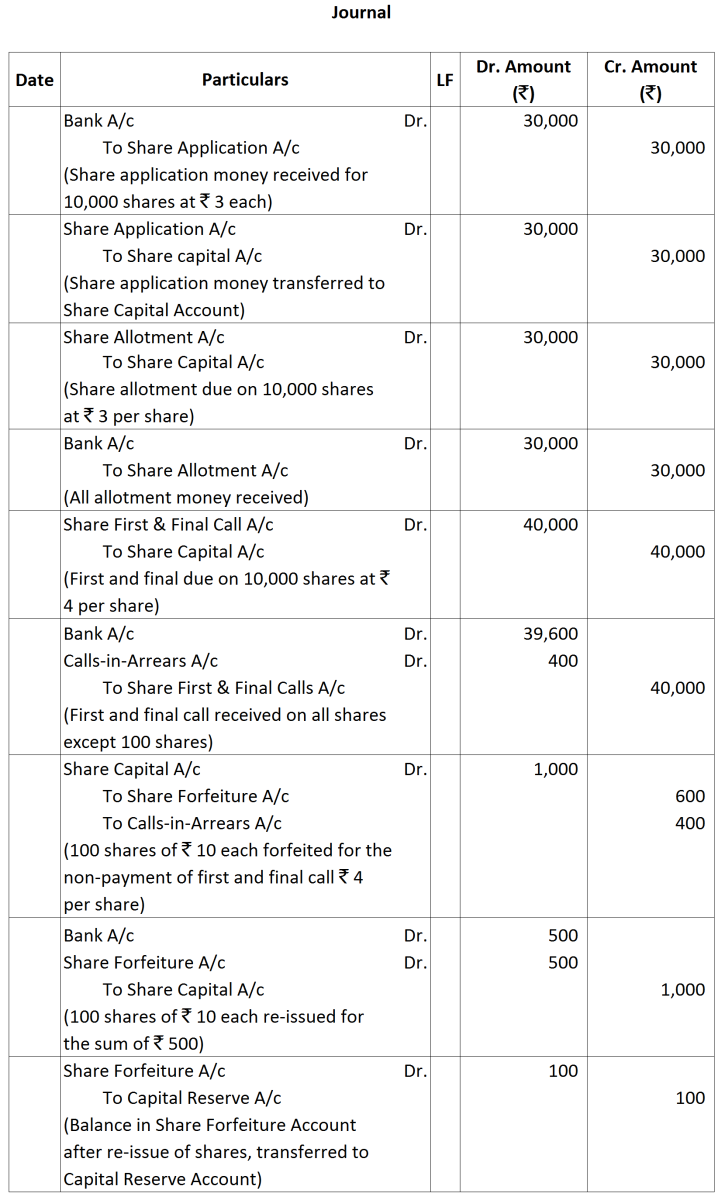

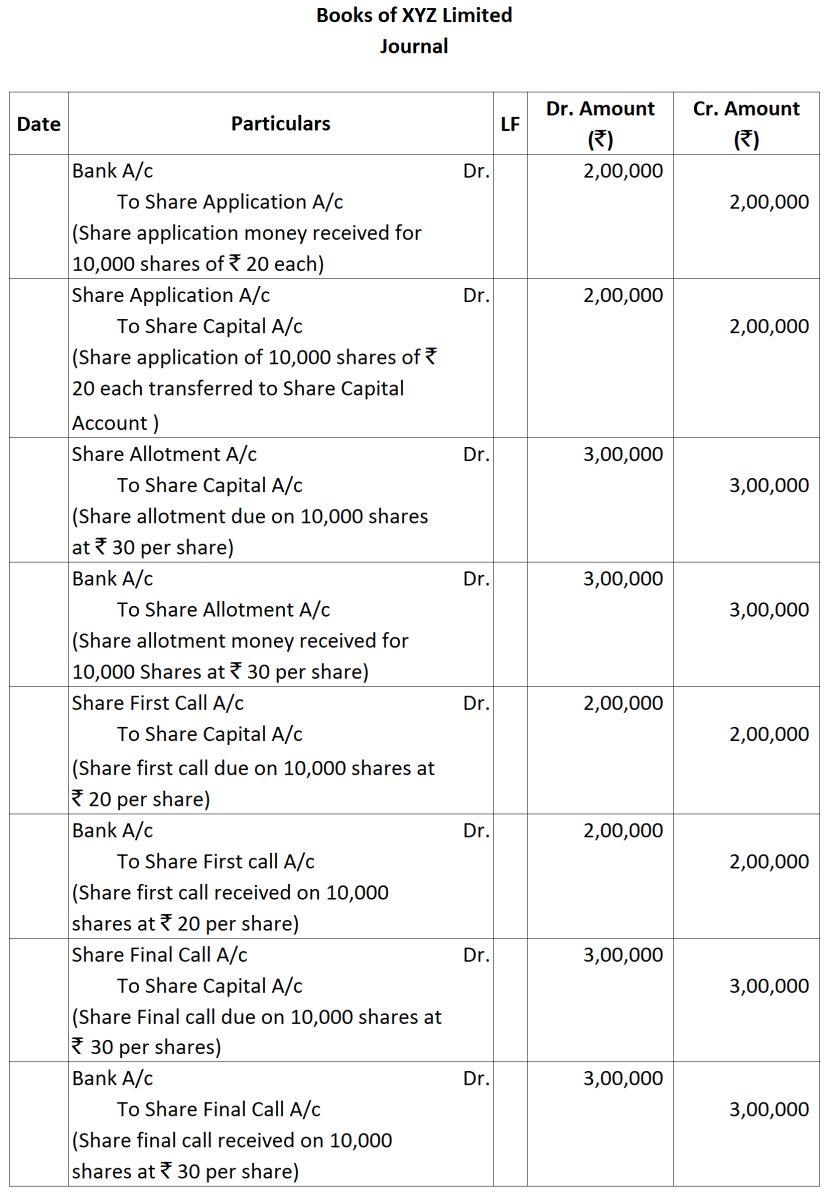

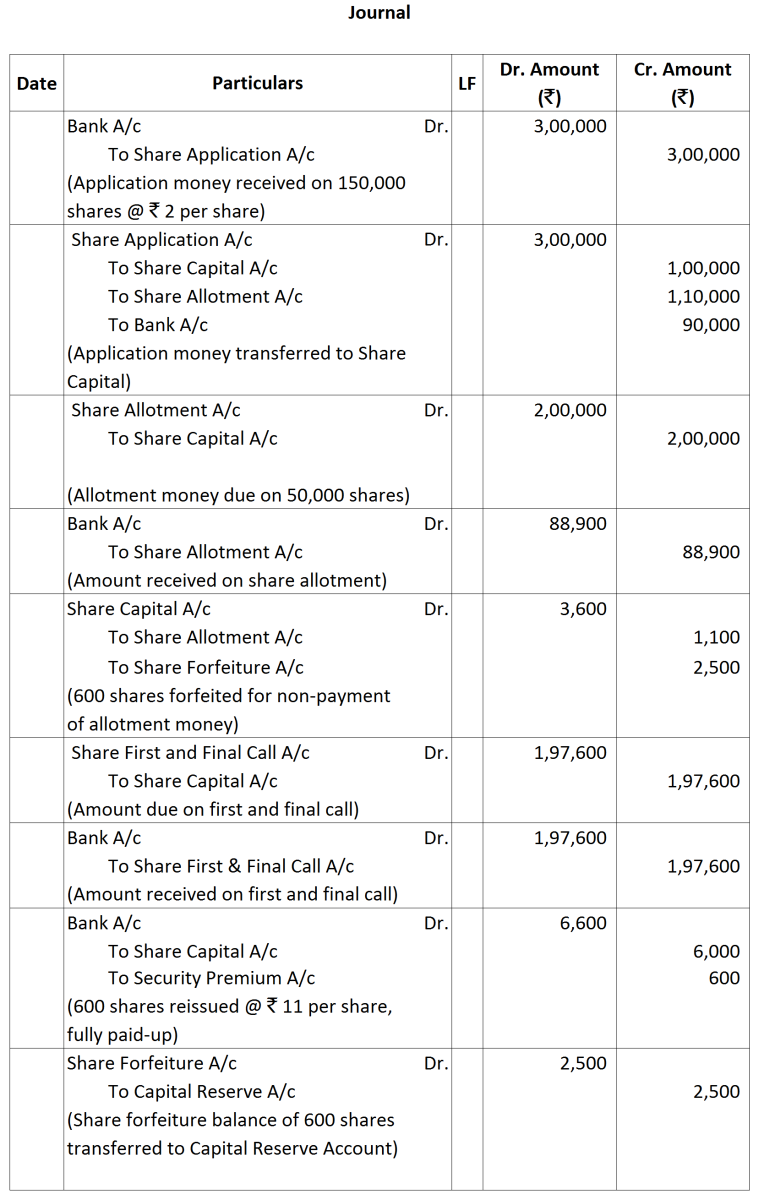

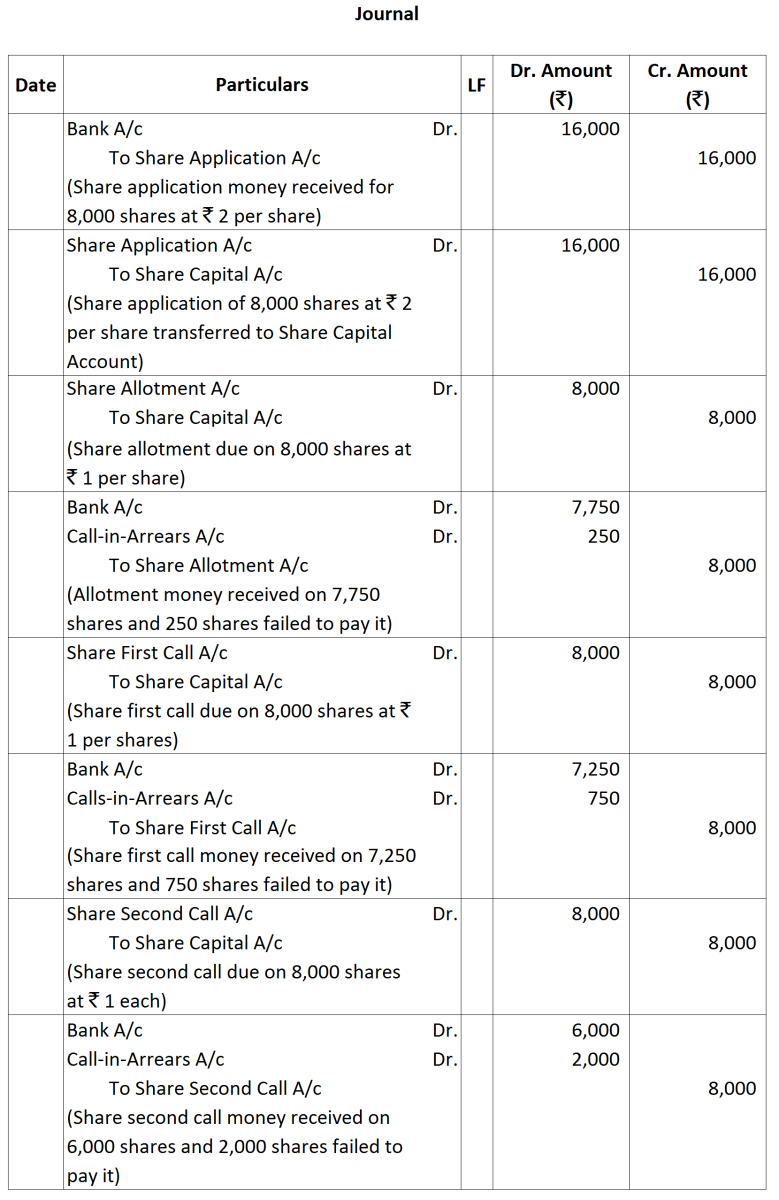

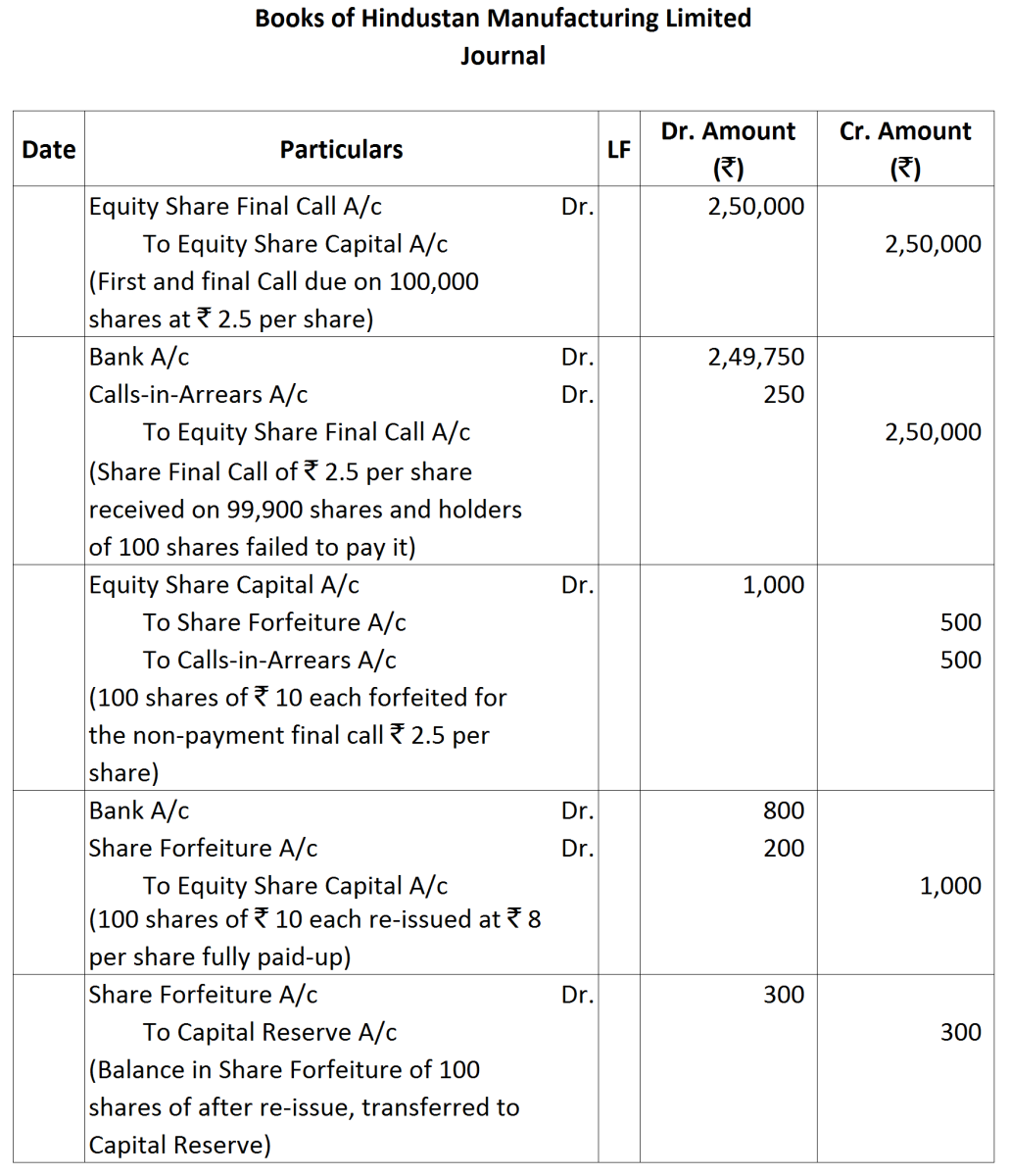

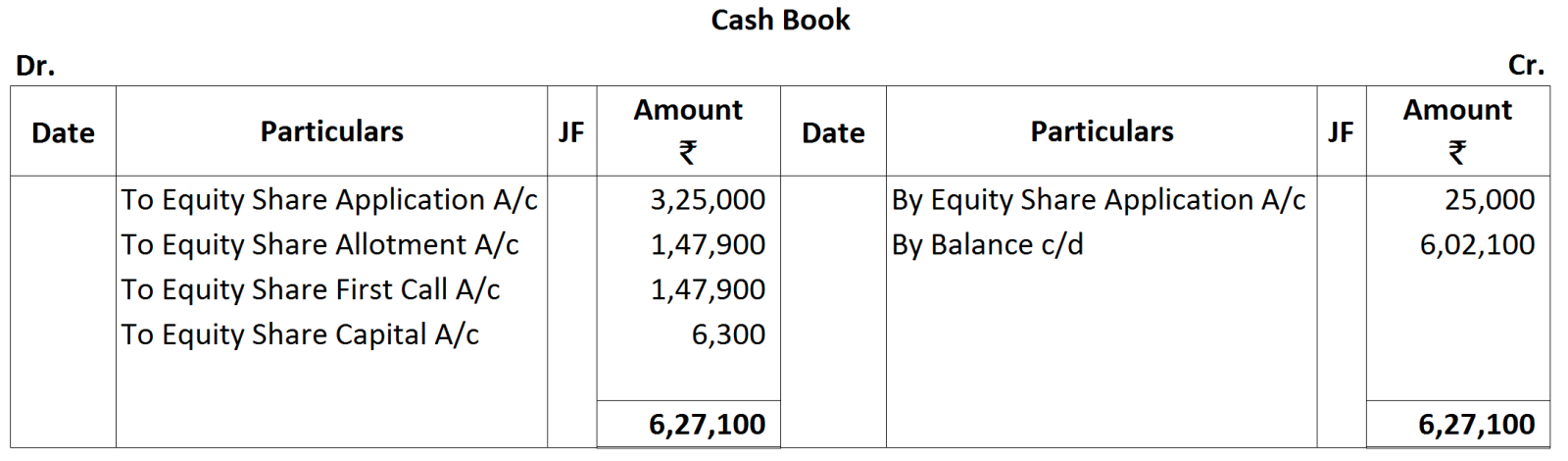

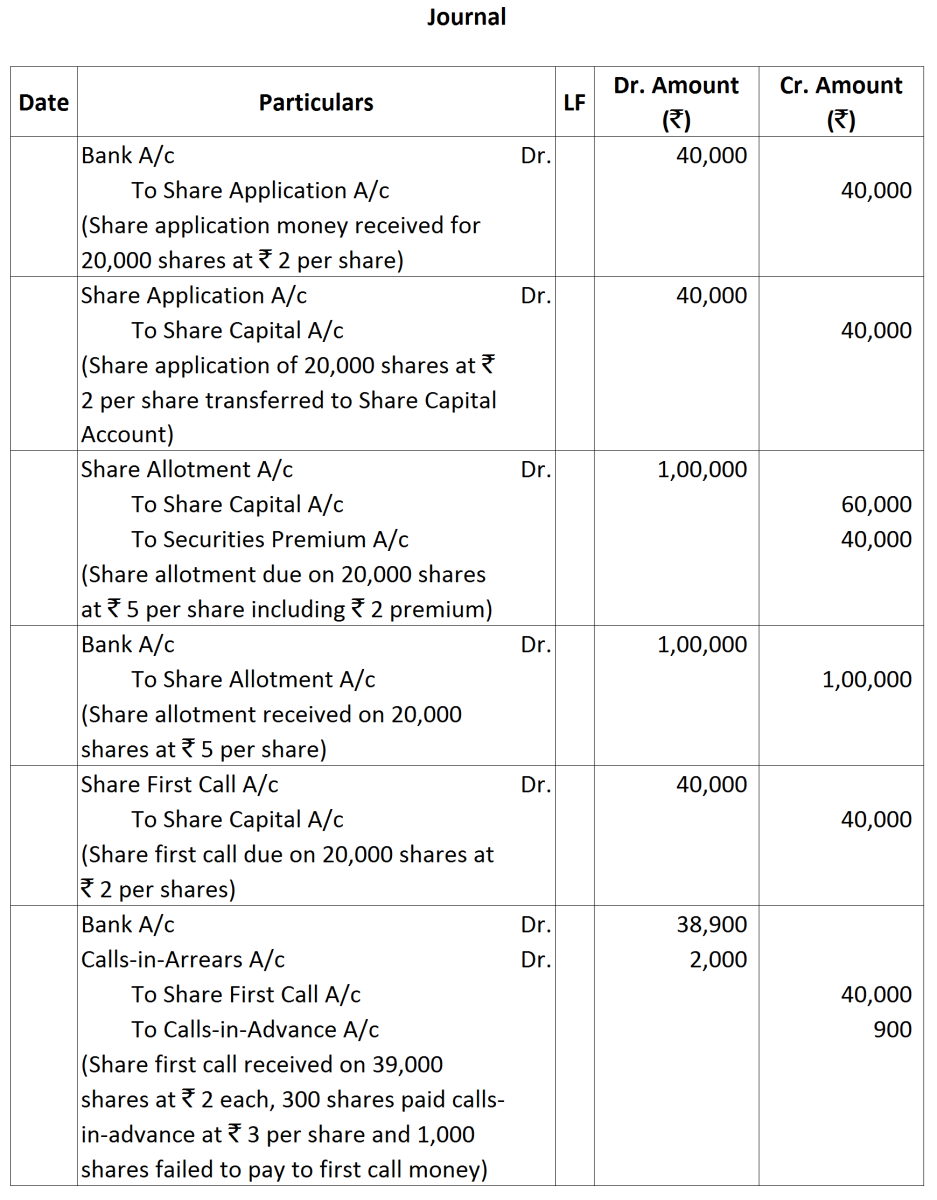

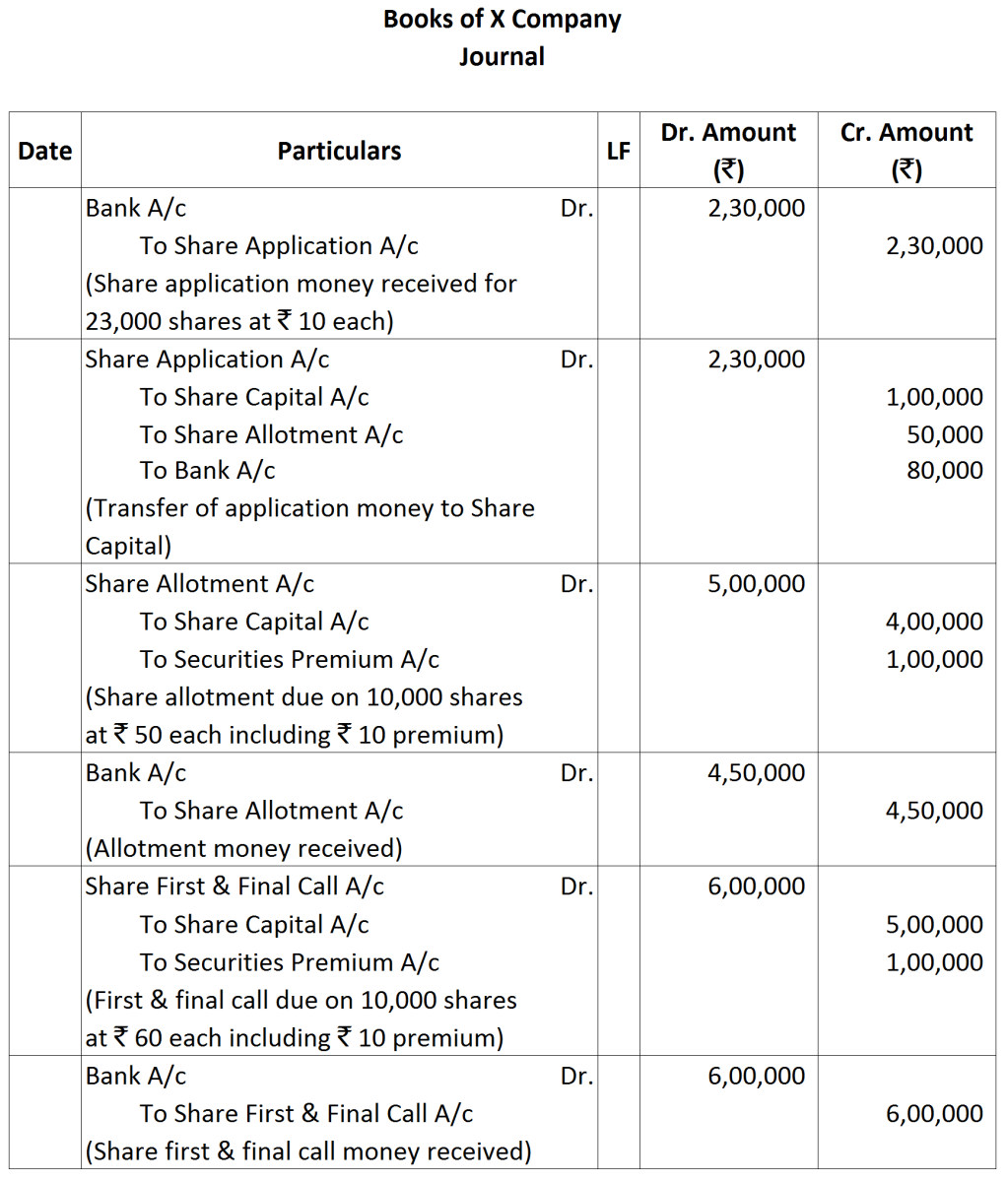

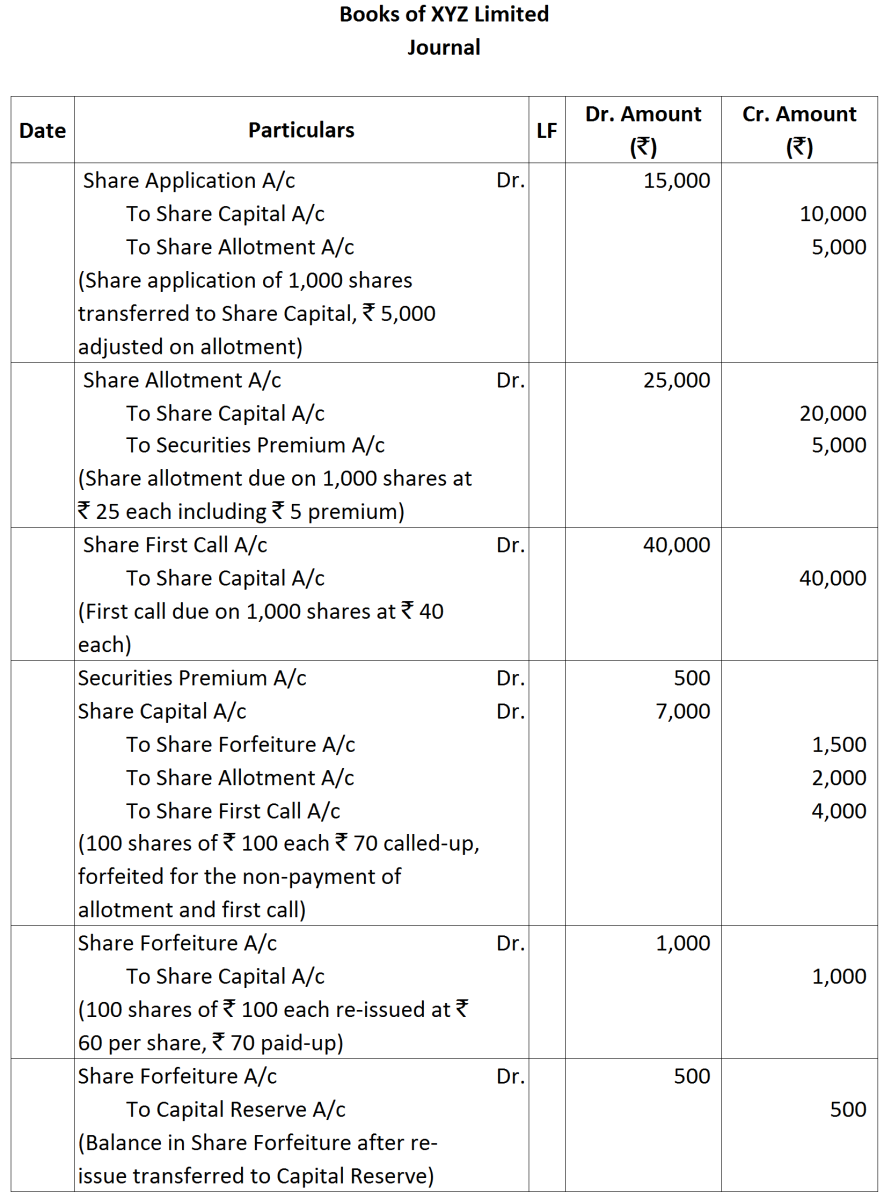

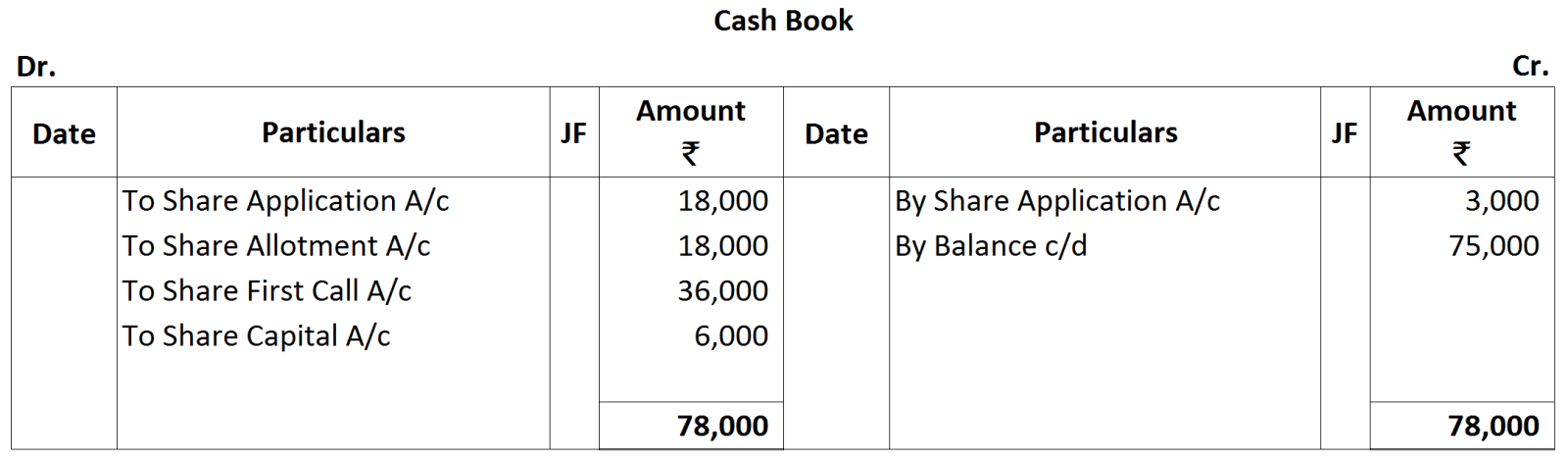

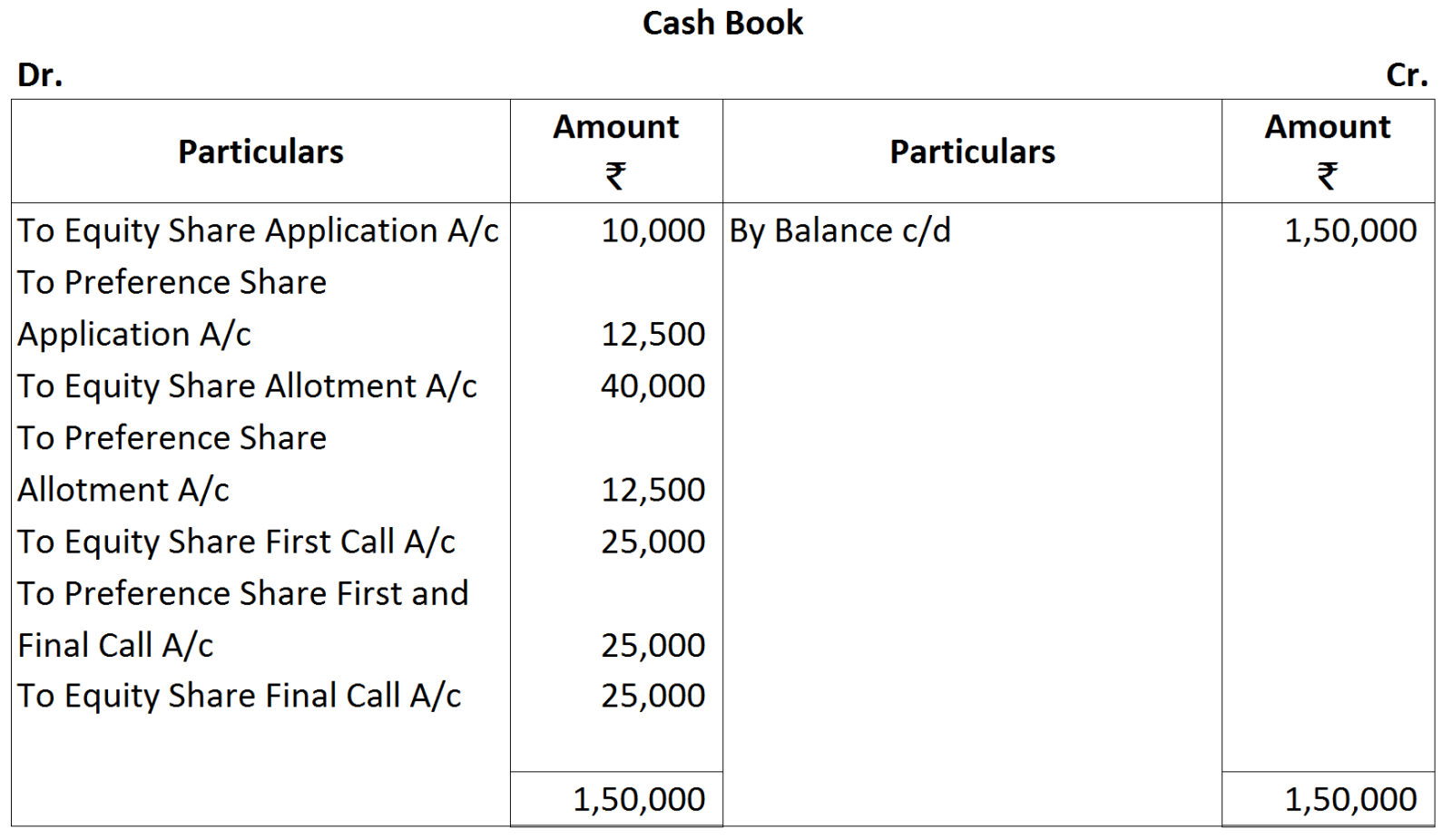

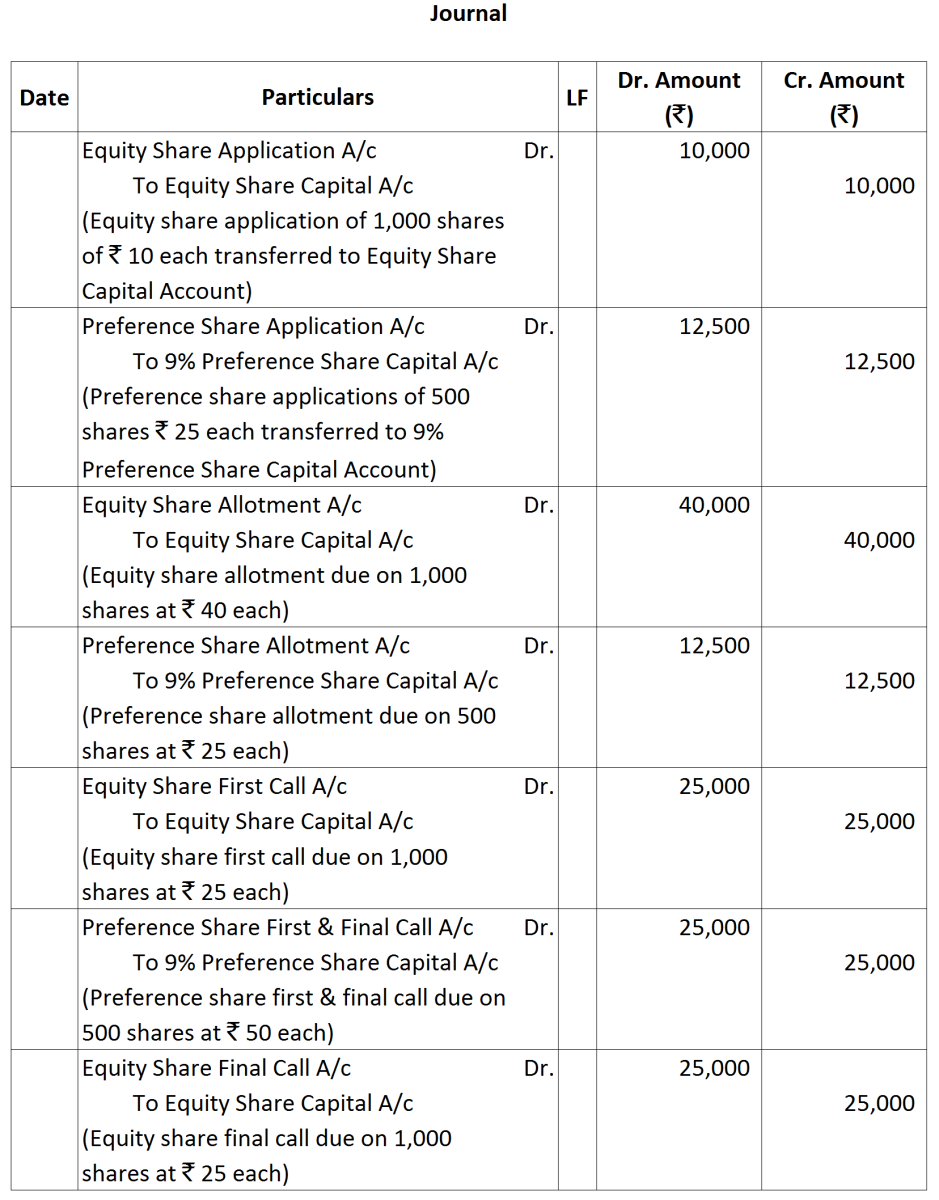

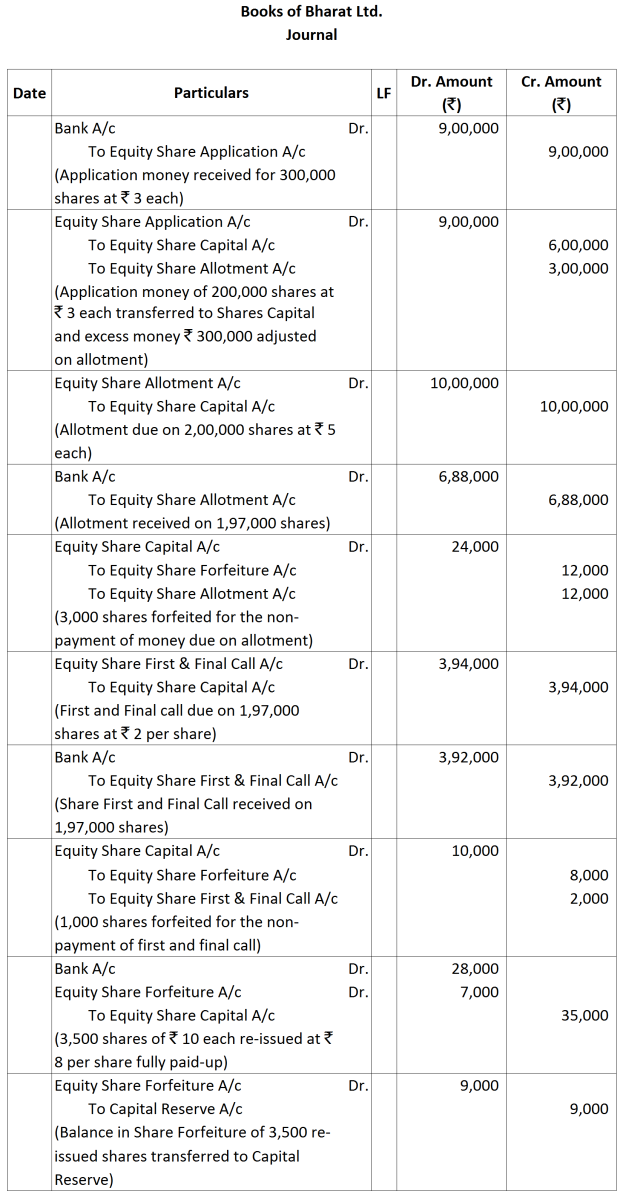

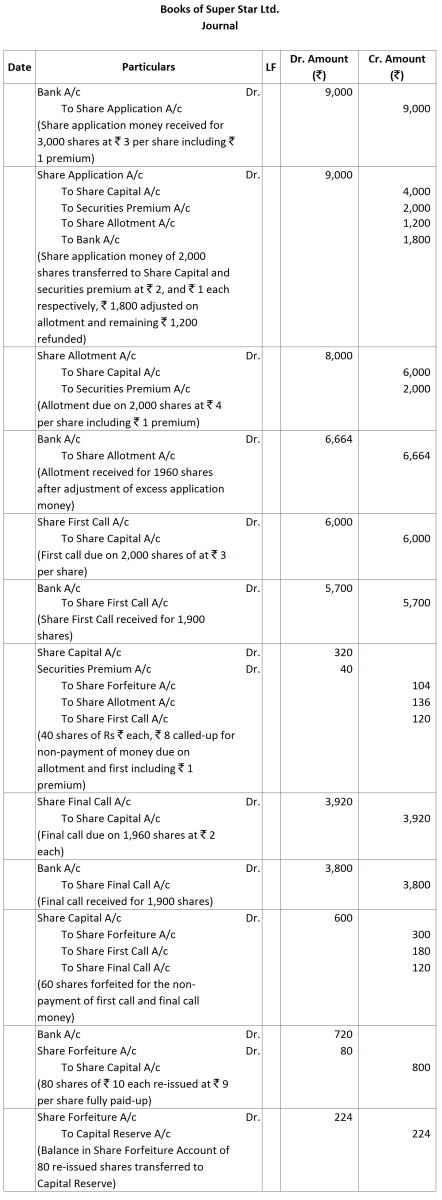

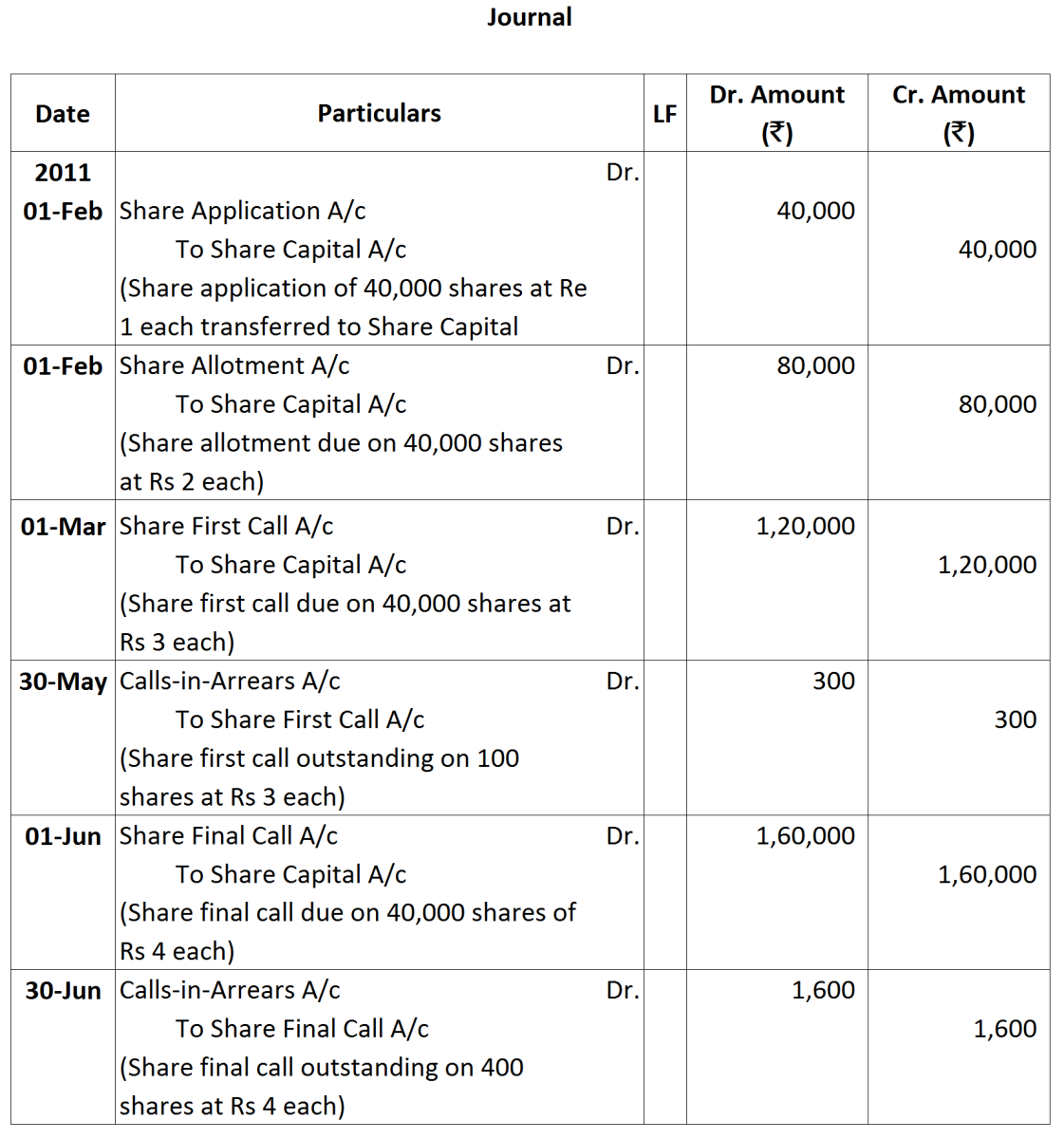

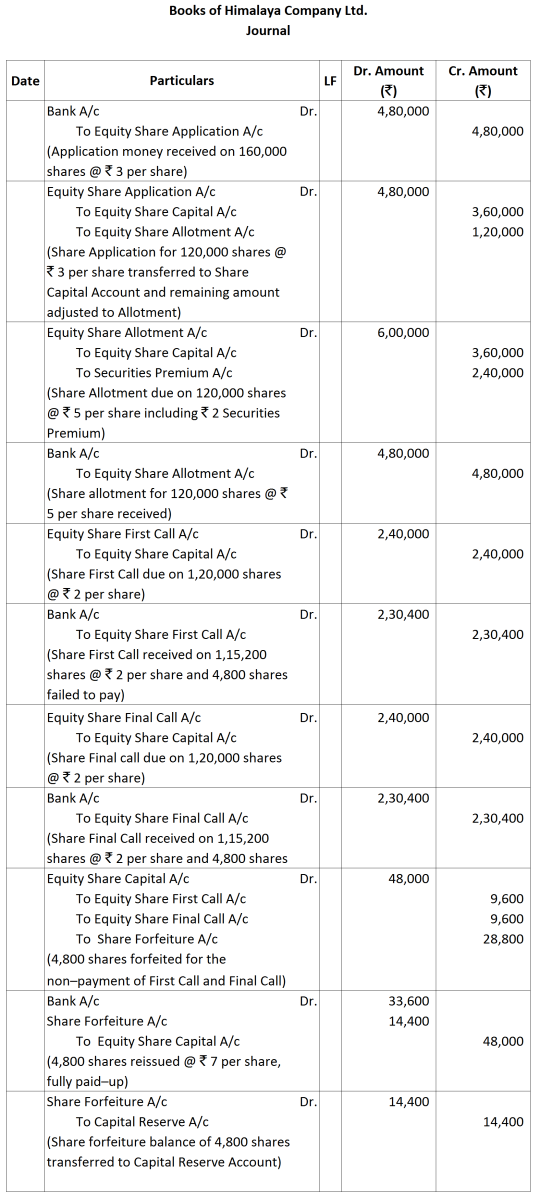

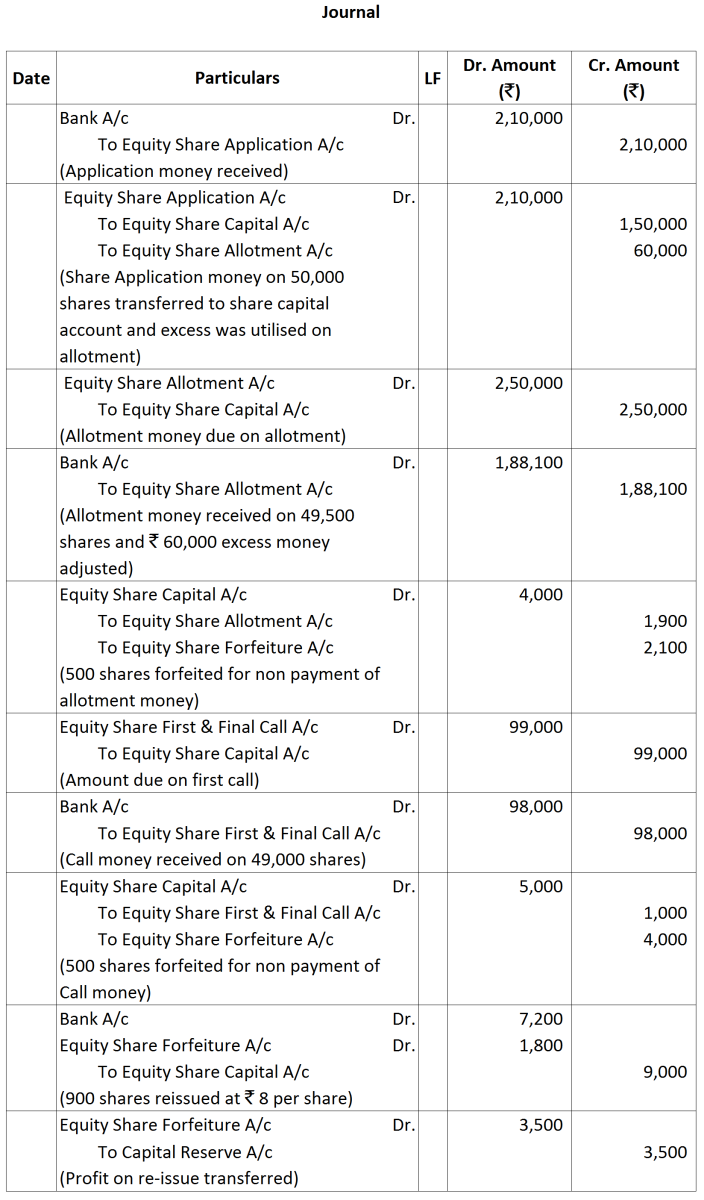

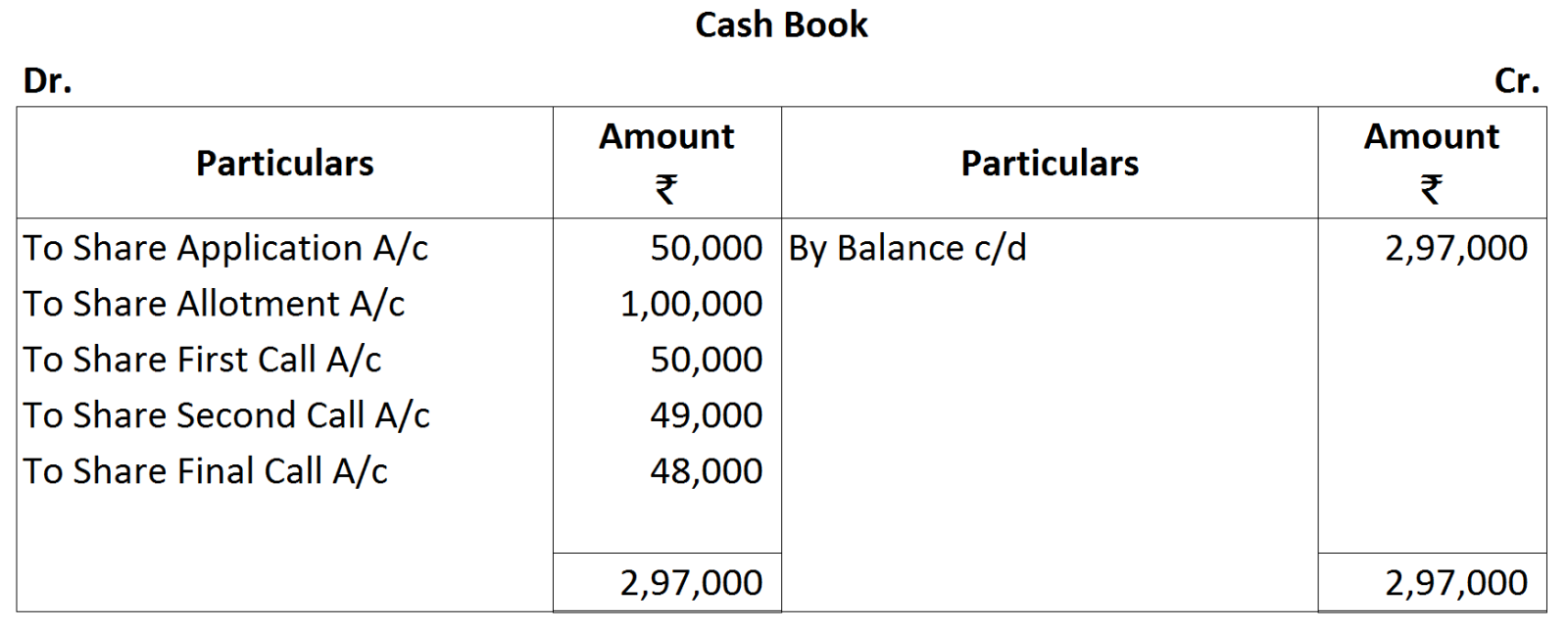

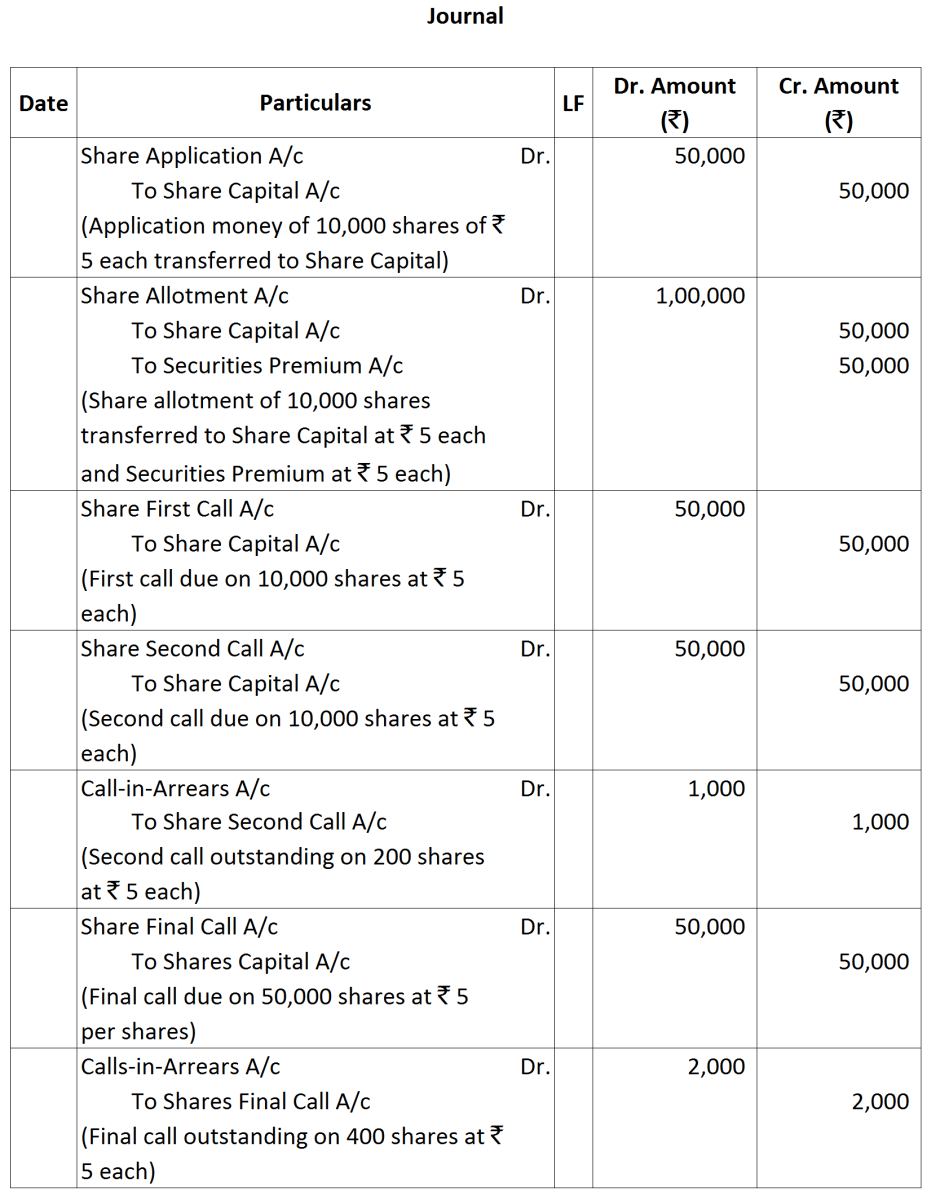

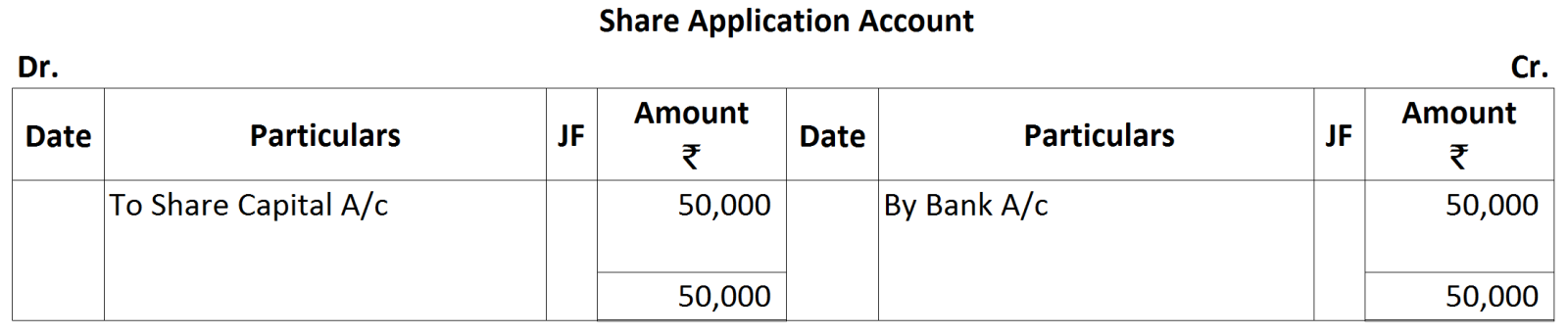

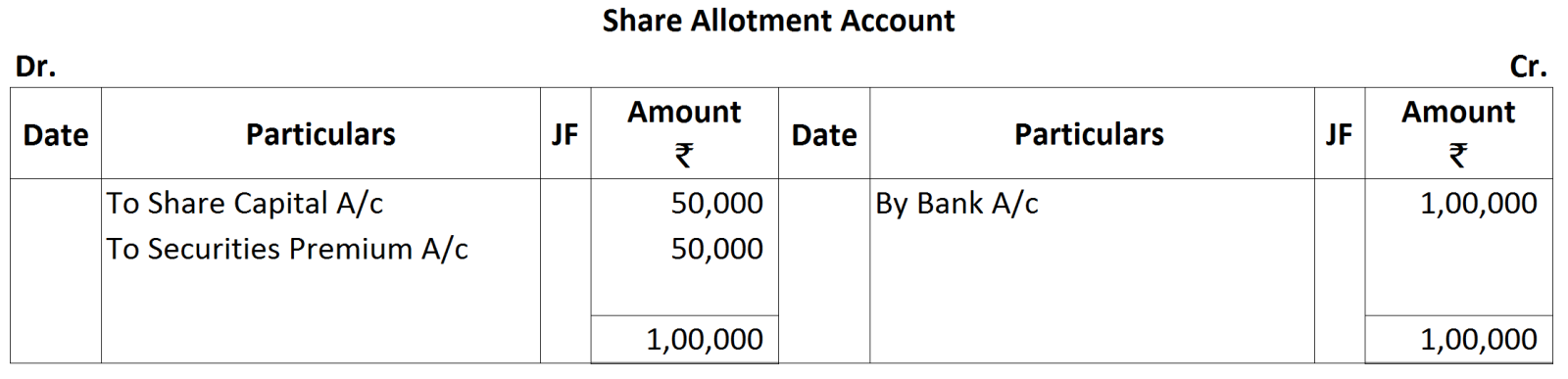

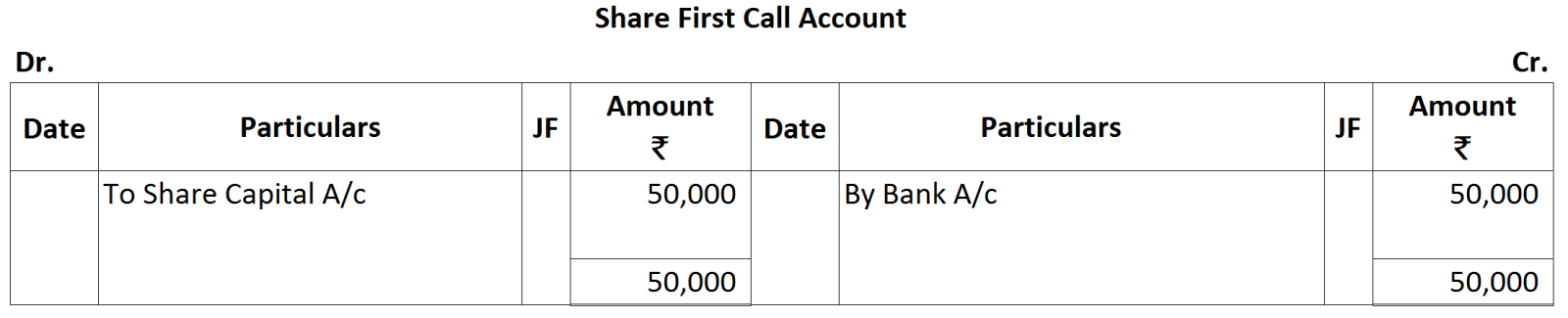

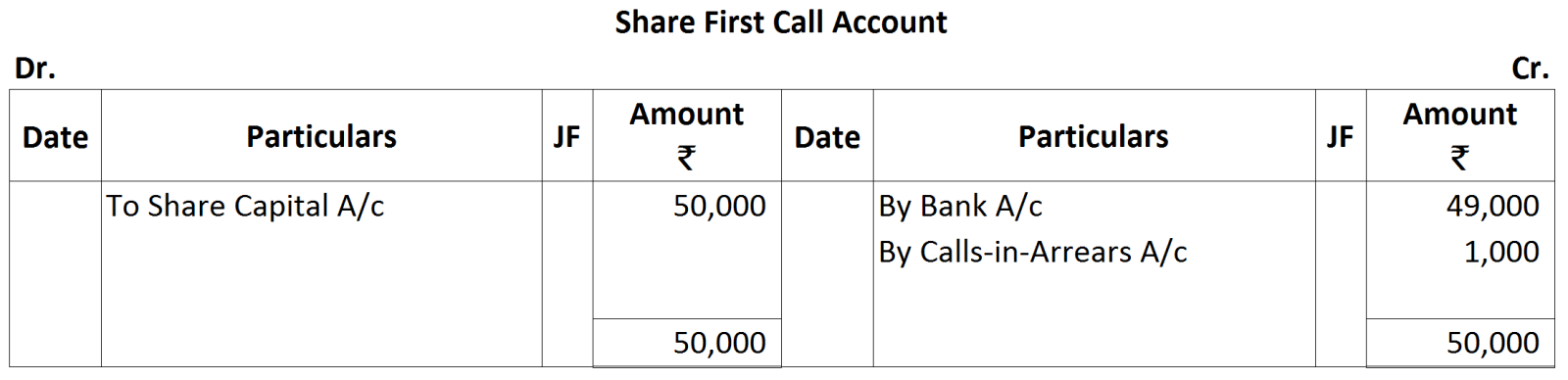

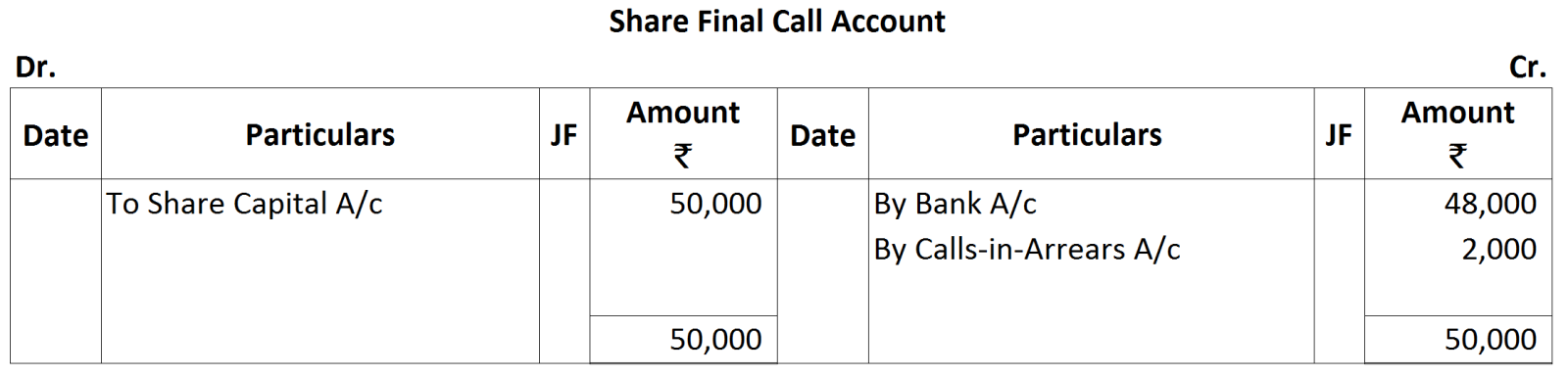

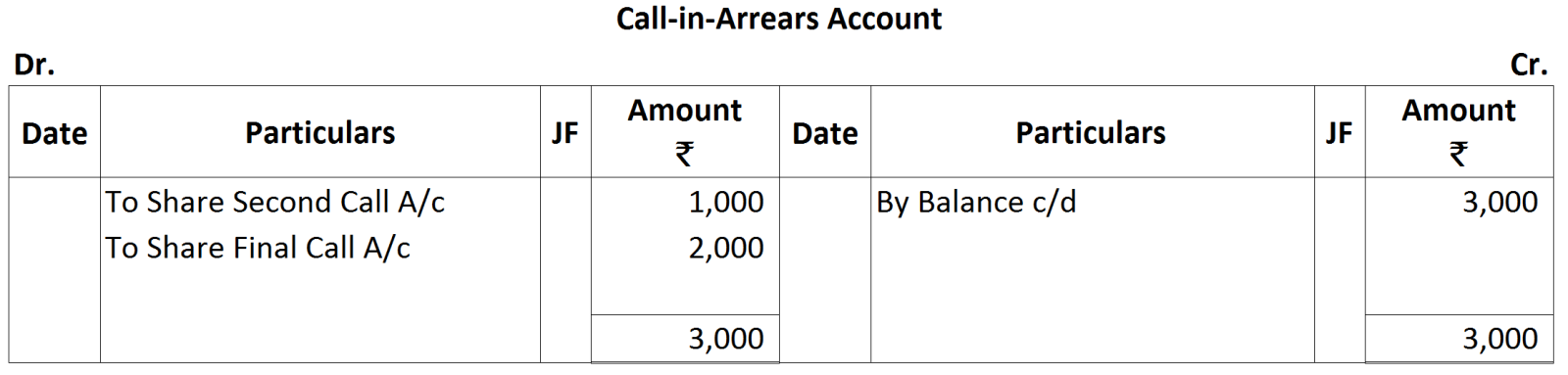

