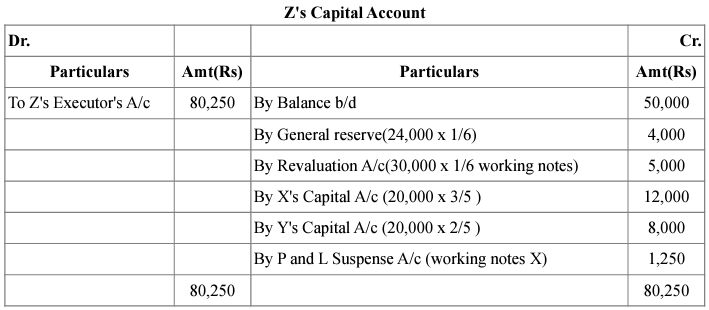

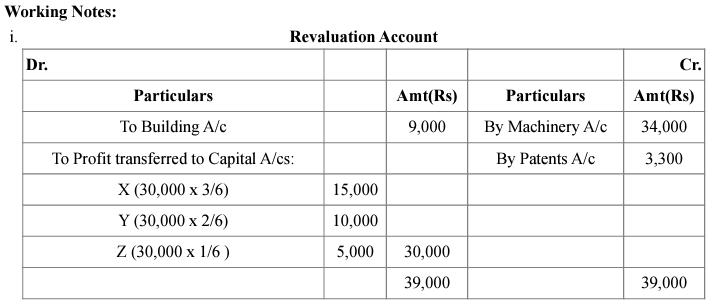

X, Y, and Z were partners sharing profits in the ratio 3 : 2 : 1. On 31st March 2008, their Balance Sheet stood as under :

| Liabilities | | Amt(Rs.) | Assets | Amt(Rs.) |

| Capitals: | | | Cash at Bank | 70,000 |

| X | 75,000 | | Investments | 50,000 |

| Y | 70,000 | | Patents | 15,000 |

| Z | 50,000 | 1,95,000 | Stock | 25,000 |

| Creditors | | 72,000 | Debtors | 20,000 |

| General Reserve | | 24,000 | Buildings | 75,000 |

| | | Machinery | 36,000 |

| | 2,91,000 | | 2,91,000 |

Z died on May 31st, 2008. It was agreed that

a. Goodwill was valued at 3 years' purchase of the average profits of the last five years, which were 2003: Rs. 40,000; 2004: Rs. 40,000; 2005: Rs. 30,000; 2006: Rs. 40,000 and 2007: Rs. 50,000.

b. Machinery was valued at Rs. 70,000, Patents at Rs. 20,000 and Buildings at Rs. 66,000.

c. For the purpose of calculating Z's share of profits until the date of death, it was agreed that the same be calculated based on the average profits for the last 2 years.

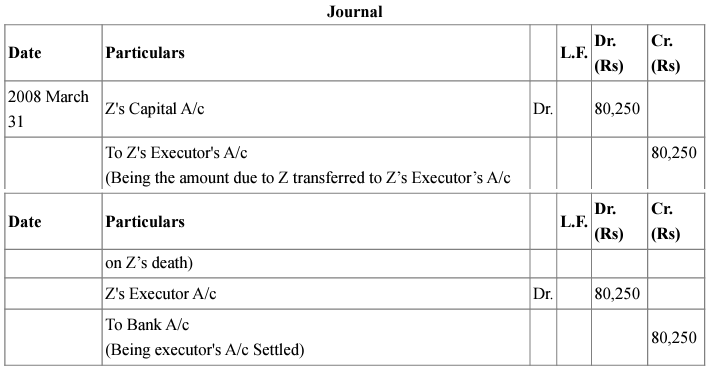

d. The executor of the deceased partner is to be paid the entire amount due by means of a cheque.

Prepare Z's Capital Accounts to be rendered to the executor and also a journal entry for the settlement of the amount due to Z's executor.