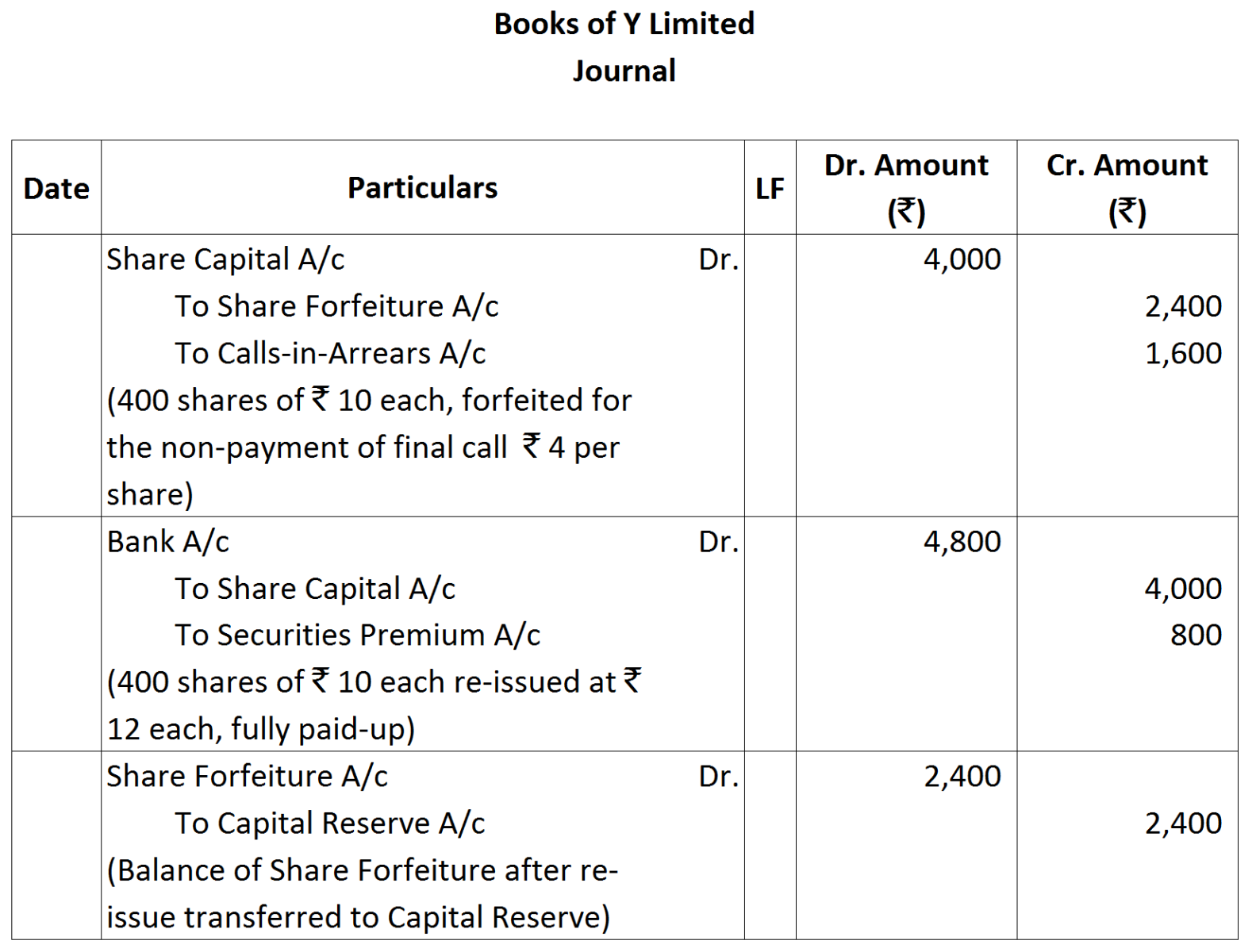

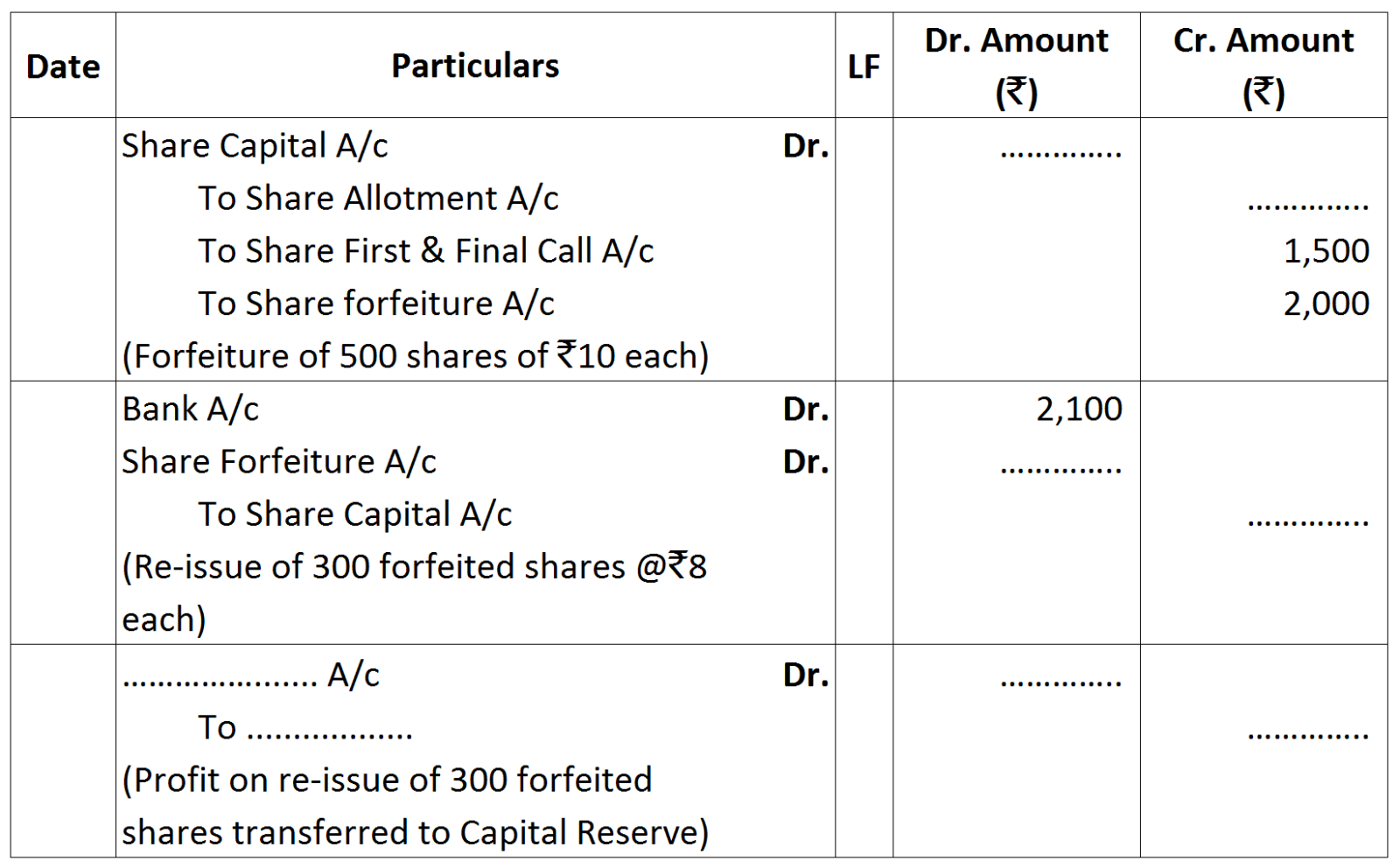

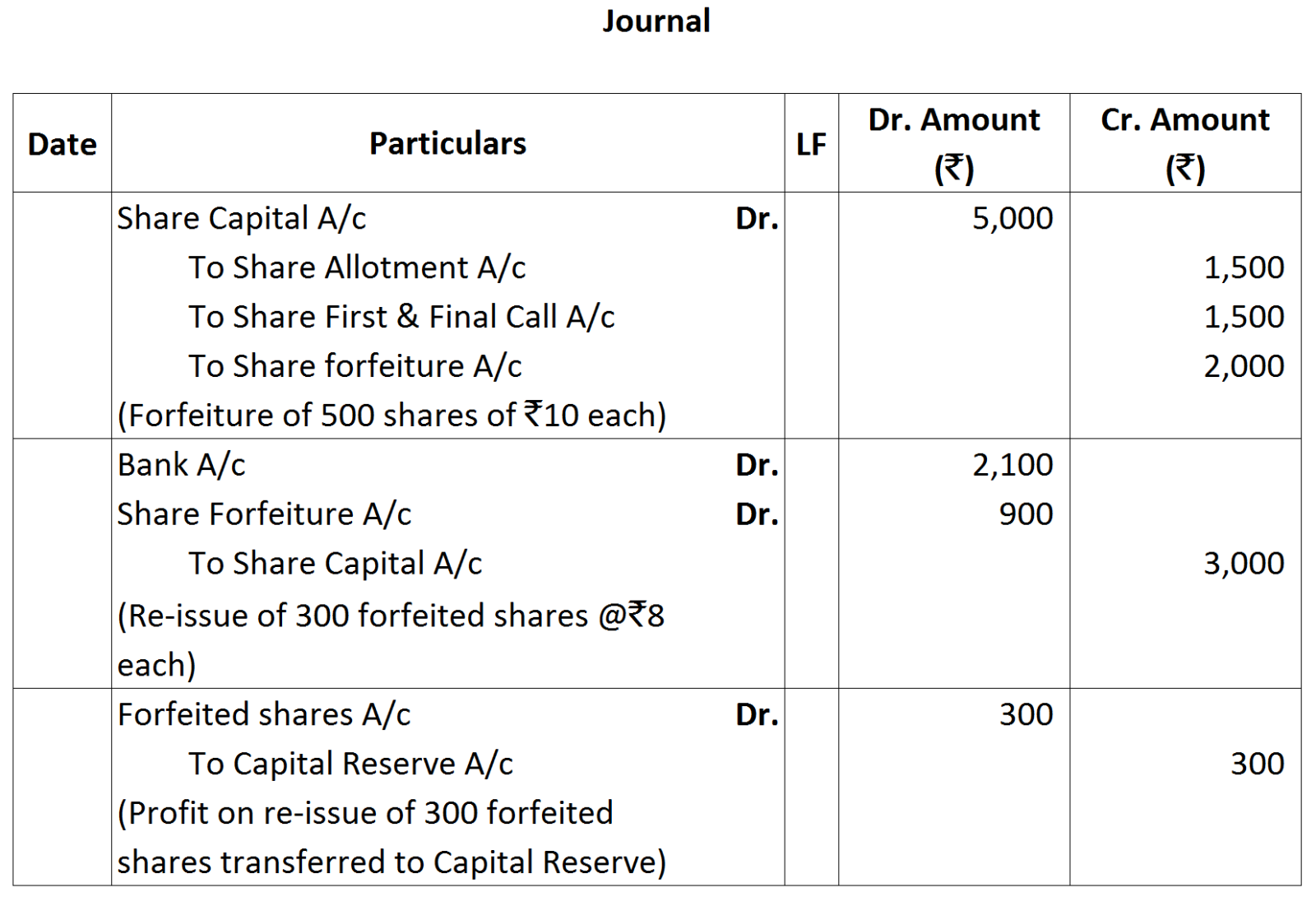

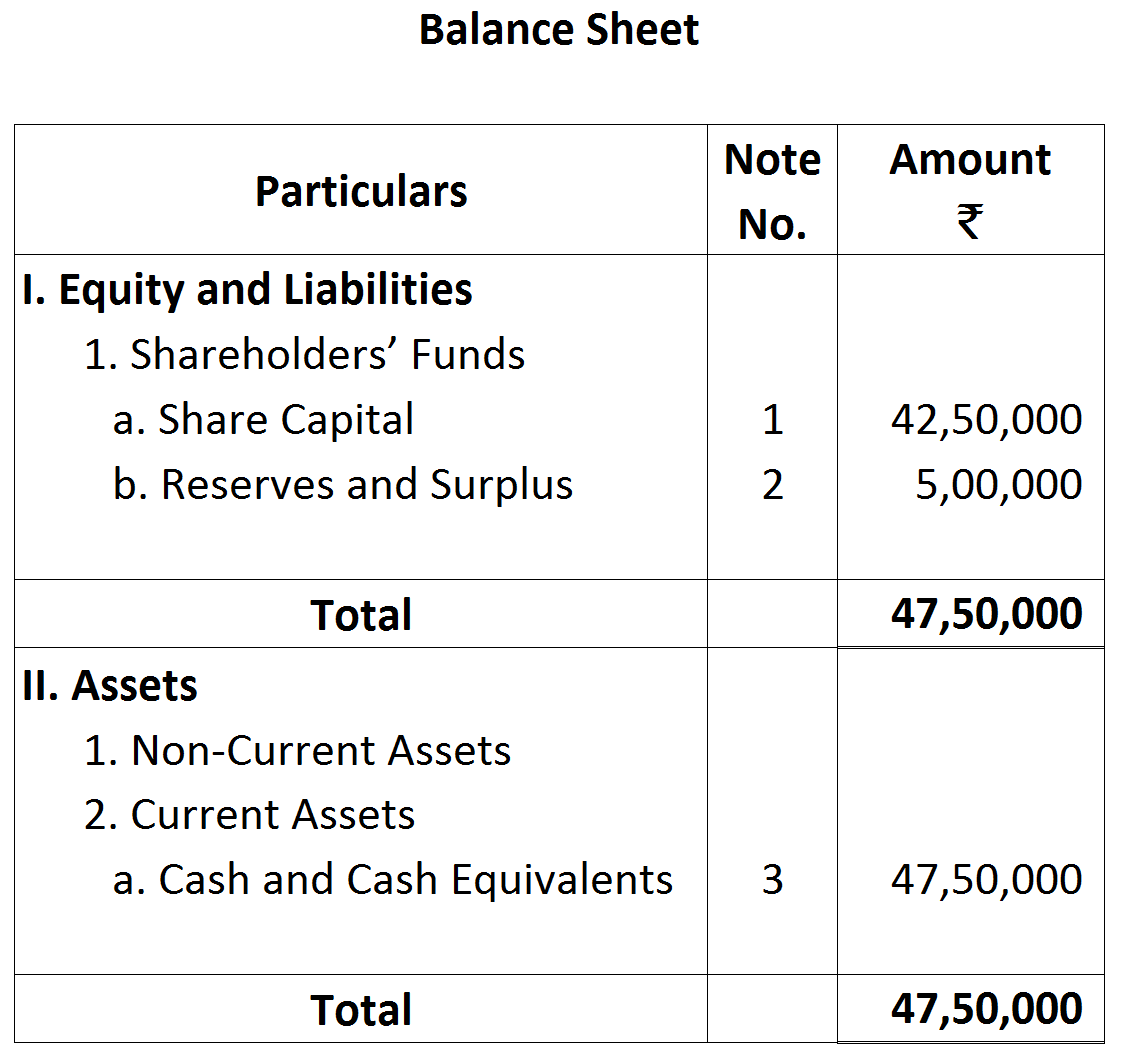

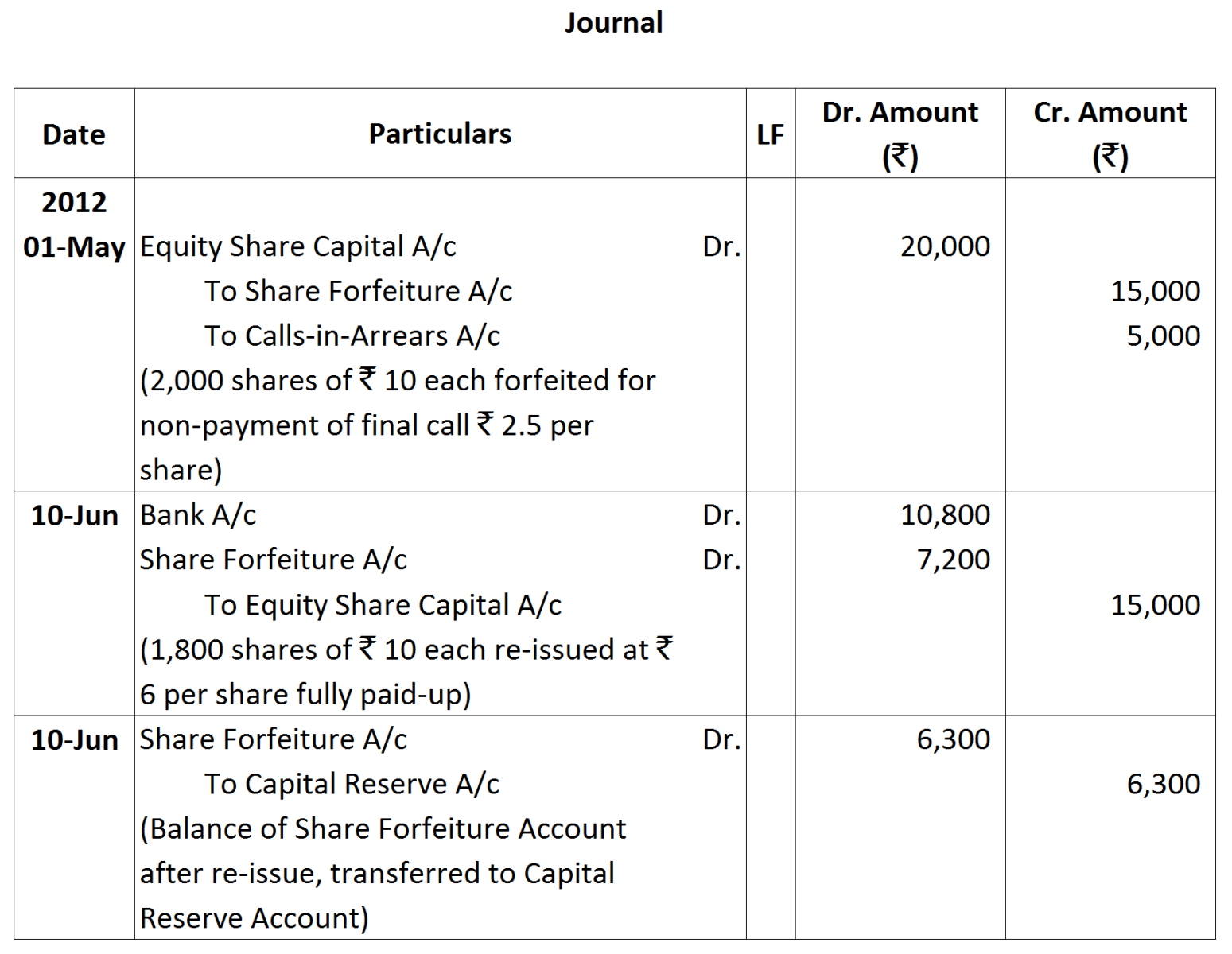

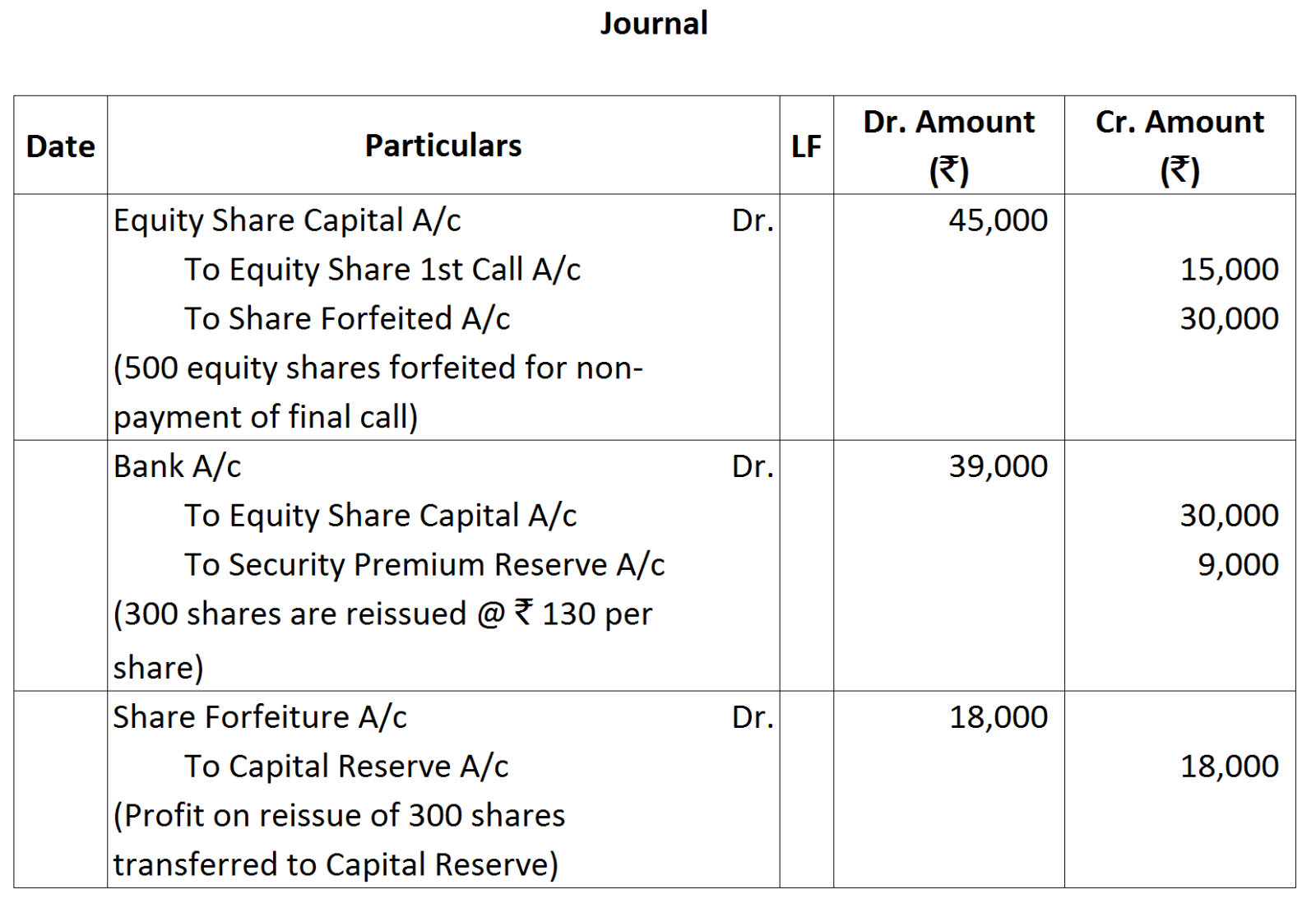

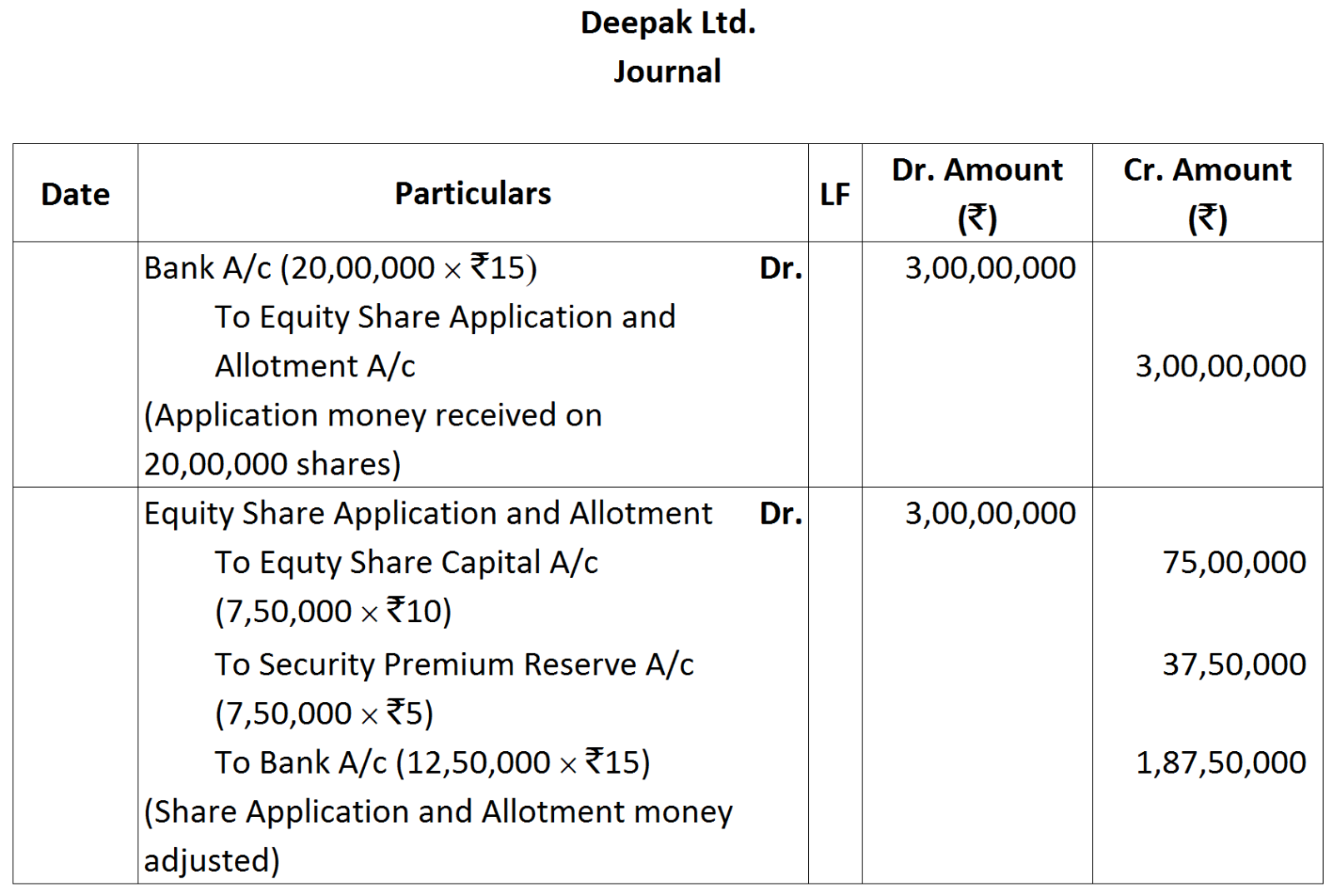

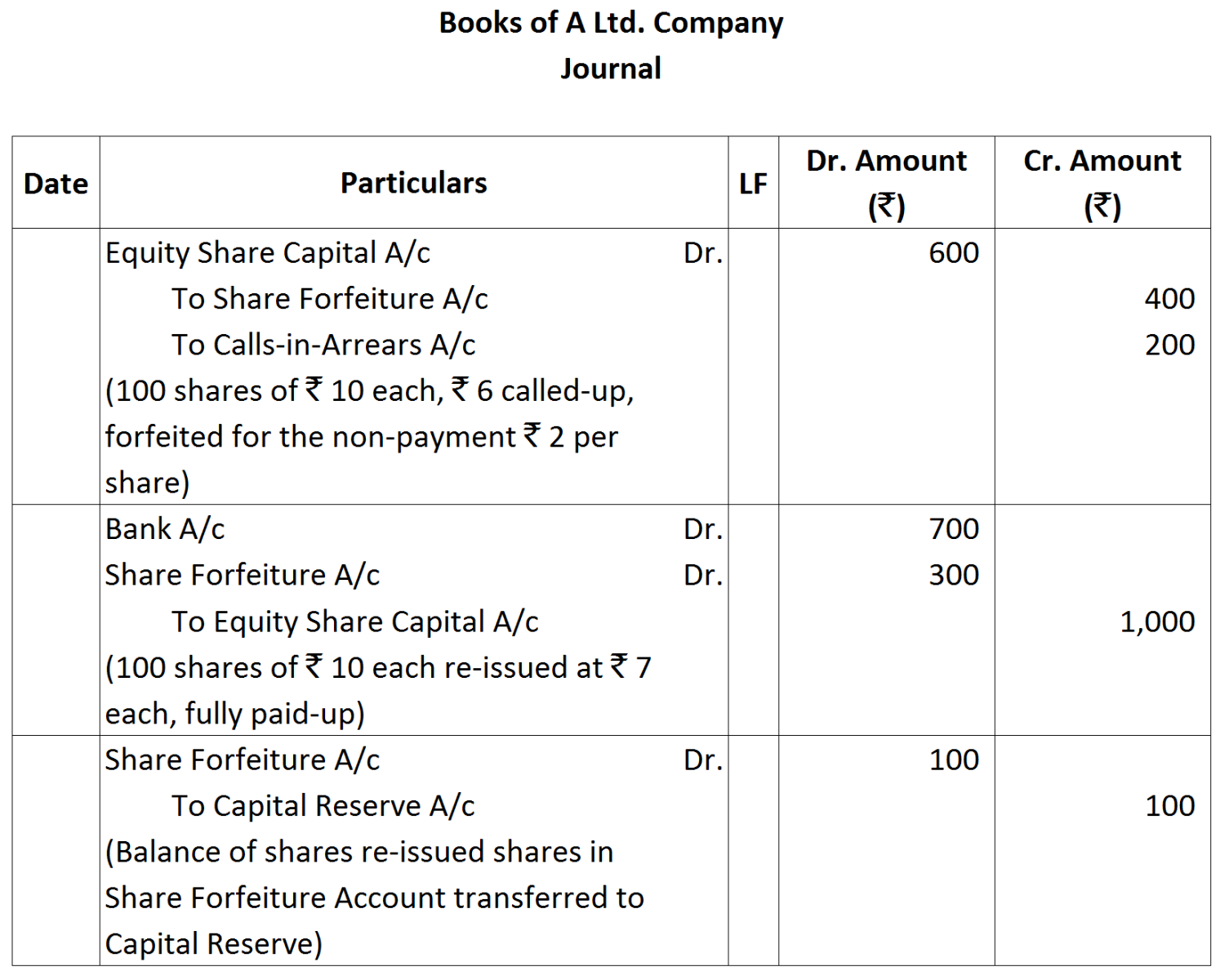

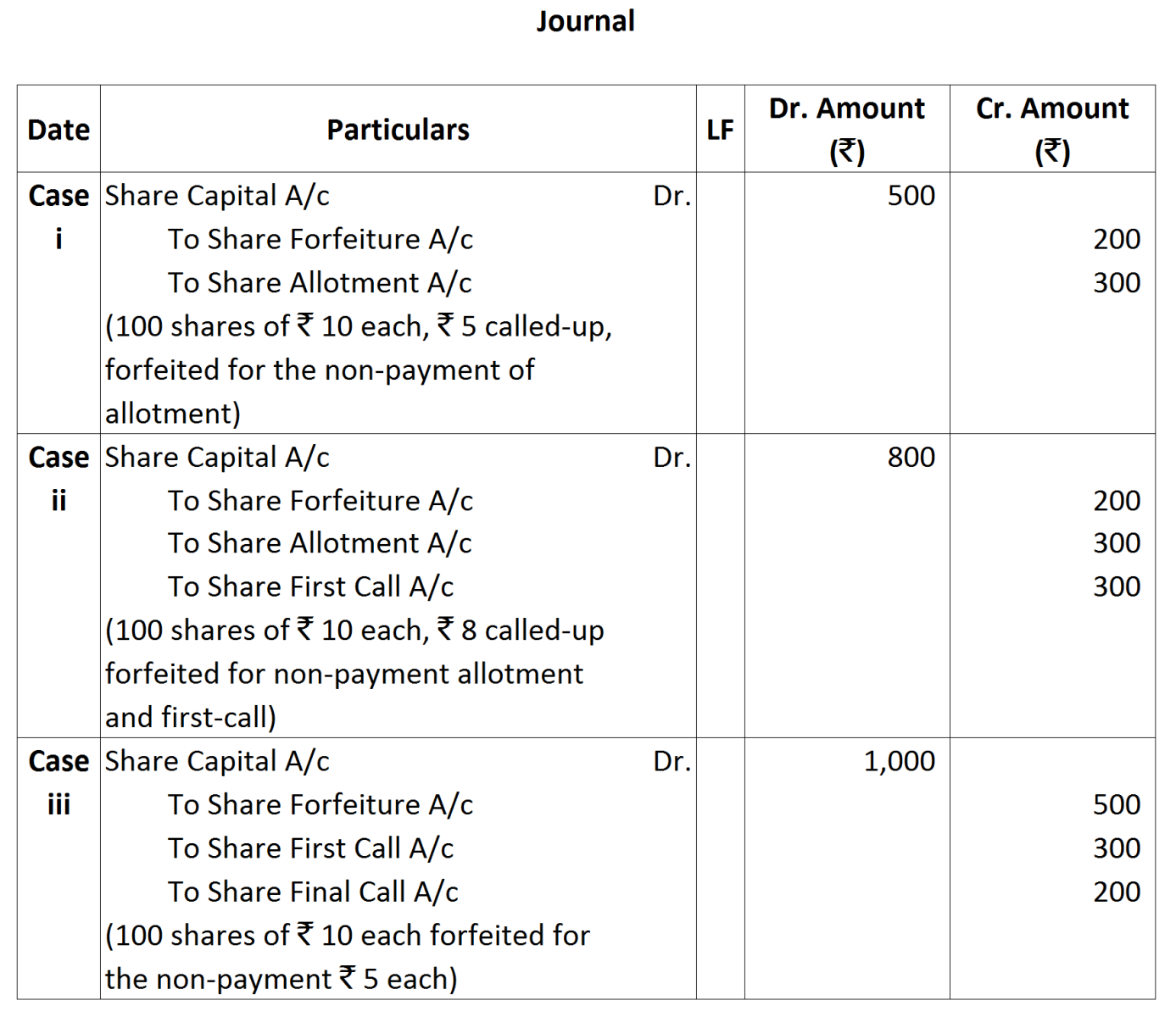

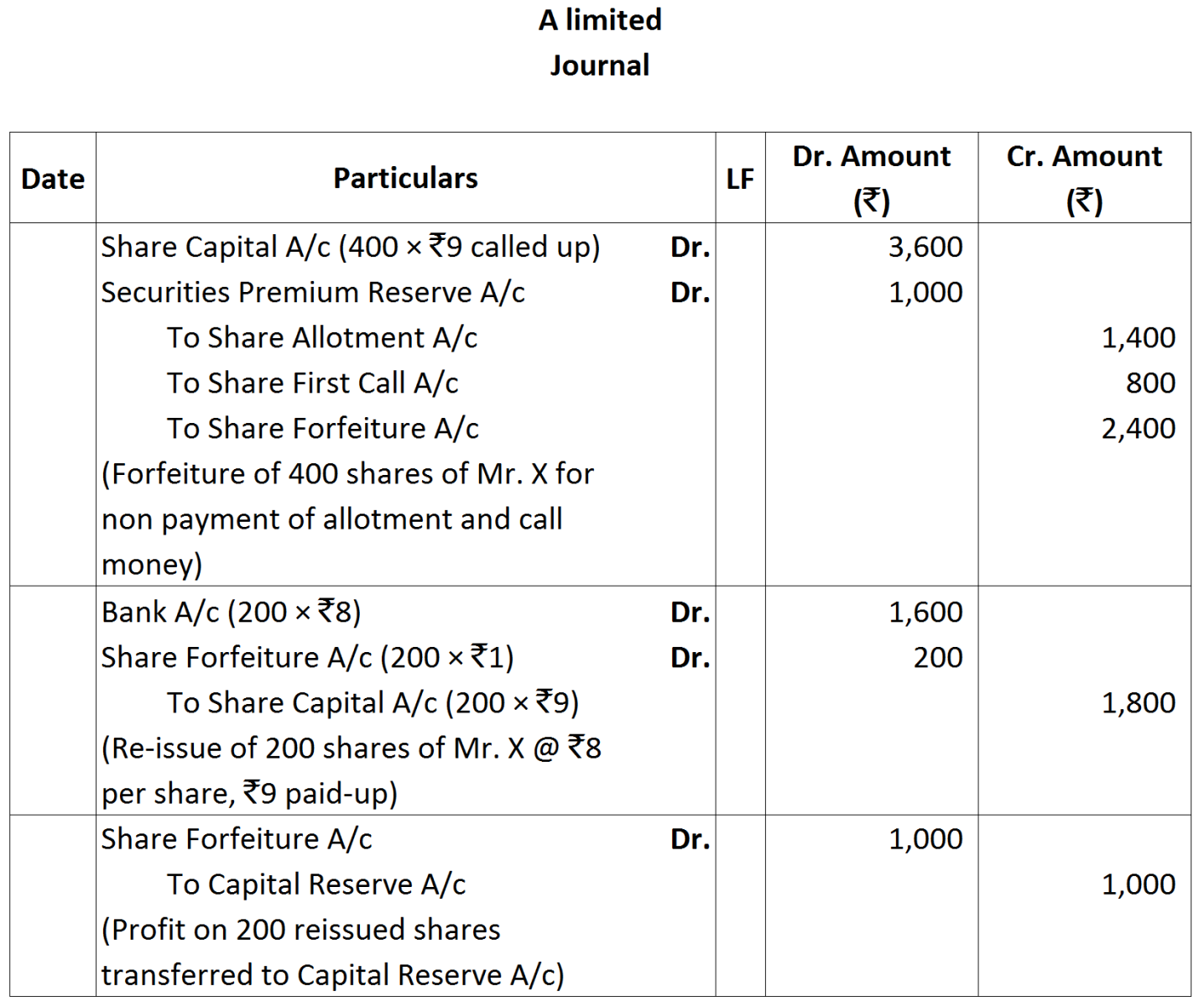

Question 14 Marks

The partnership between A & B was dissolved on March 31, 2005. Their capitals on that date were Rs. 1,70,000 and Rs. 30,000 respectively. Rs. 1,00,000 was owed by the firm to A, and B owed to the firm Rs. 20,000. Creditors on that date were Rs. 2,00,000. The assets realised Rs. 4,50,000 exclusive of what was owed by B. Find the profit or loss on realisation.

Answer

Working Notes :

View full question & answer→| Dr. | REALIZATION A/c | Cr. |

| Particulars | Amount (Rs.) | Particulars | Amount (Rs |

| Sundry Assets Bank-payment of creditors. |

4,80,000 2,00,000 |

Creditors Bank – assets realized Loss transferred to: A’s Capital 15,000 B’s Capital 15,000 |

2,00,000 4,50,000 30,000 |

| 6,80,000 | 6,80,000 |

| MEMORANDUM BALANCE SHEET As on 31.3.05 |

| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Capitals A 1,70,000 B 30,000 A’s loan Creditors |

2,00,000 1,00,000 2,00,000 |

B’s loan Sundry Assets (bal. fig.) |

20,000 4,80,000 |

| 5,00,000 | 5,00,000 |

Working Note:

Working Note: Alternate Answer

Alternate Answer

Notes of Account:

Notes of Account:

Note:

Note:

Working Notes:

Working Notes:

Working Note:

Working Note:

Notes to Account:

Notes to Account:

Notes to Accounts:

Notes to Accounts:

Working Notes:-

Working Notes:- Working Notes:

Working Notes:

Working Note:

Working Note:

Working Notes:

Working Notes:

Working Notes:

Working Notes:

Working Notes:

Working Notes: Values:

Values:

Working Notes:

Working Notes:

Working Notes:

Working Notes: