Question 14 Marks

Anirudh Ltd. has 4,000, 8% debentures of Rs. 100 each due for redemption on March 31, 2005. The company has a debenture redemption reserve of Rs. 1,50,000 on that date. Assuming that no interest is due record the necessary journal entries at the time of redemption of debentures.

Answer

View full question & answer→| JOURNAL OF ANIRUDH LTD. |

| Date | Particular | LF | Dr. | Cr. |

| P & L Appropriation A/c Debenture Redemption Reserve ( Debenture Redemption Reserve created) |

50,000 4,00,000 4,00,000 2,00,000 |

50,000 4,00,000 4,00,000 2,00,000 |

||

| Debenture A/c Debenture holders (Amount of Debentures due) |

||||

| Debenture holders Bank A/c (The amount of the debentures paid to the debenture holders) |

||||

| Debenture Redemption reserve General reserve (Debenture Redemption reserve transferred to general reserve) |

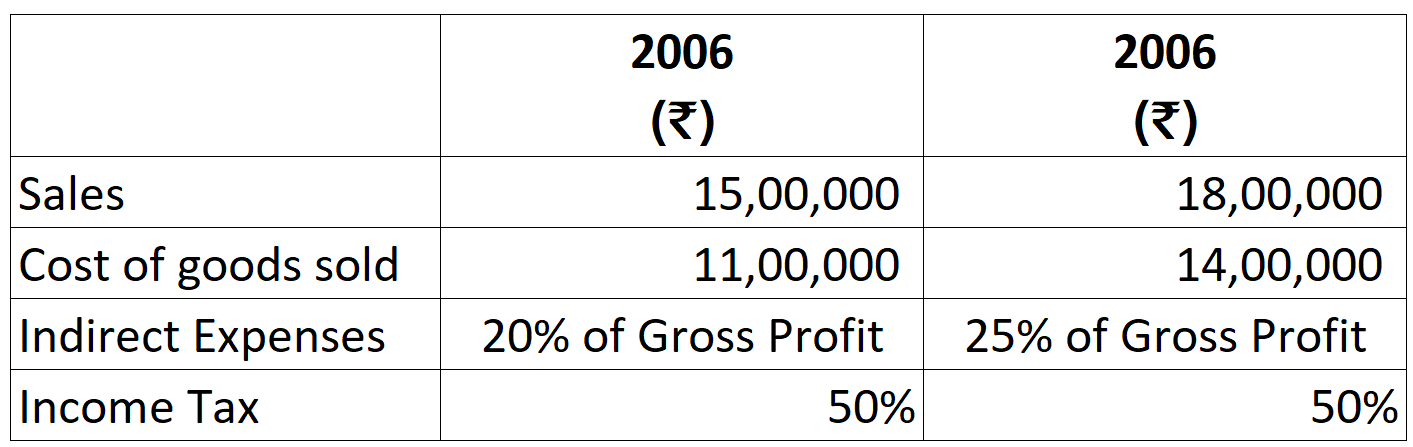

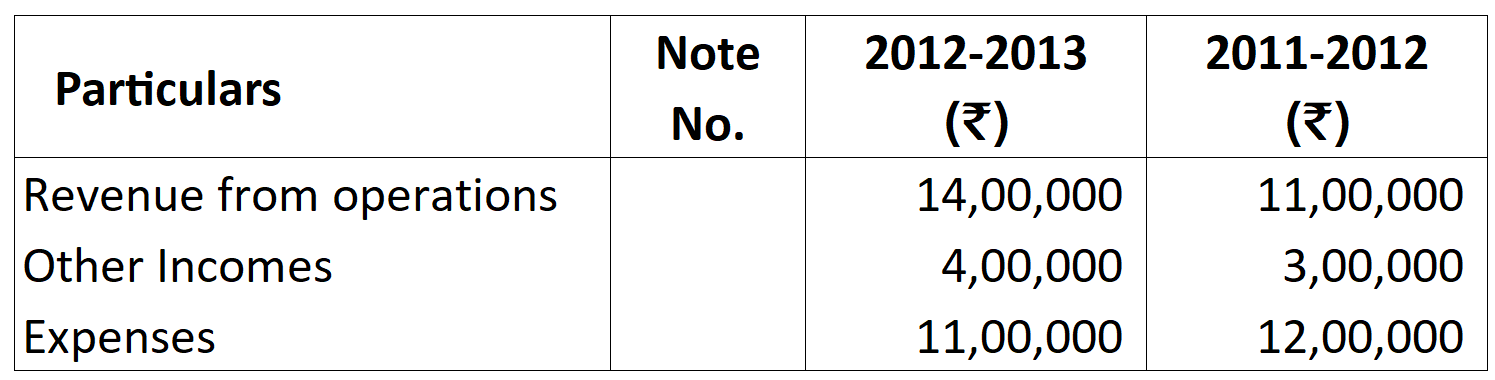

Values:

Values:

Interest on investments @ ₹ 50,000 and taxes payable @ 50%.

Interest on investments @ ₹ 50,000 and taxes payable @ 50%.

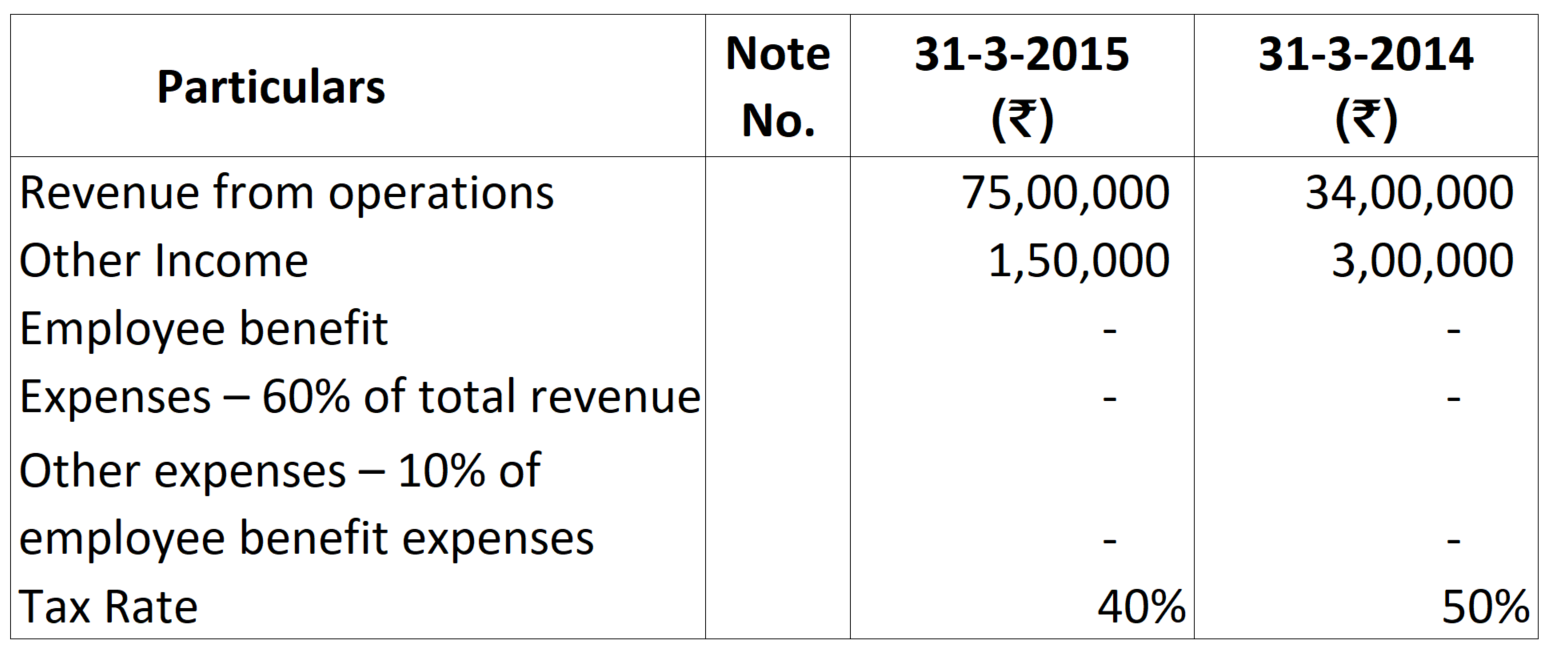

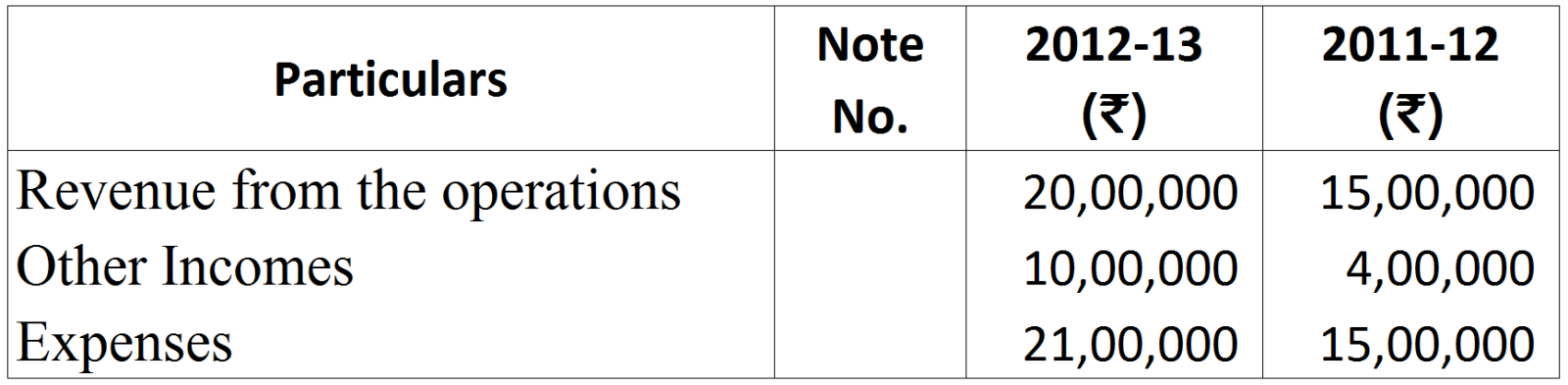

Values:

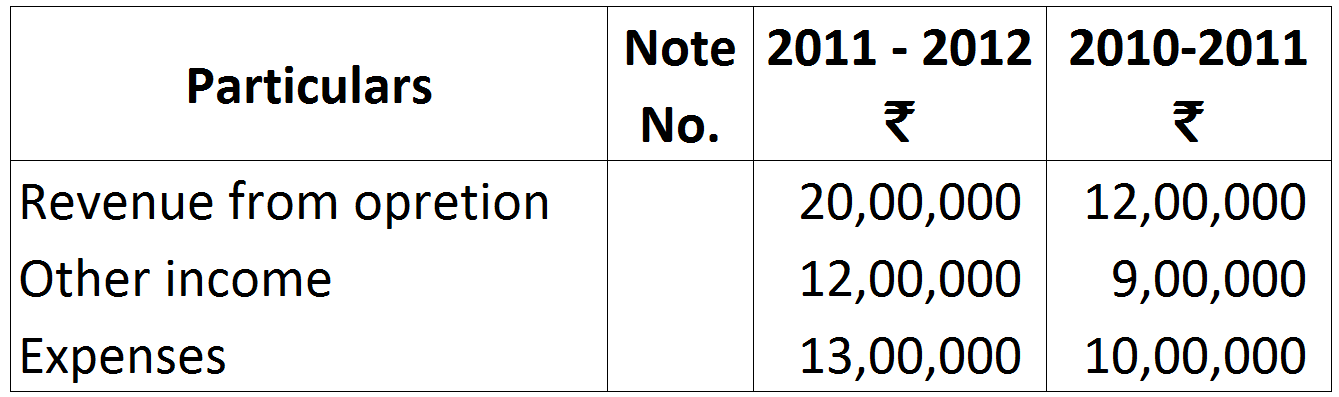

Values:

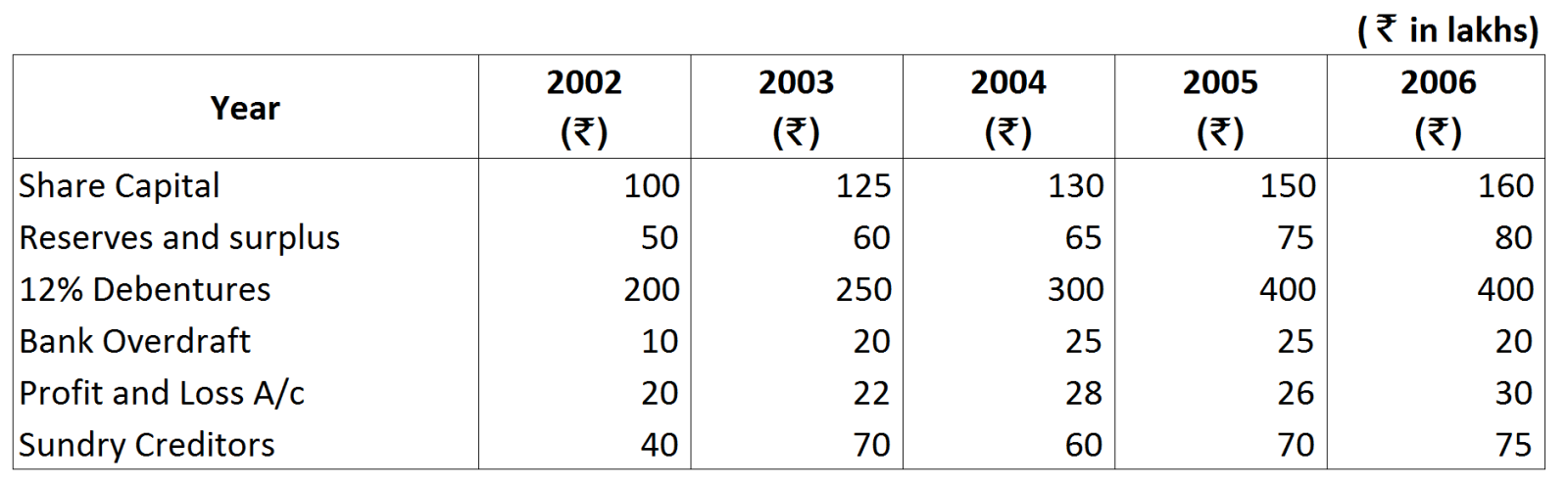

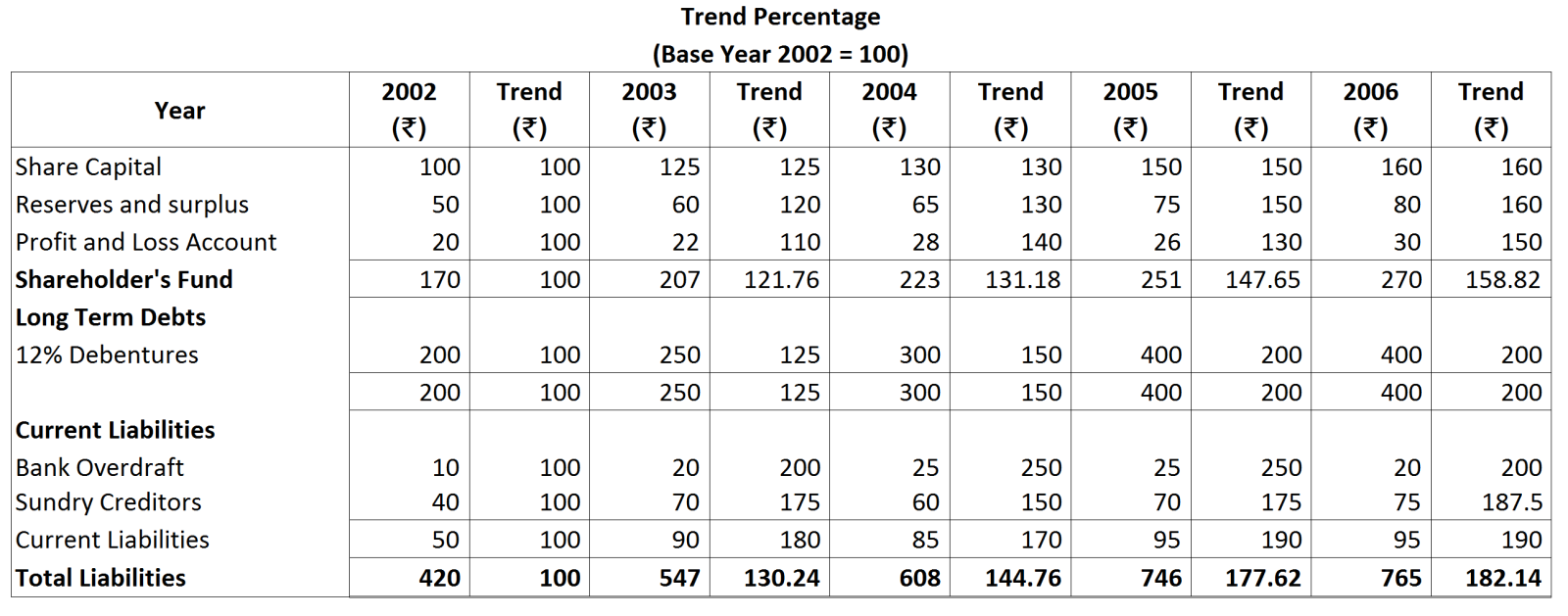

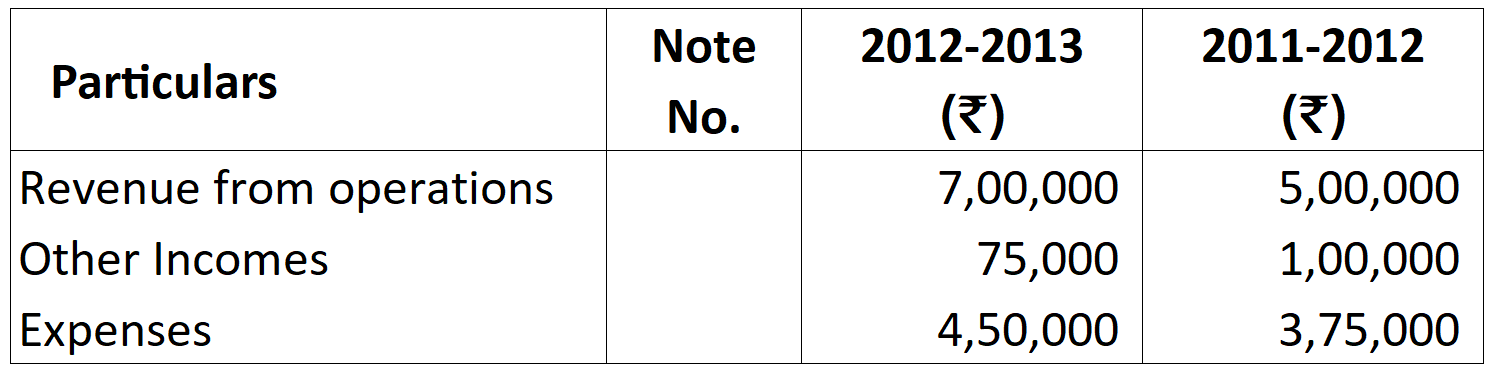

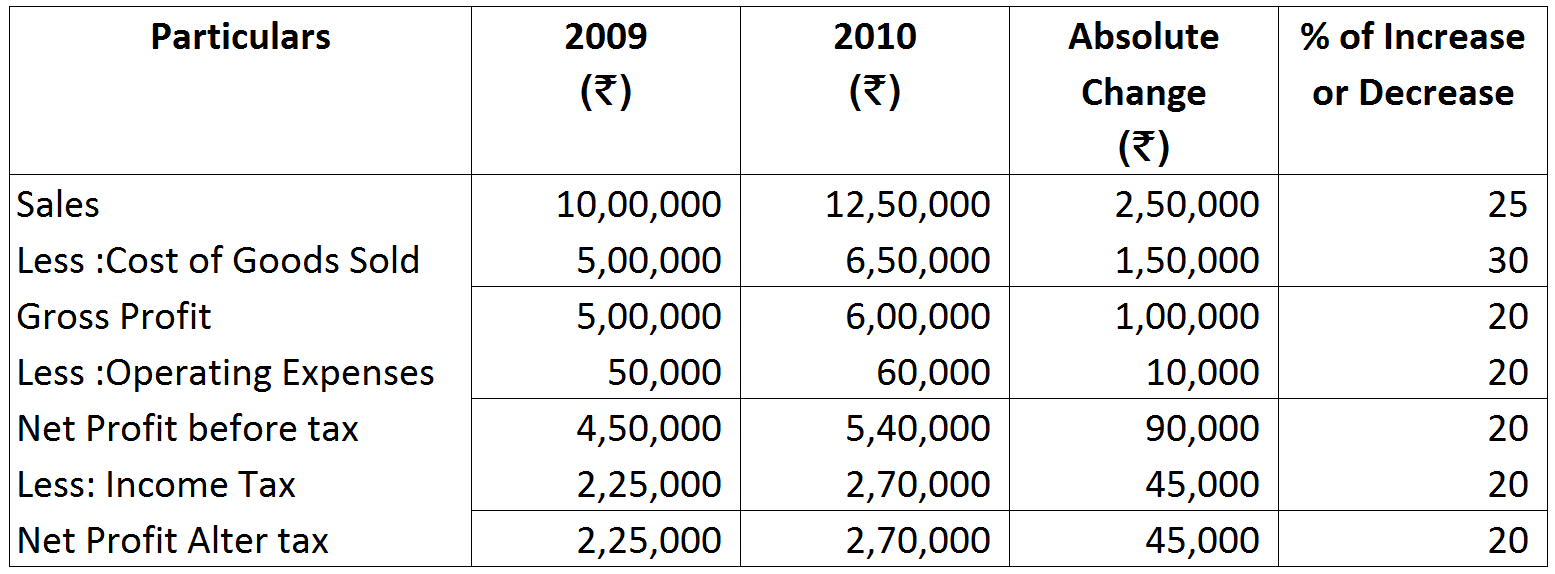

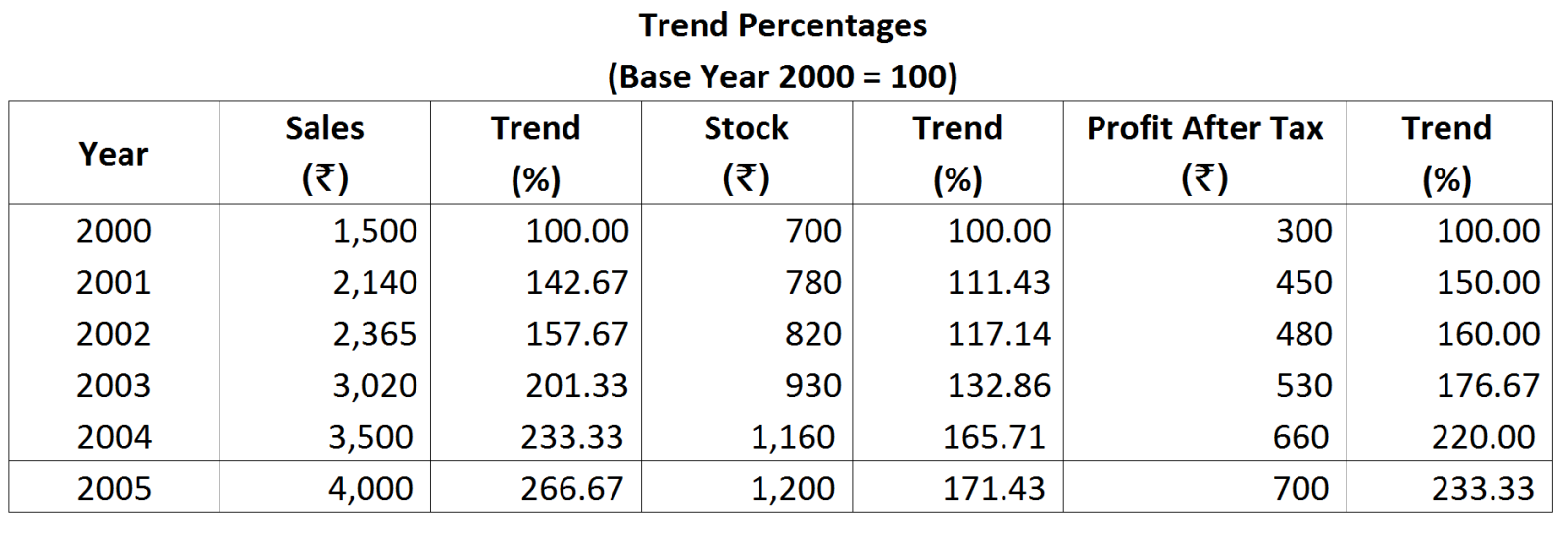

$\text{Trend Percentage}=\frac{\text{Present Year Value}}{\text{Base Year Value}}\times100$

$\text{Trend Percentage}=\frac{\text{Present Year Value}}{\text{Base Year Value}}\times100$