U.P. Sugar Works Ltd. was registered on 1st January, 2014 with an authorised capital of ₹ 15,00,000 divided into 15,000 shares of ₹ 100 each. The company issued on 1st April, 2014, 5,000 shares of ₹ 100 each at a premium of ₹ 5 per share payable ₹ 25 per share on application, ₹ 30(including premium) on allotment and the balance in two equal installments of ₹ 25 each on 1st July ad 1st October respectively. All the allotments and call moneys were paid when due, except in case of one shareholder who failed to pay the final call on 100 shares held by him. His shares were forfeited on 1st November after giving him a due notice. Show necessary entries in the books of the company to record these transactions.

Answer

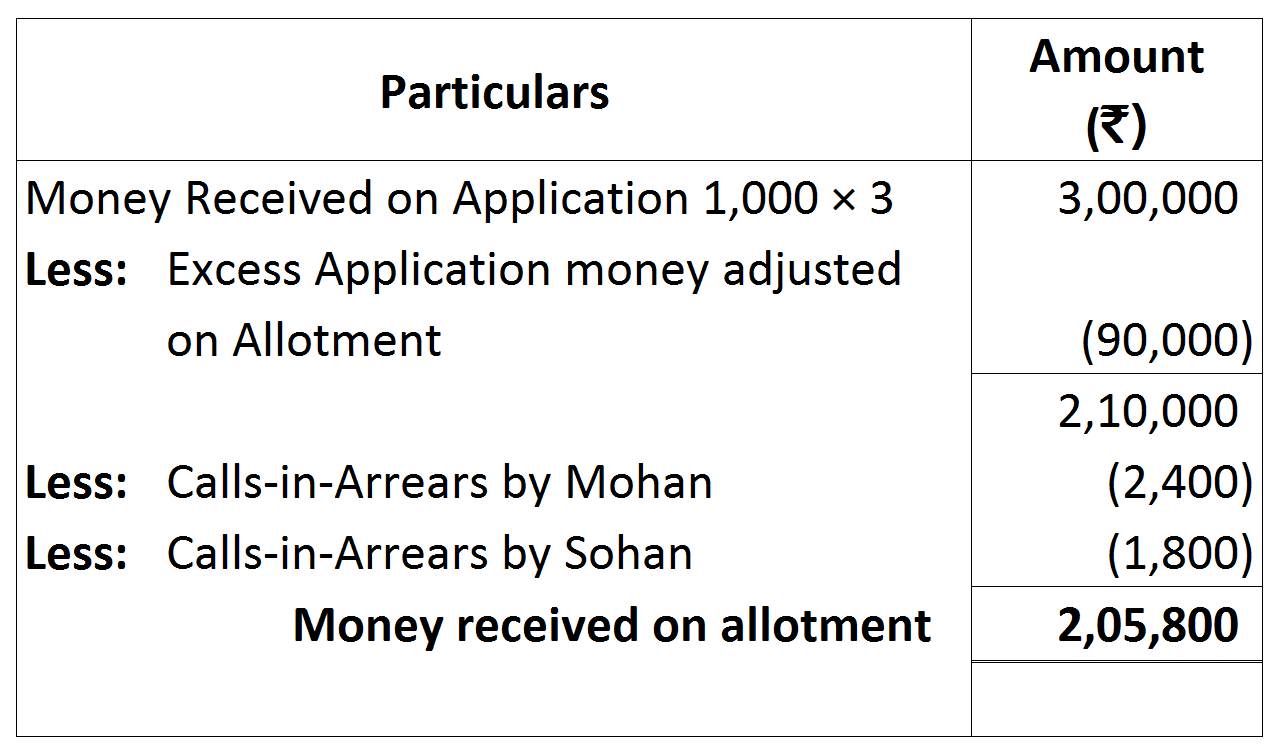

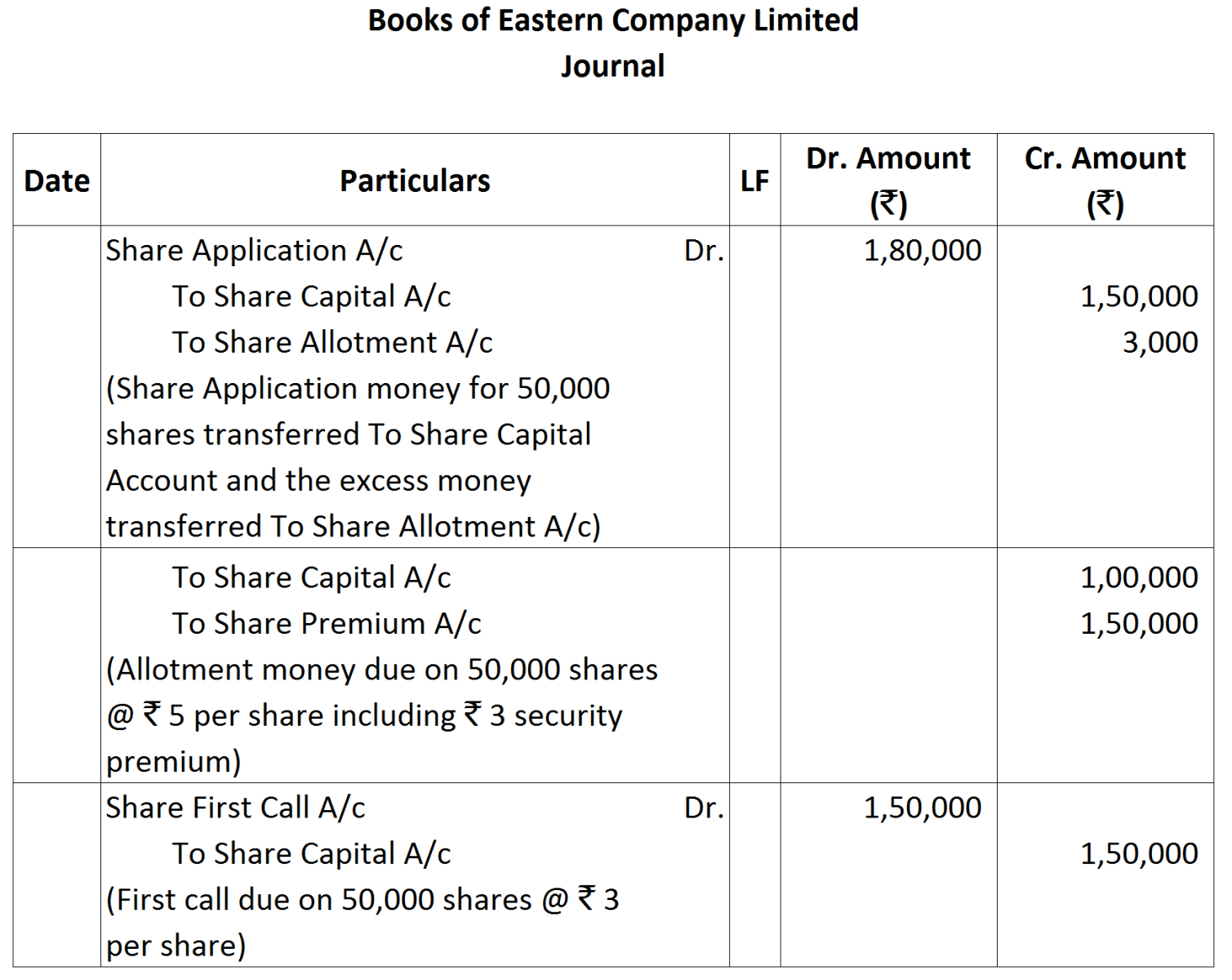

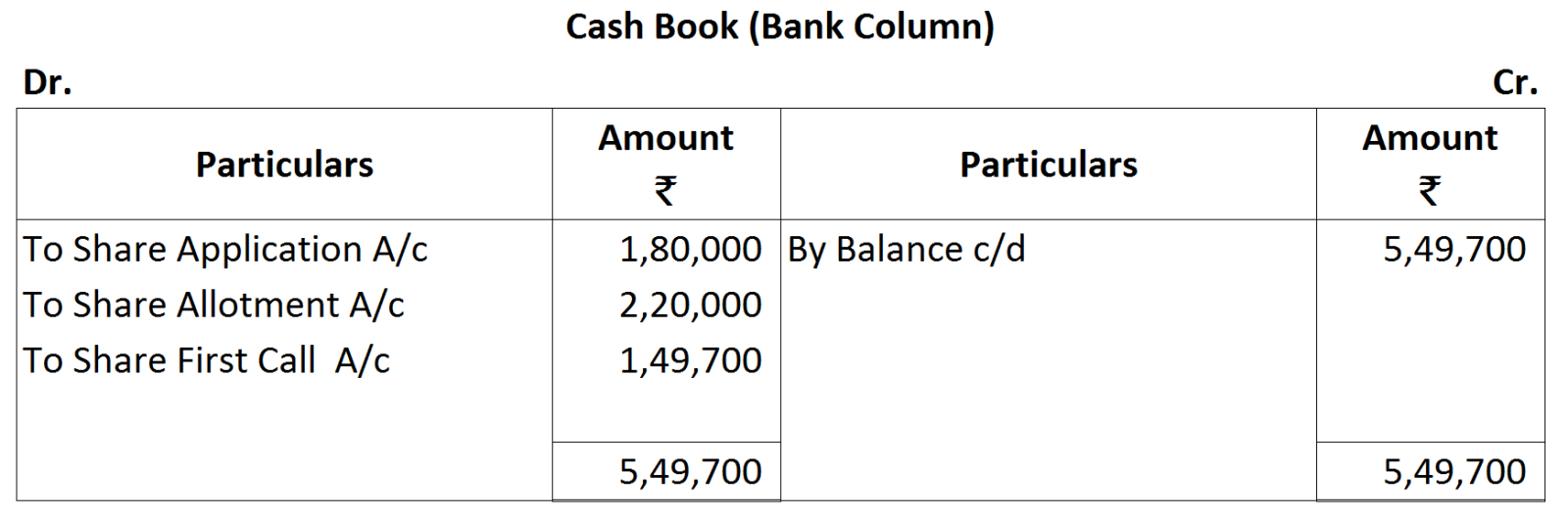

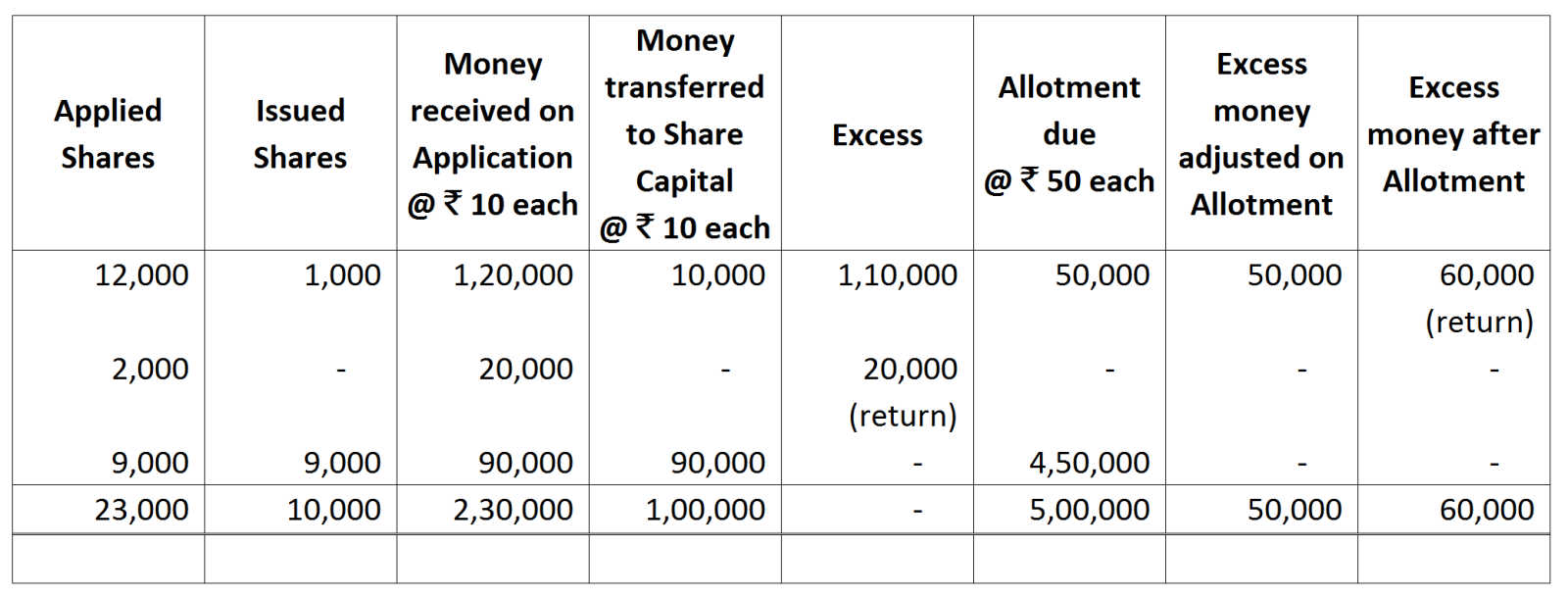

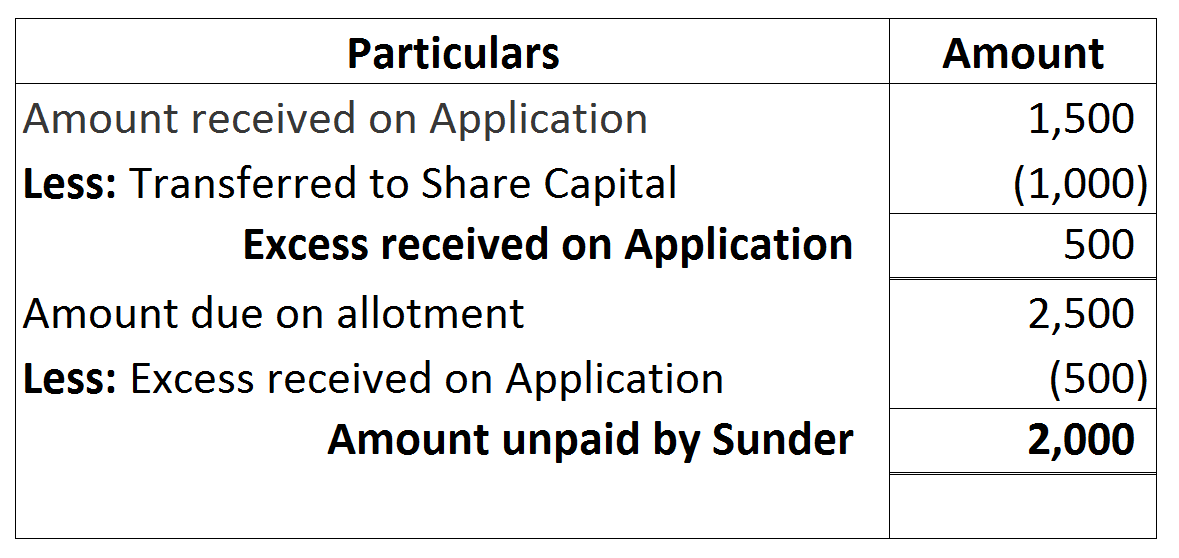

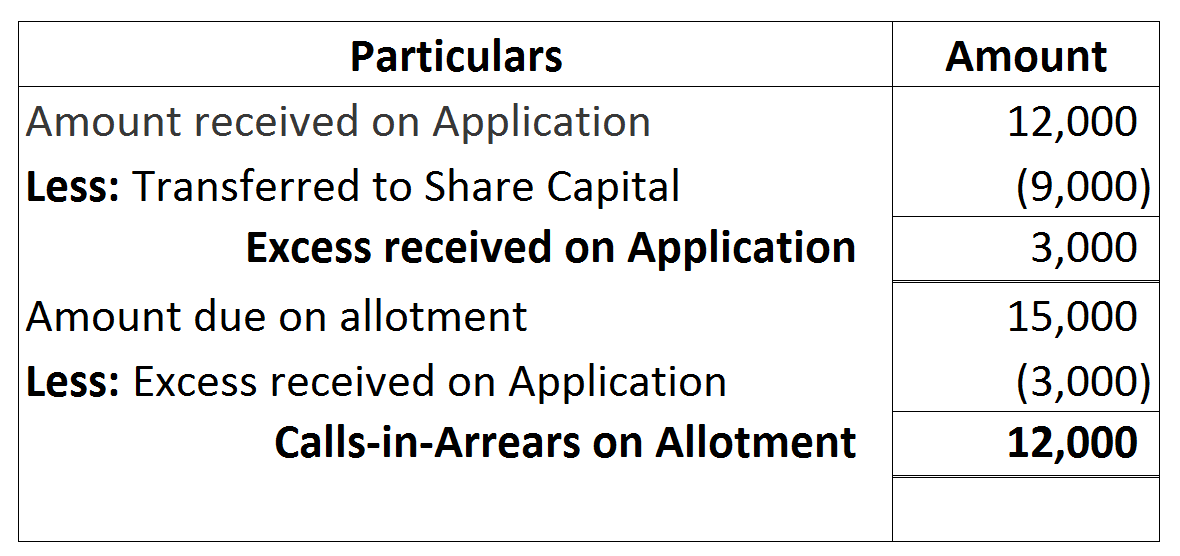

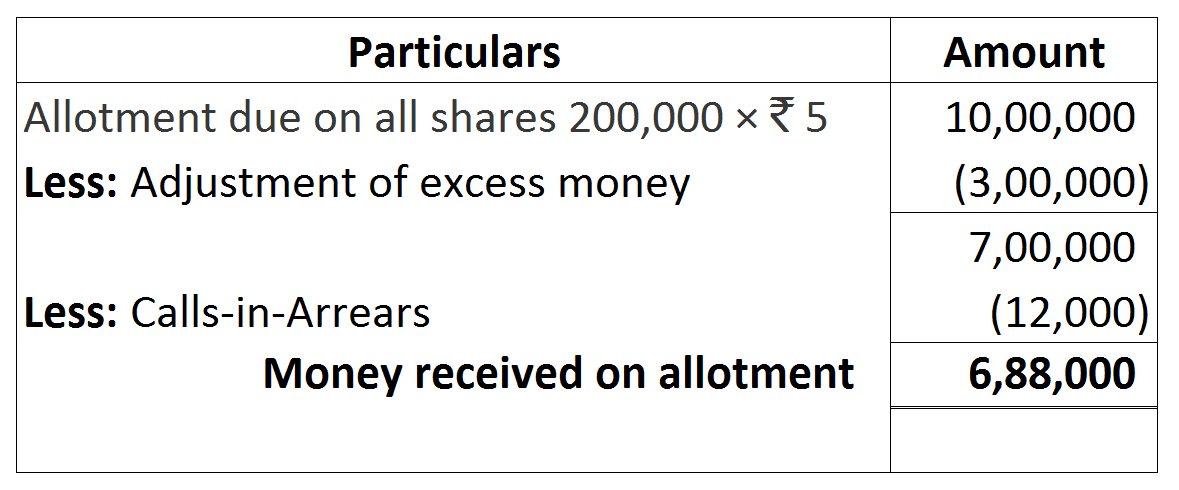

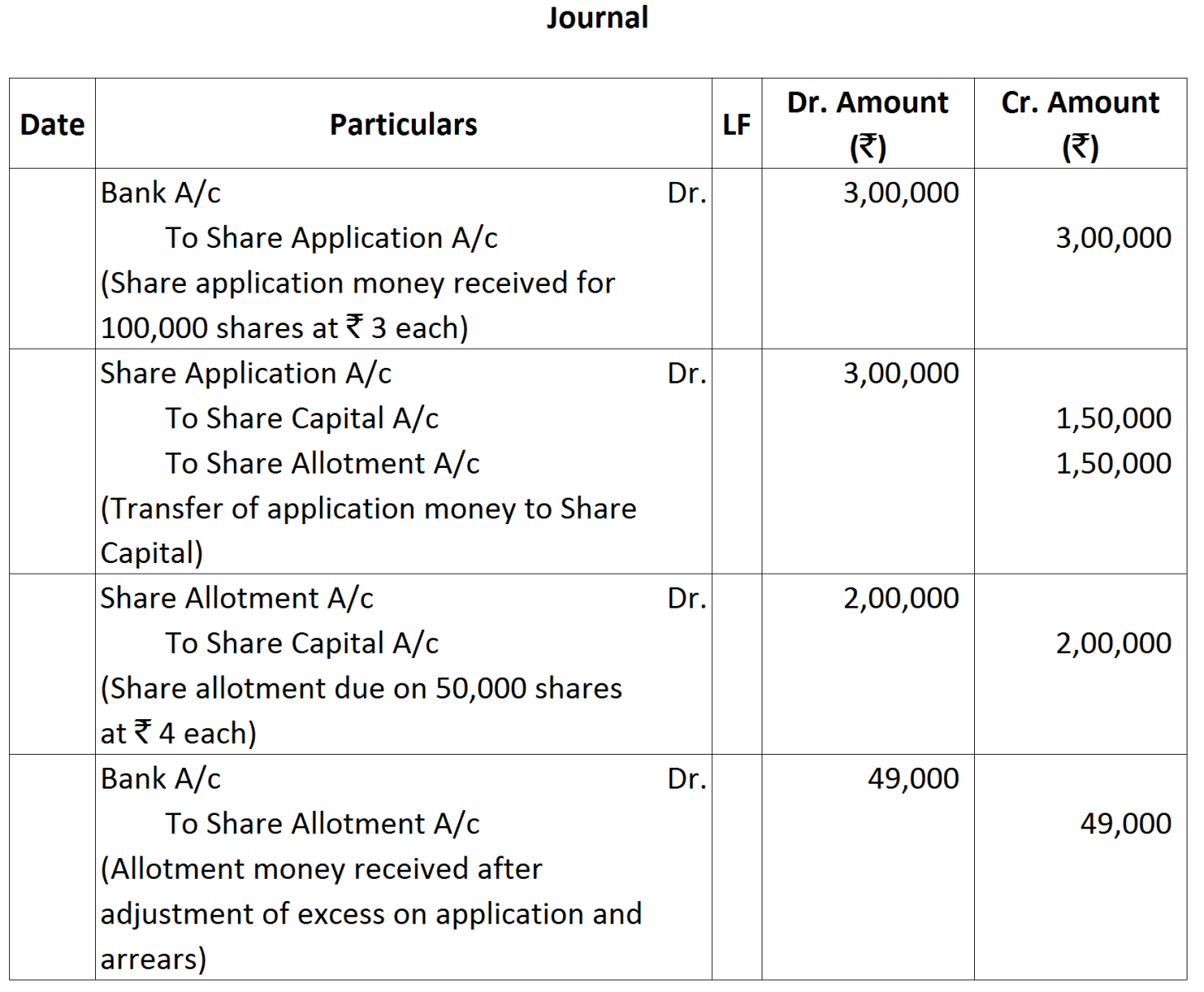

View full question & answer→Authorised capital 15,000 shares of 100 each. Issued and applied capital 5,000 shares of ₹ 100 each at a premium ₹ 5.

|

Application

|

=

|

₹ 25

|

|

|

Allotment

|

=

|

₹ 30

|

(25 + 5)

|

|

First Call

|

=

|

₹ 25

|

|

|

Final Call

|

=

|

₹ 25

|

|

|

|

|

105

|

(100 + 5)

|

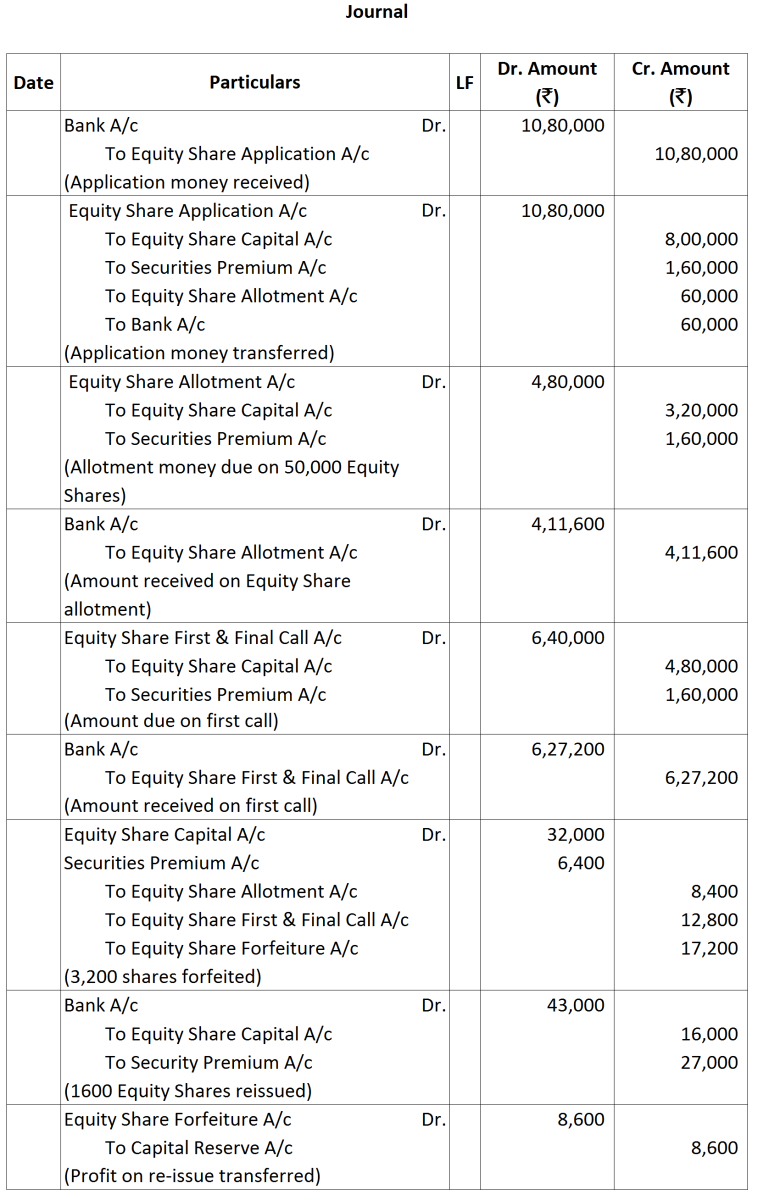

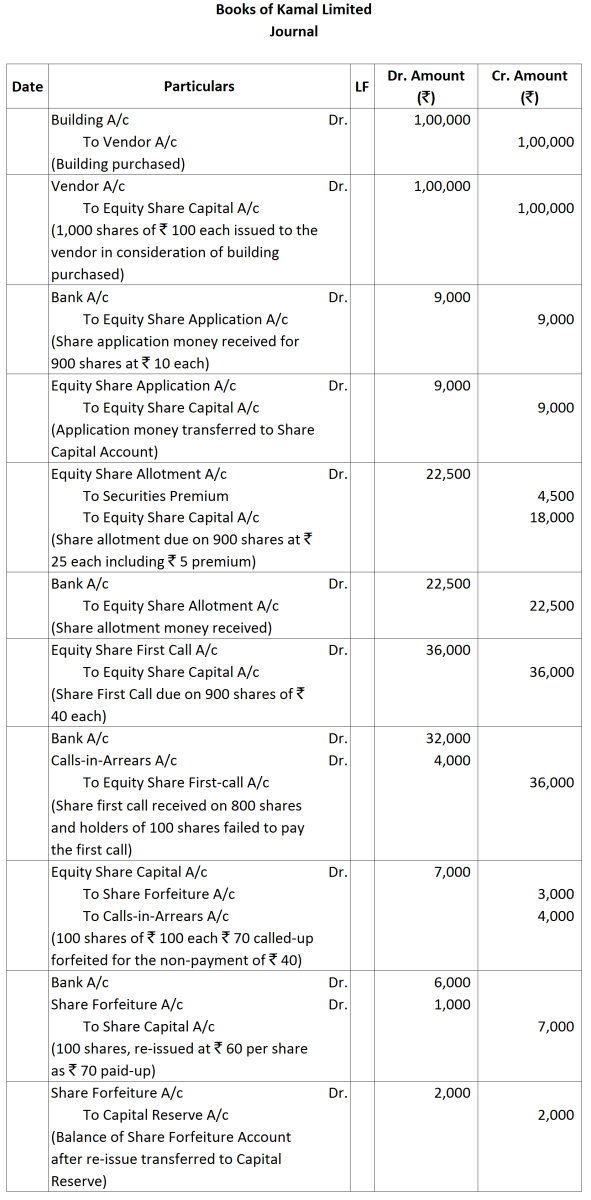

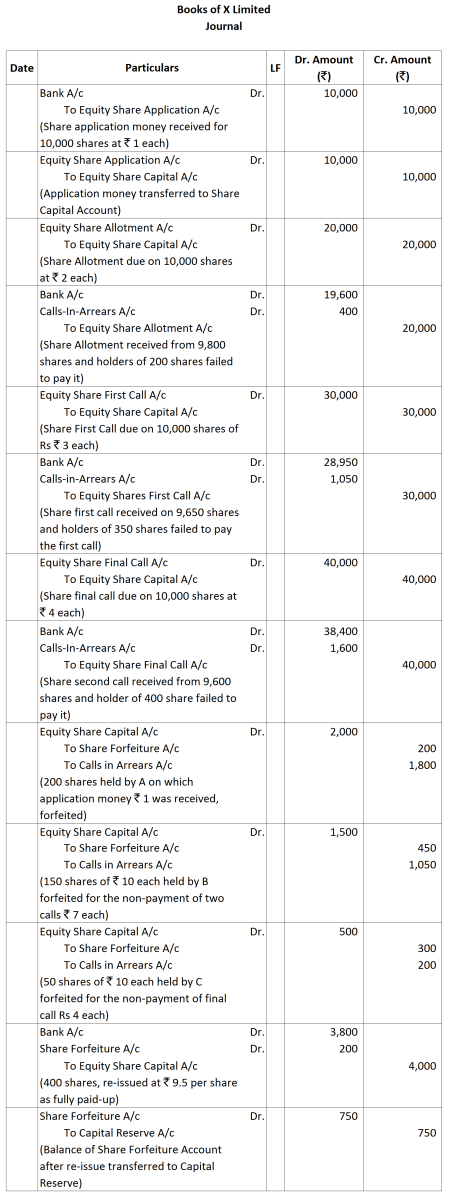

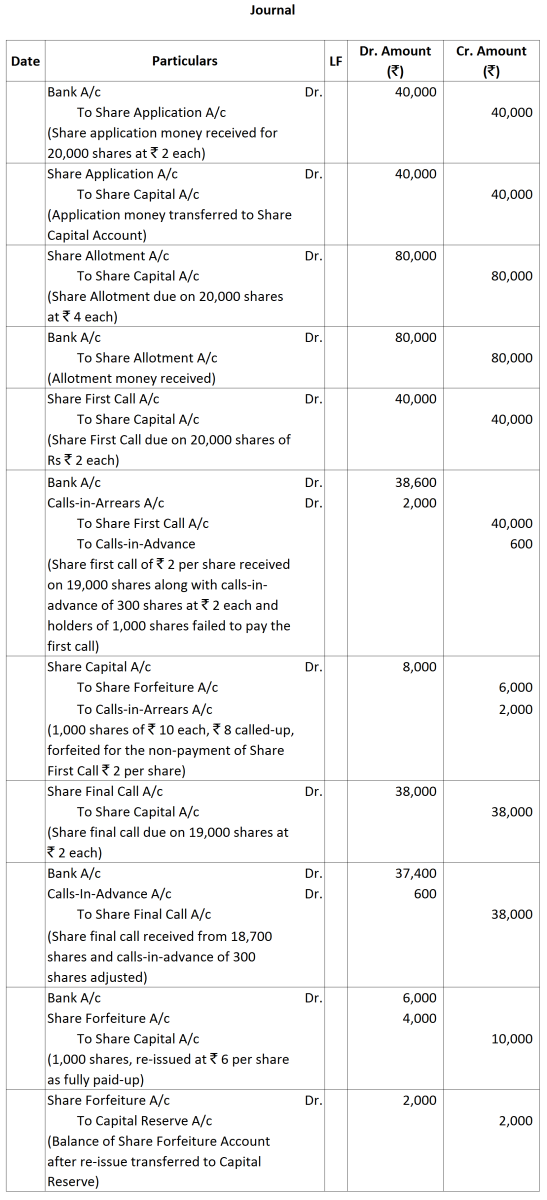

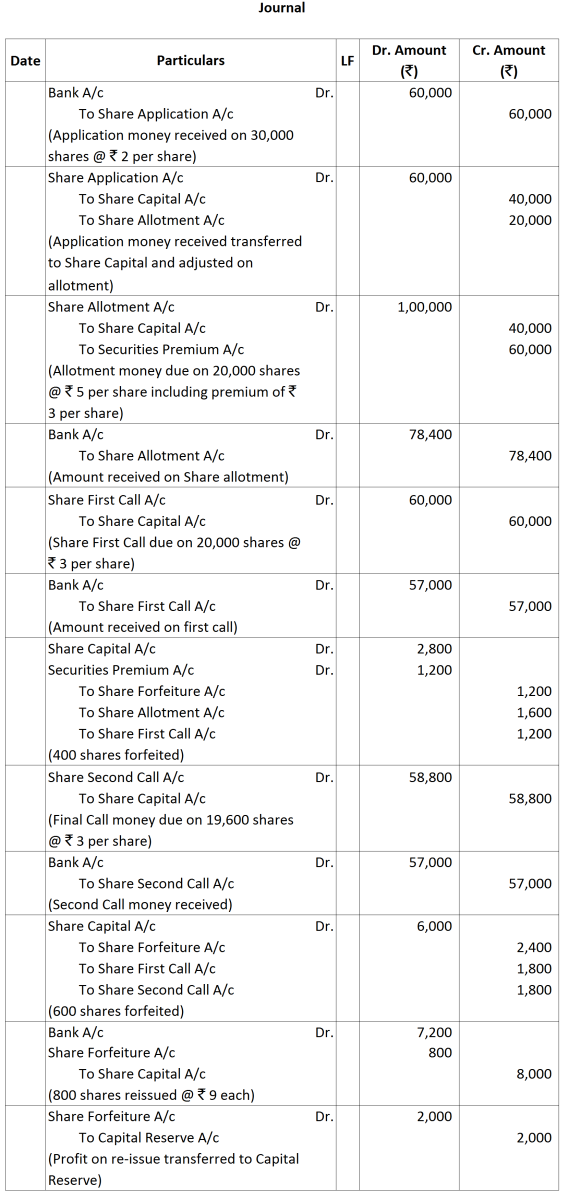

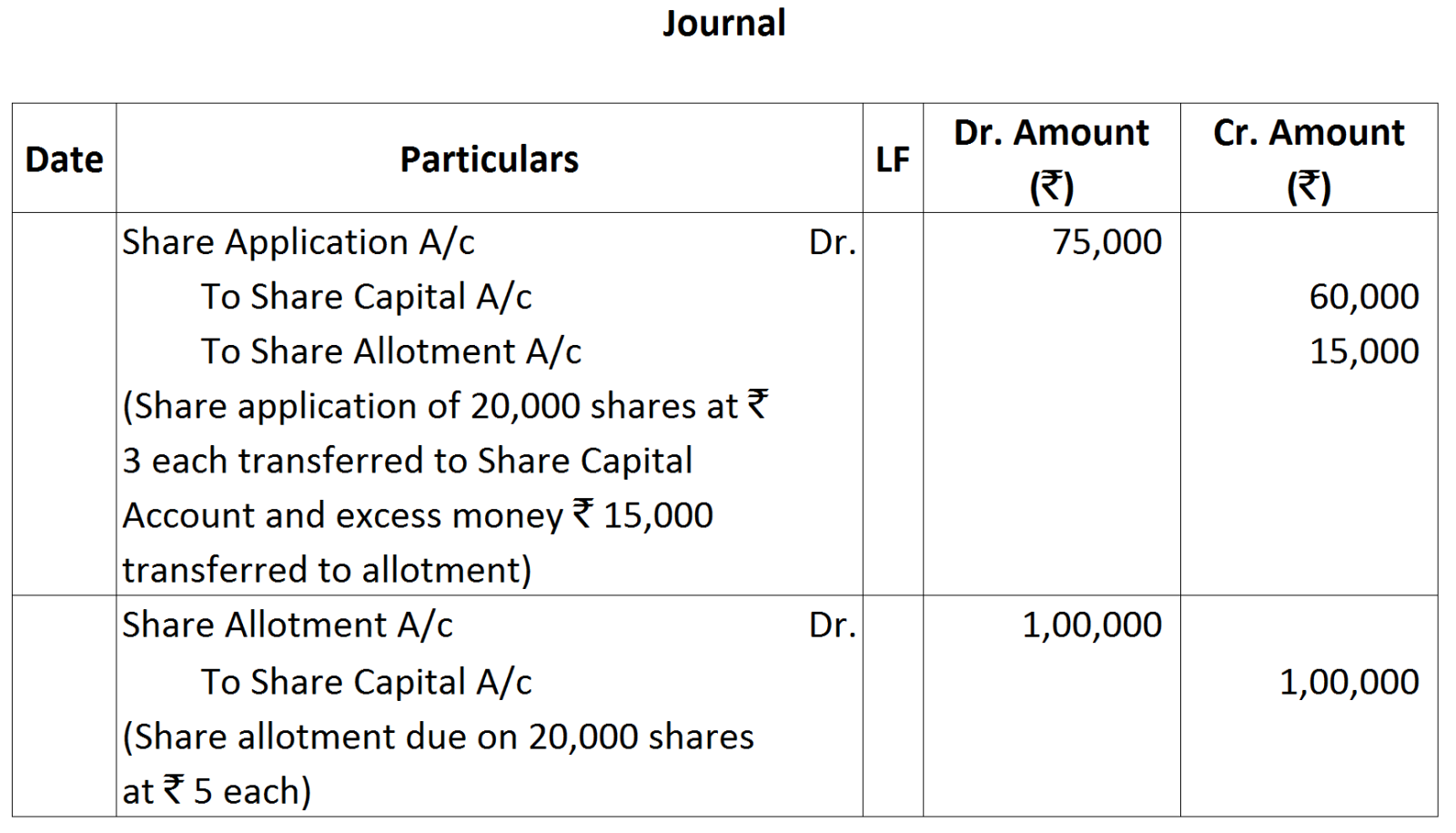

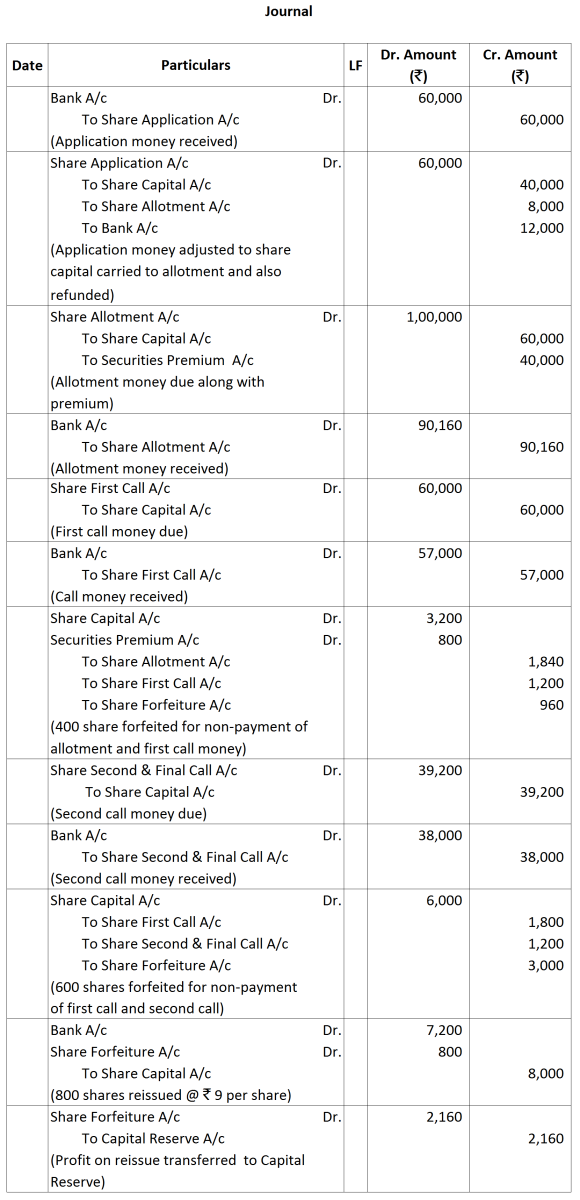

Working Notes:

Working Notes:

Working Notes:

Working Notes: Working Note:

Working Note:

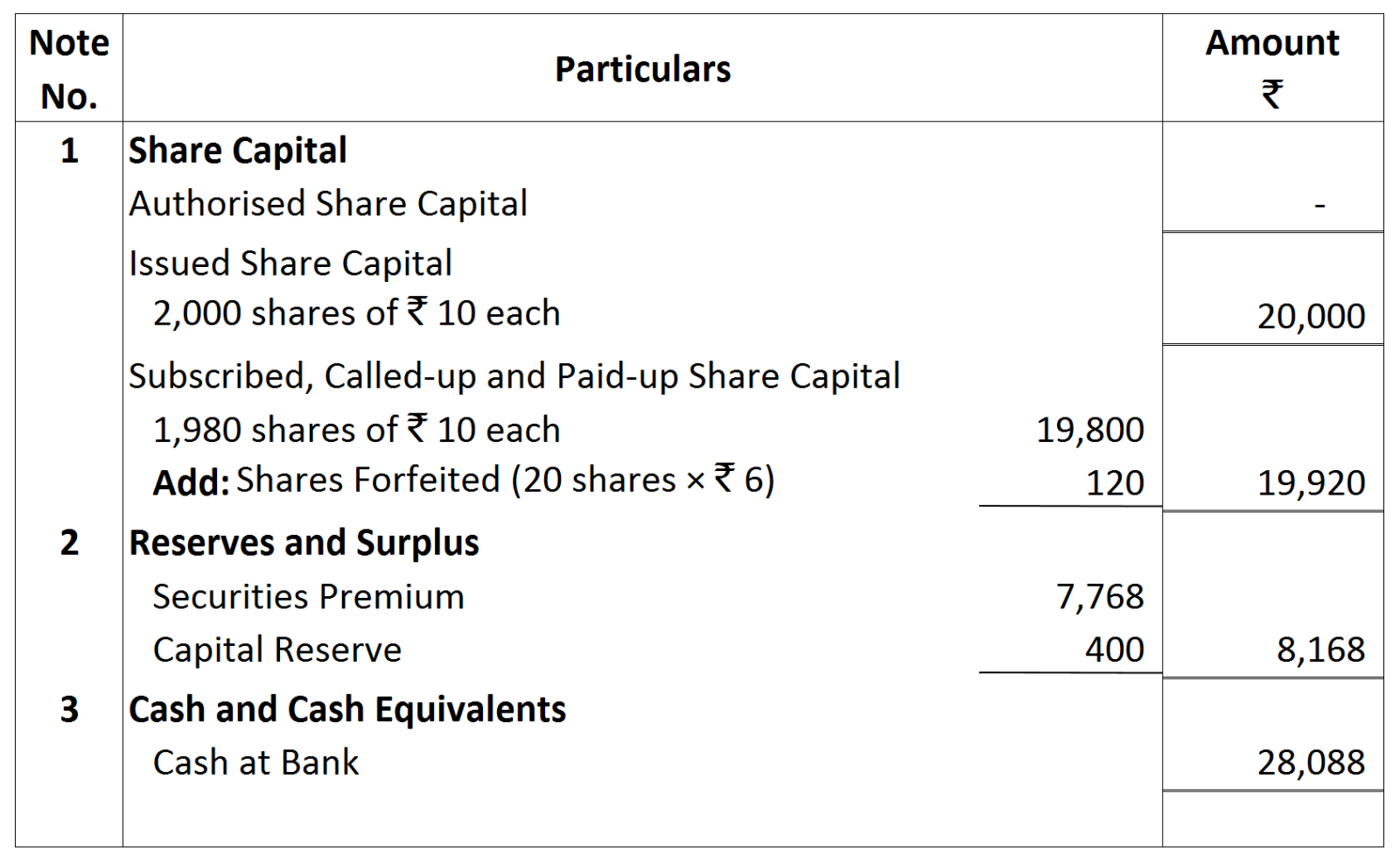

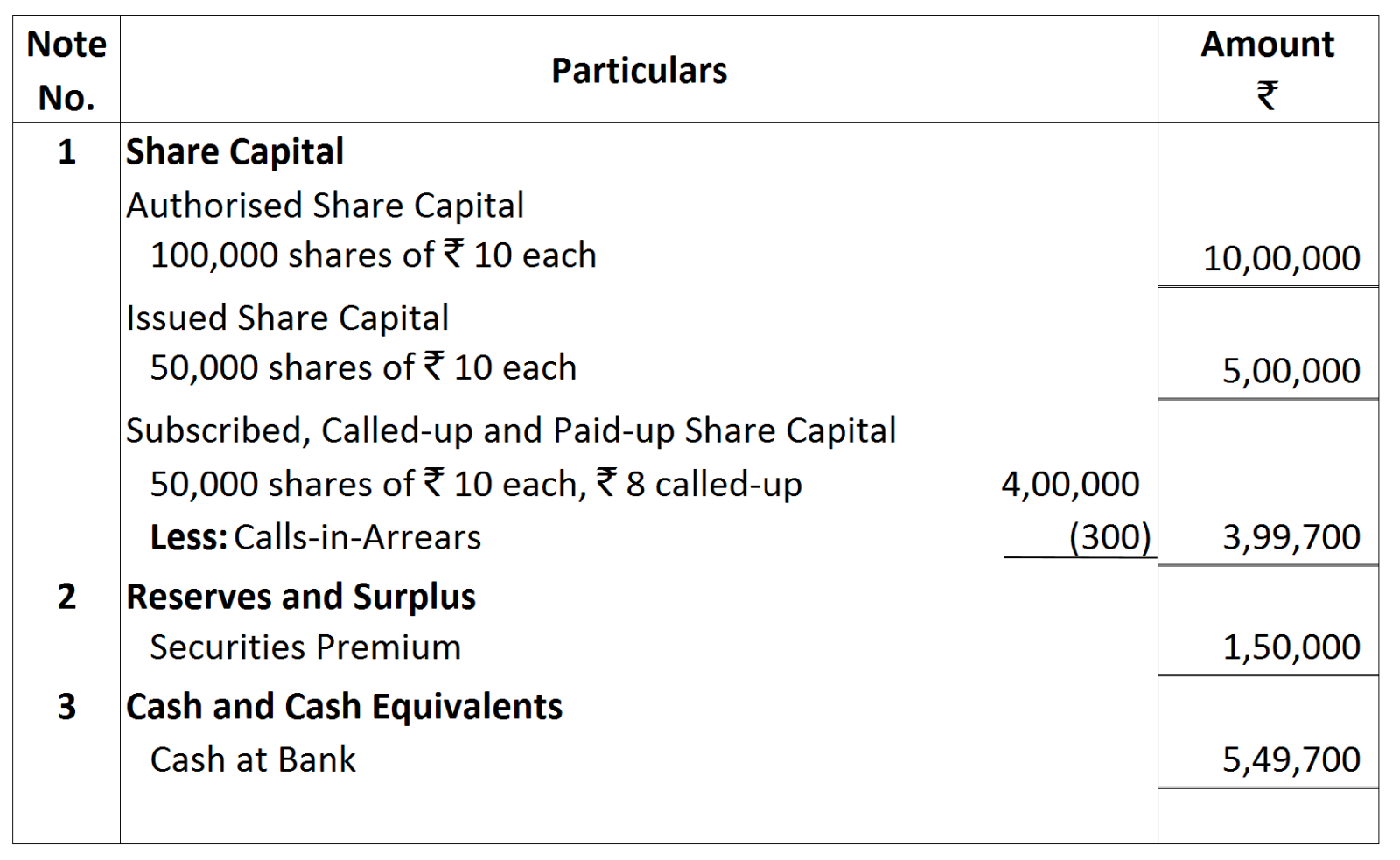

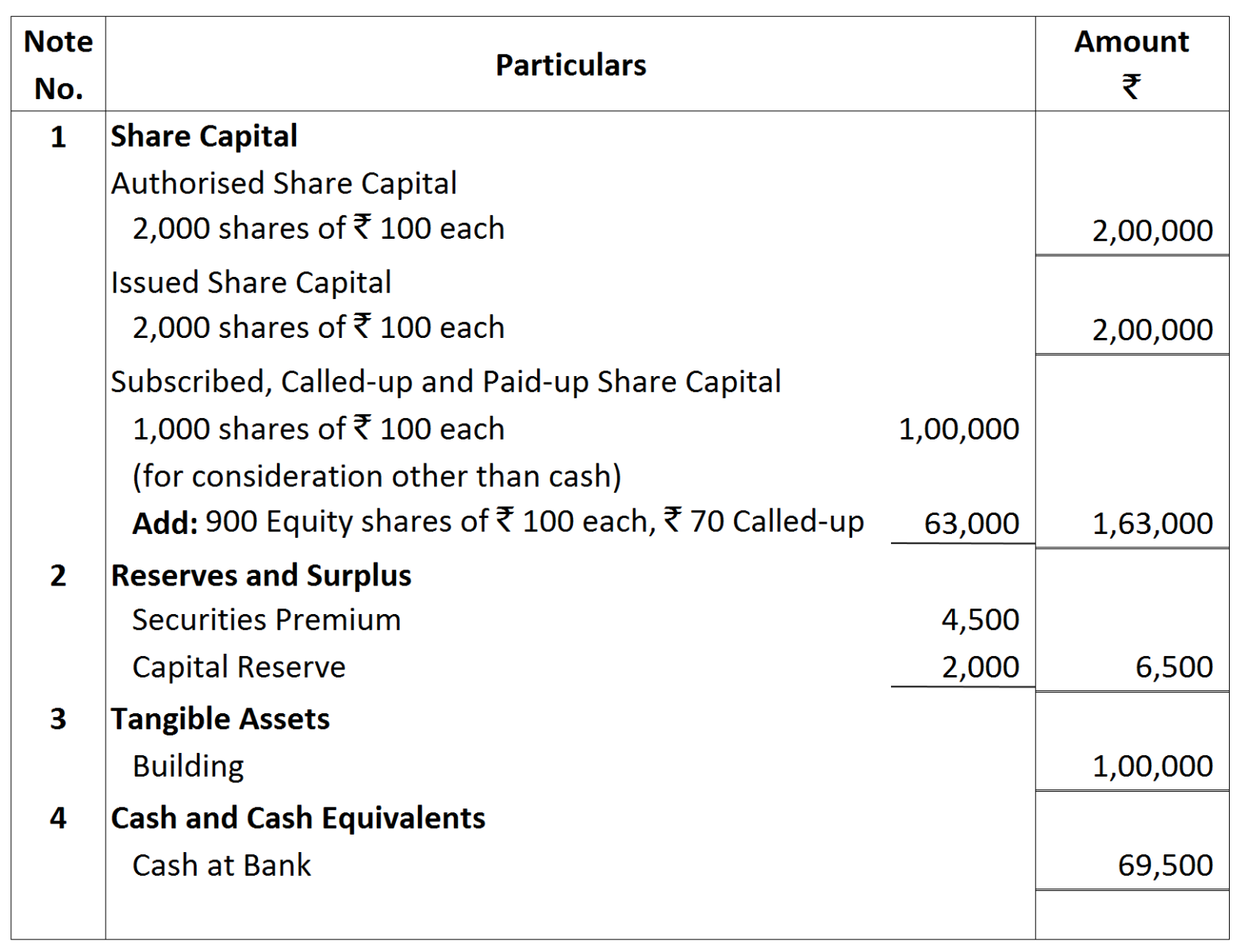

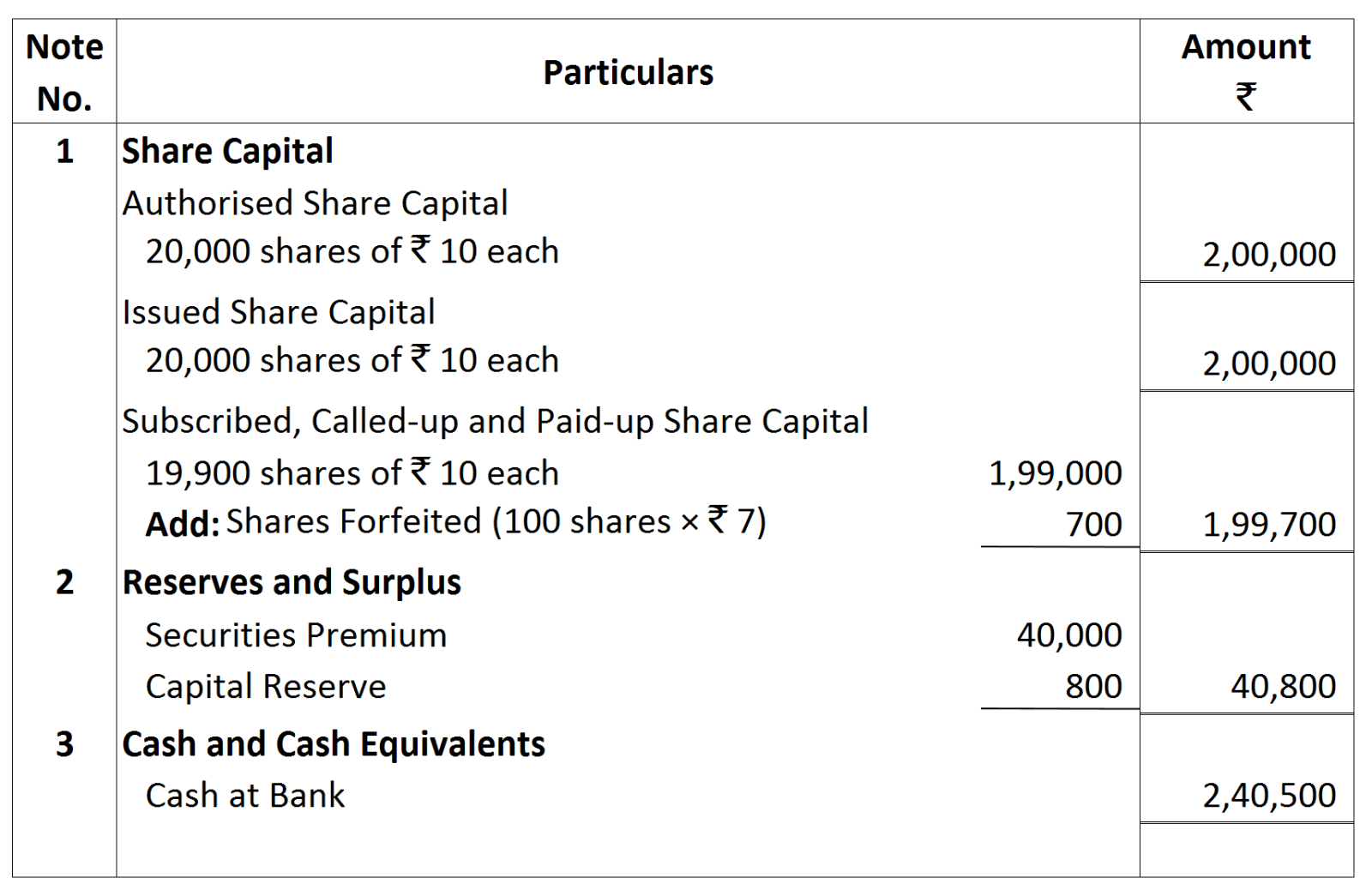

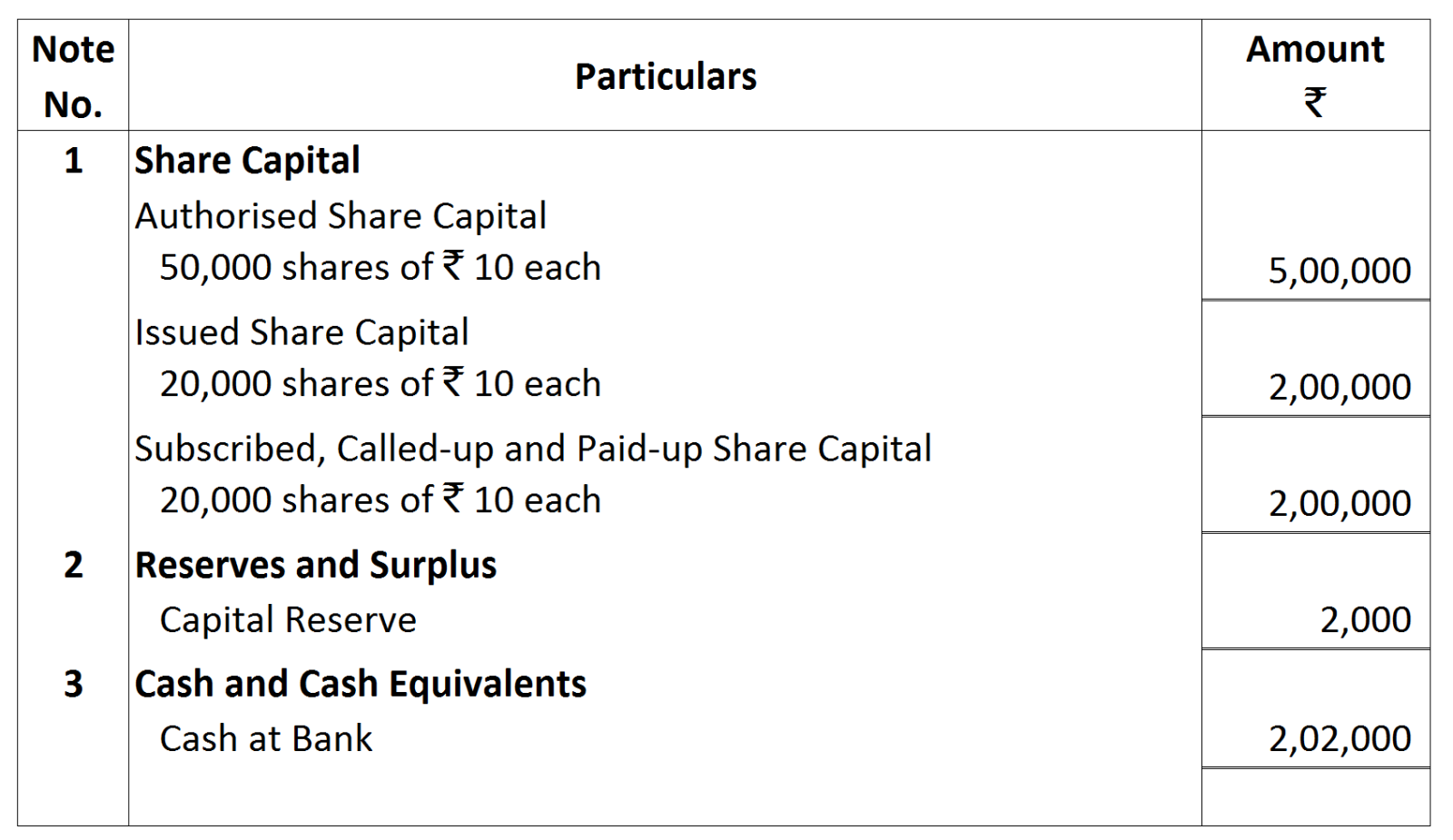

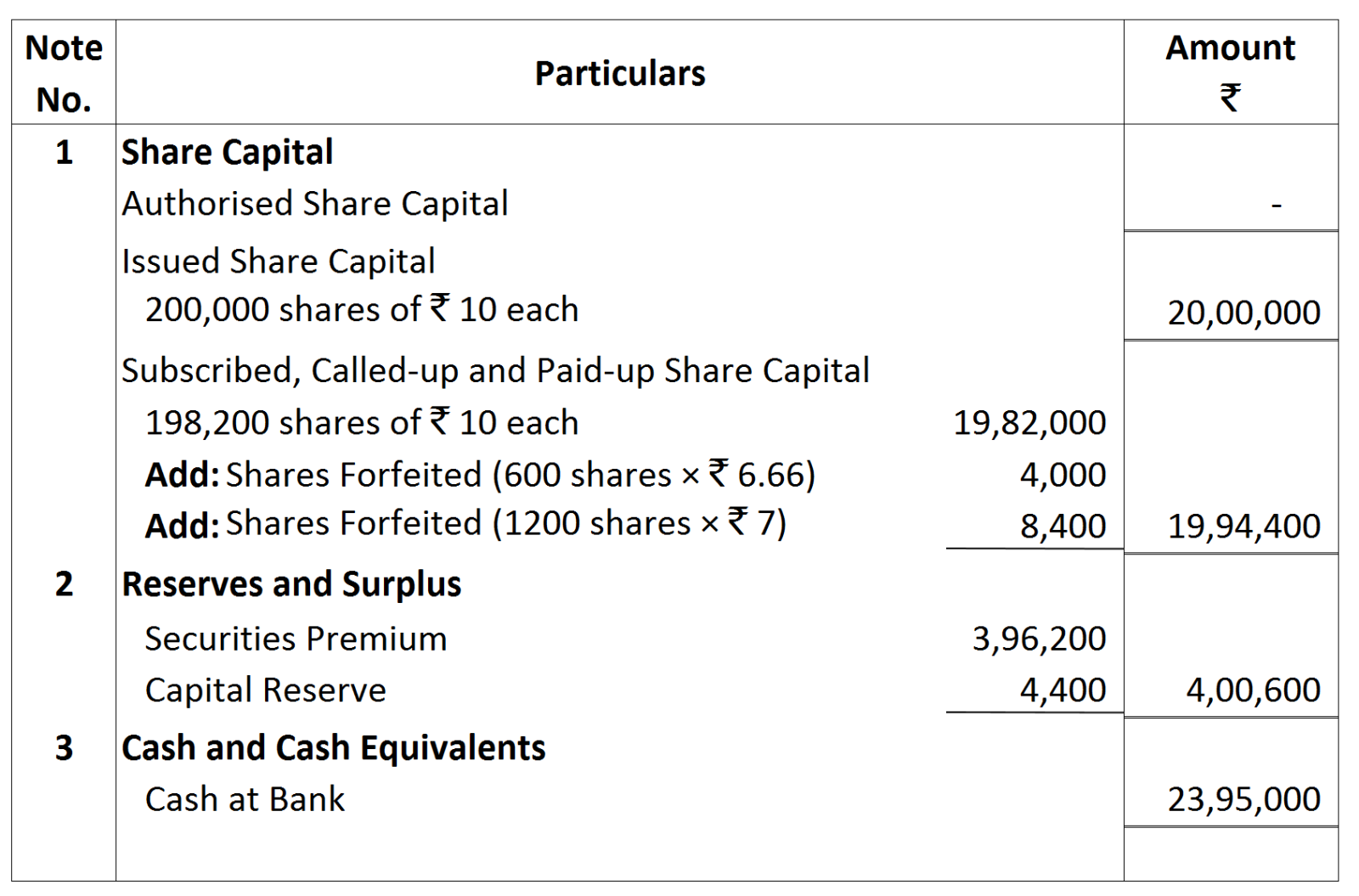

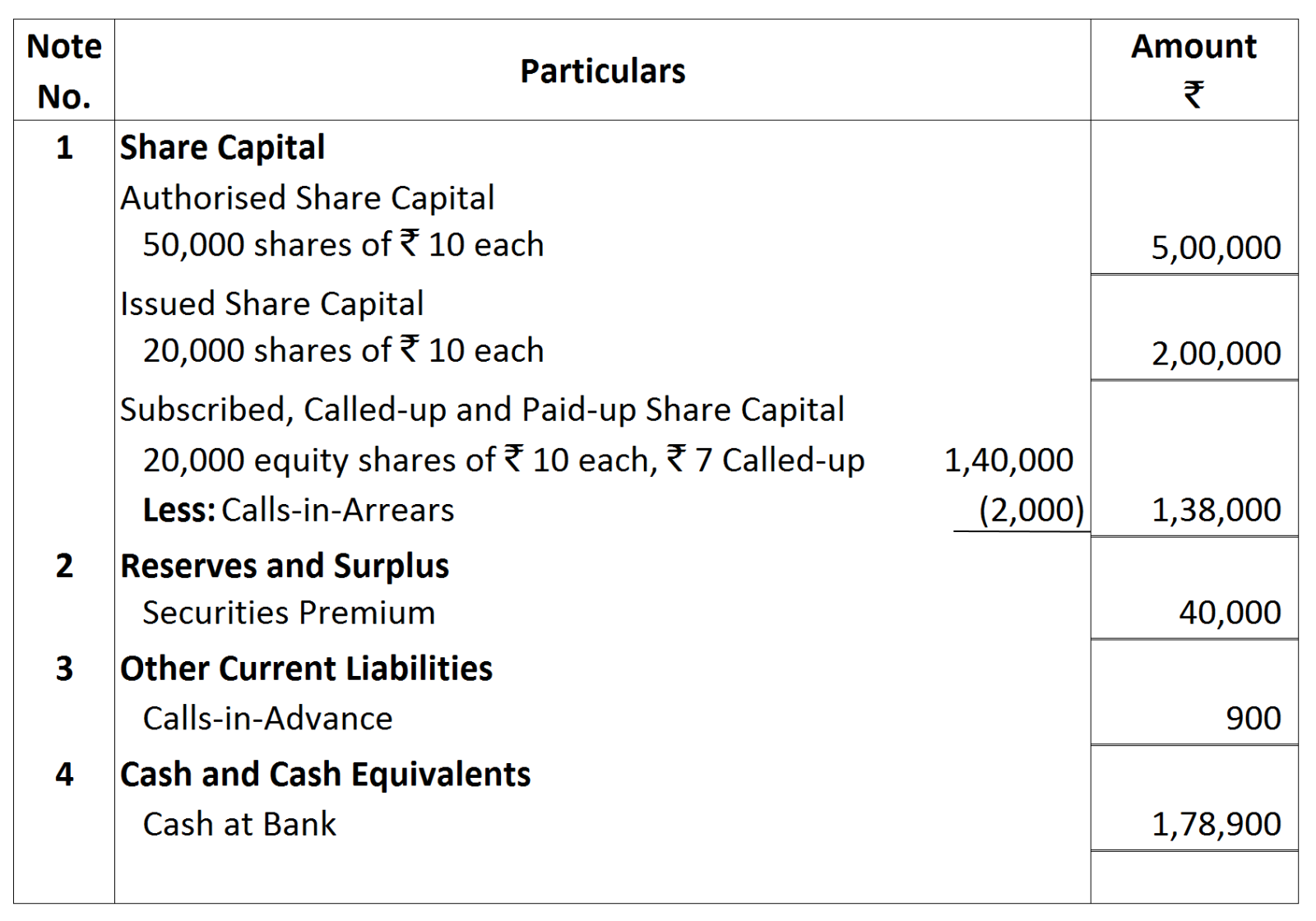

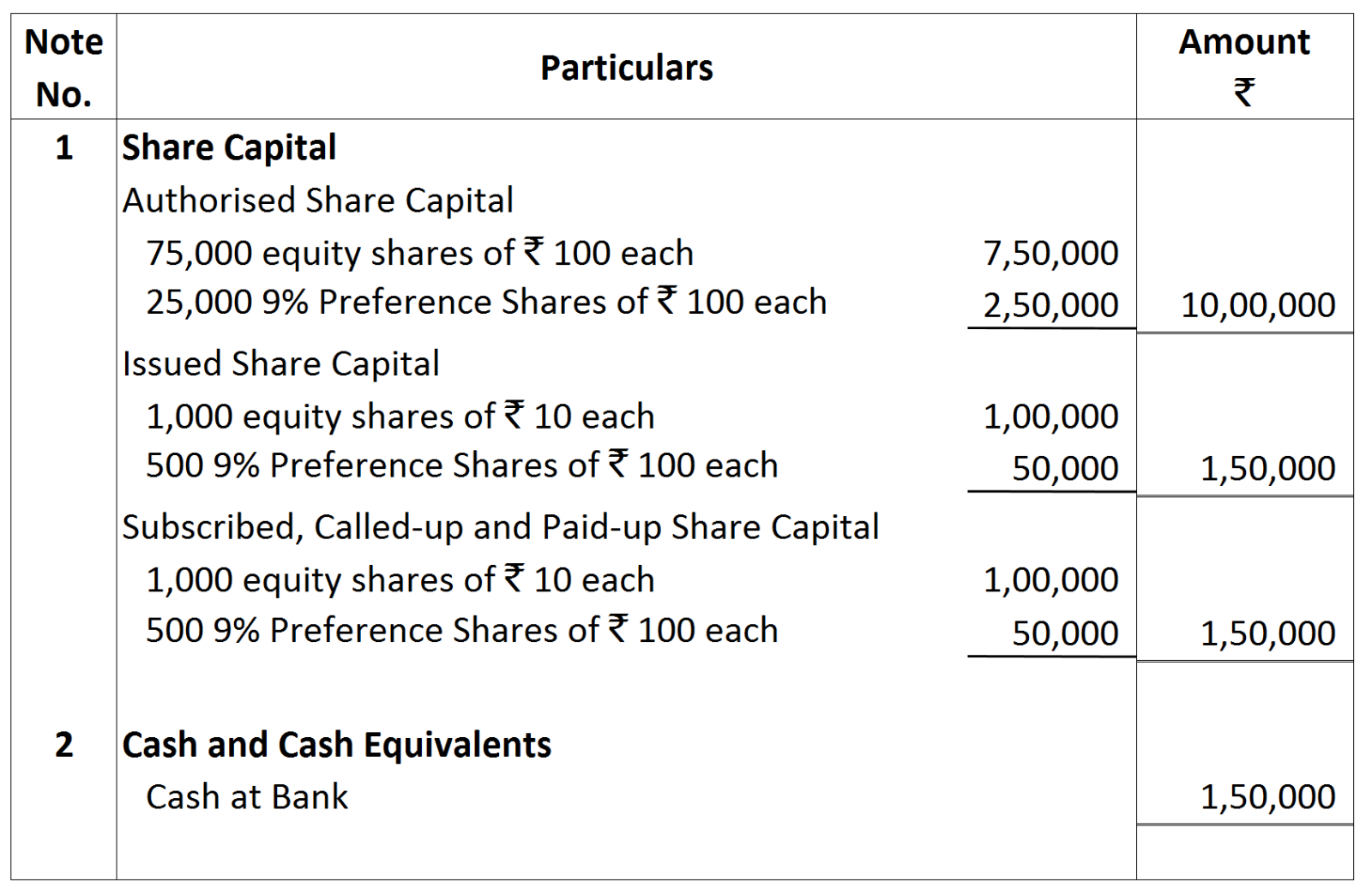

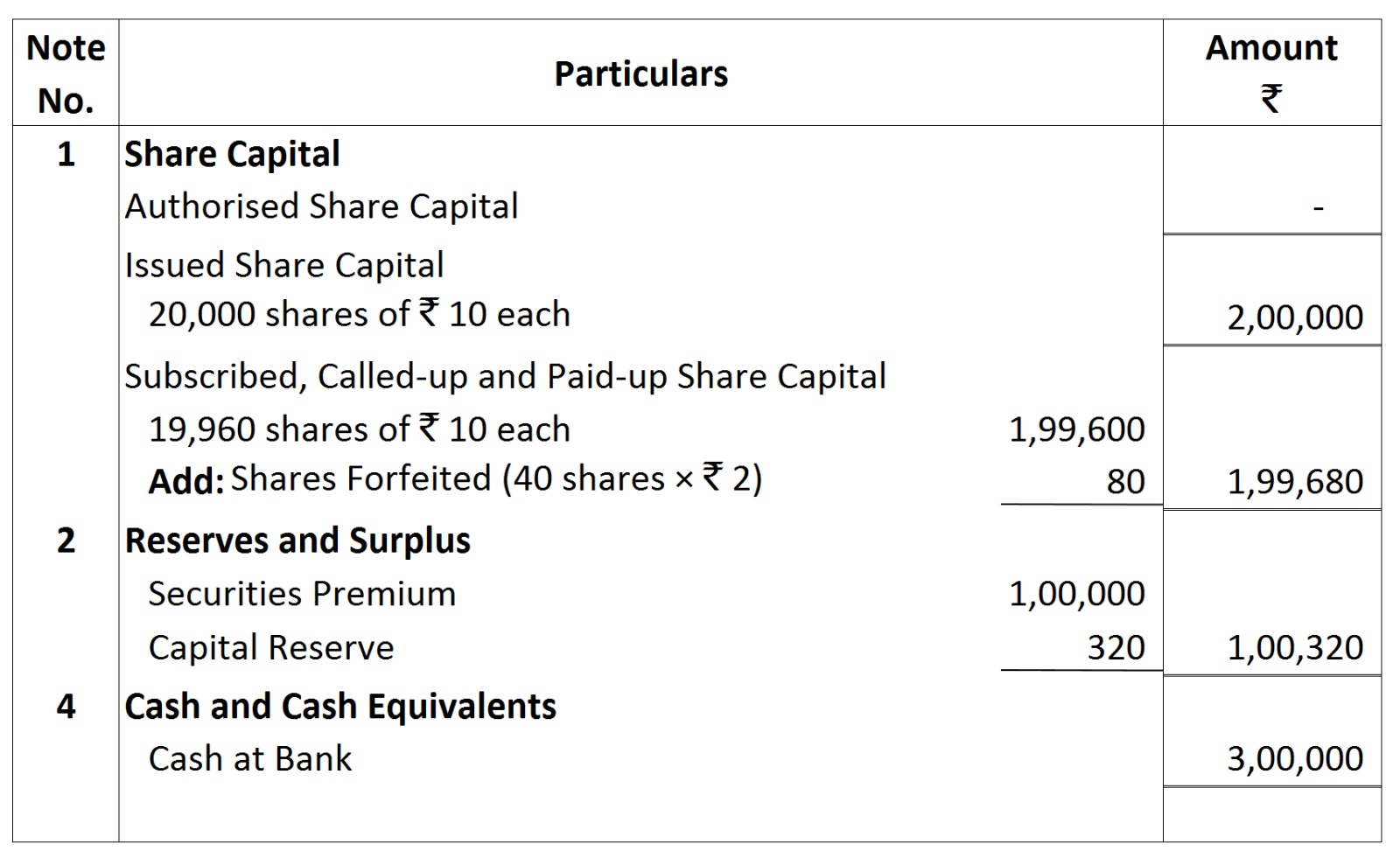

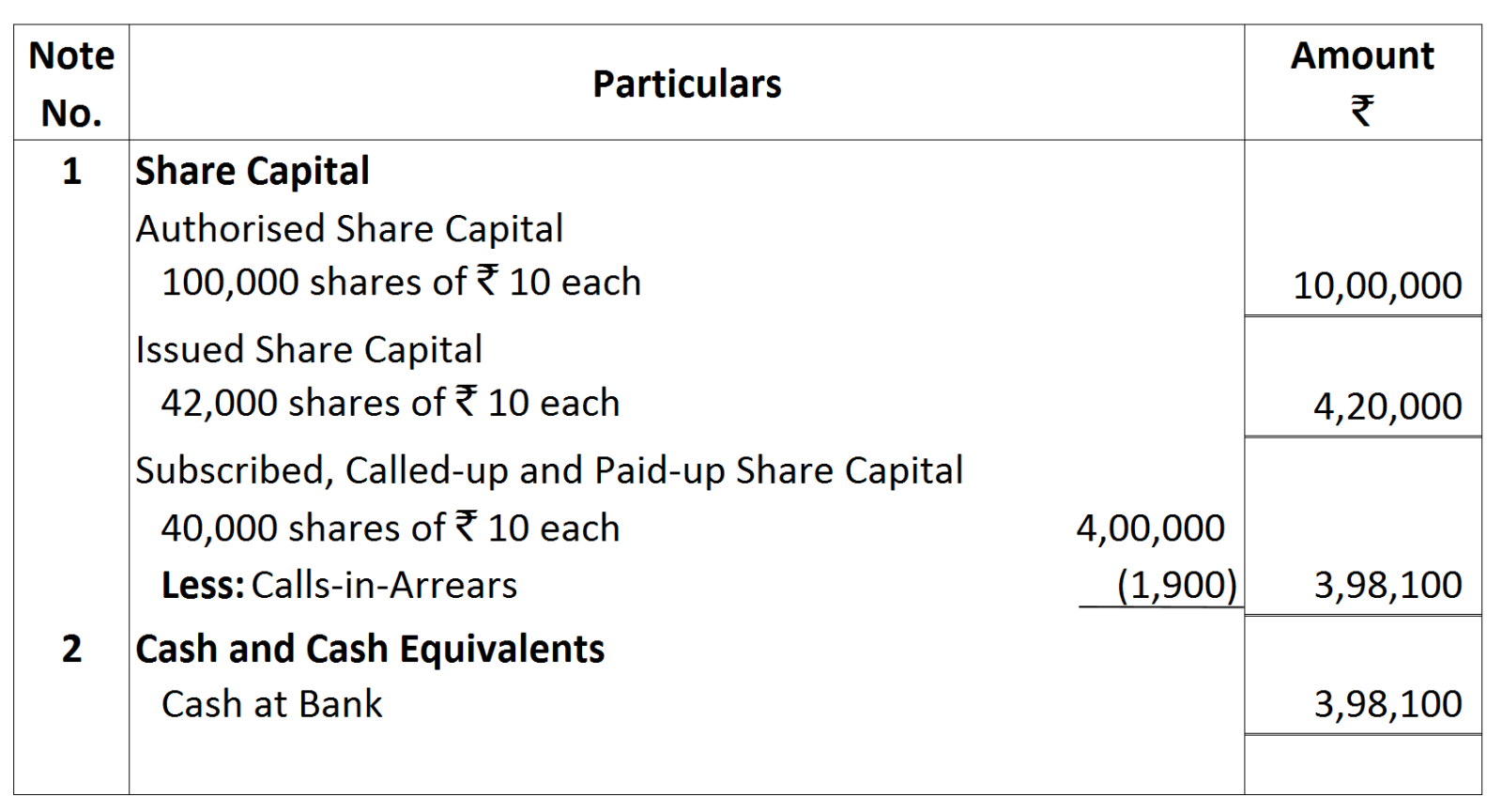

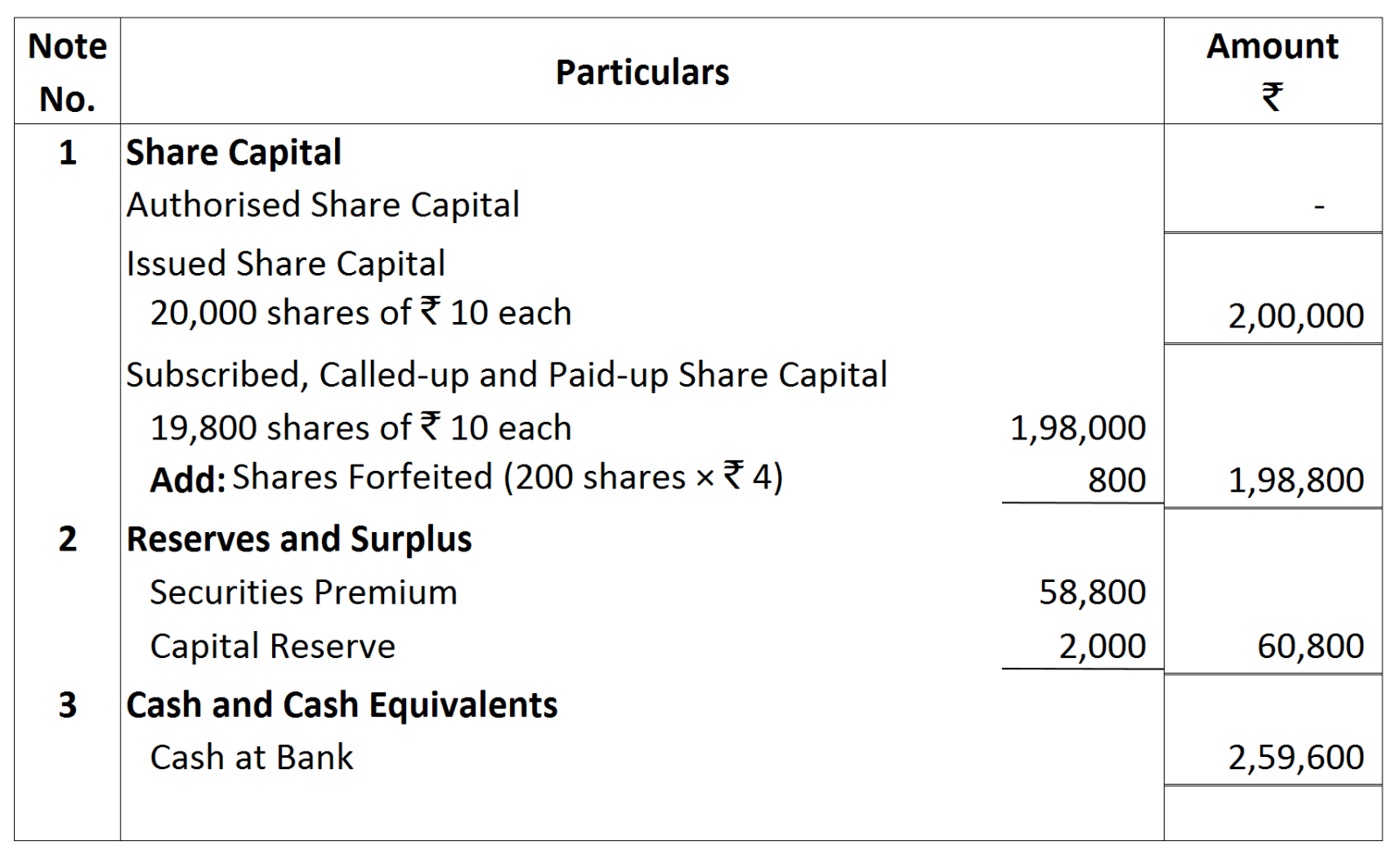

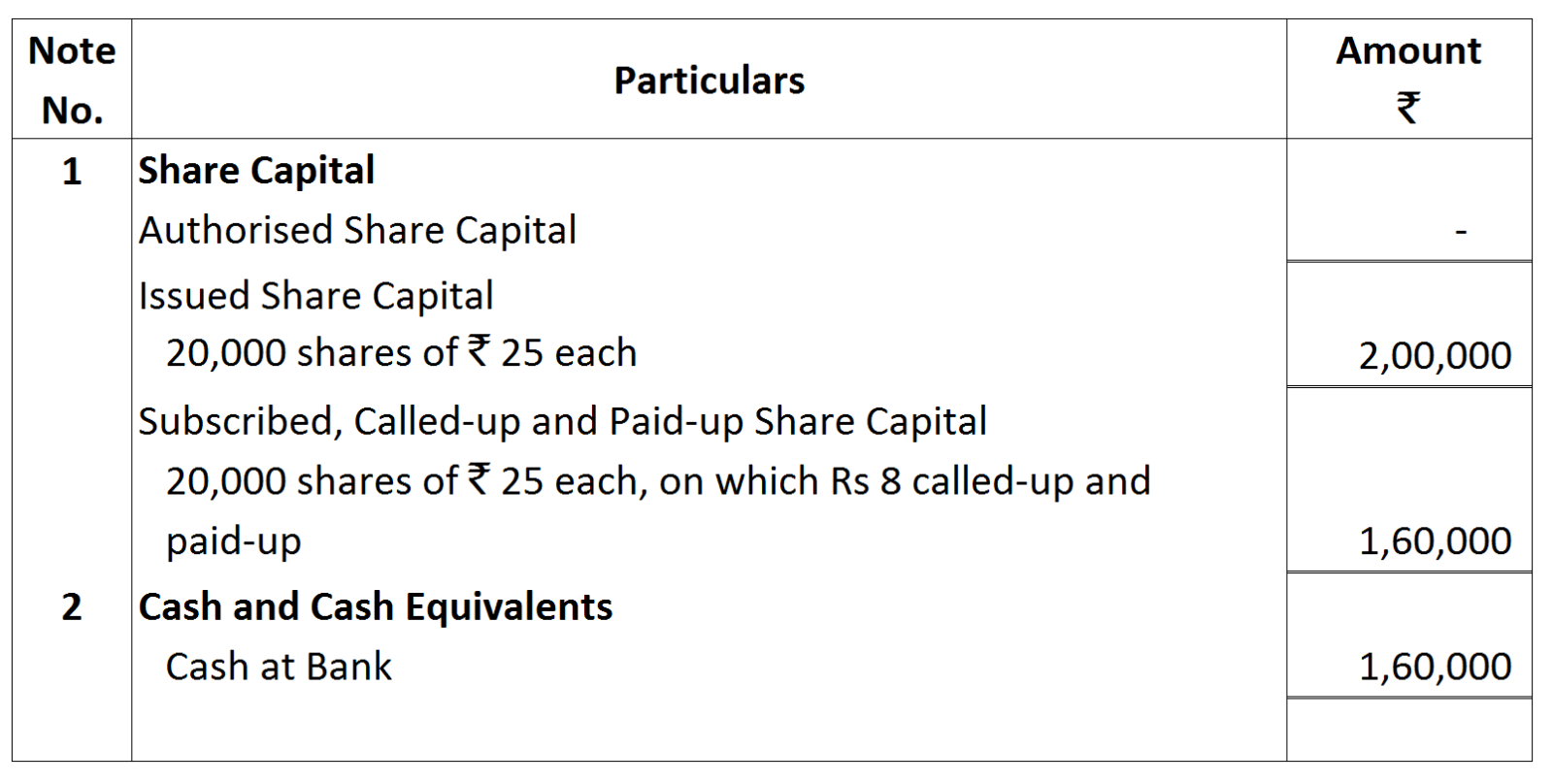

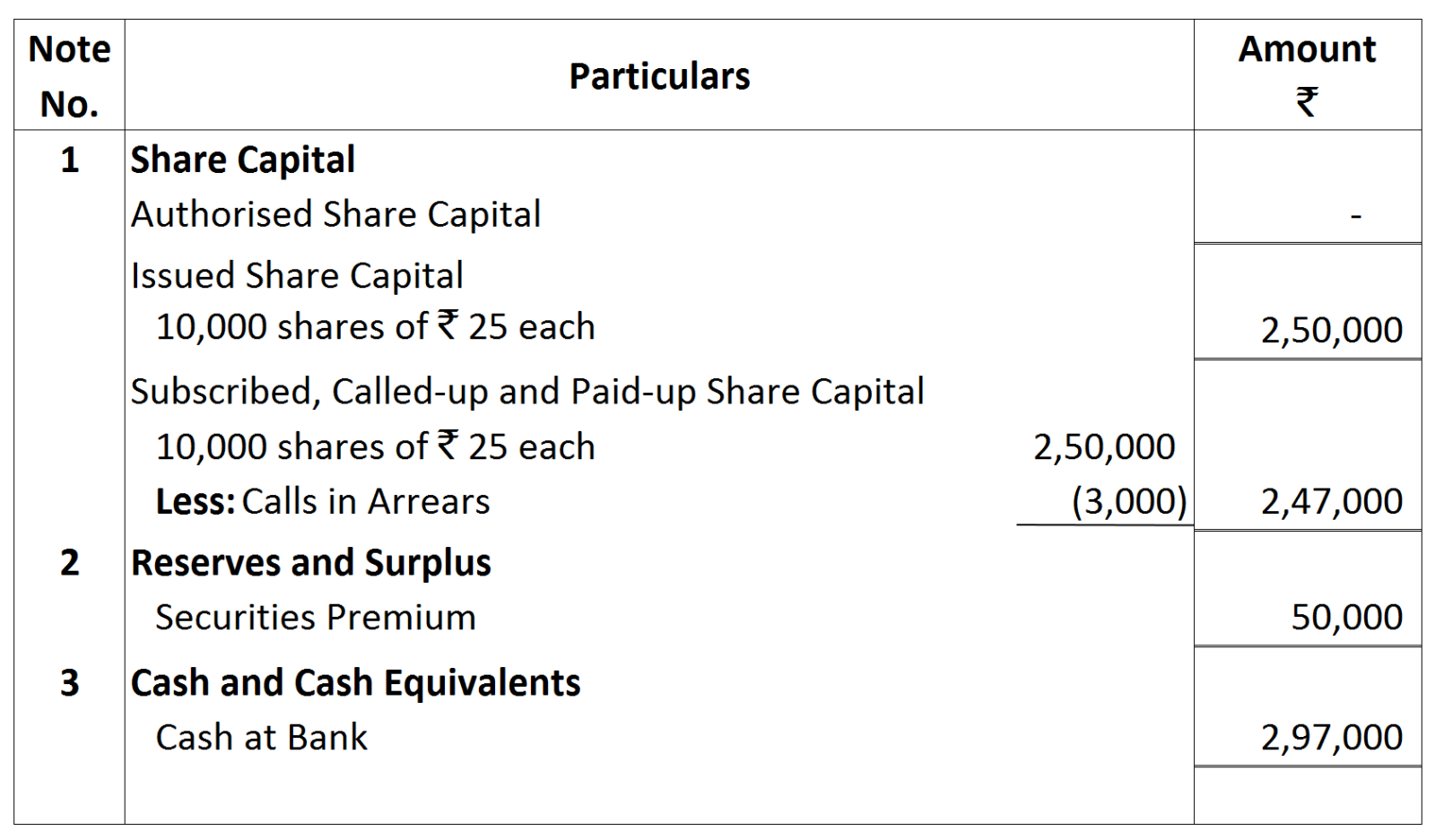

NOTES TO ACCOUNTS:

NOTES TO ACCOUNTS:

Working Notes:

Working Notes:

Notes to Account:

Notes to Account:

Working Notes:

Working Notes:

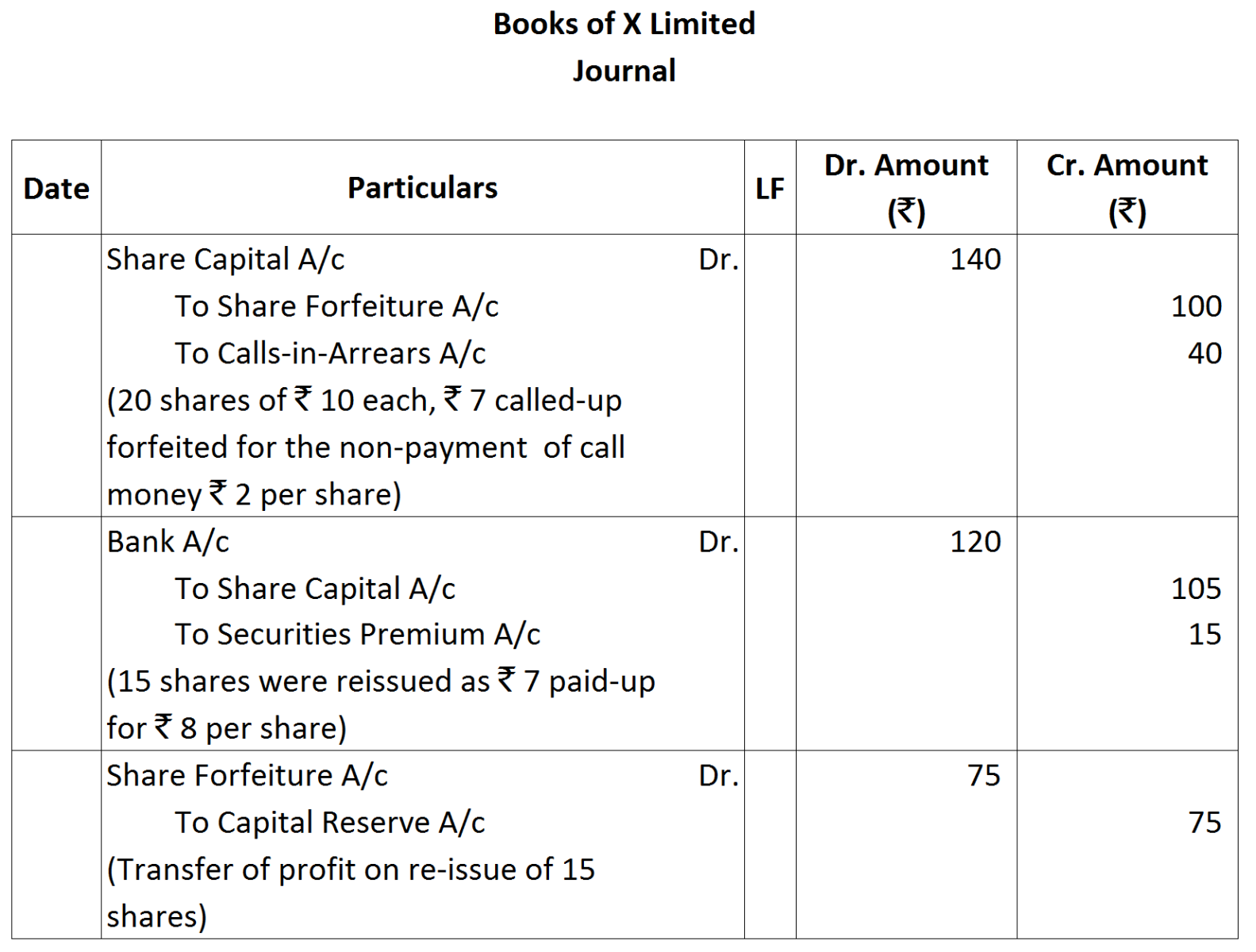

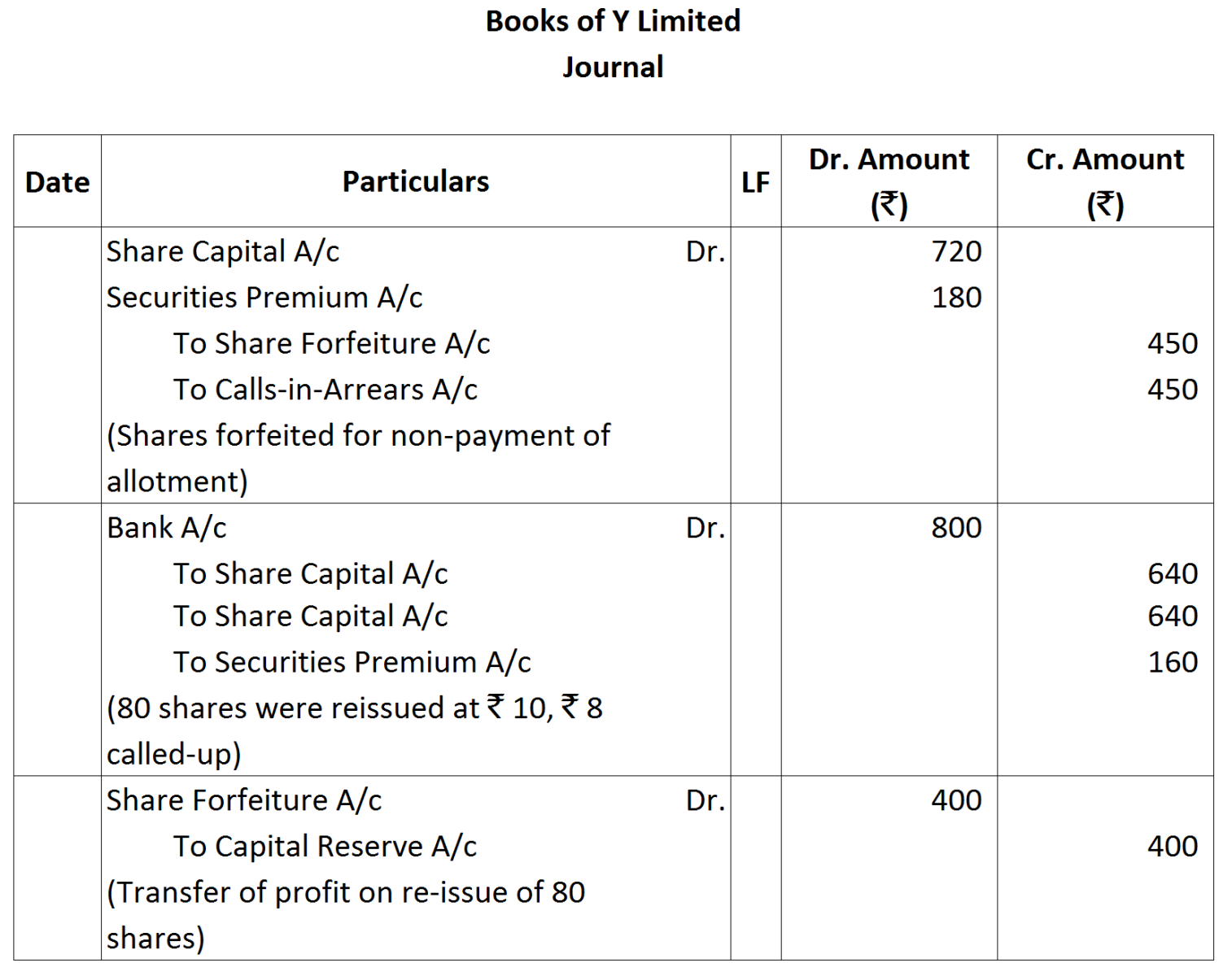

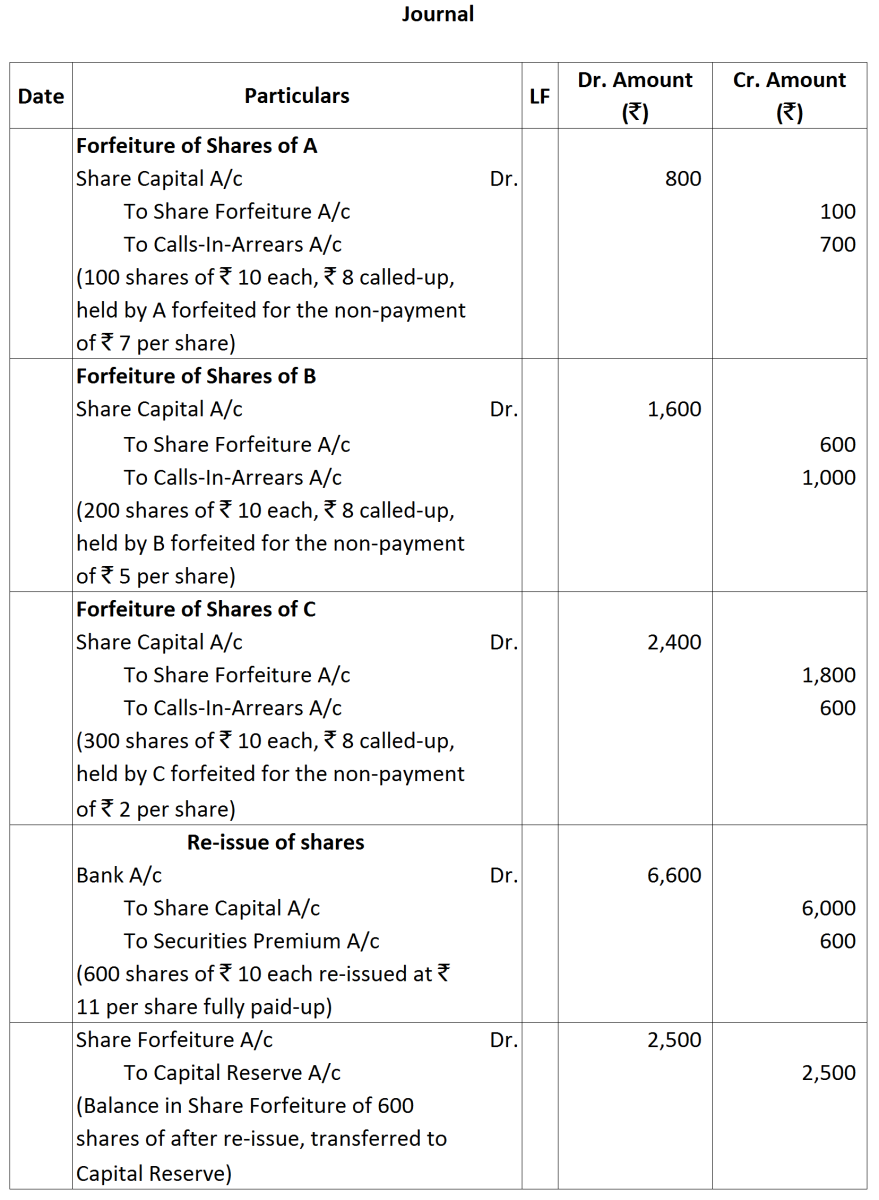

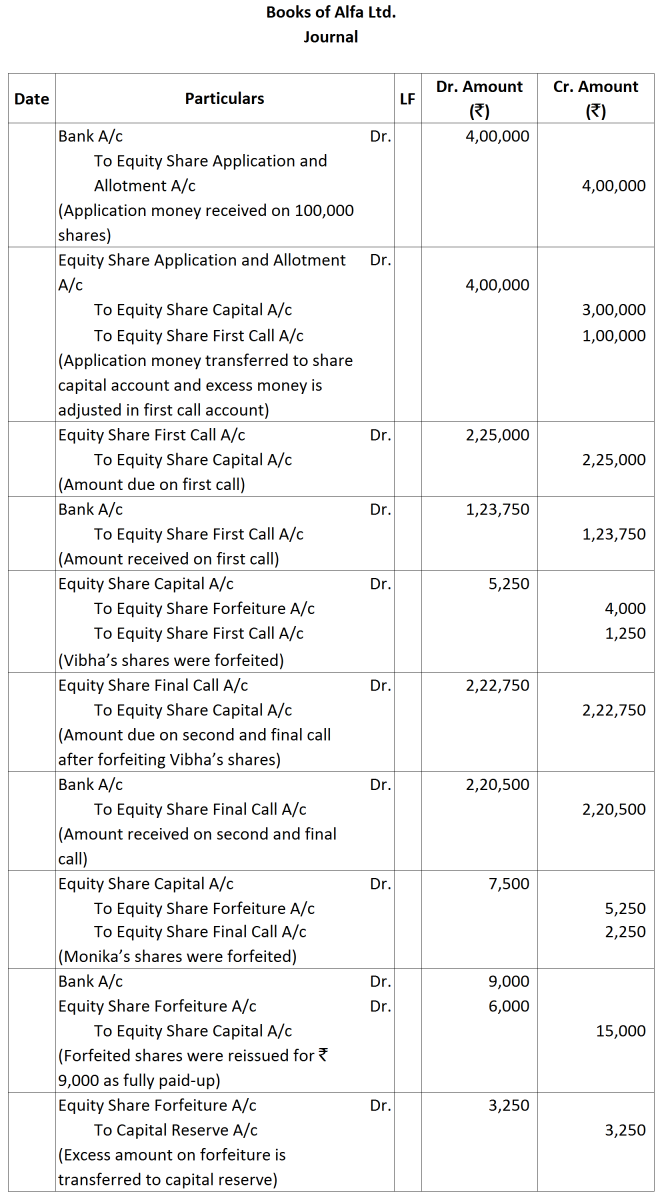

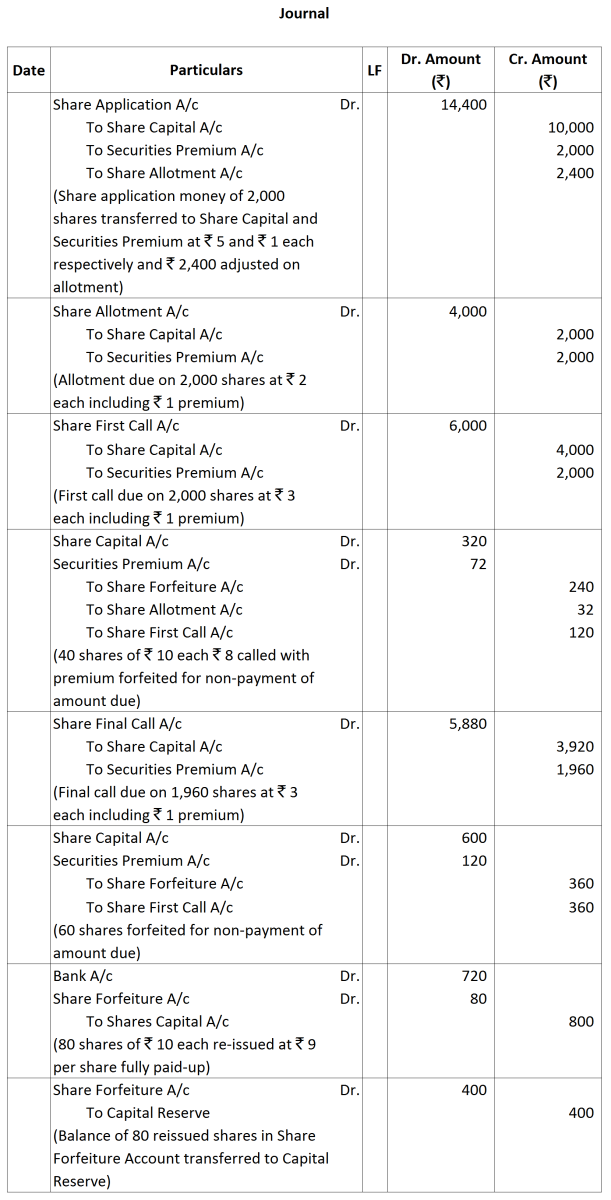

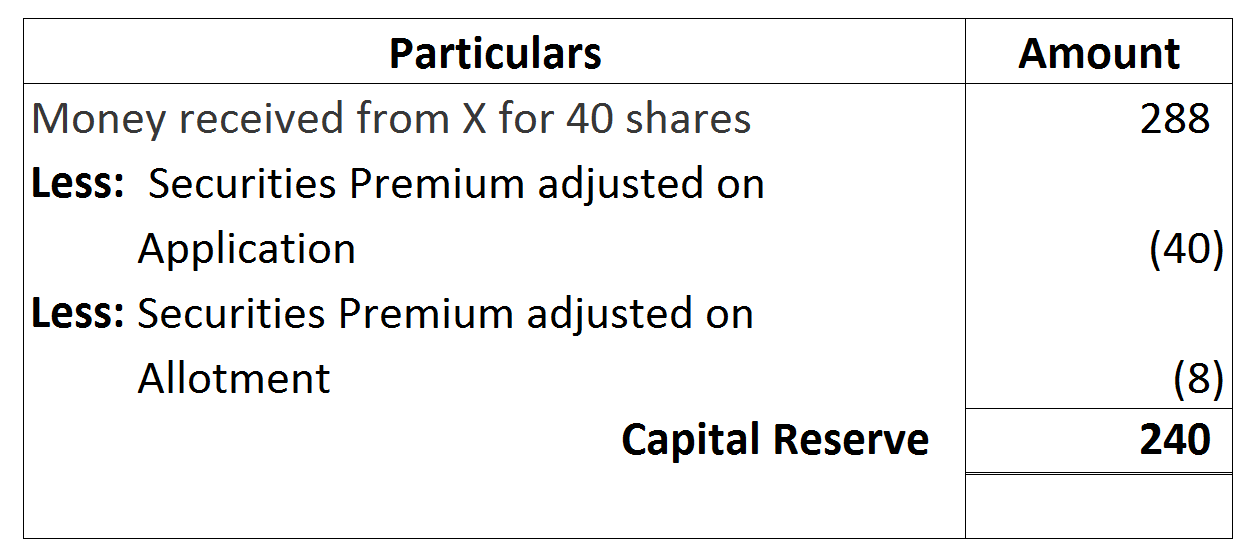

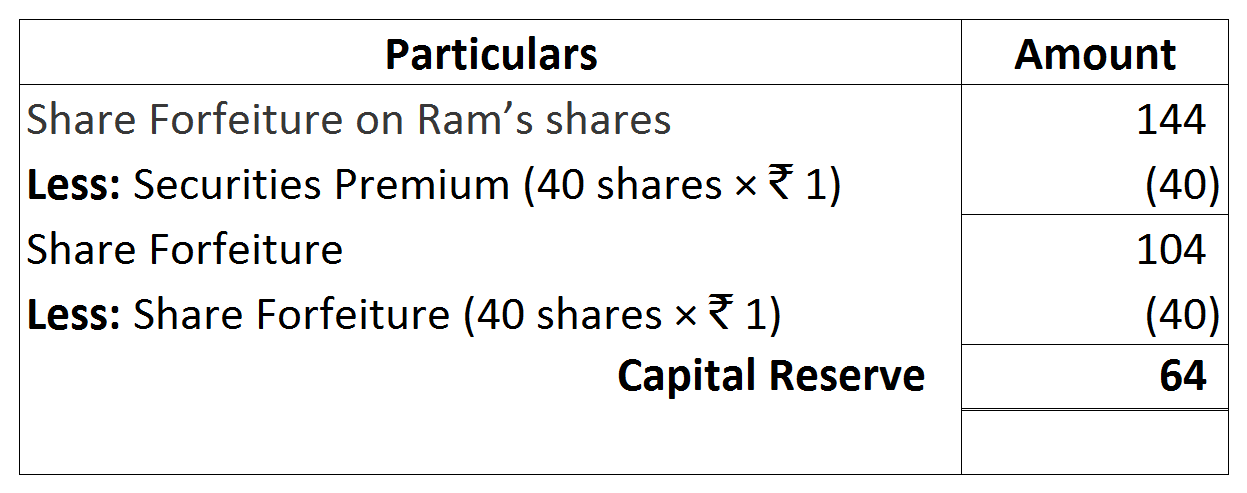

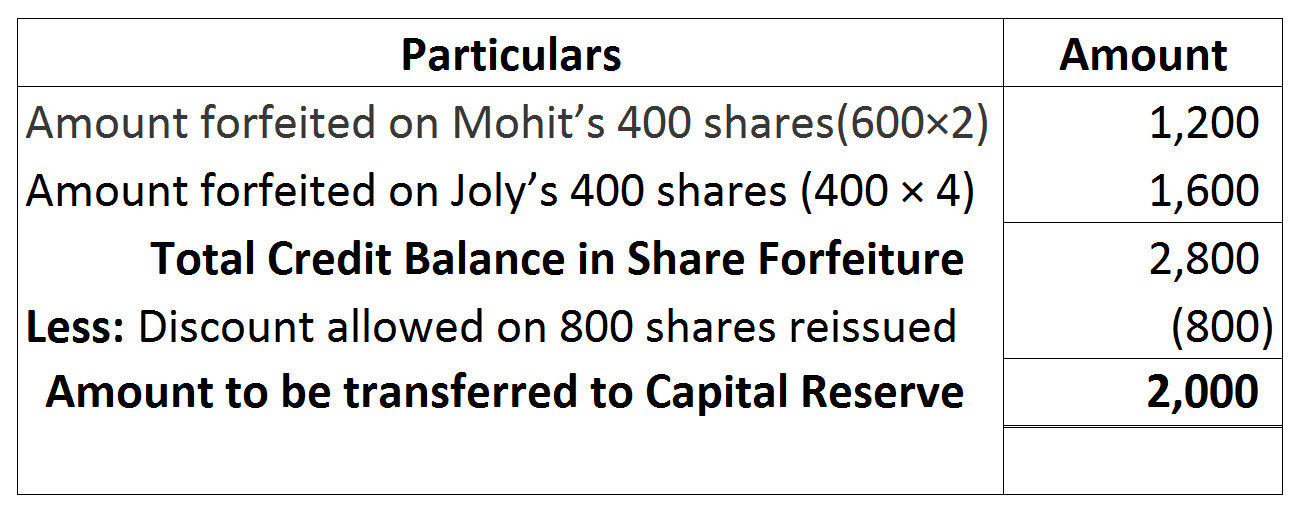

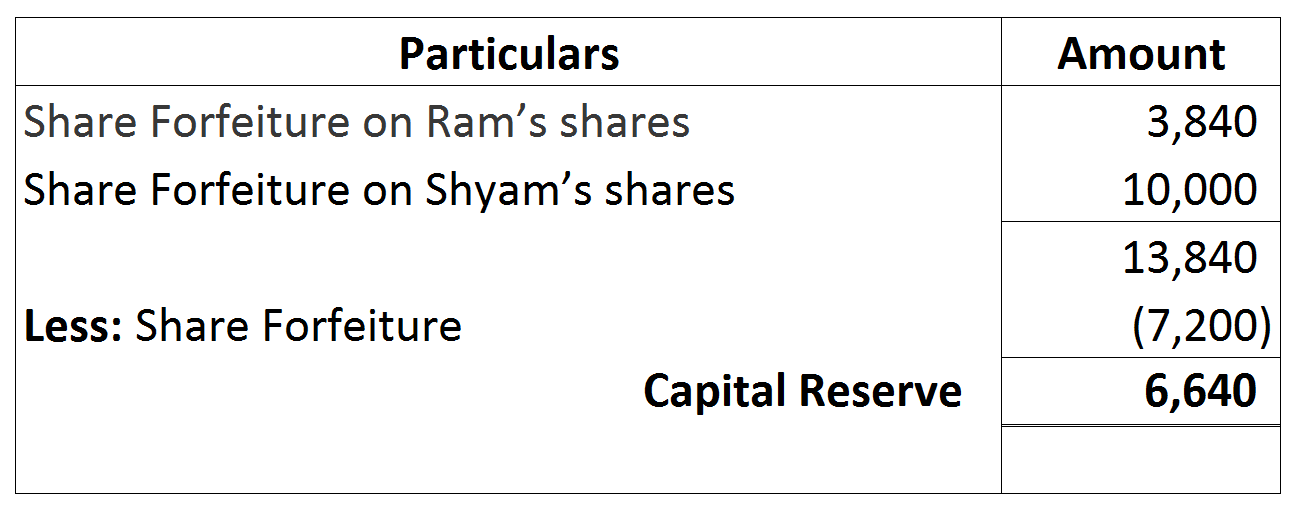

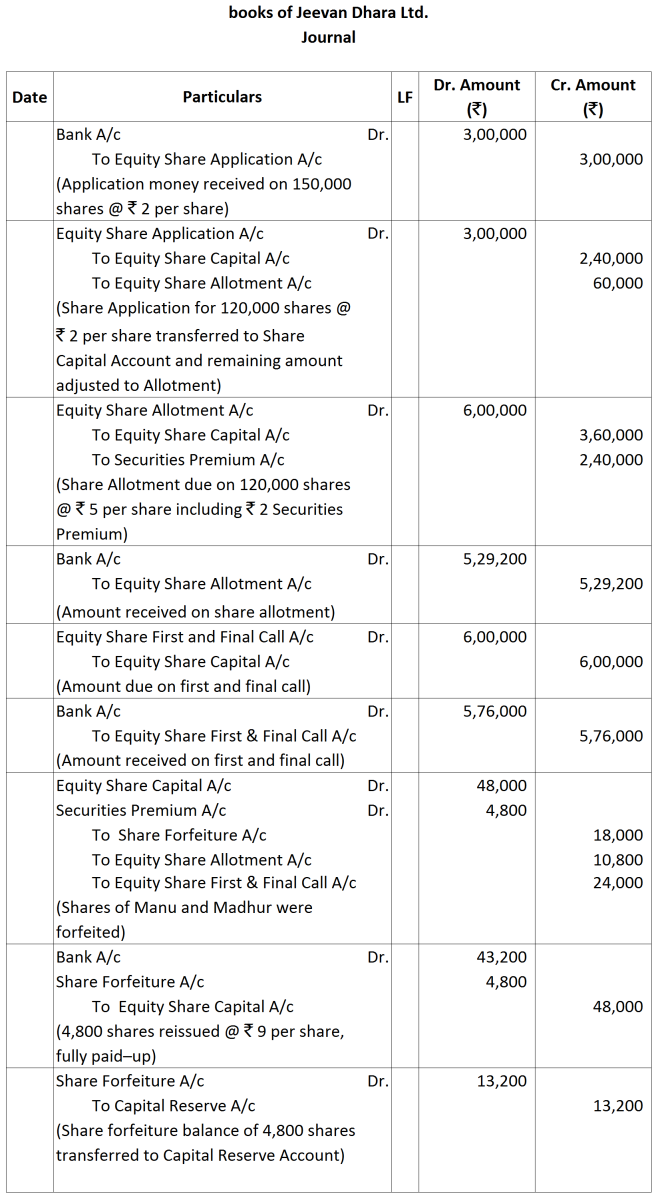

Capital Reserve on re-issue of 20 shares = ₹ 5 × 20 shares = ₹ 100 Y’s Shares: Share Forfeiture on 60 Shares of Y

Capital Reserve on re-issue of 20 shares = ₹ 5 × 20 shares = ₹ 100 Y’s Shares: Share Forfeiture on 60 Shares of Y

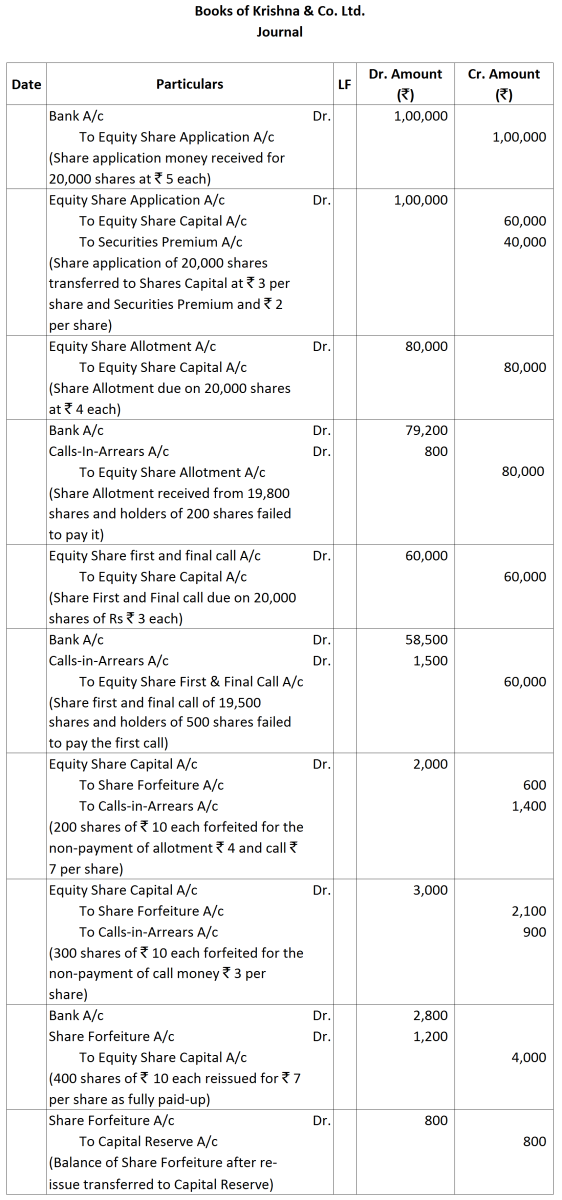

Working Notes:

Working Notes:

NOTES TO ACCOUNTS:

NOTES TO ACCOUNTS:

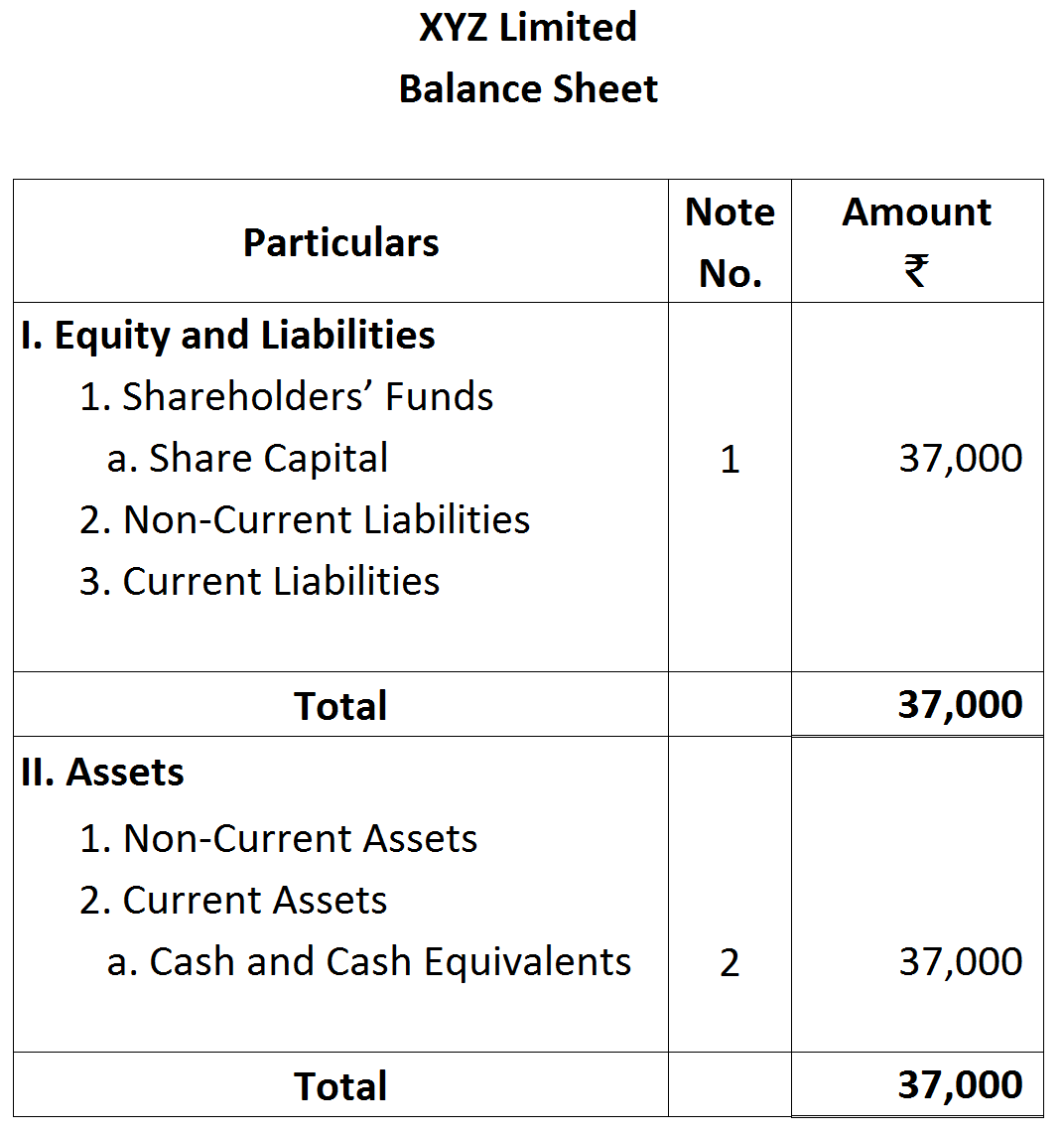

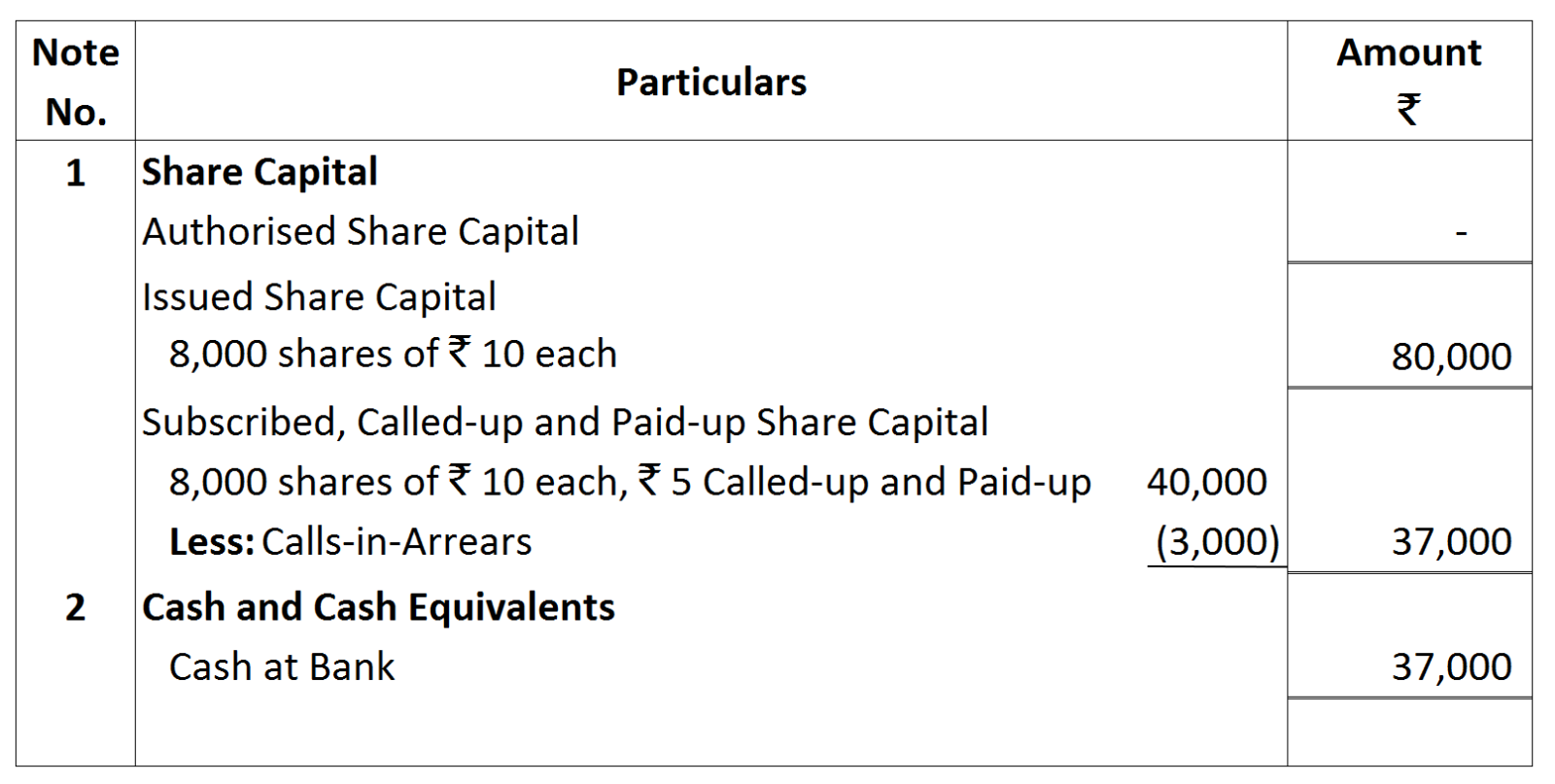

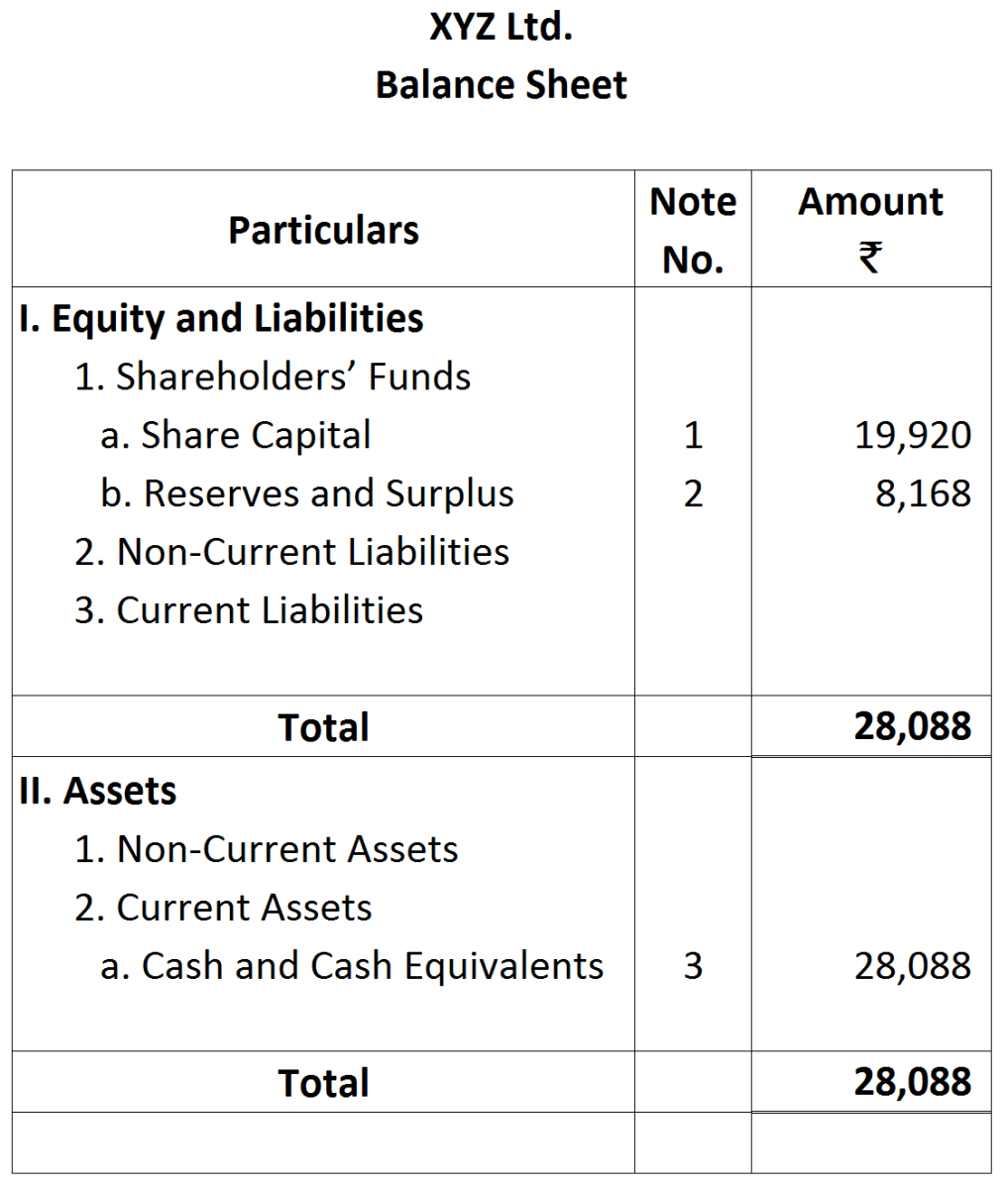

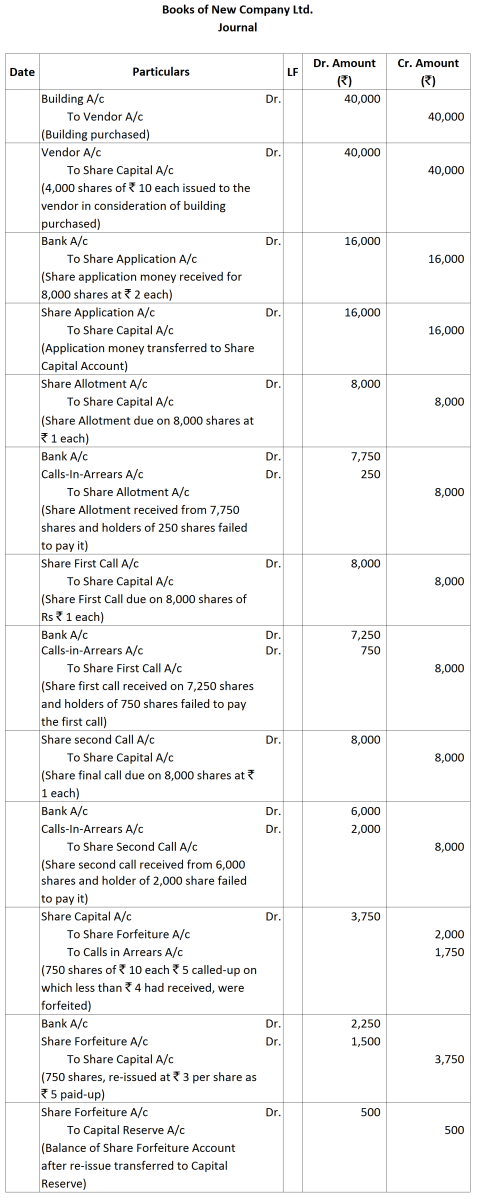

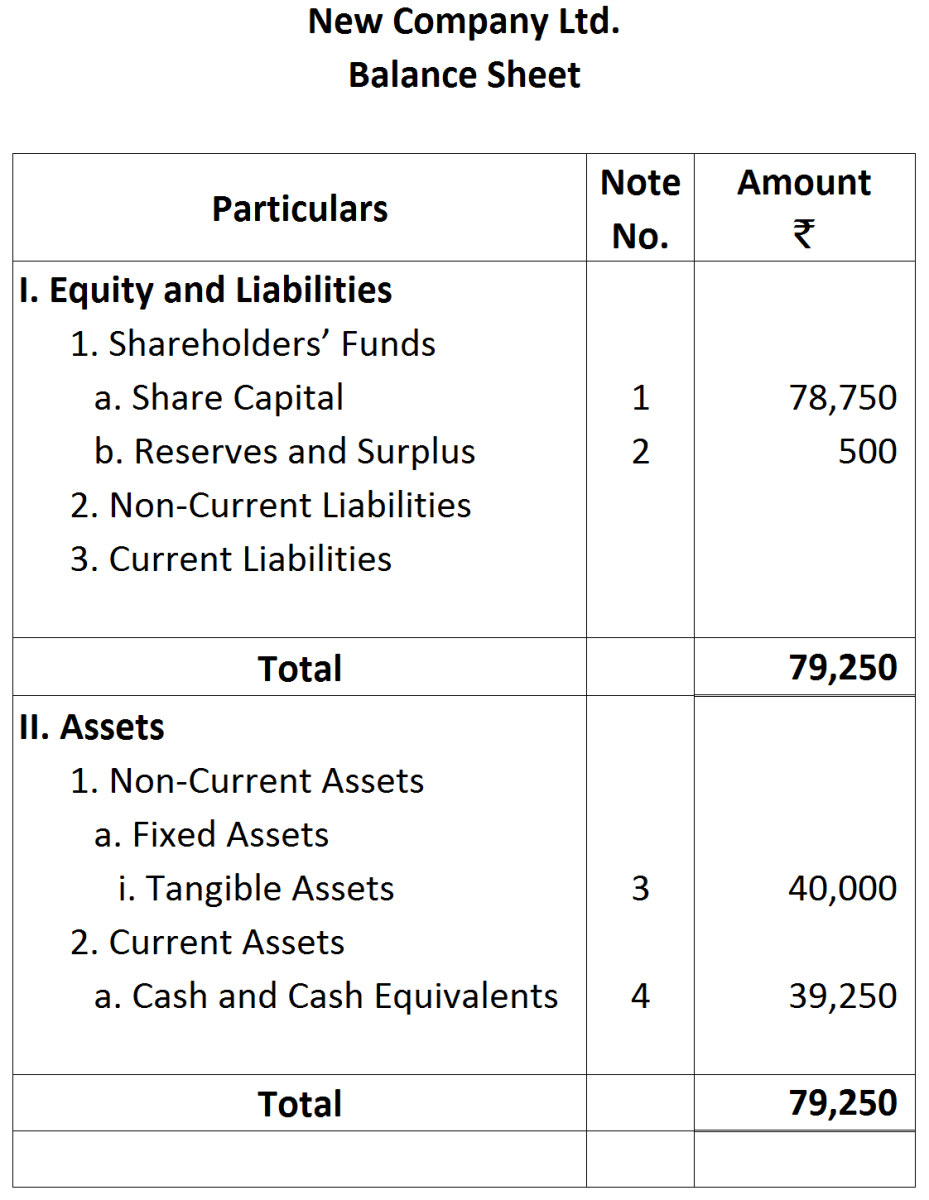

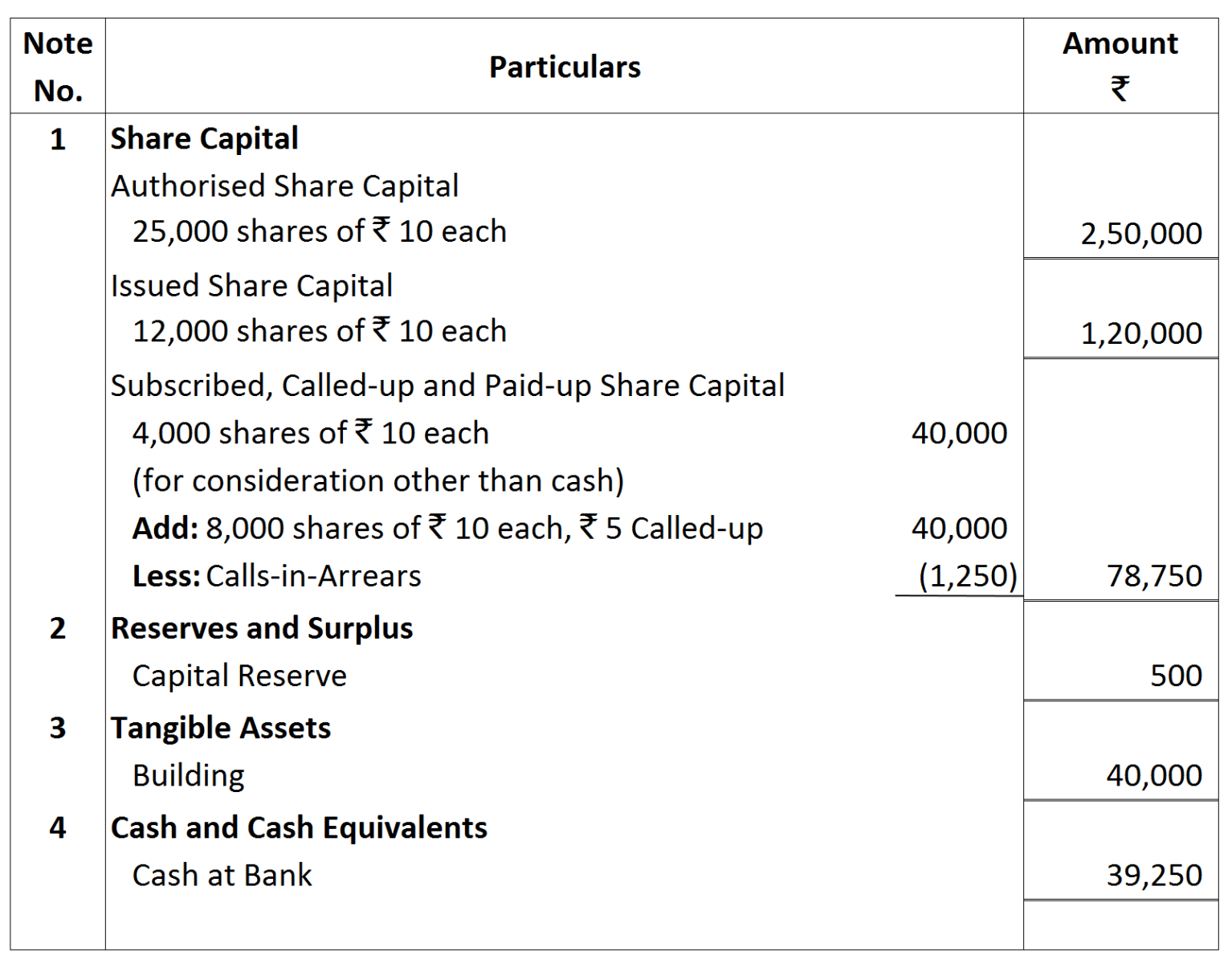

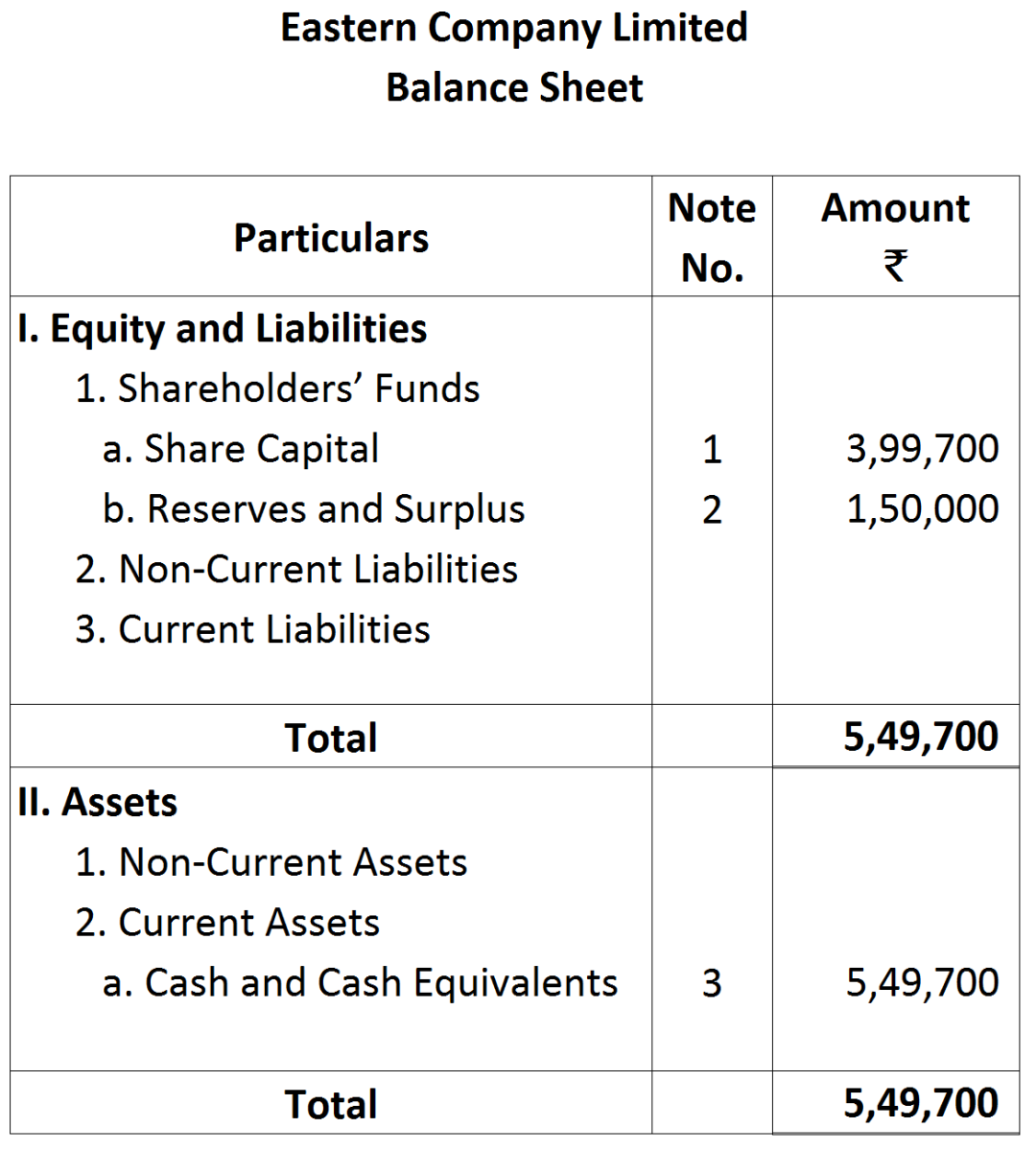

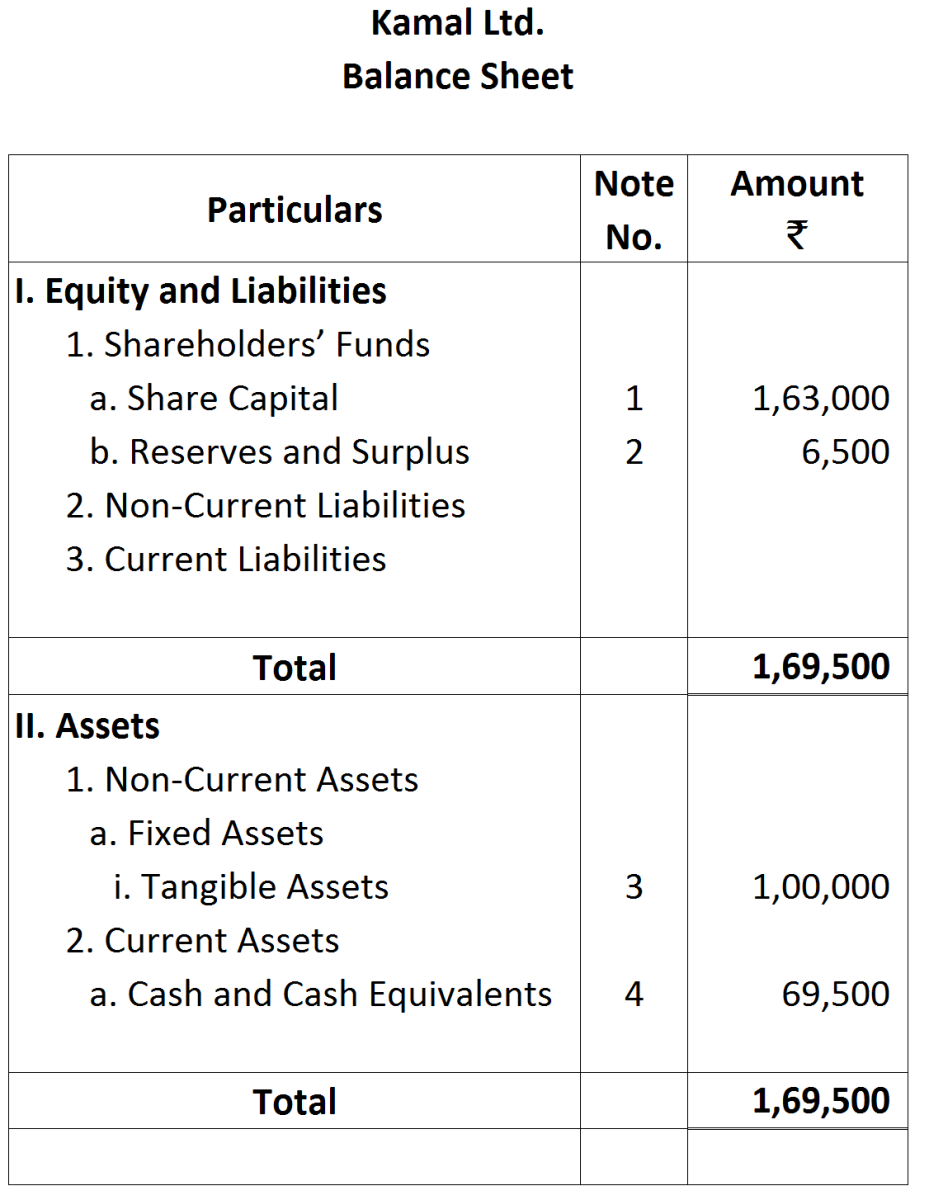

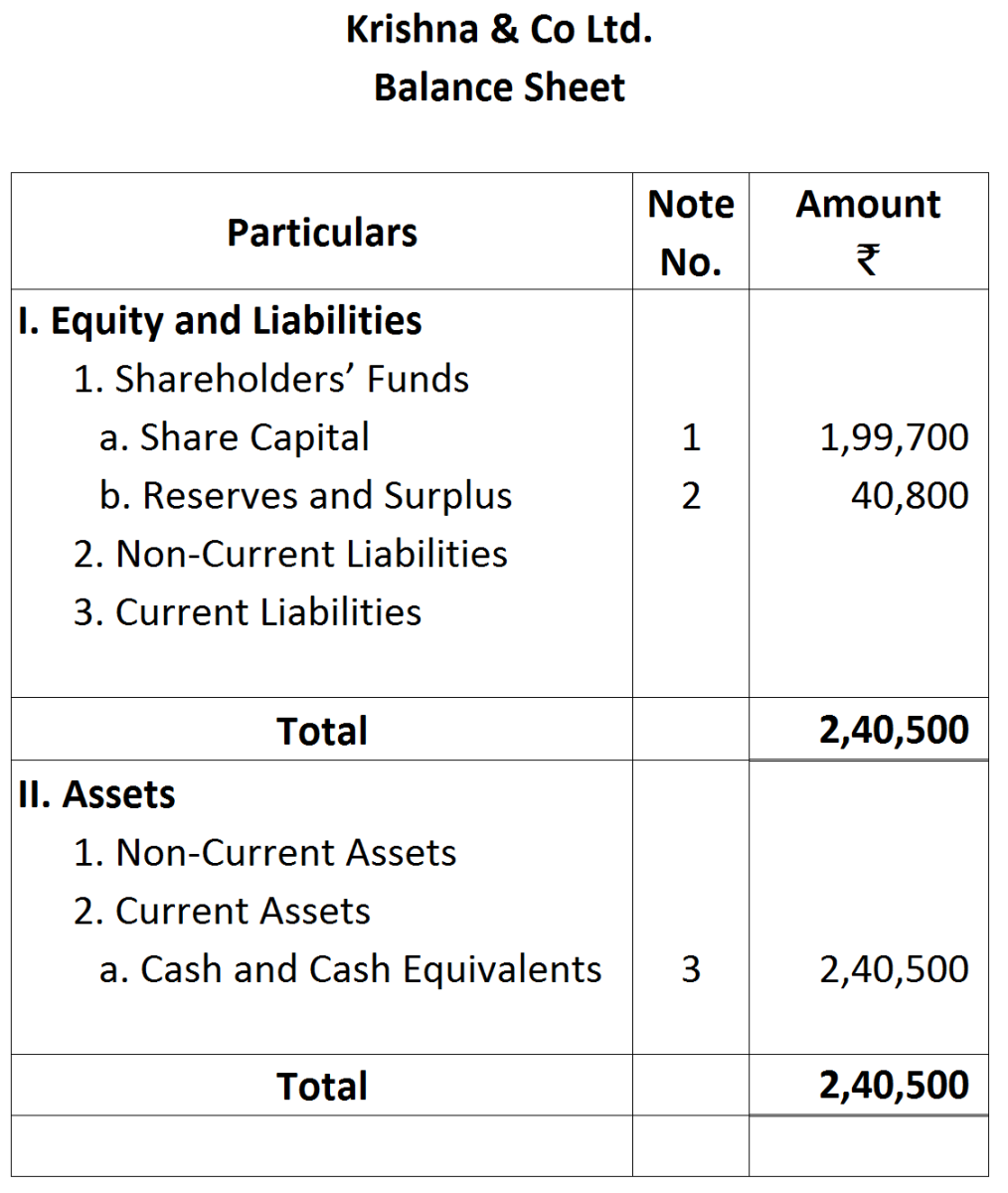

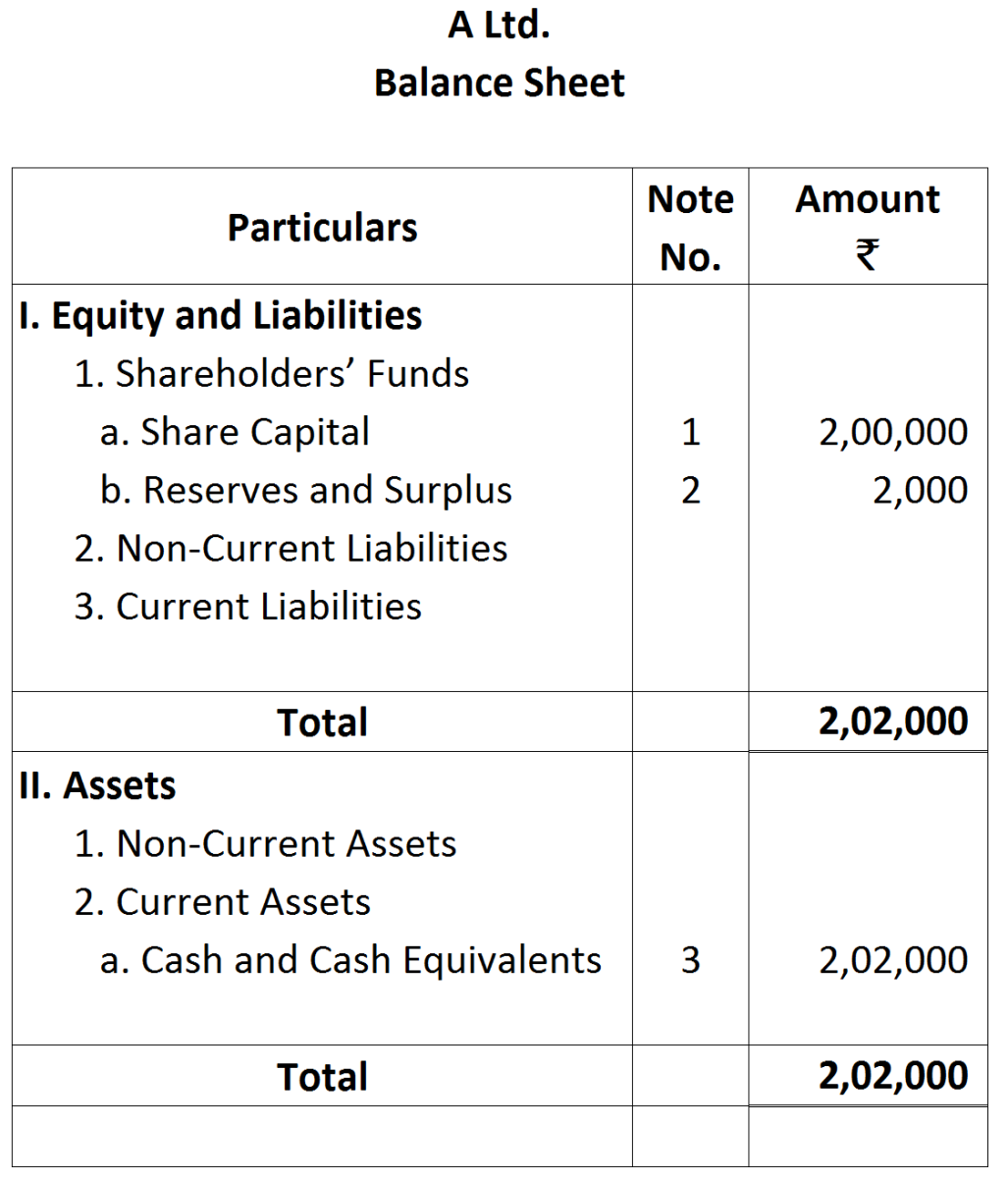

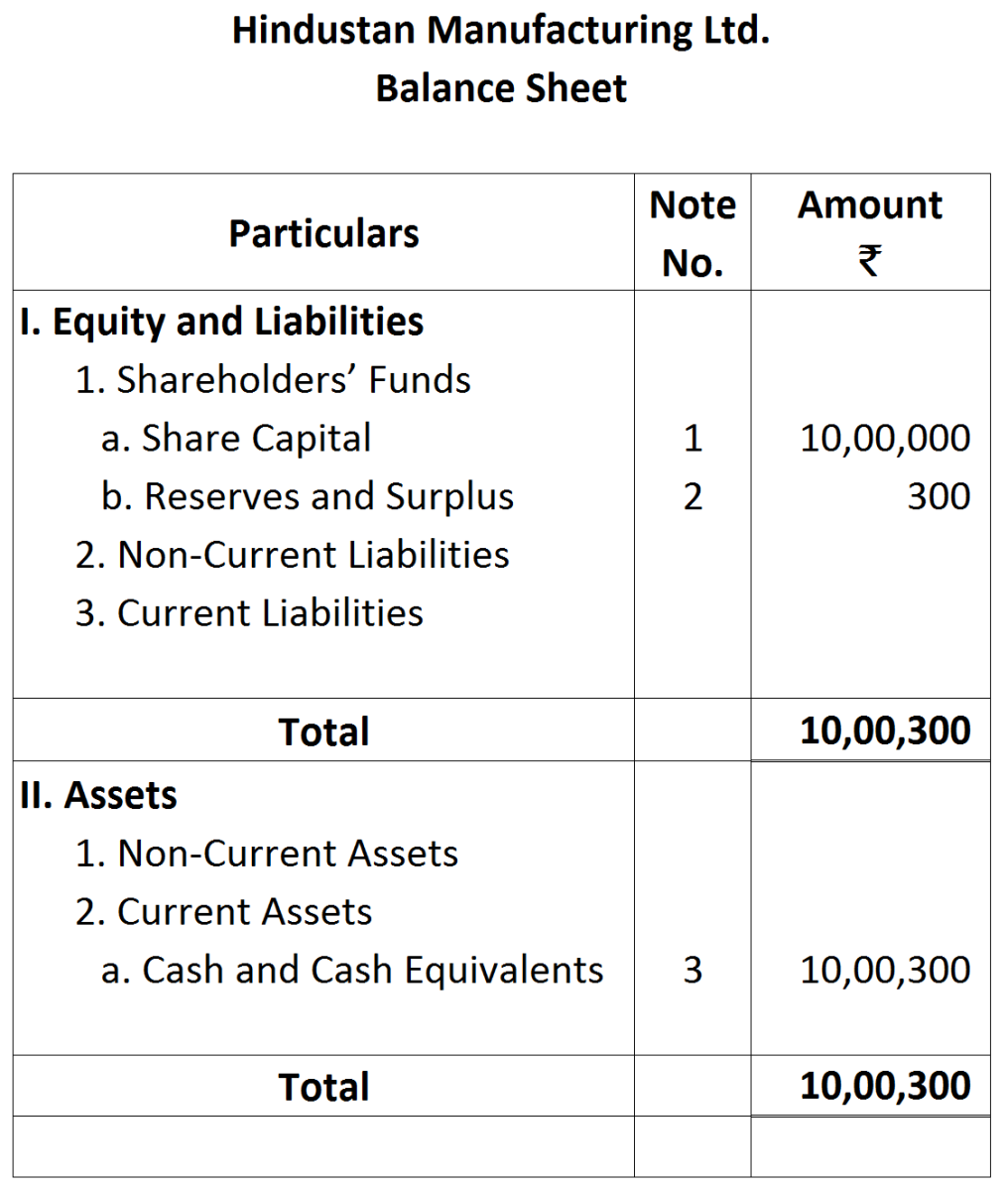

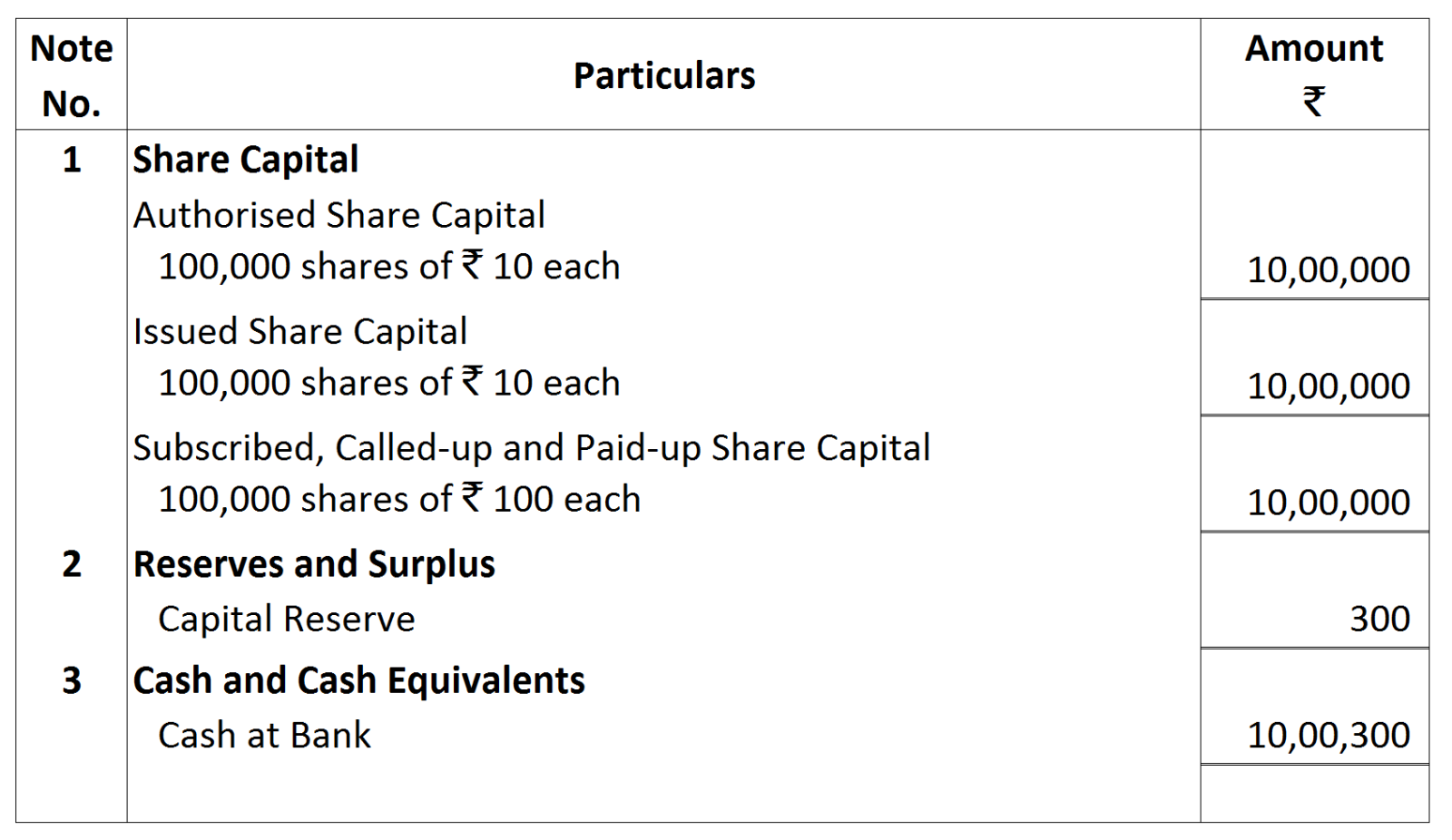

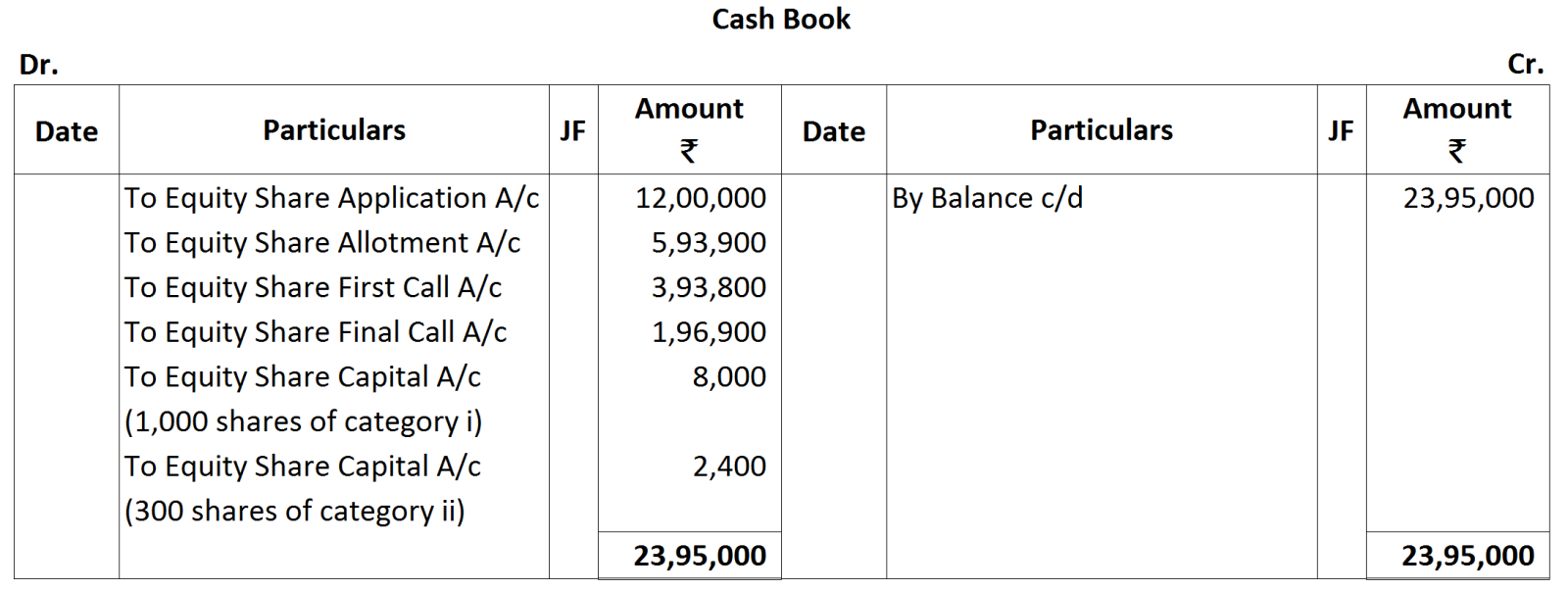

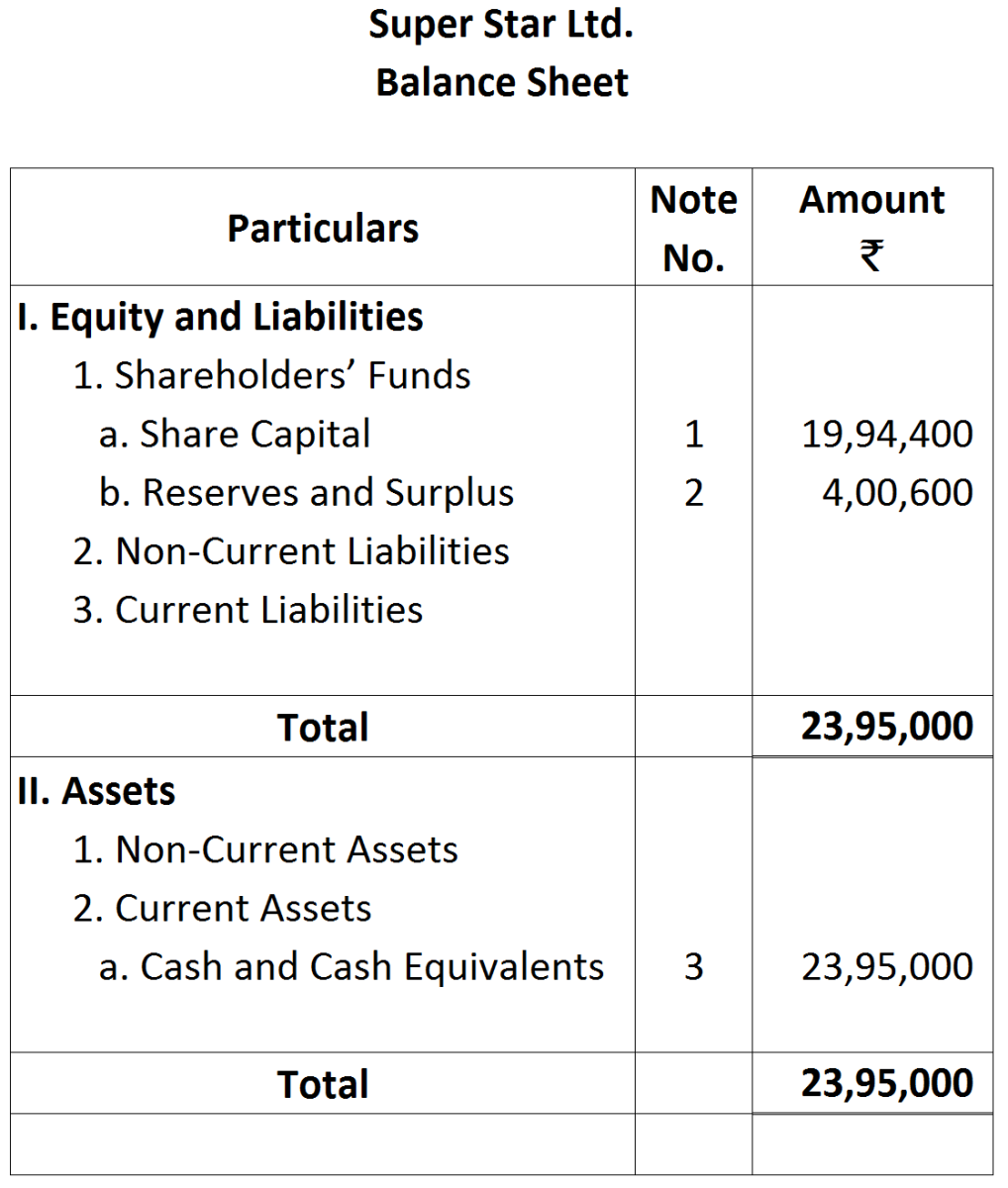

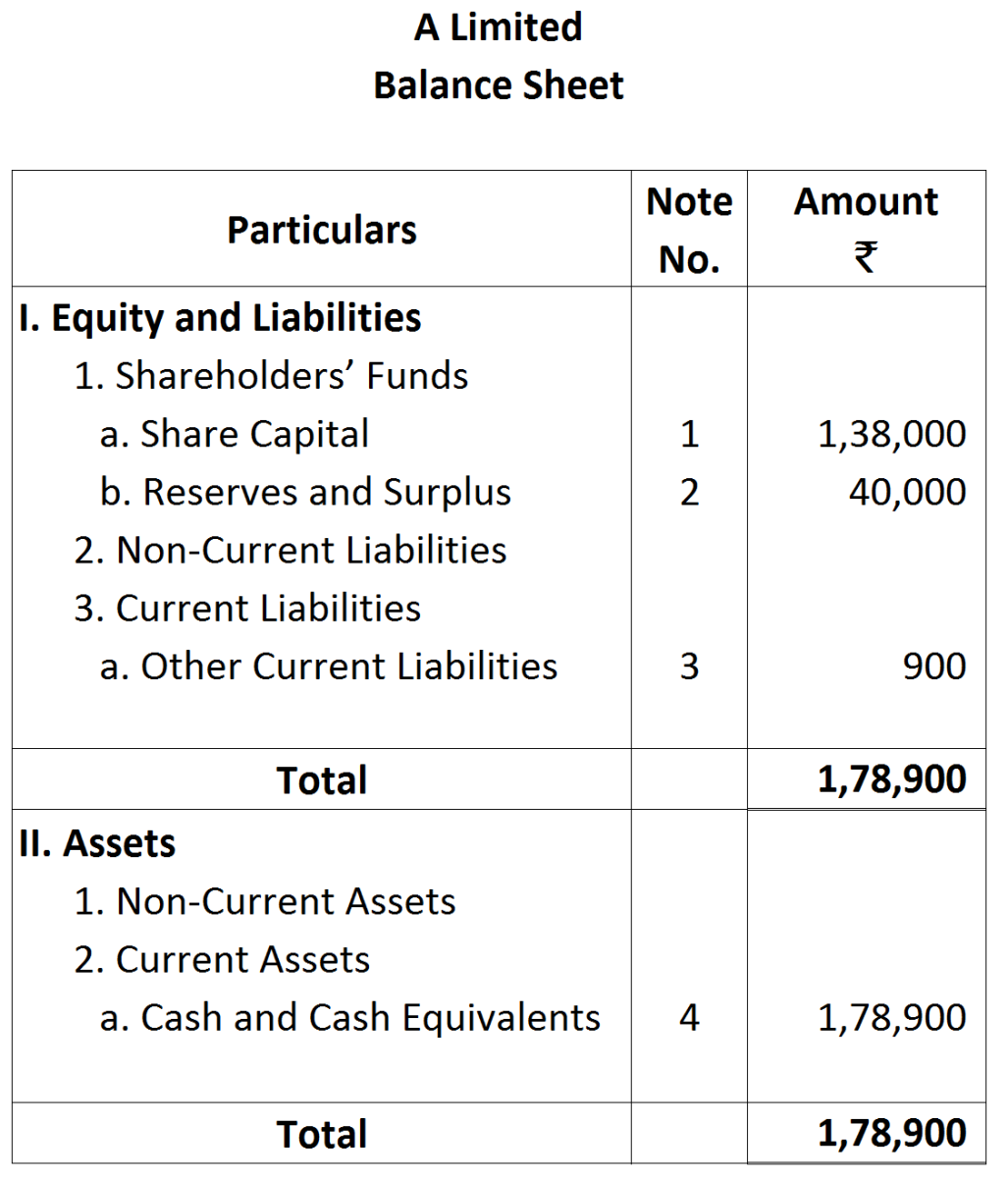

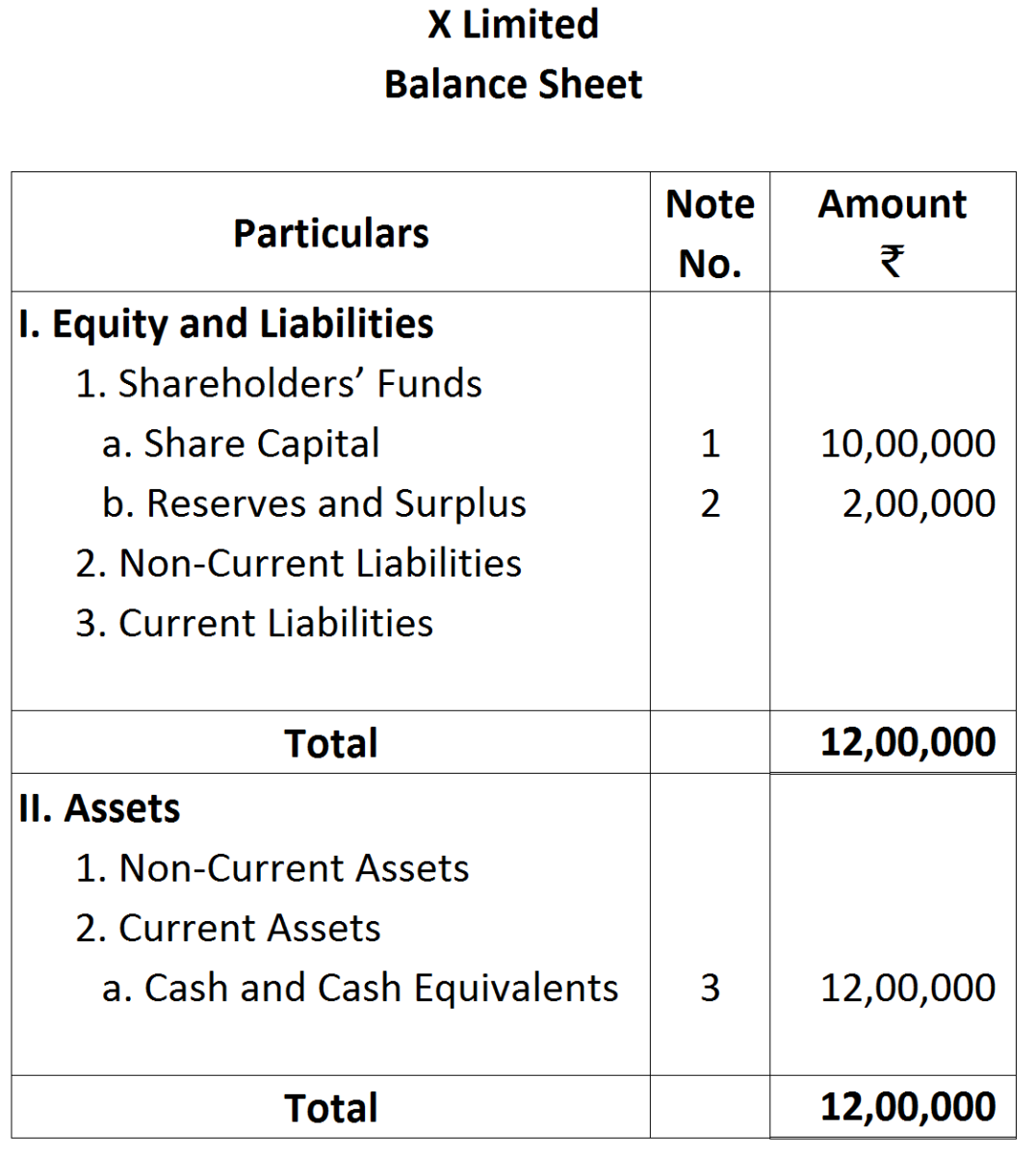

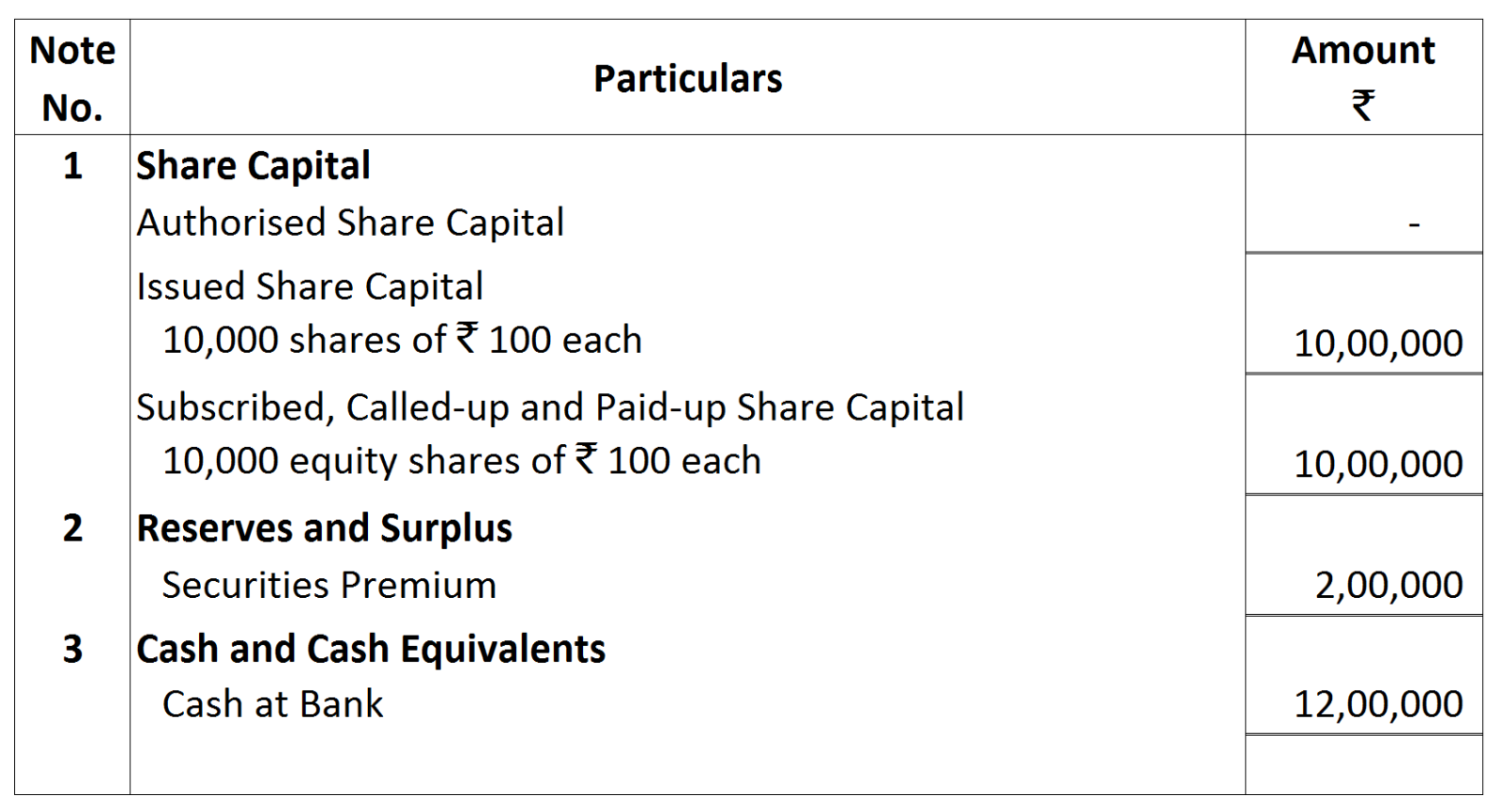

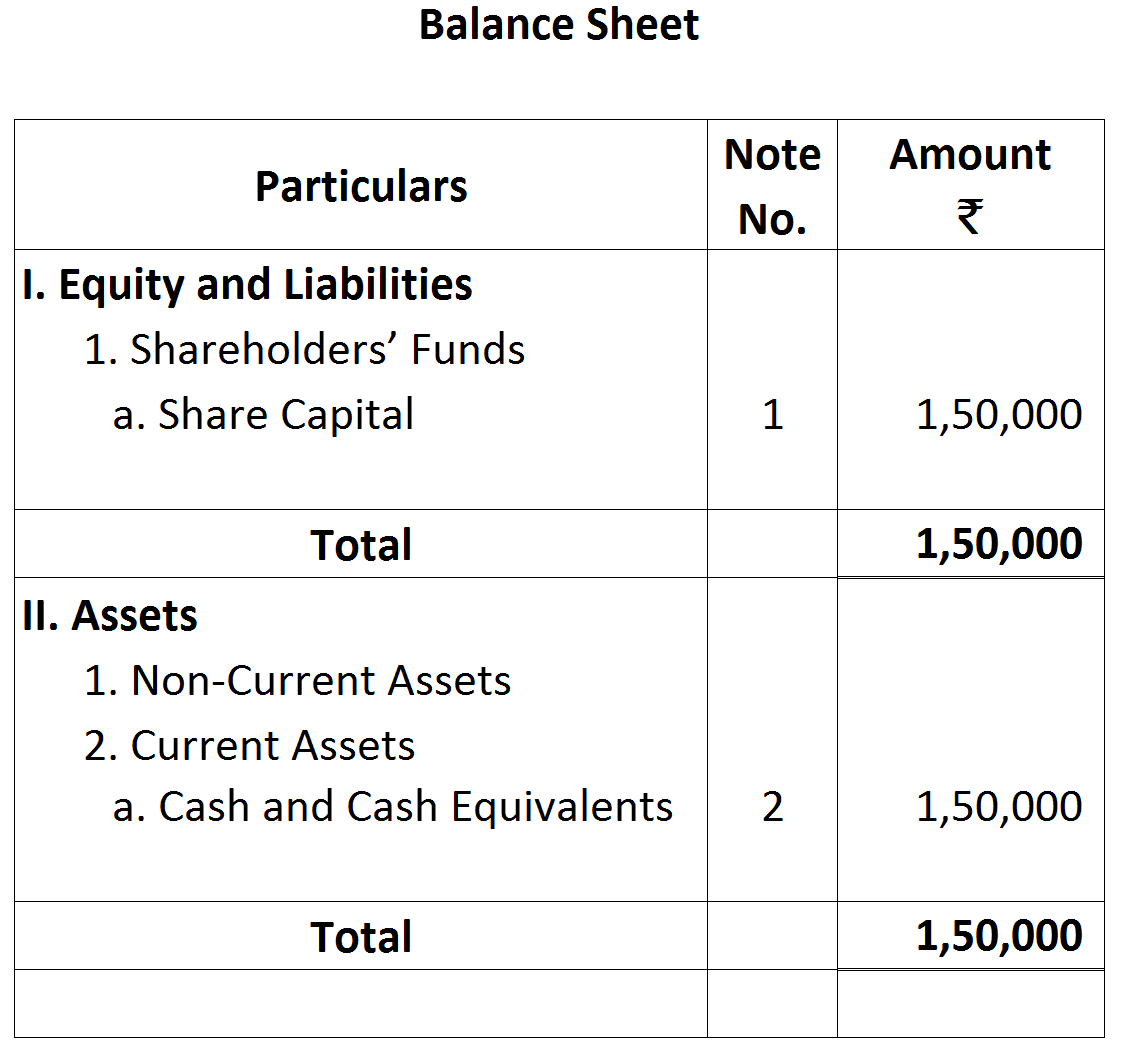

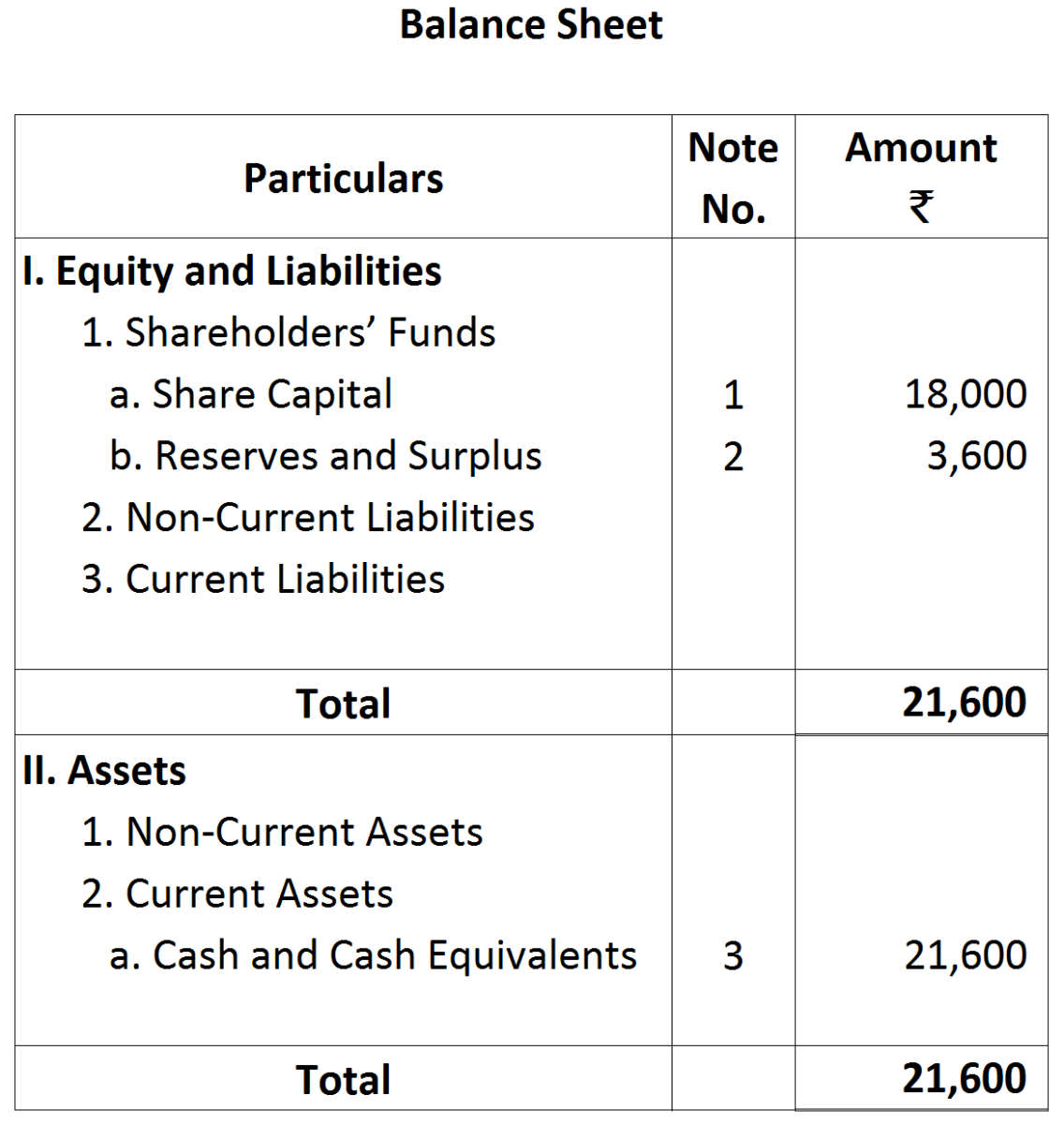

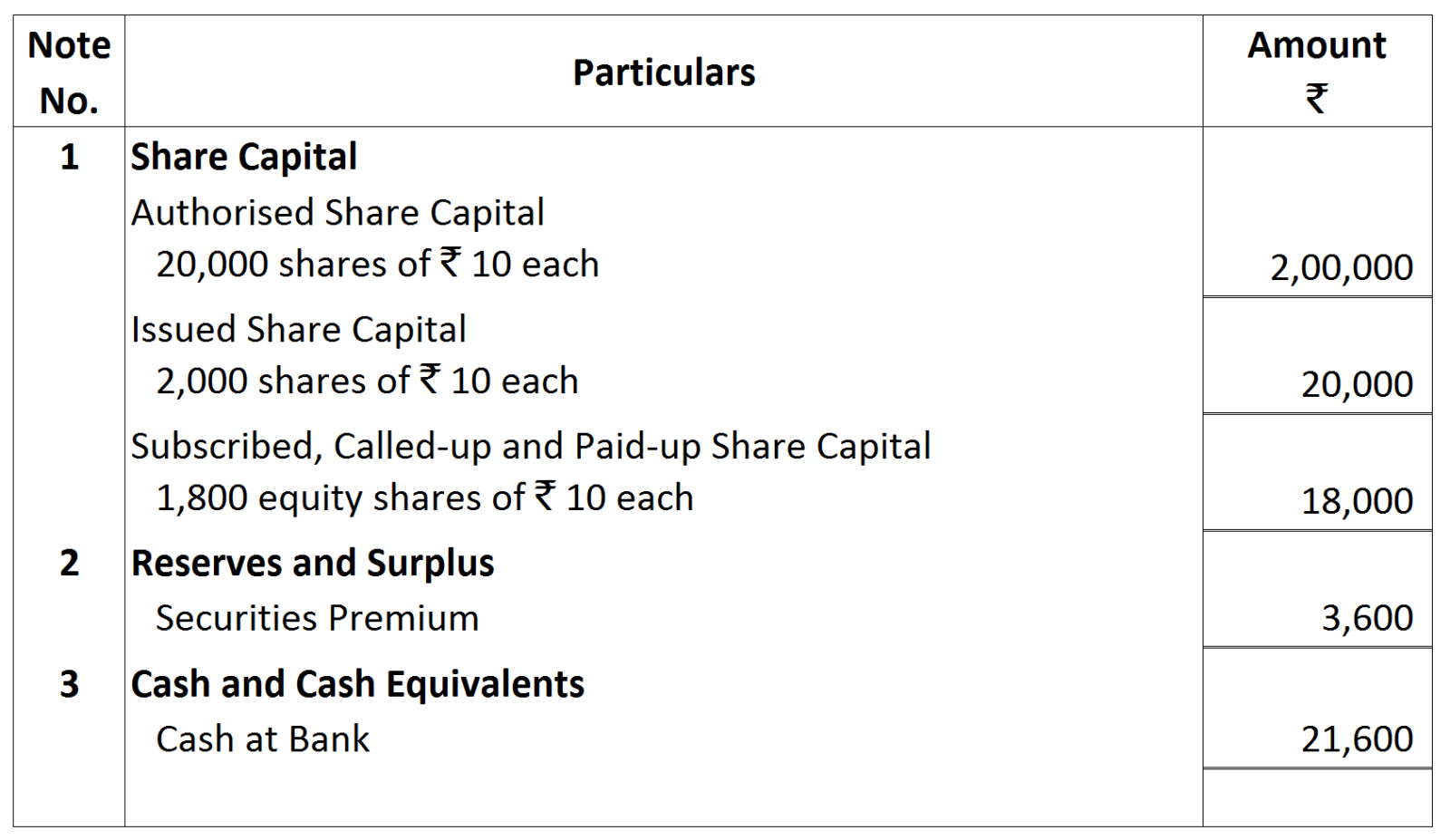

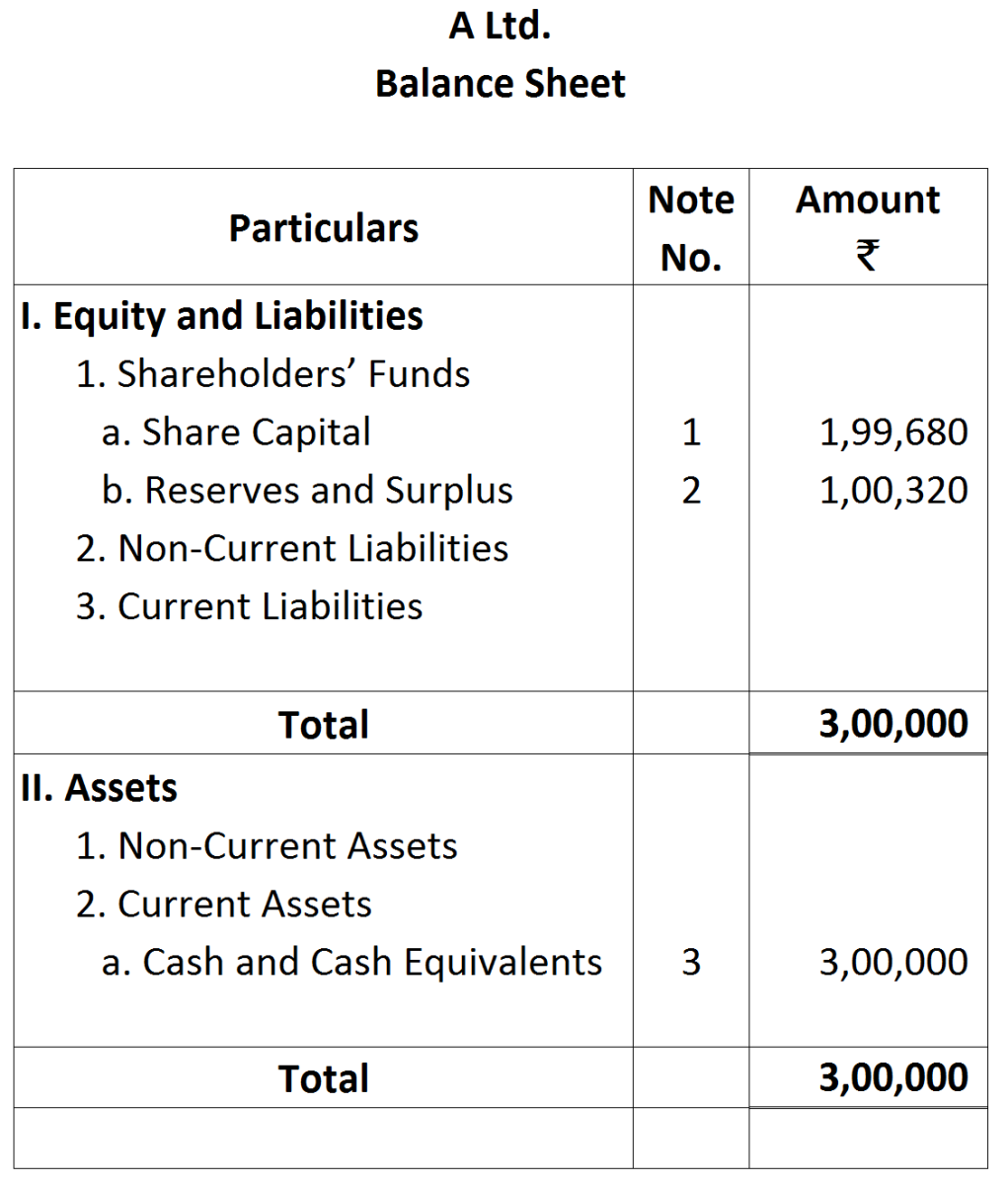

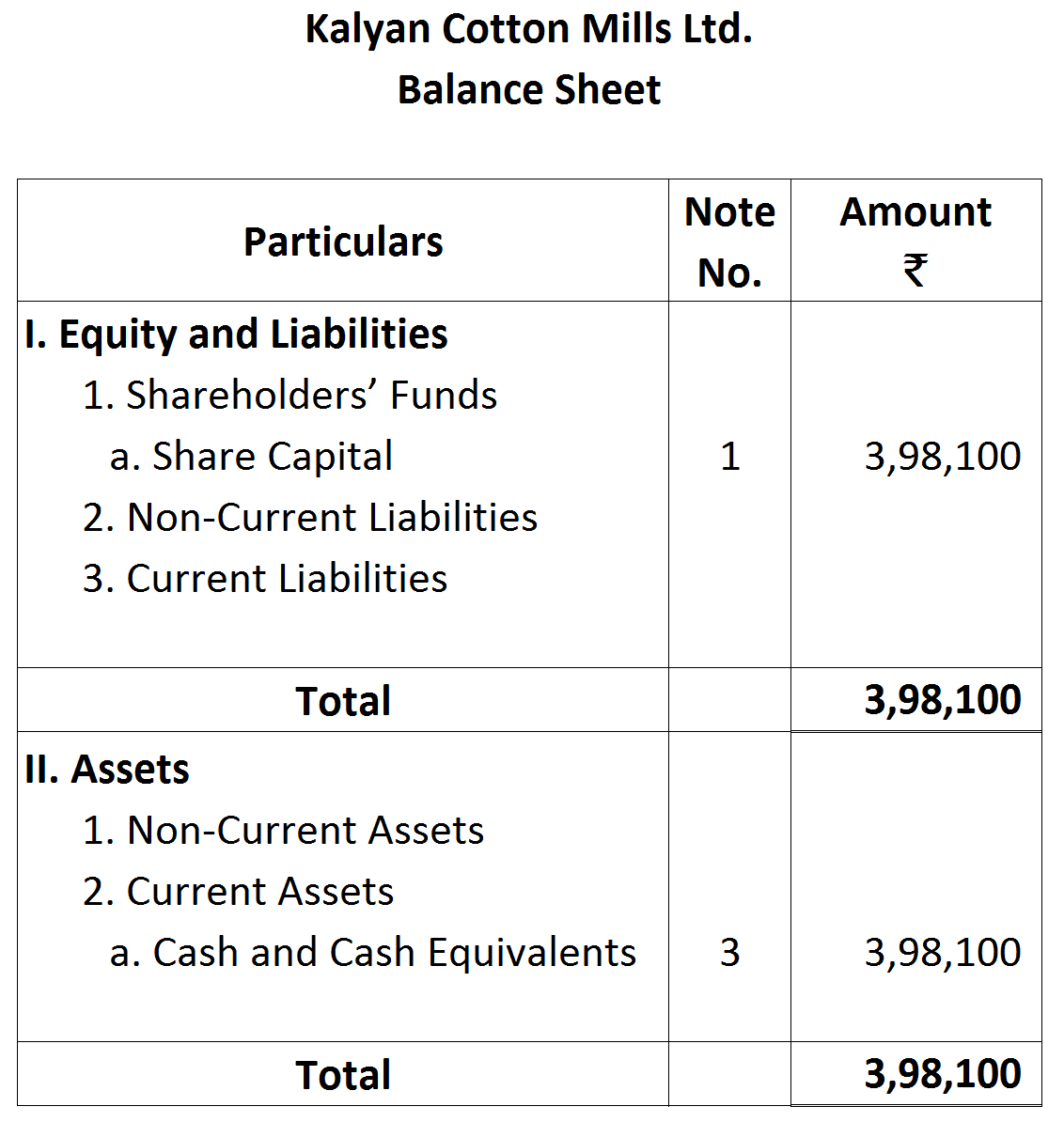

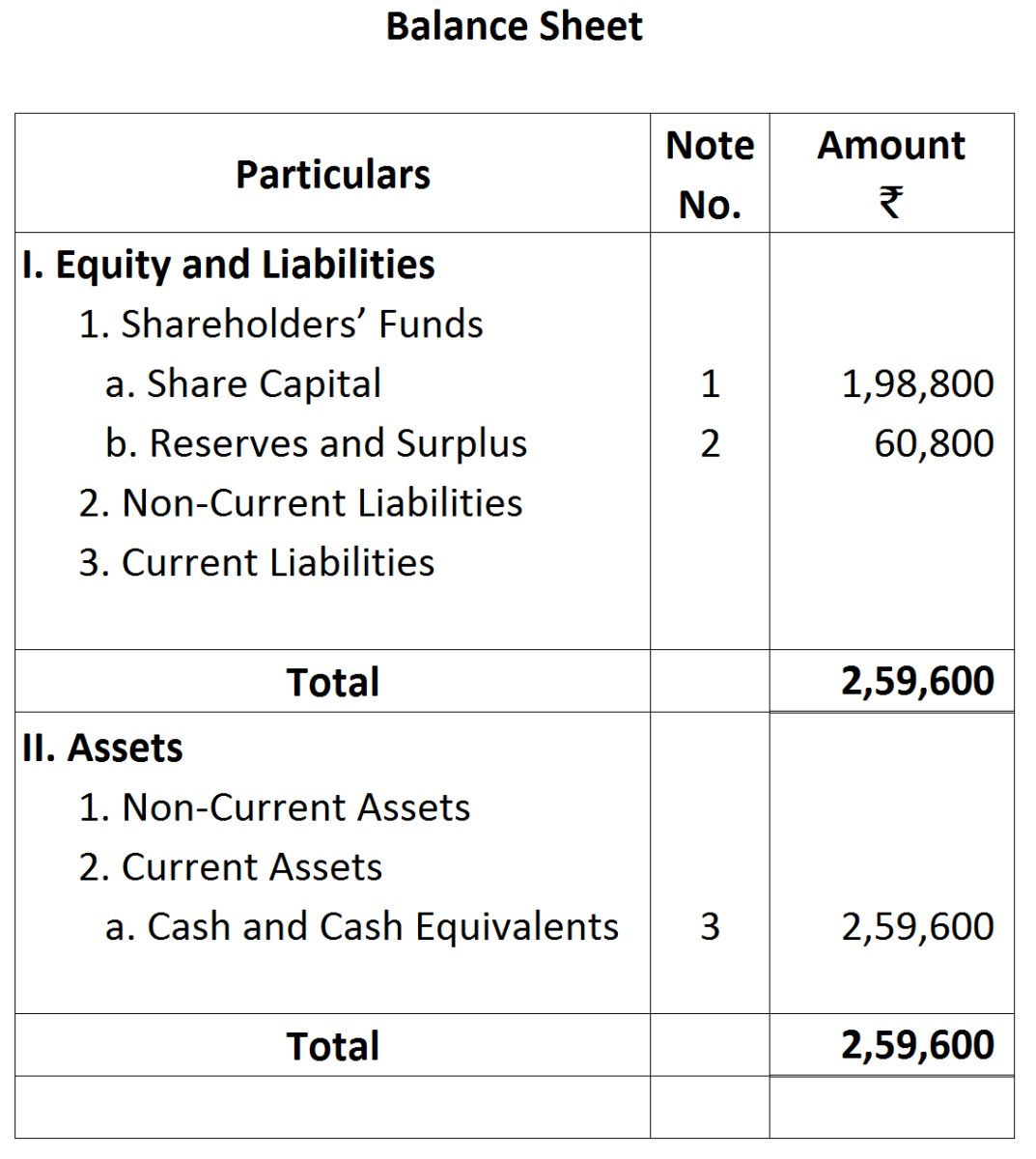

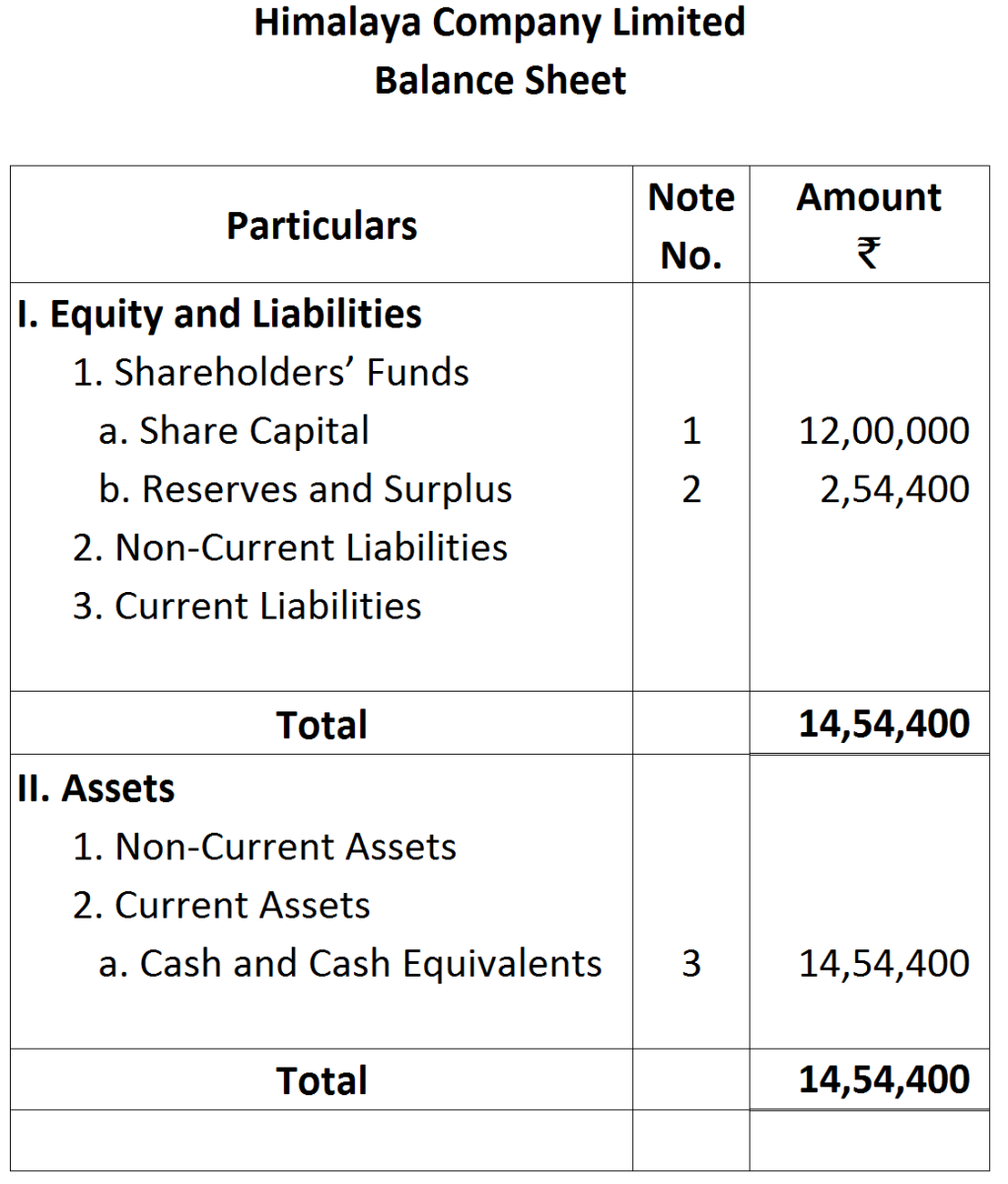

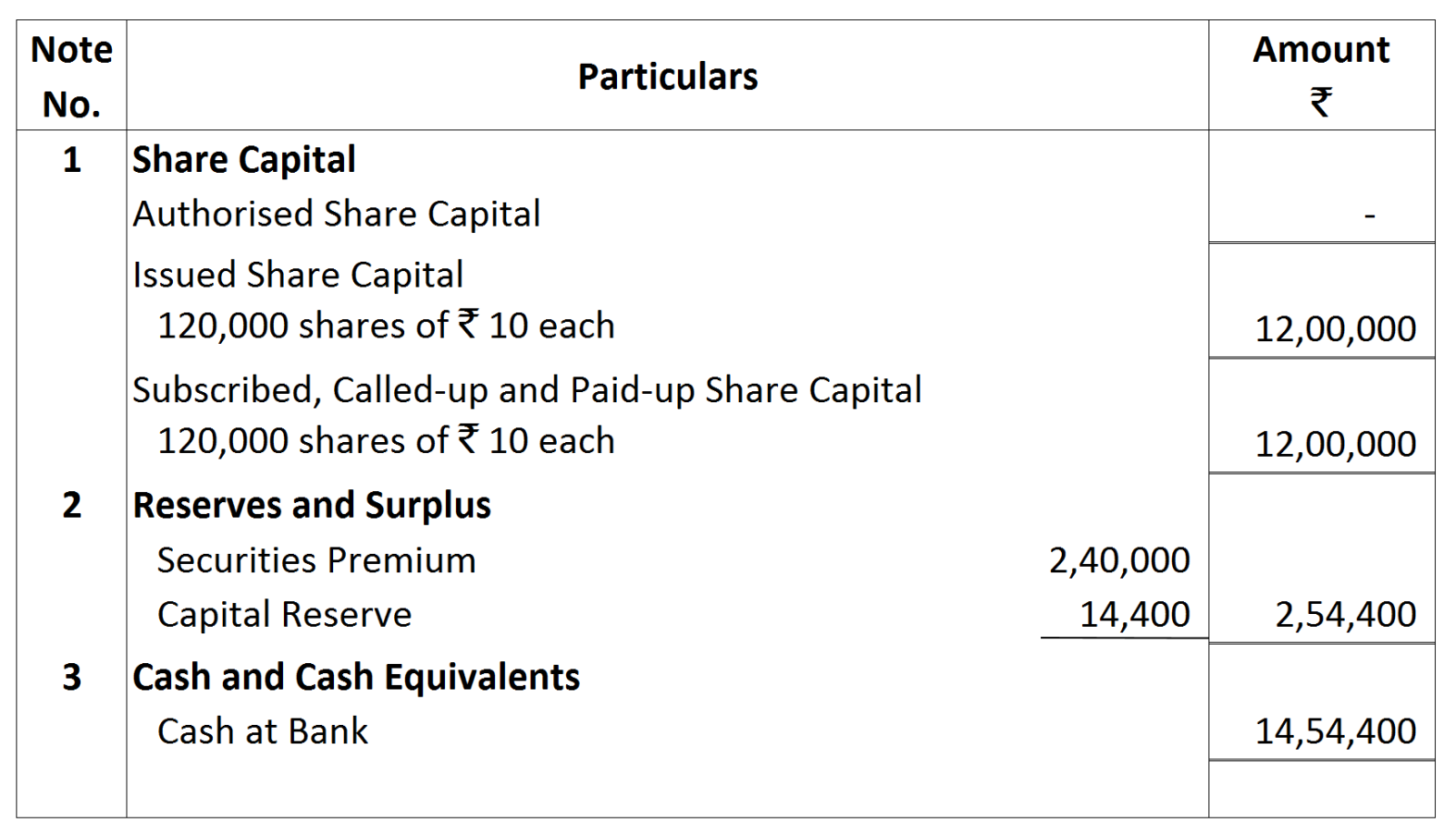

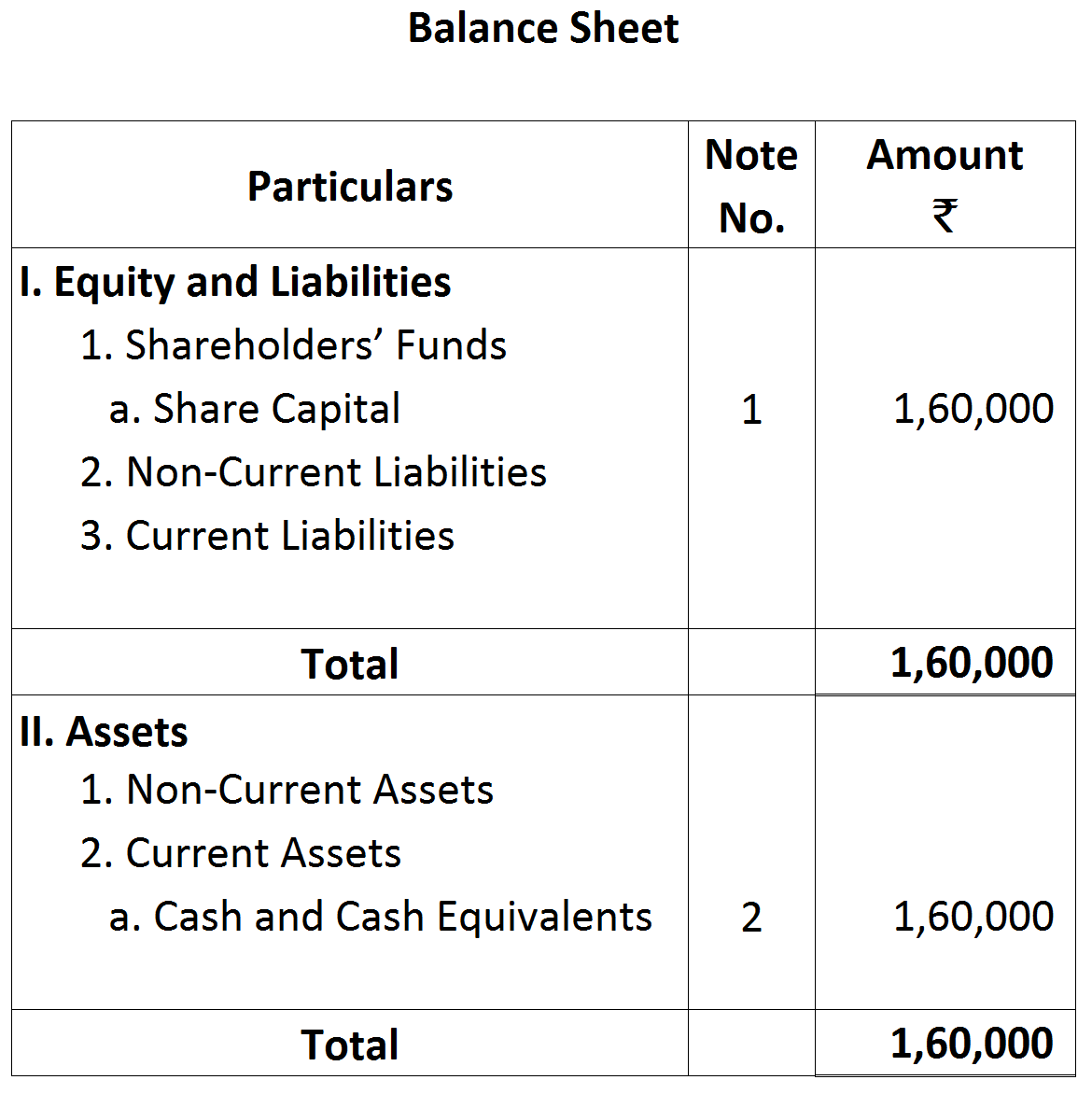

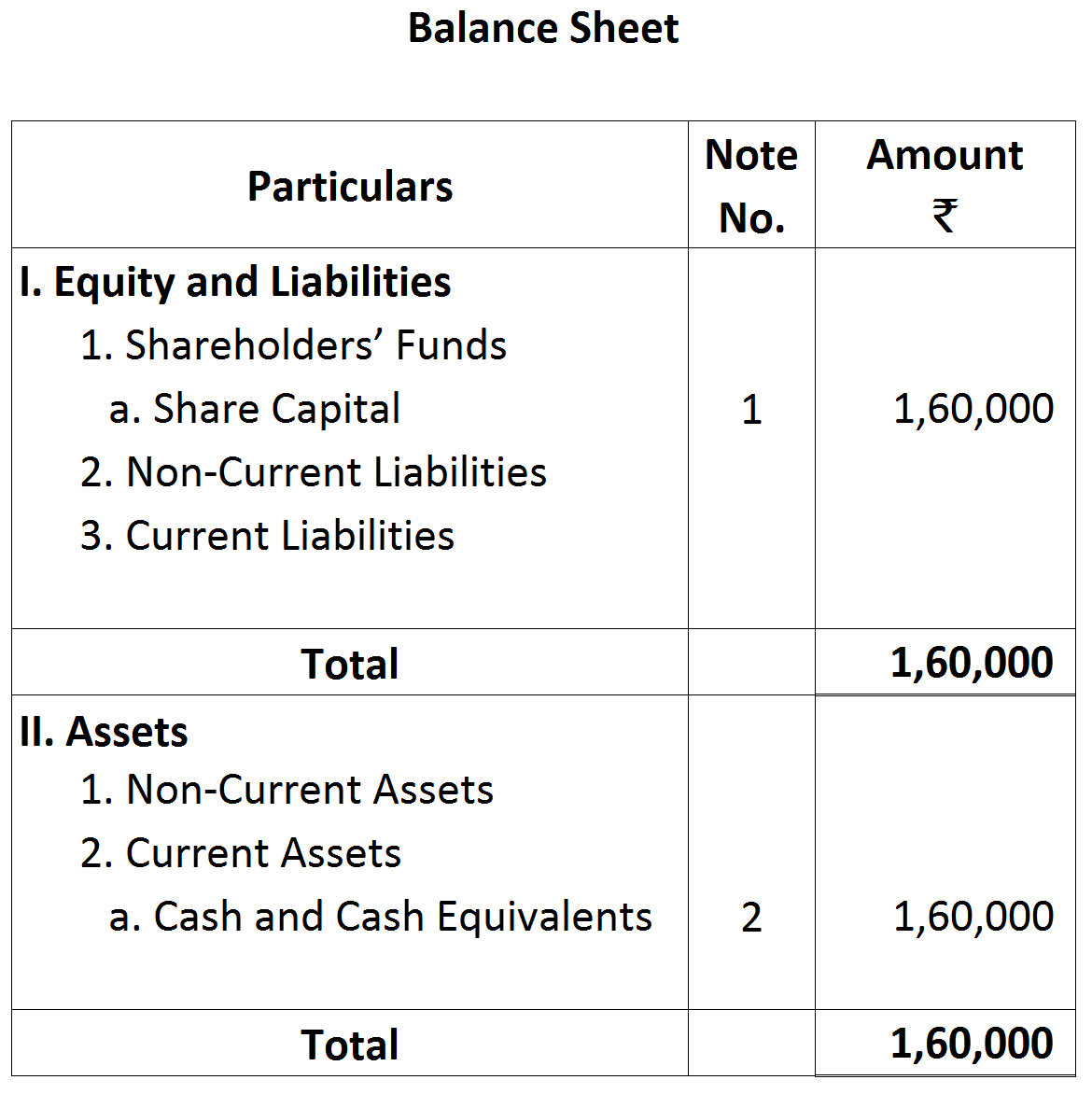

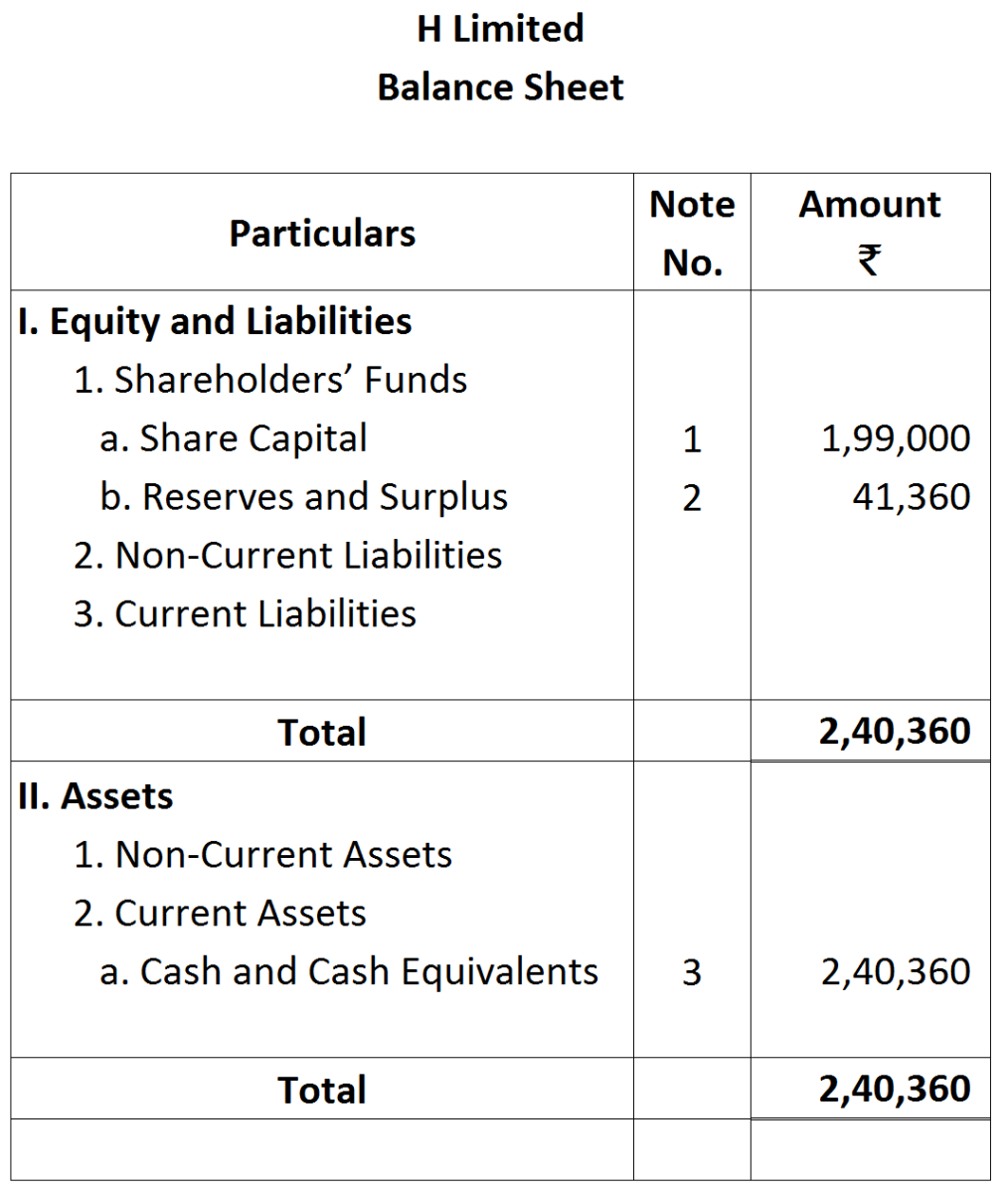

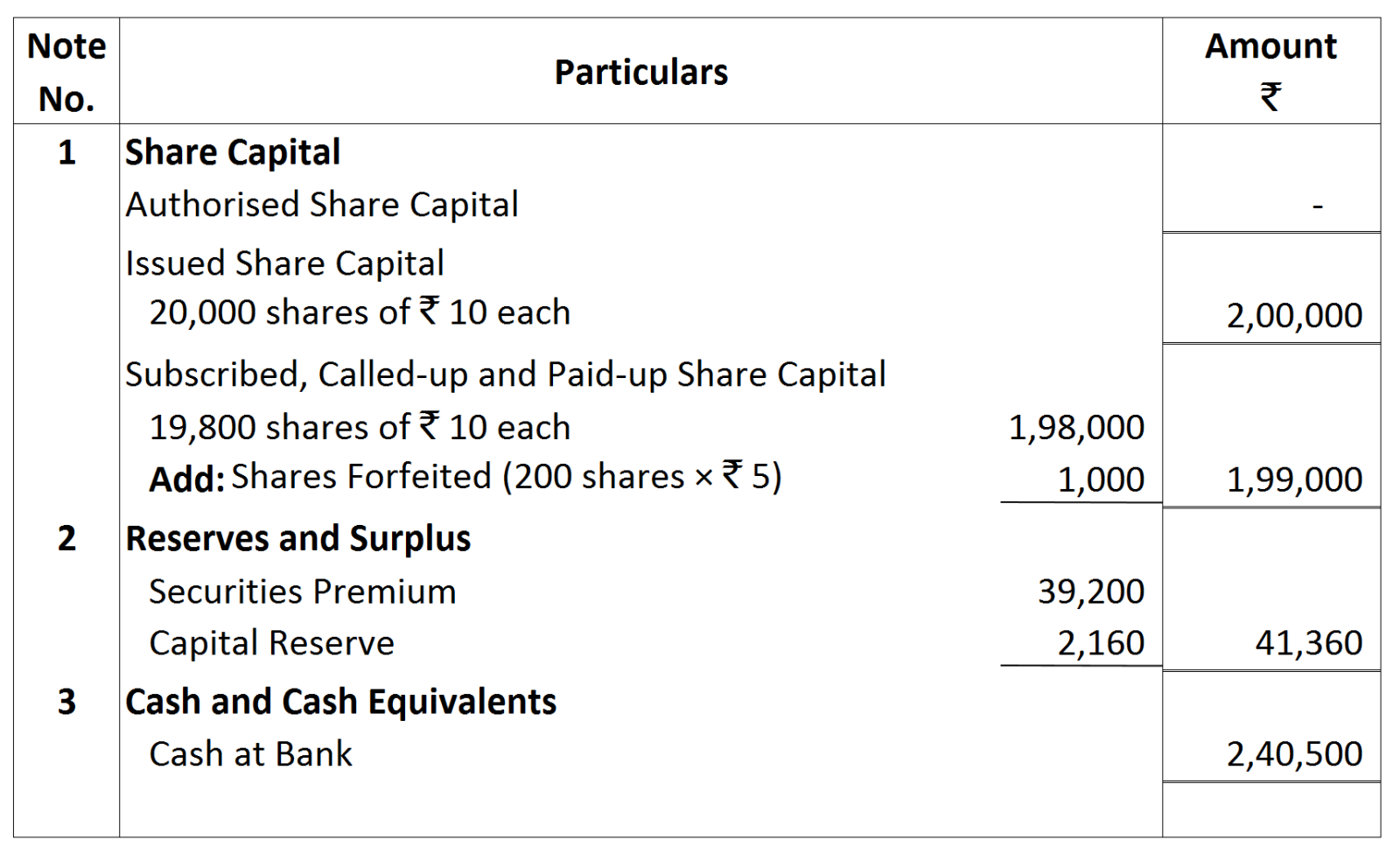

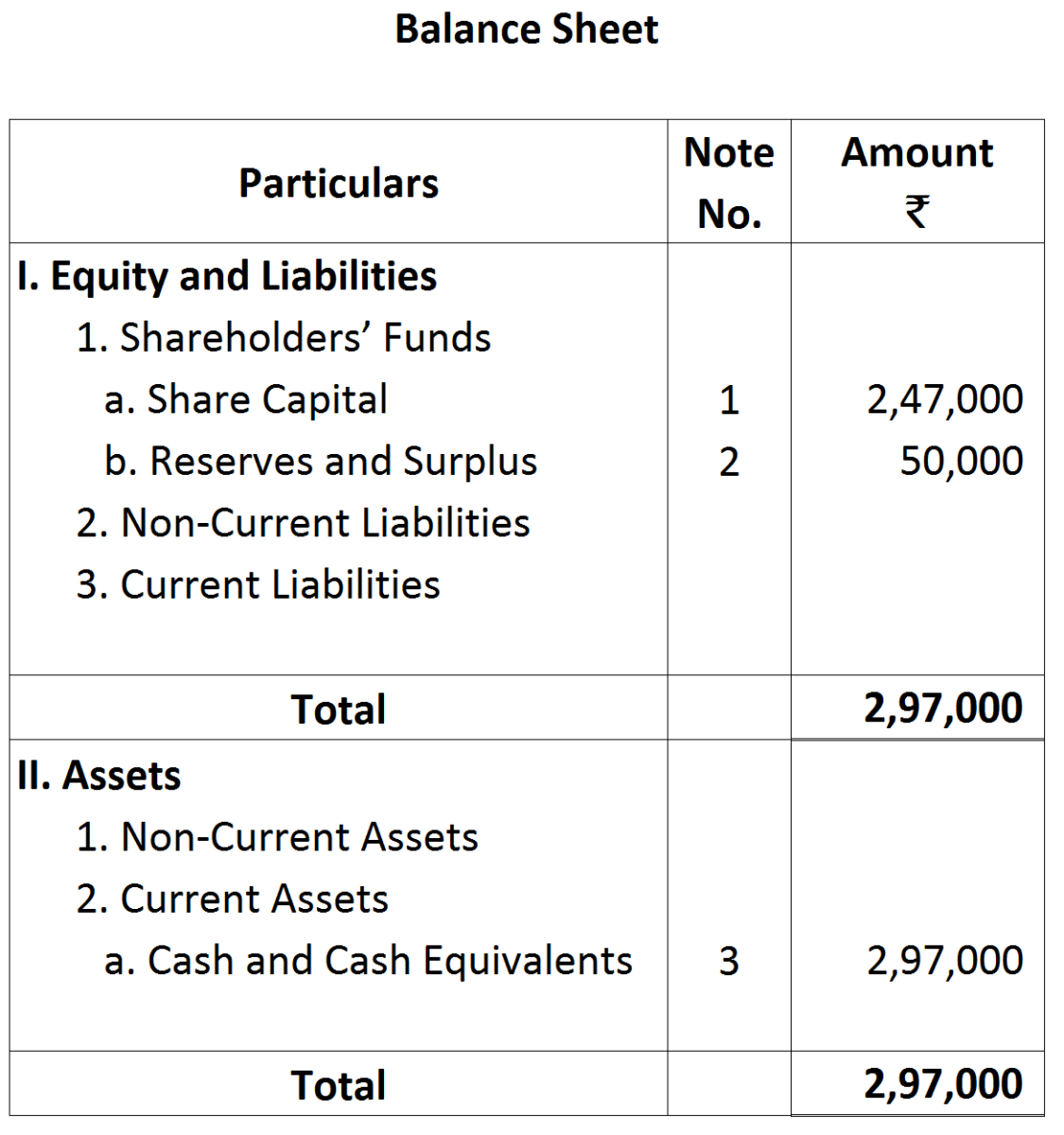

As per the Schedule III of Companies Act, 2013, the Company's Balance Sheet is presented as follows.

As per the Schedule III of Companies Act, 2013, the Company's Balance Sheet is presented as follows. NOTES TO ACCOUNTS:

NOTES TO ACCOUNTS: Working Notes:

Working Notes:

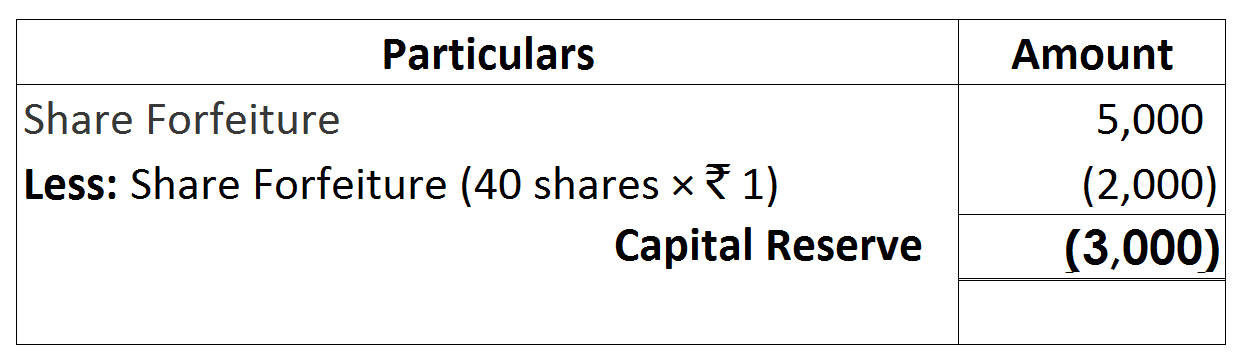

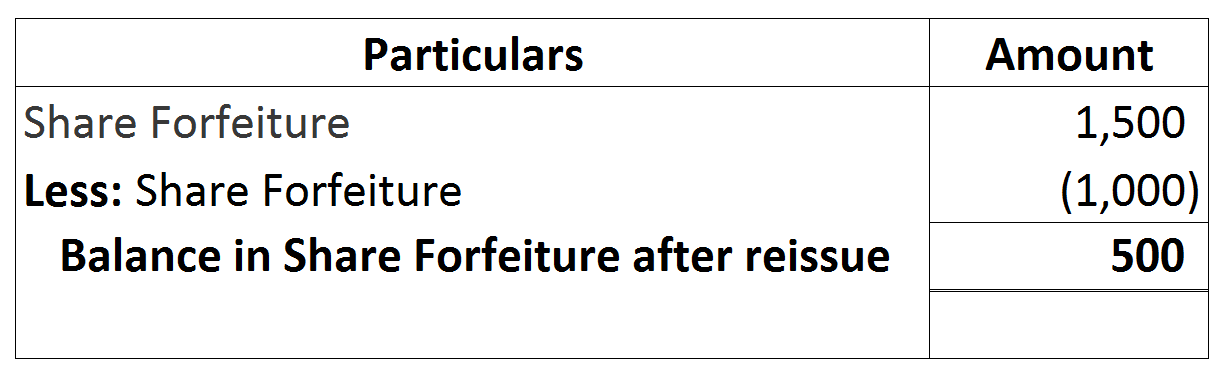

Capital Reserve:

Capital Reserve:

Notes to Account:

Notes to Account:

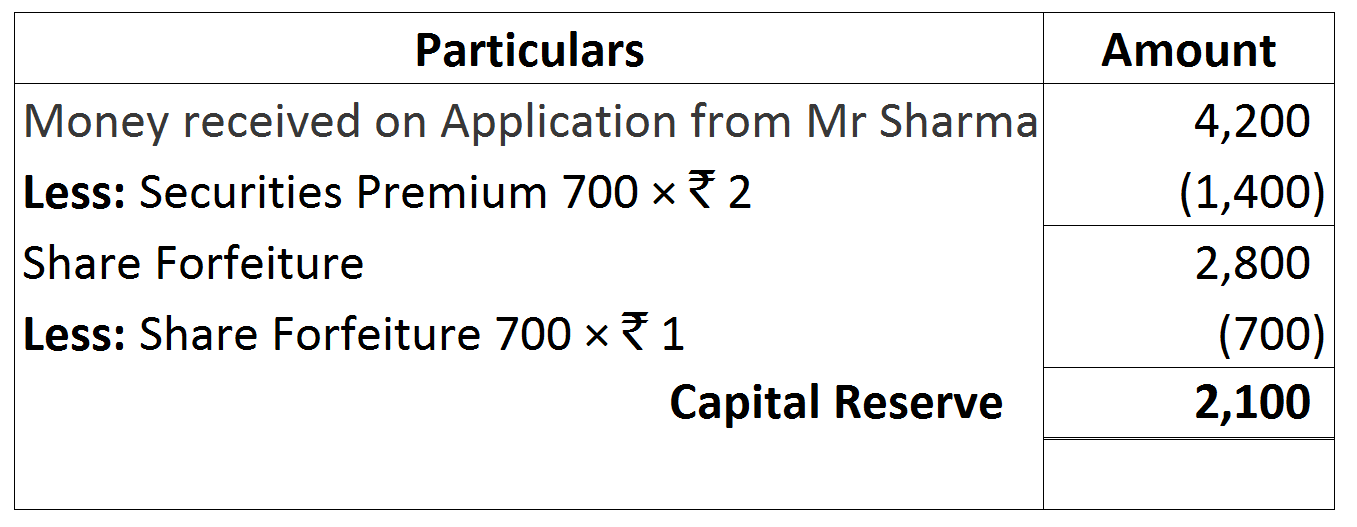

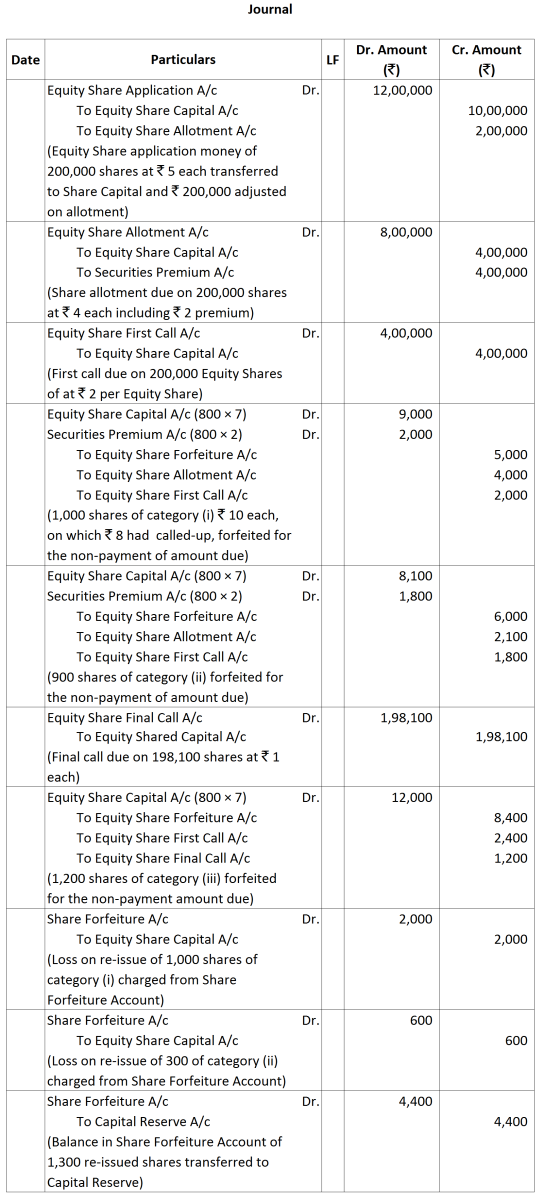

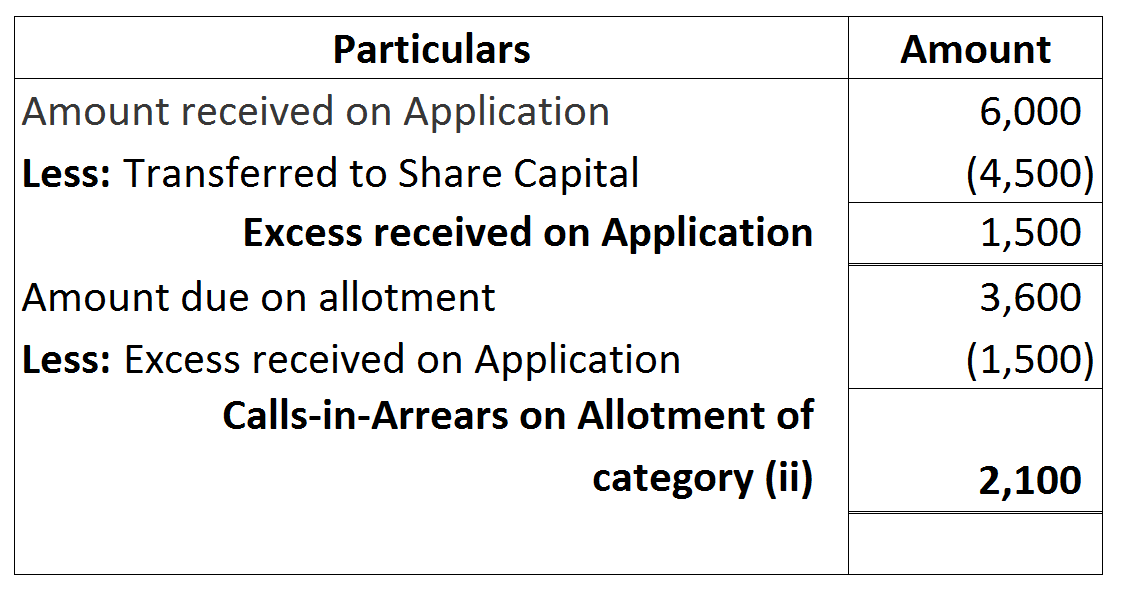

Capital Reserve Calculation of Share Forfeiture of 1,000 shares of category (i)

Capital Reserve Calculation of Share Forfeiture of 1,000 shares of category (i)

NOTES TO ACCOUNTS:

NOTES TO ACCOUNTS:

Working Notes:

Working Notes:

Working Notes:

Working Notes:

Notes to Account:

Notes to Account: Working Note:

Working Note:

Capital Reserve: Ramesh,

Capital Reserve: Ramesh,

Notes to Account:

Notes to Account: Working Notes:

Working Notes:

Notes of Account:

Notes of Account:

Working Notes:

Working Notes:

Working Notes:

Working Notes:

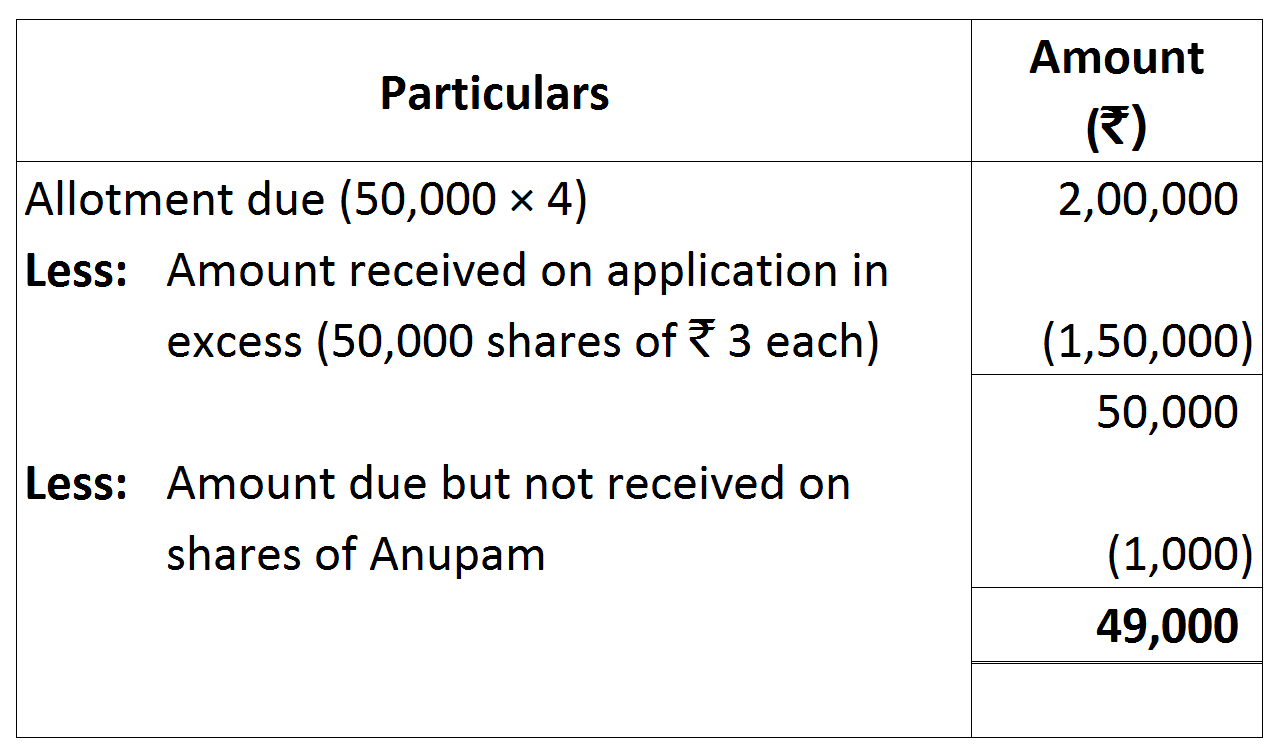

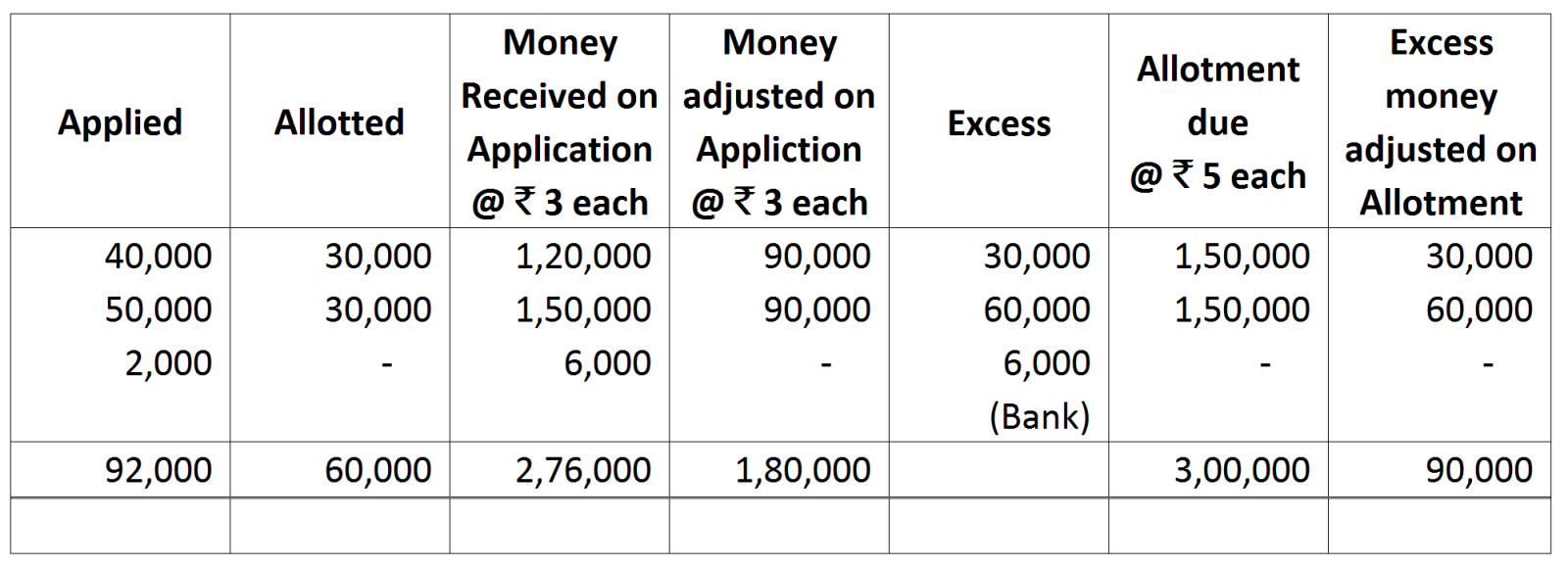

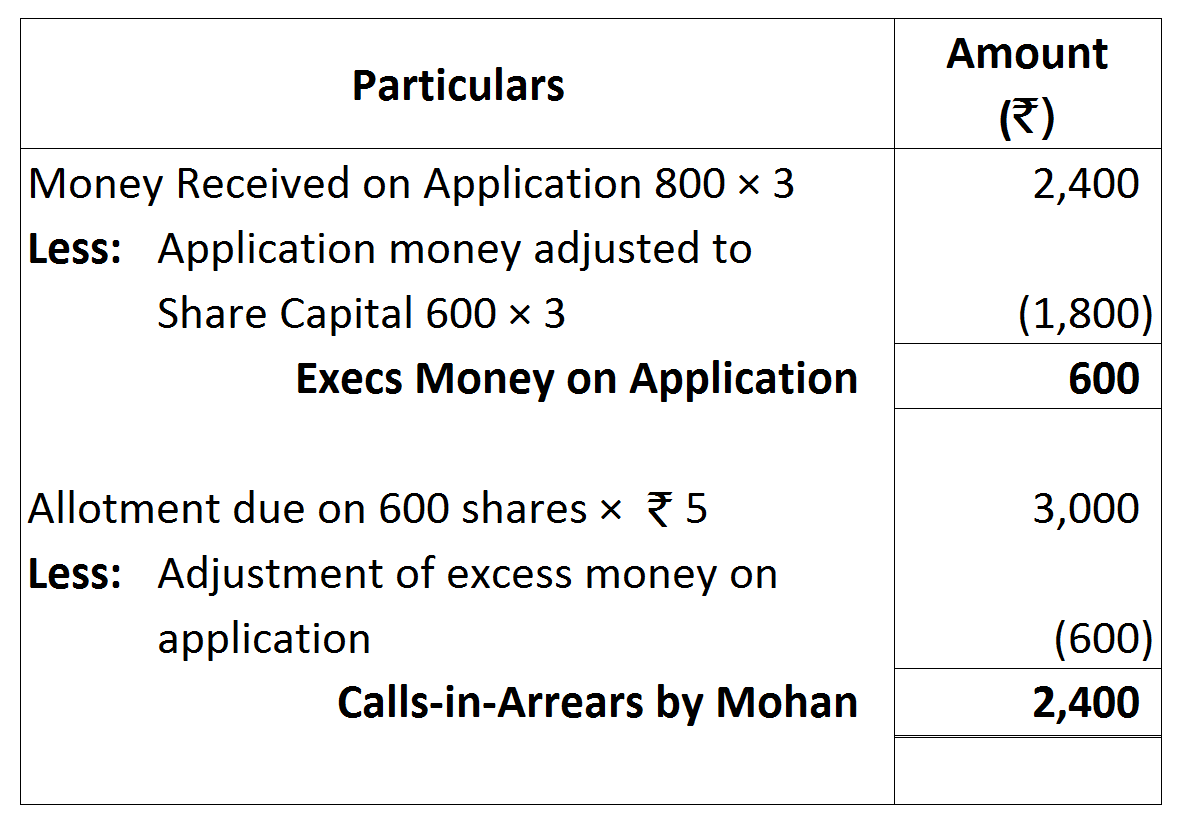

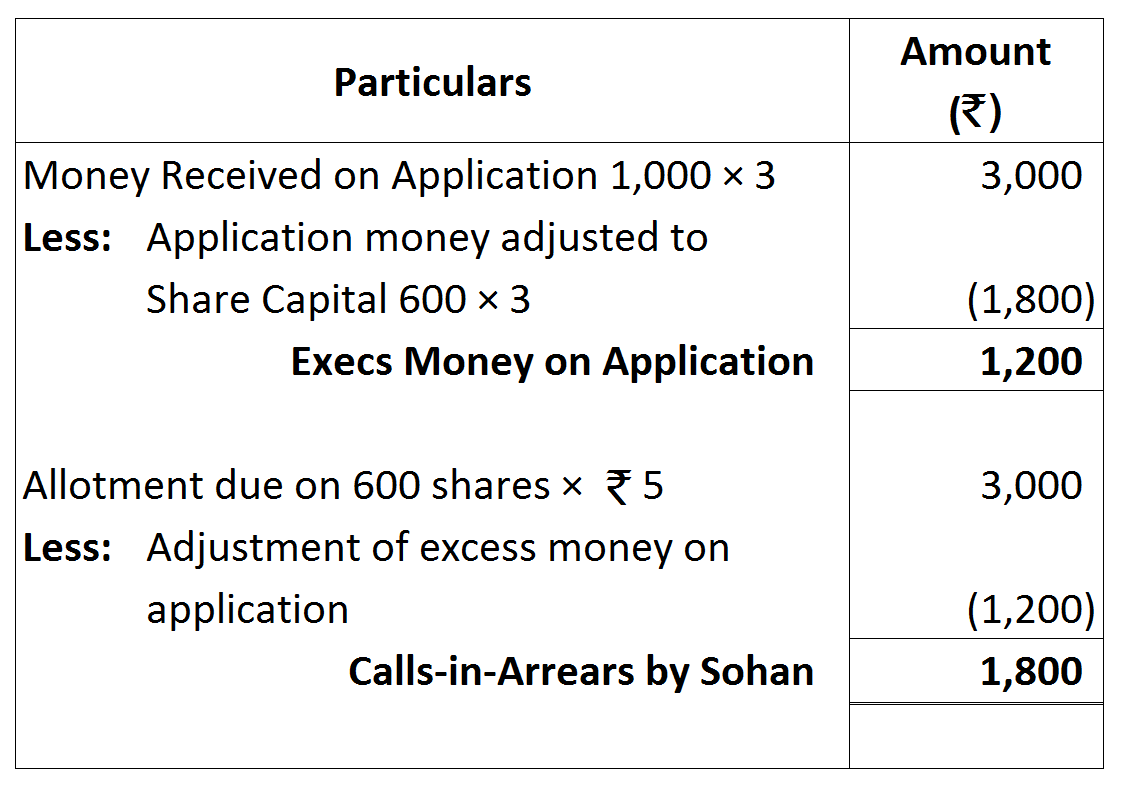

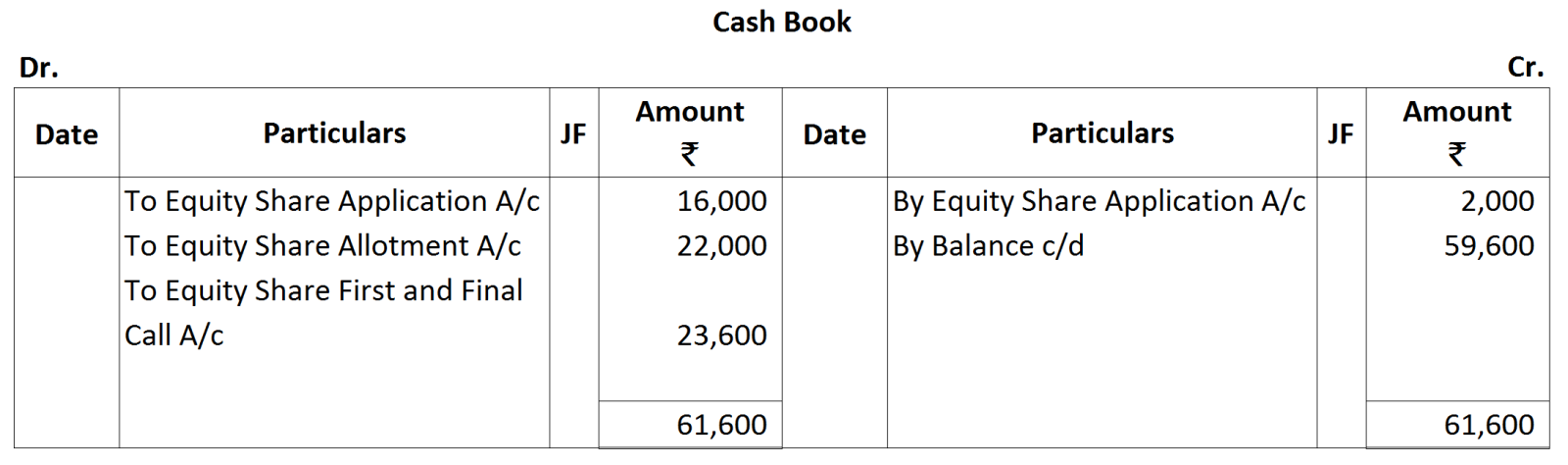

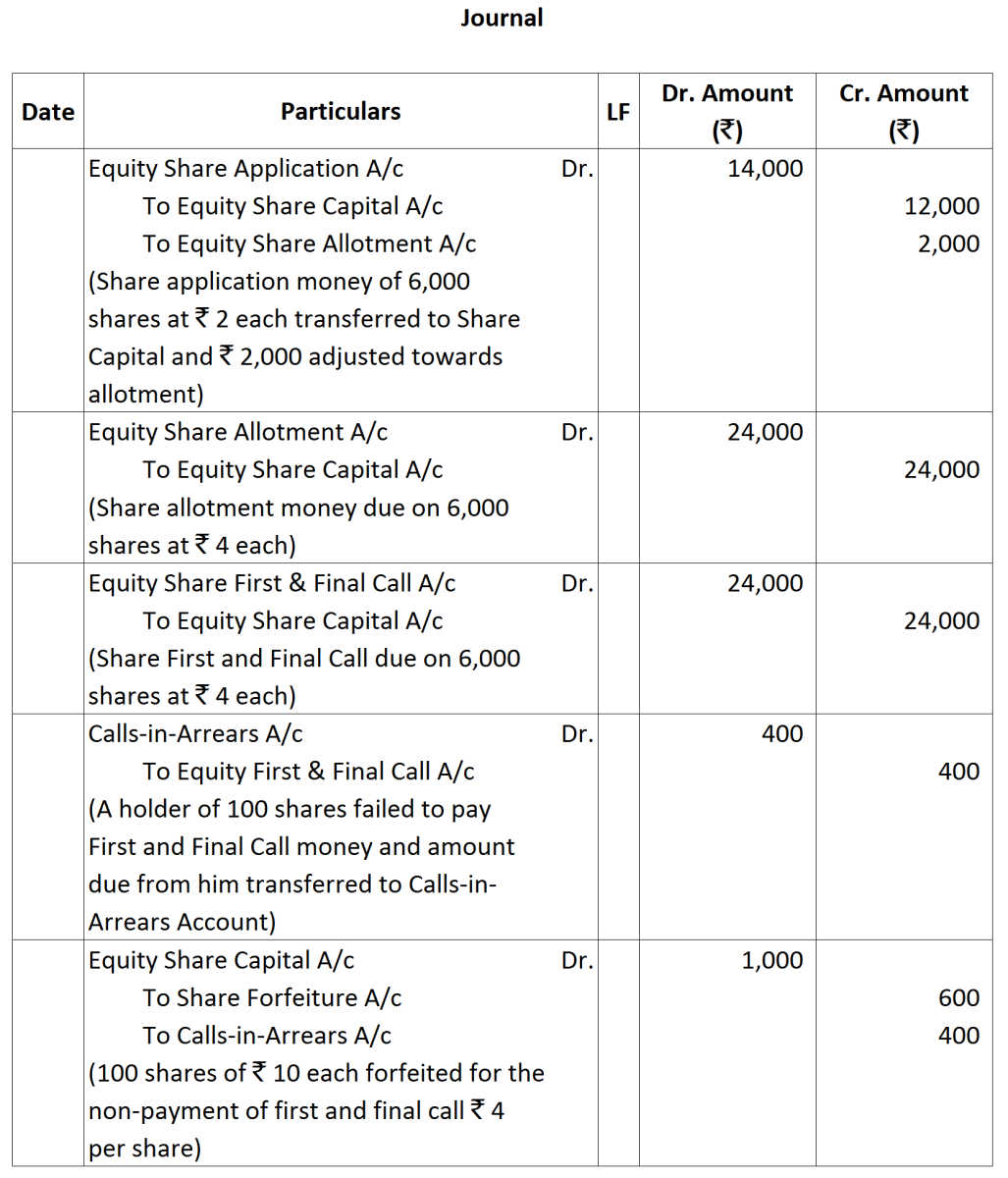

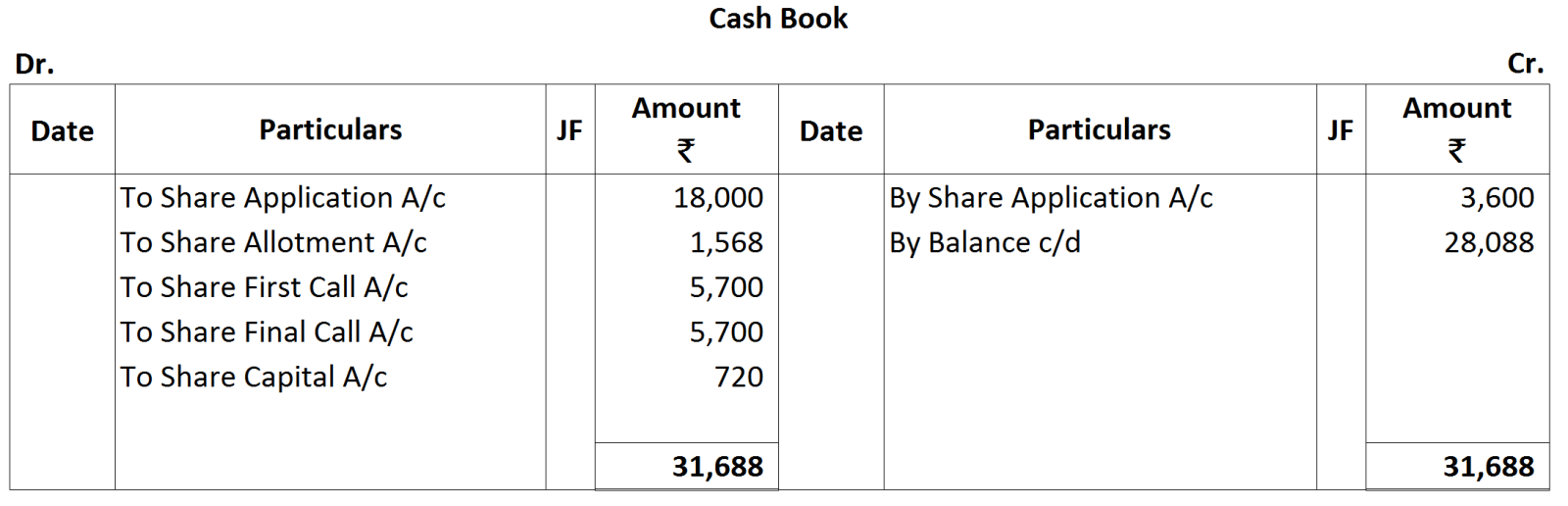

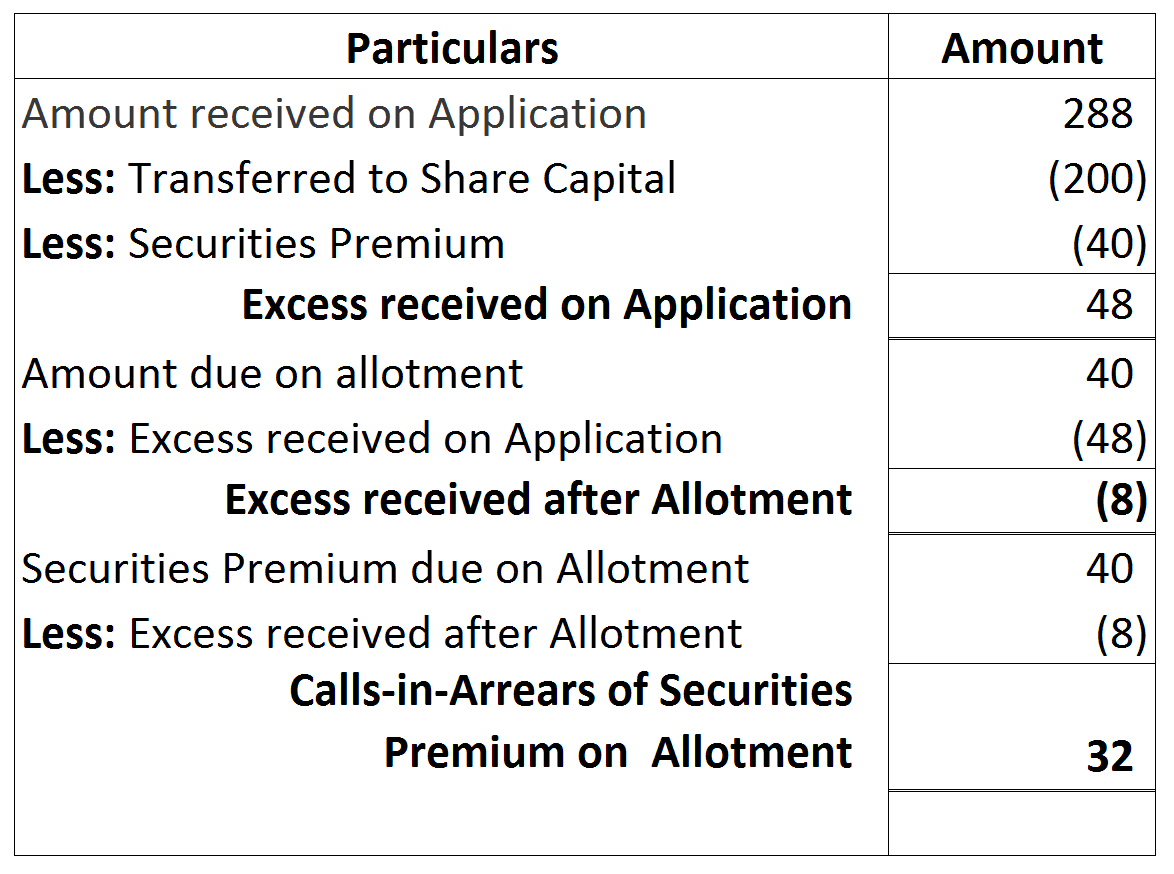

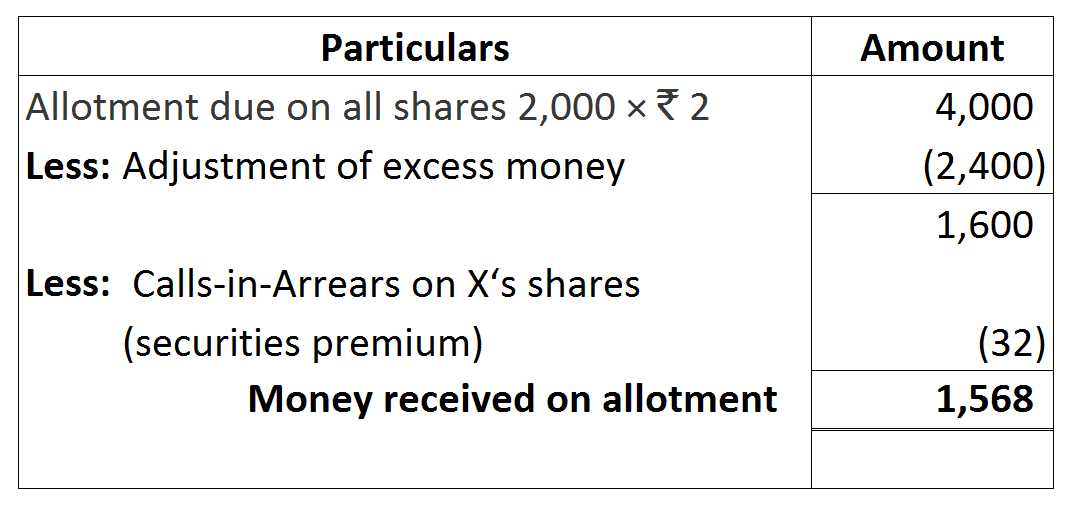

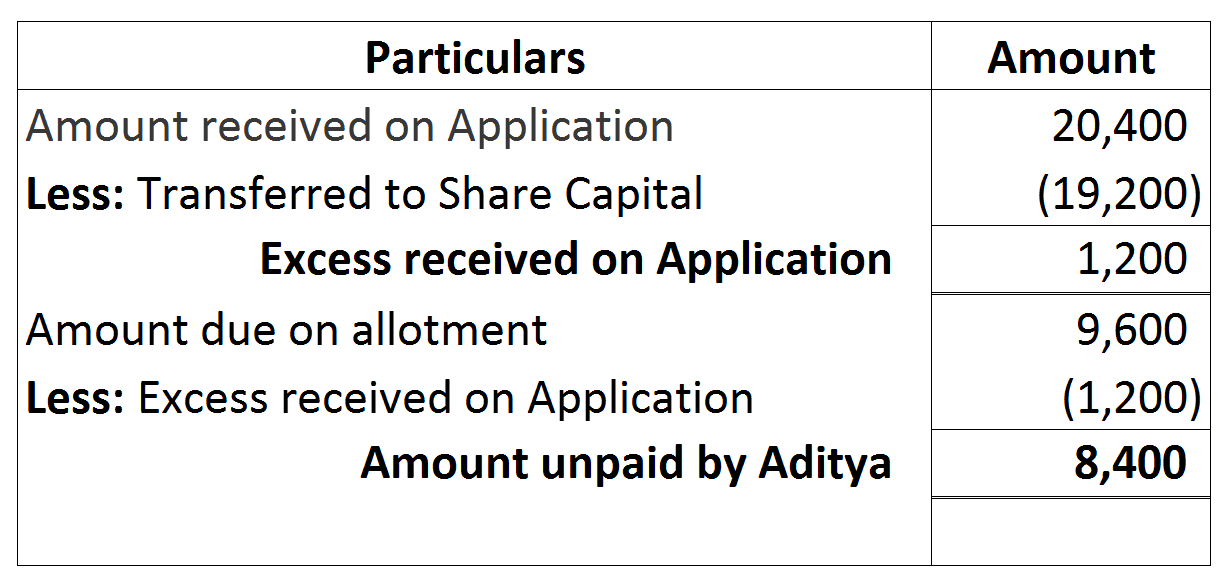

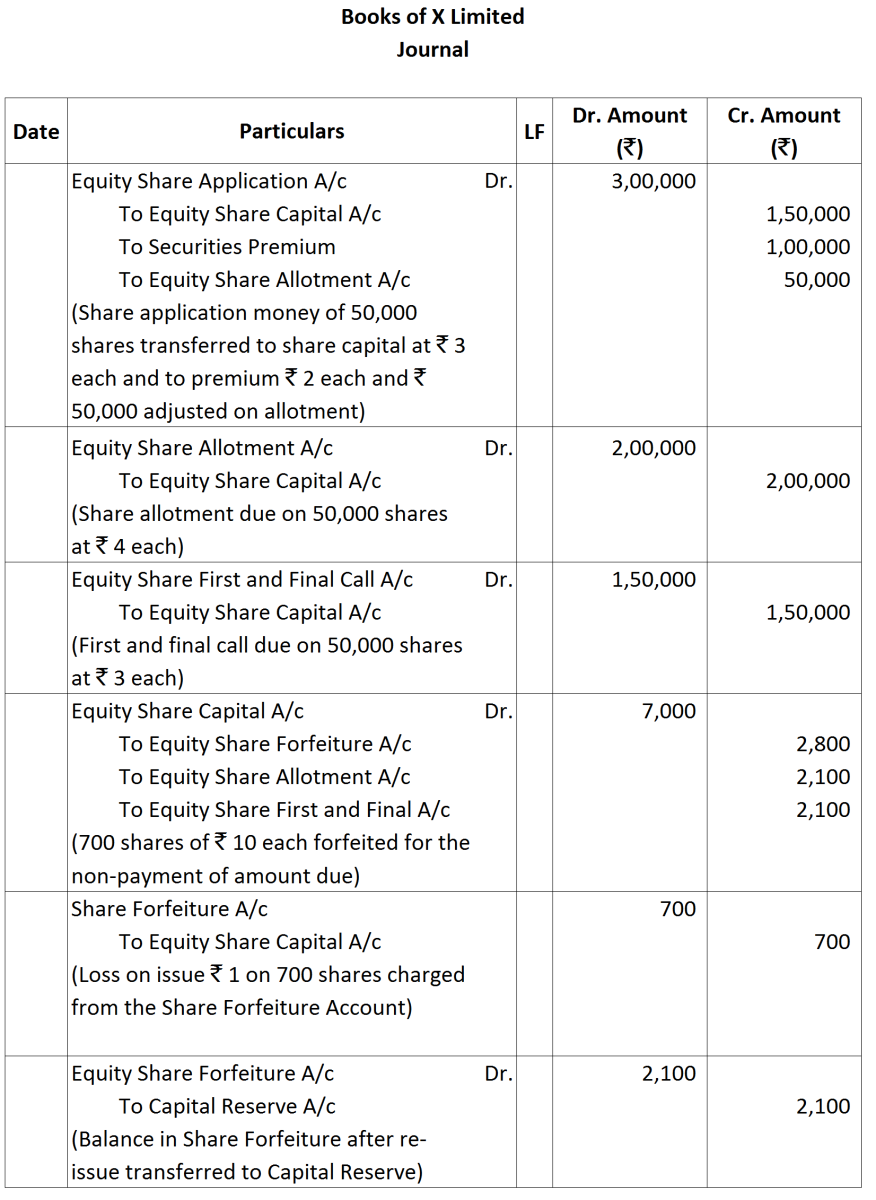

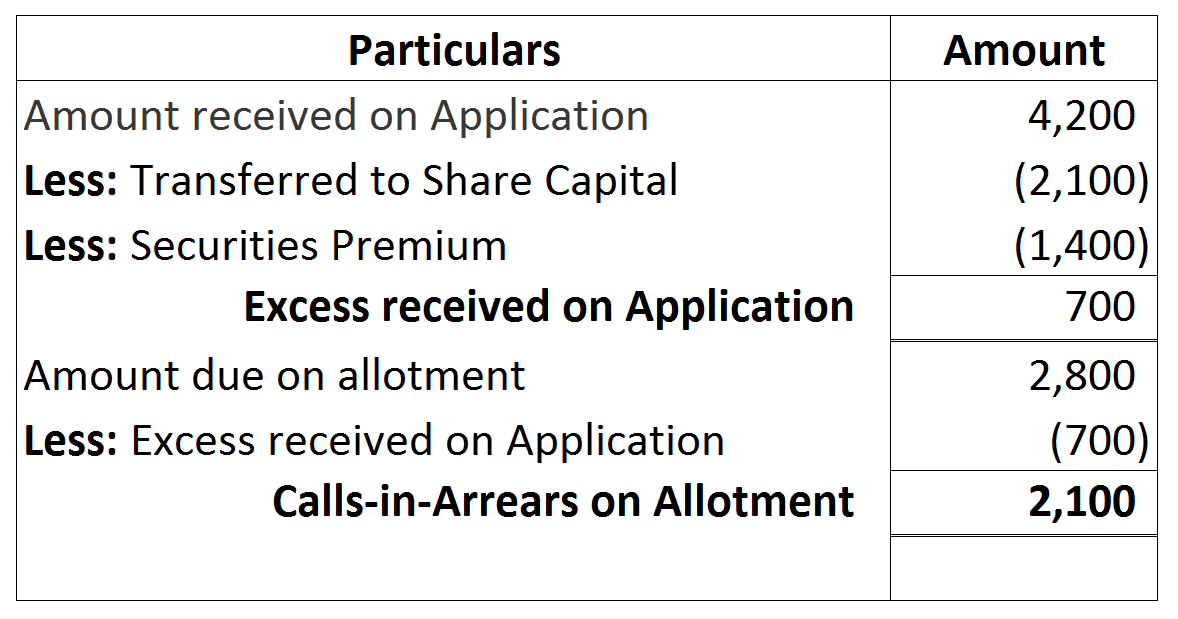

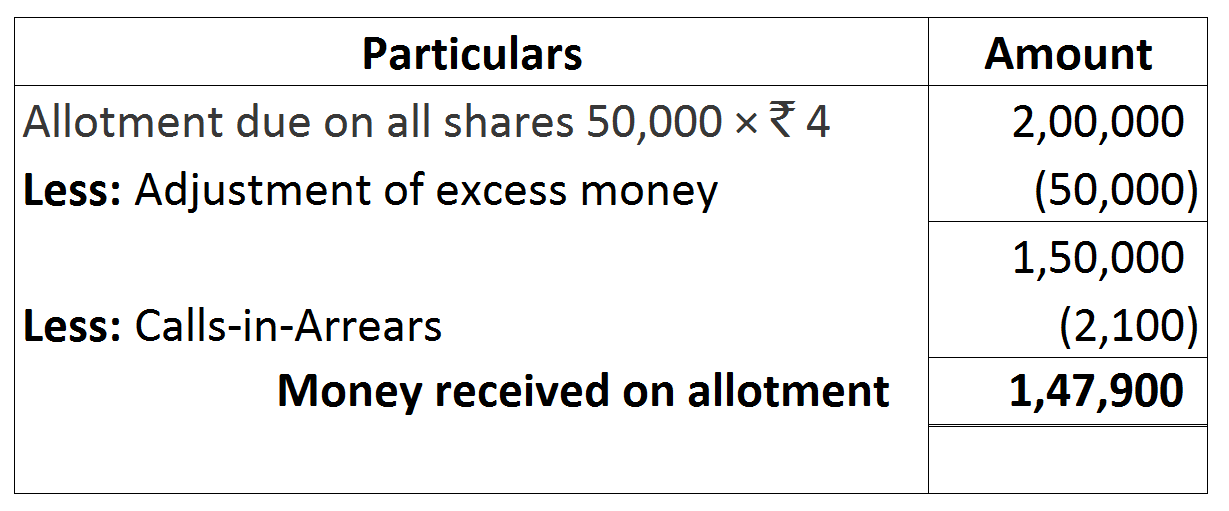

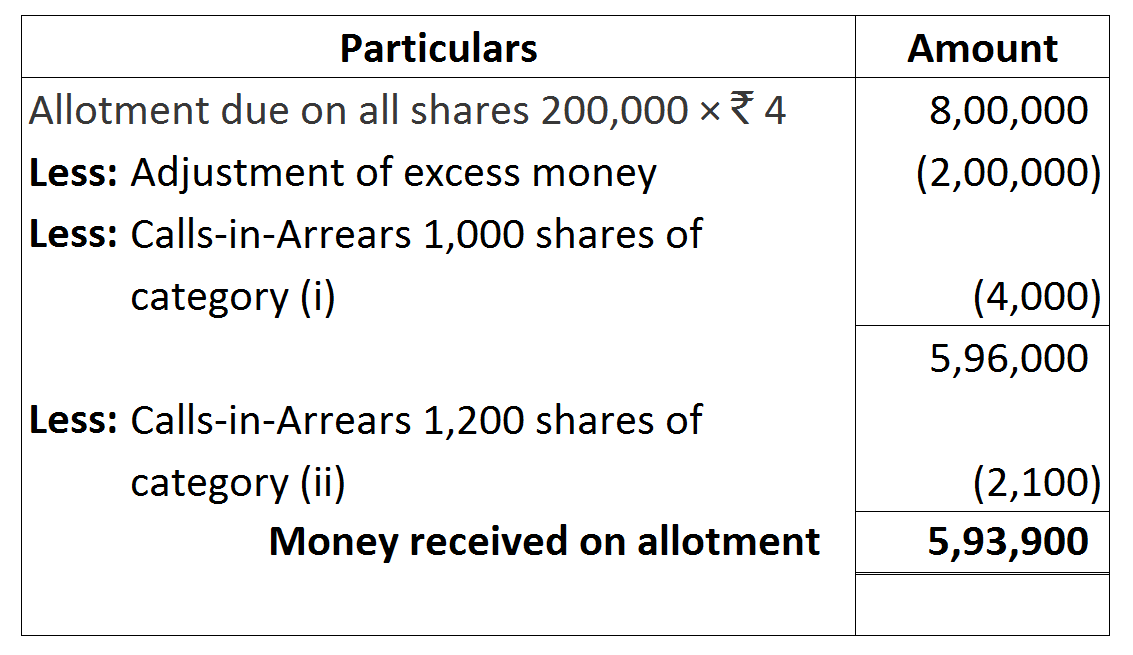

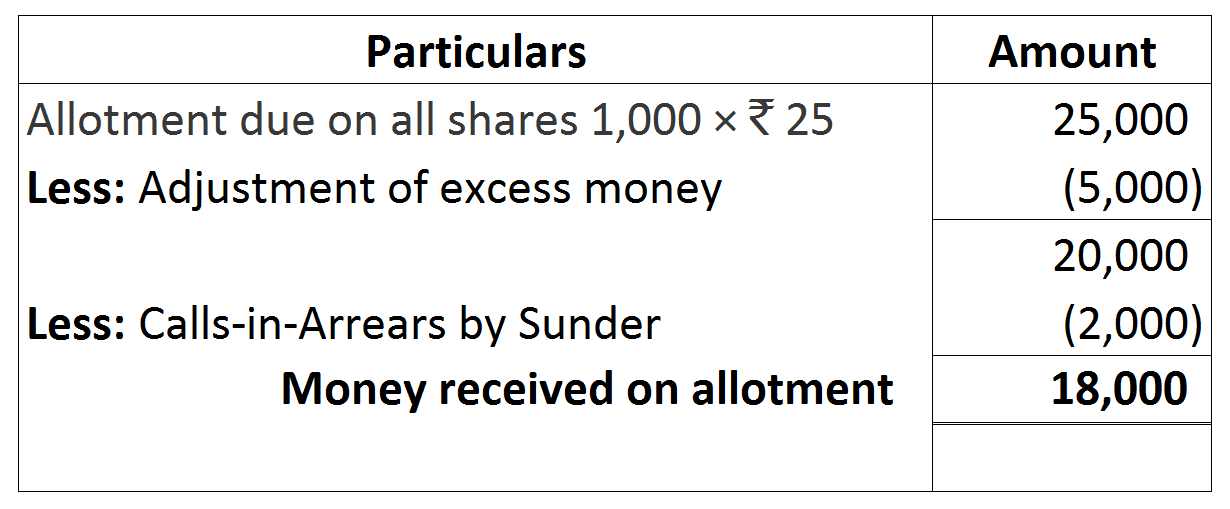

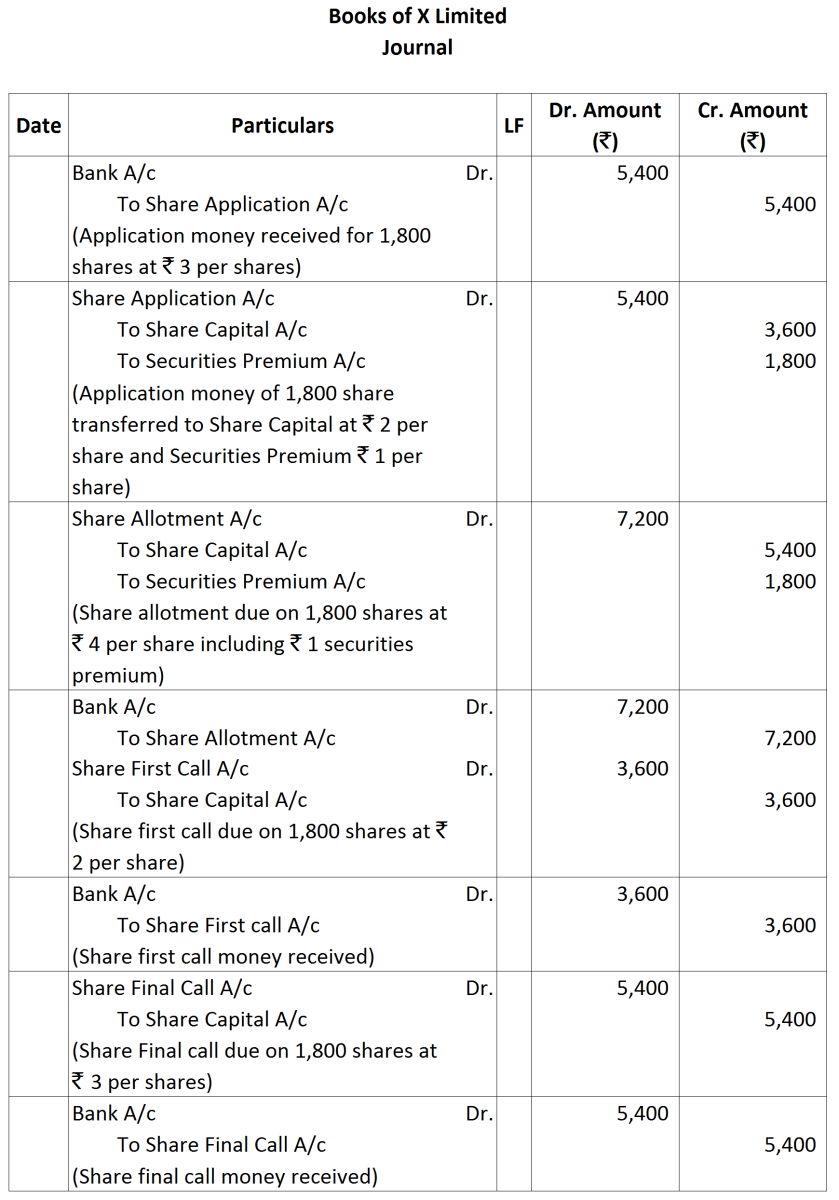

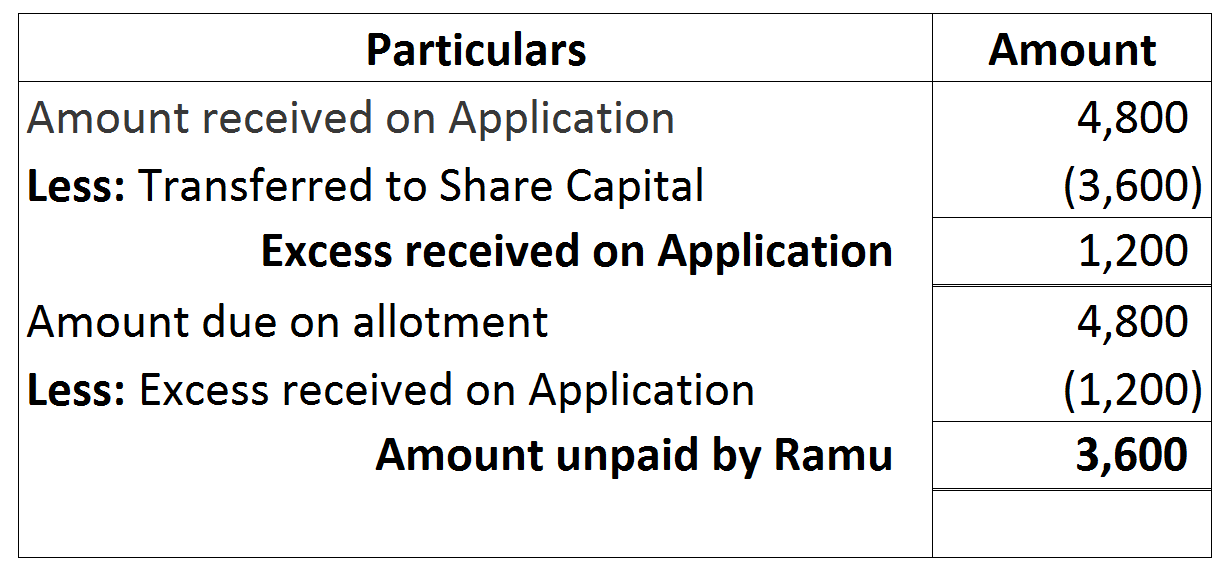

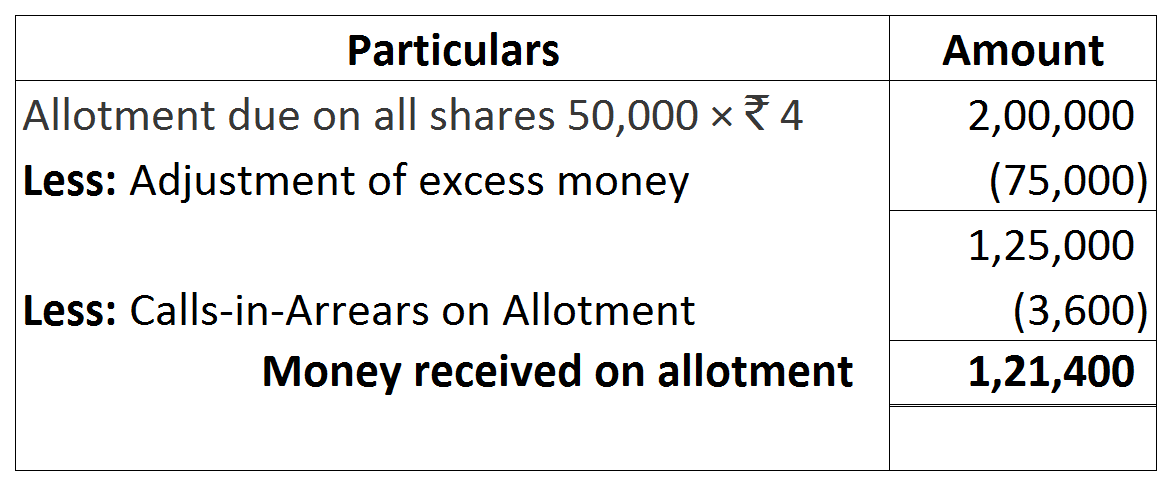

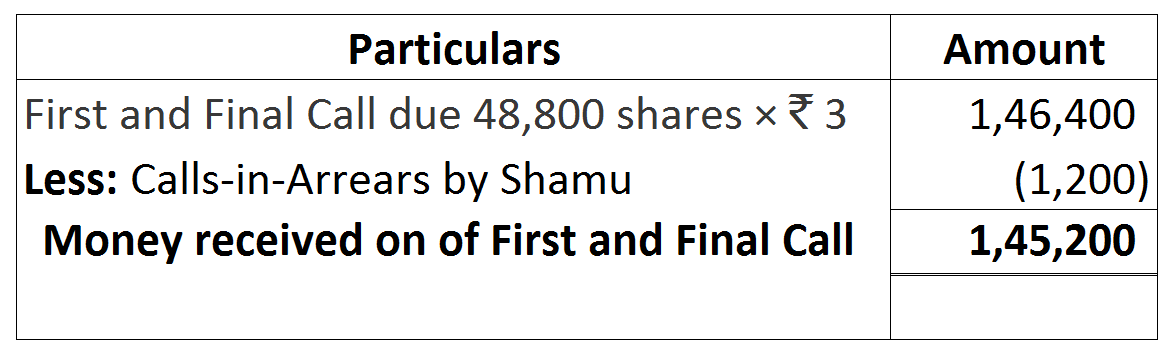

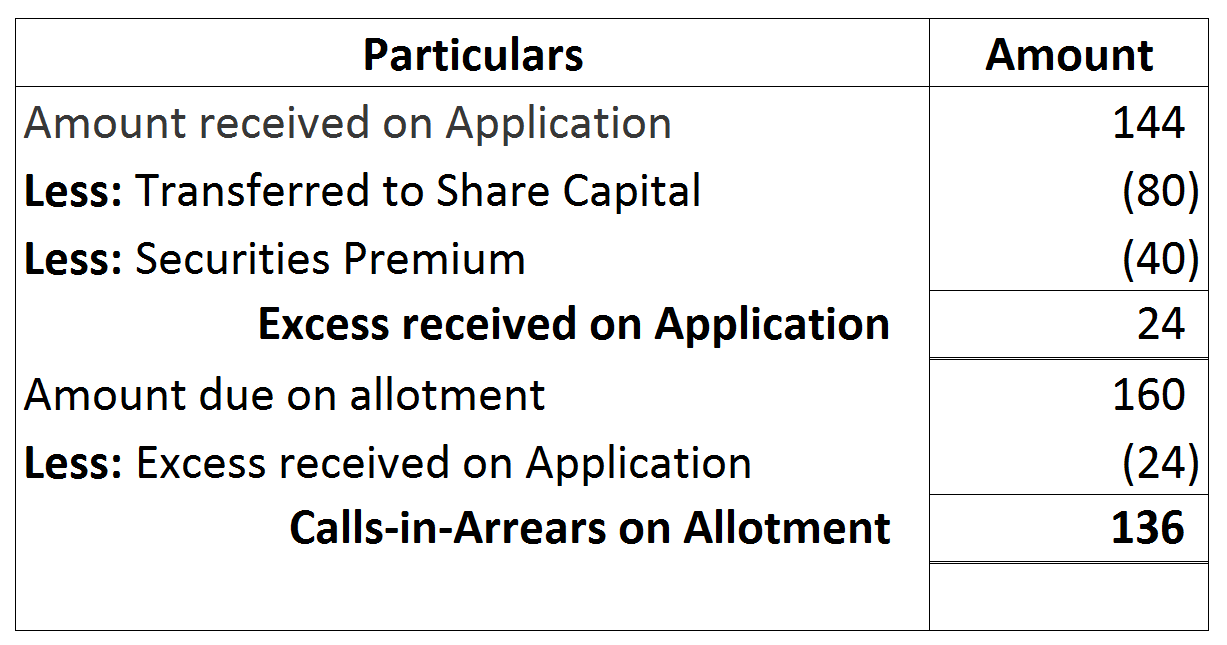

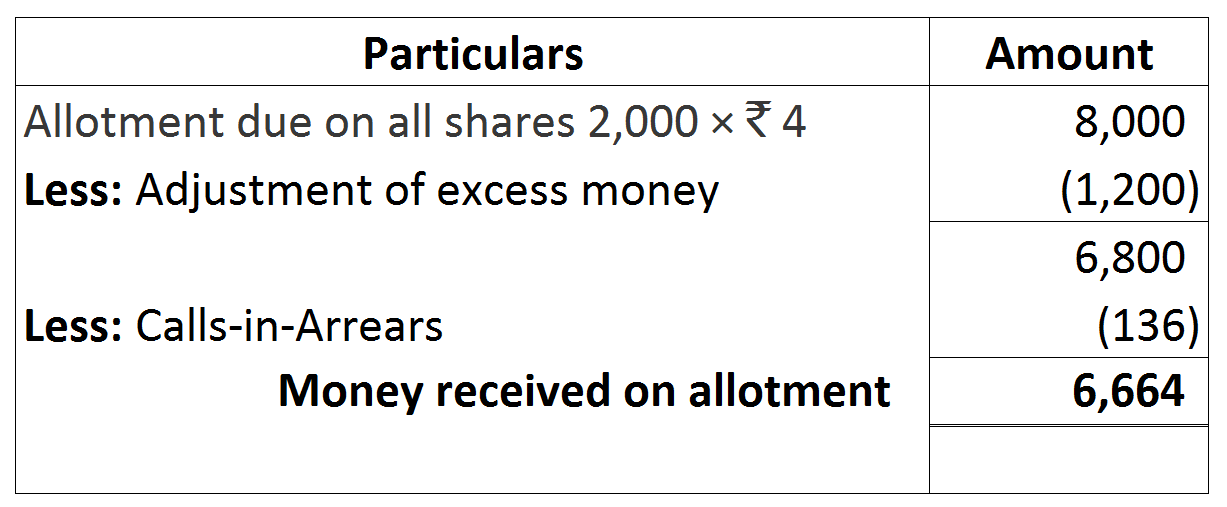

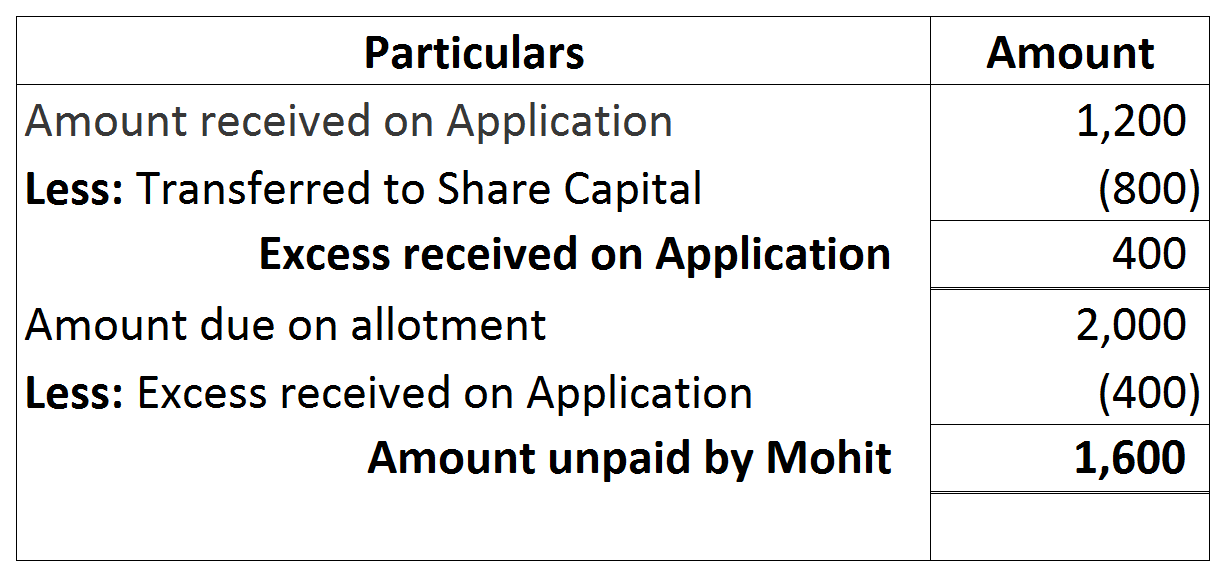

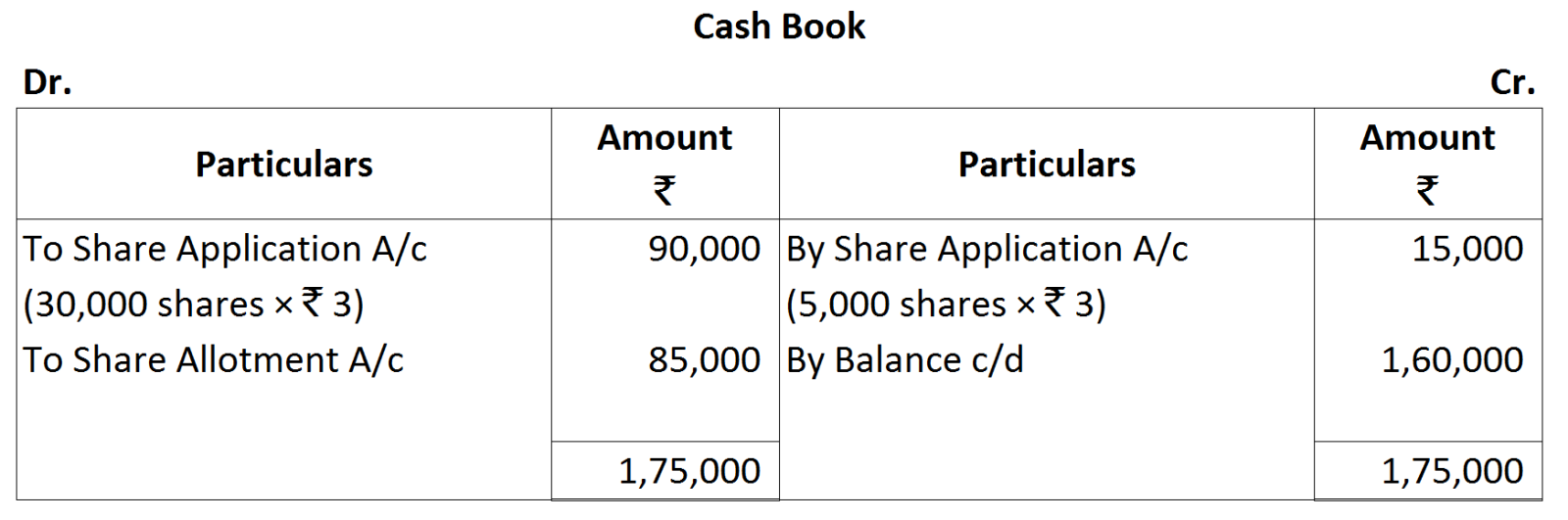

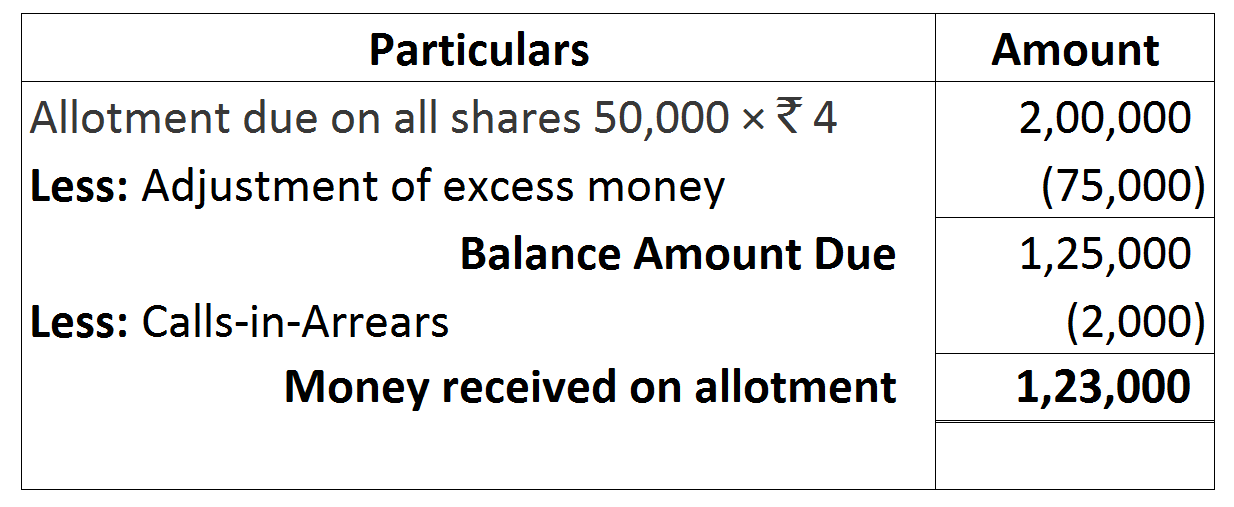

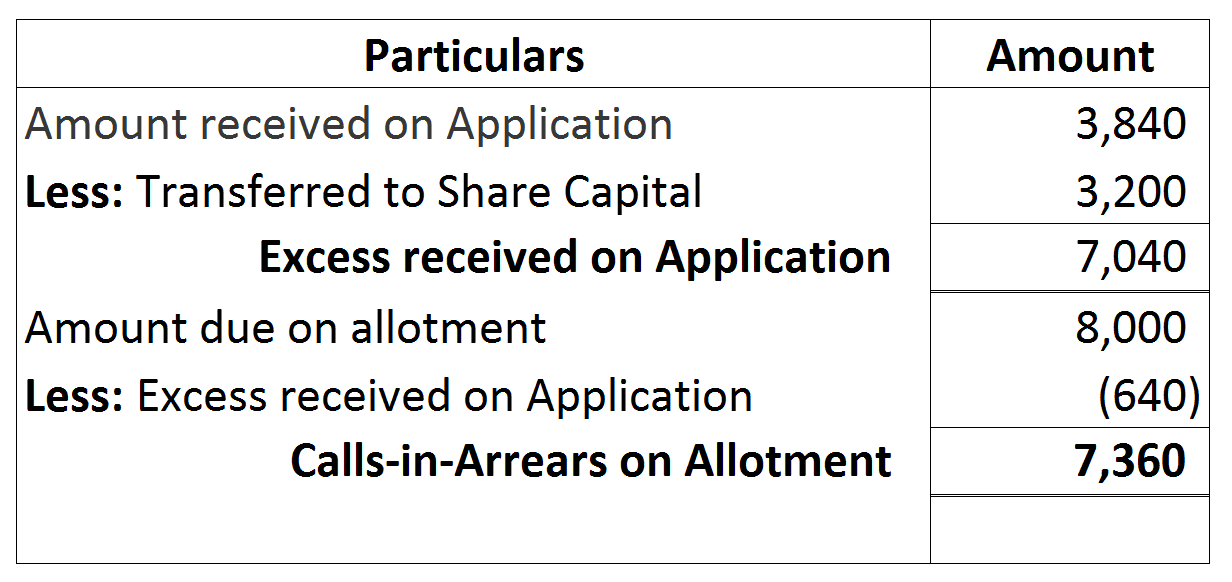

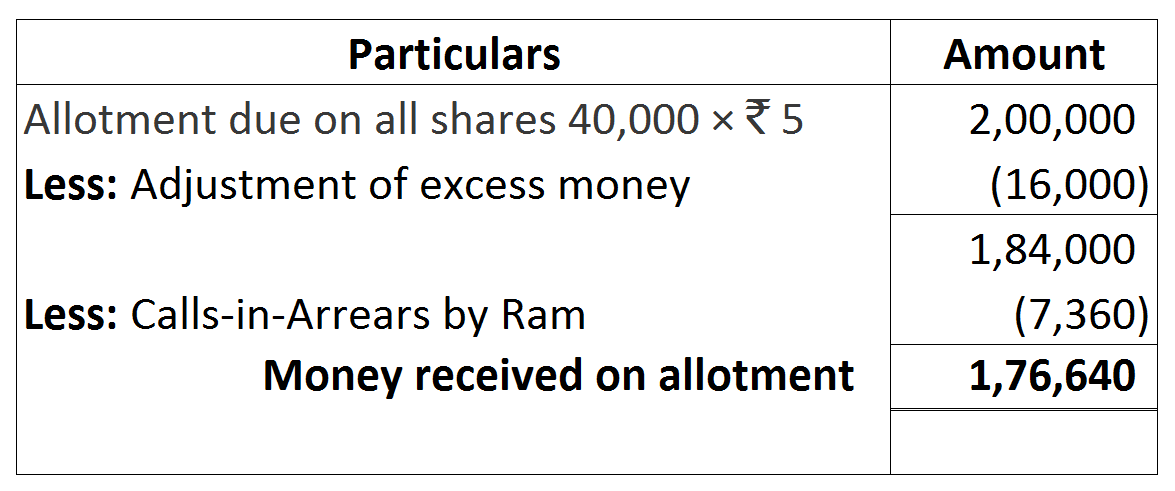

Share Allotment:

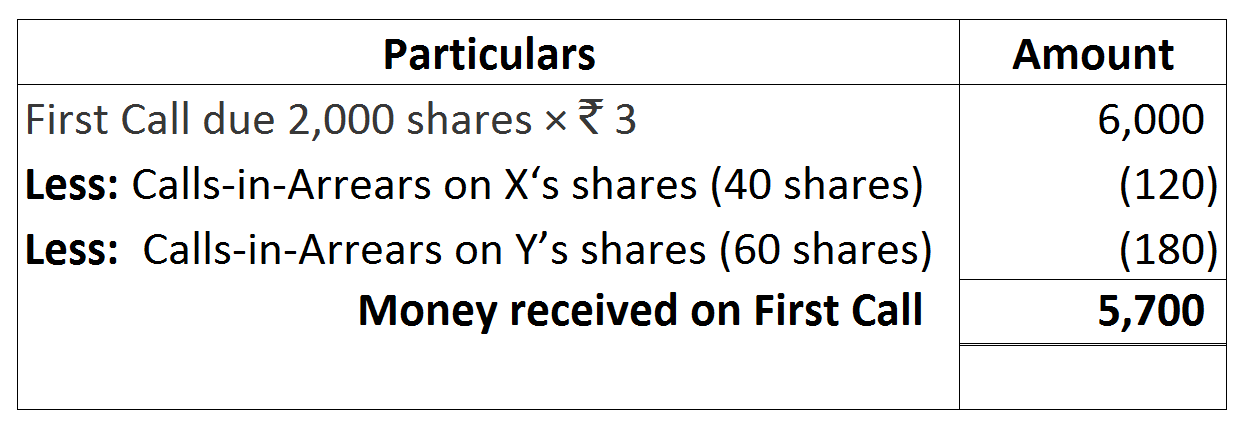

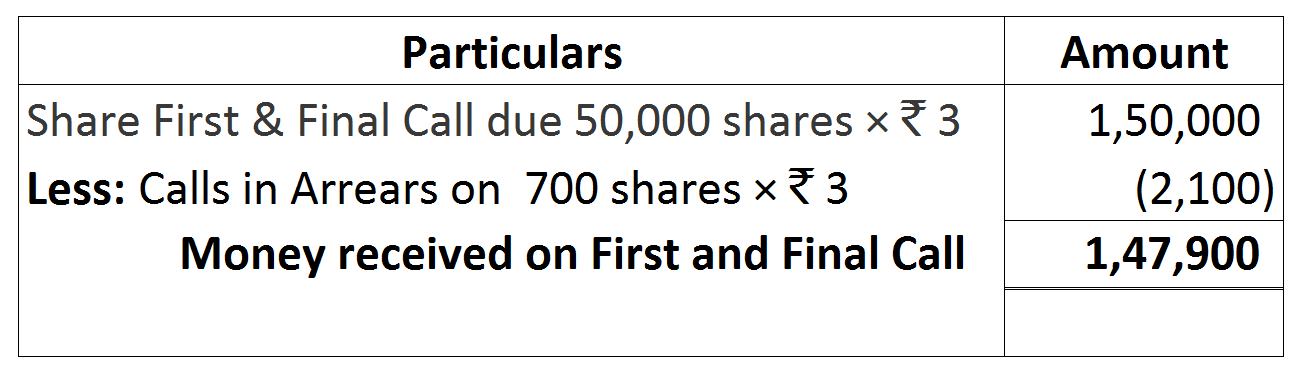

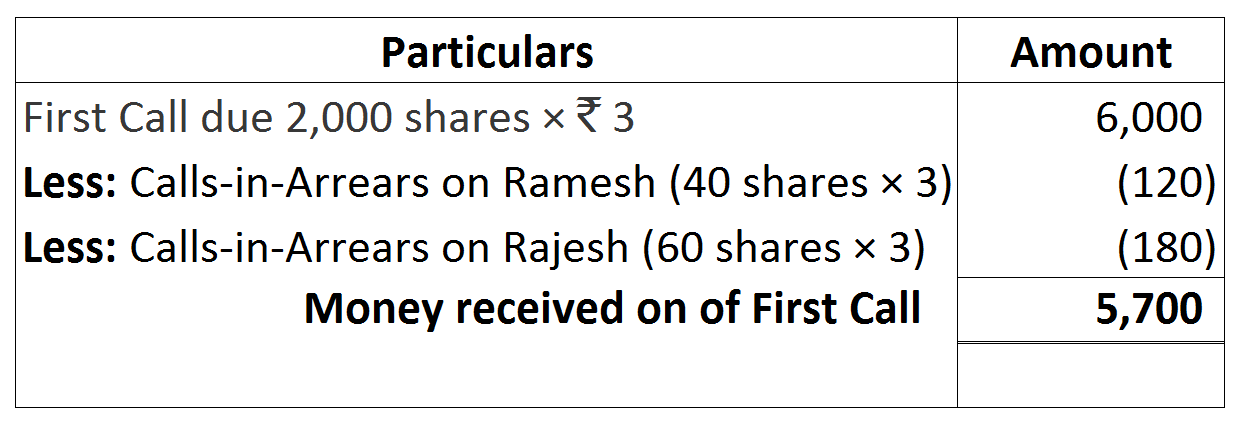

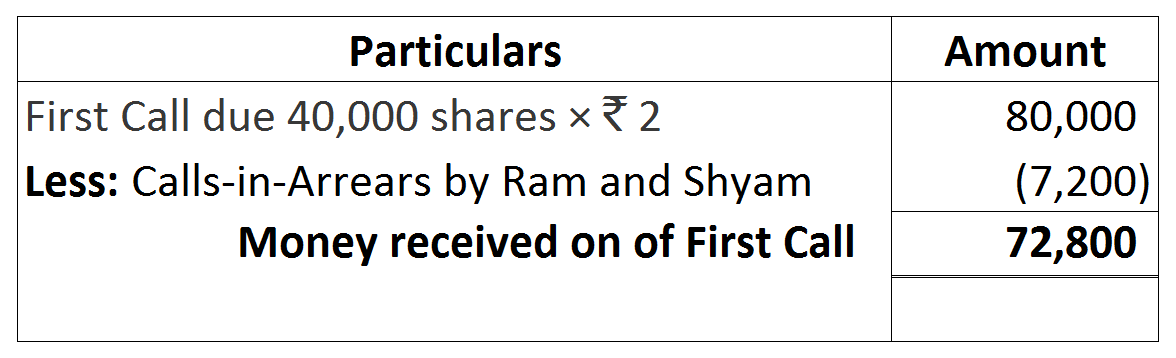

Share Allotment:  Share First Call:

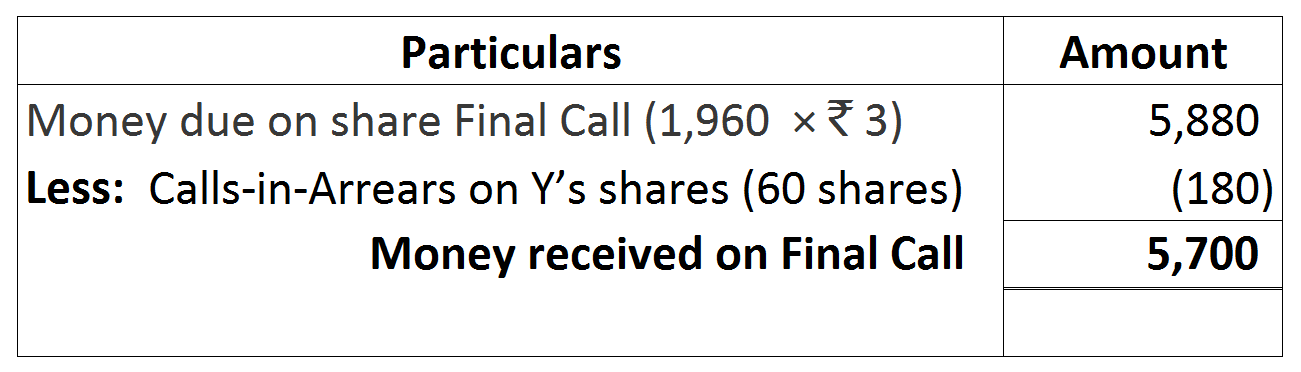

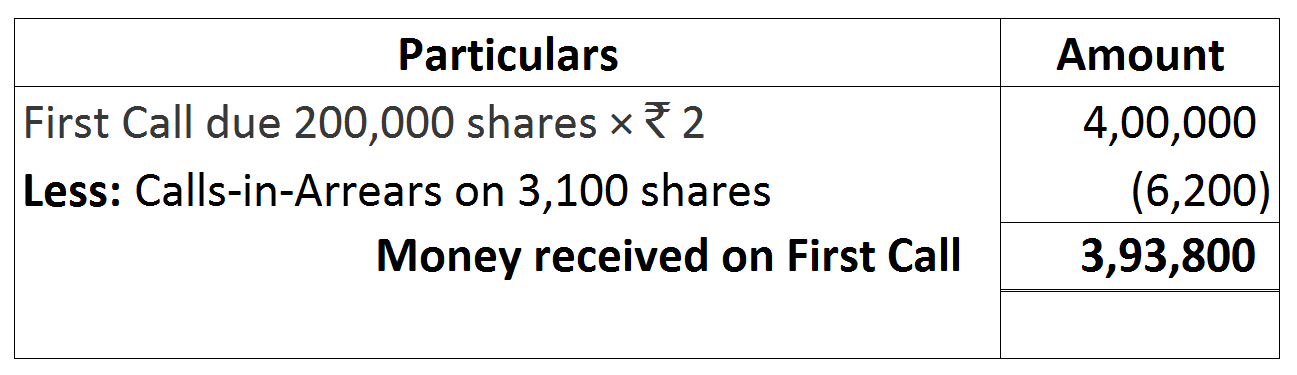

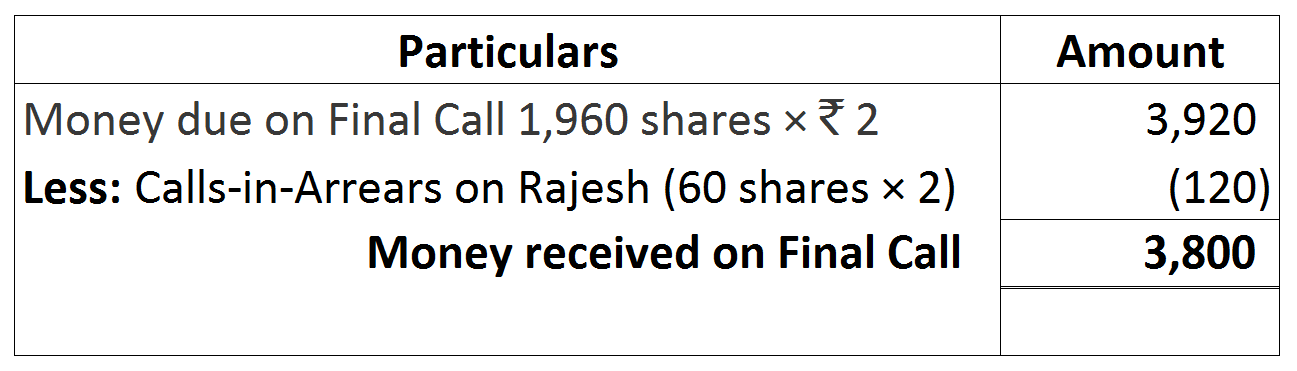

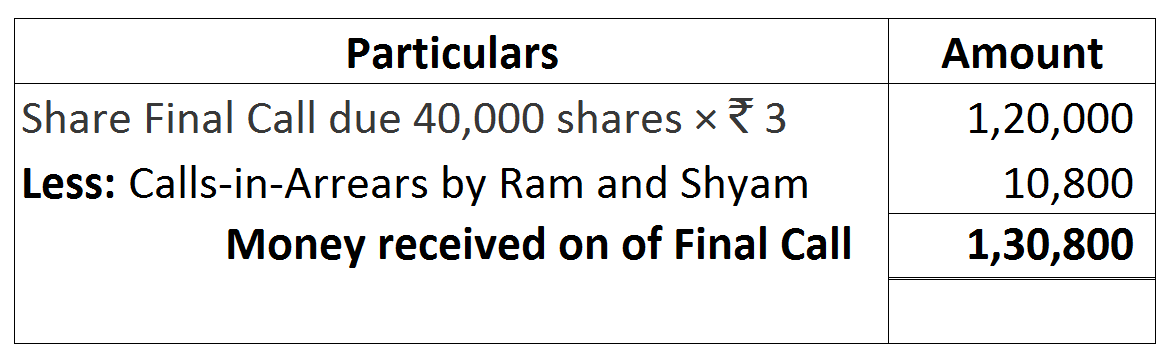

Share First Call:  Share Final Call:

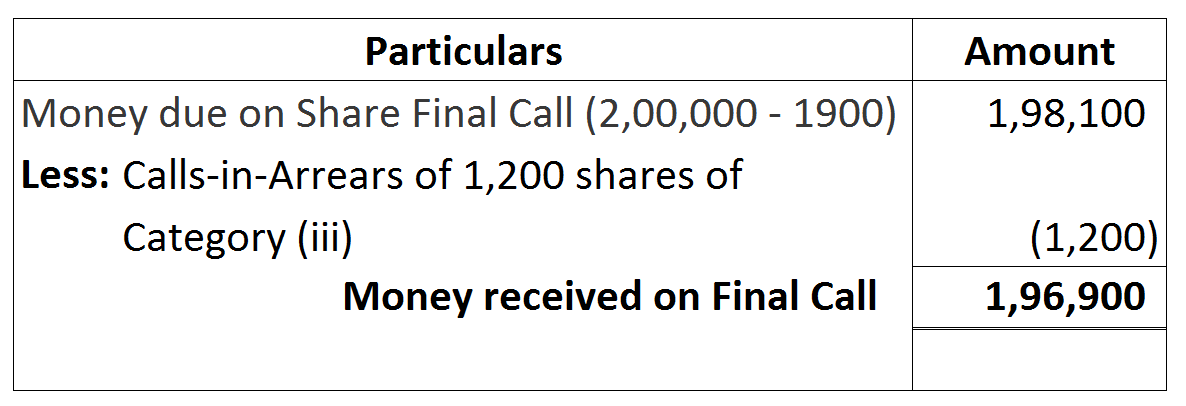

Share Final Call:  Capital Reserve:

Capital Reserve:

Working Notes:

Working Notes:

Working Notes:

Working Notes: