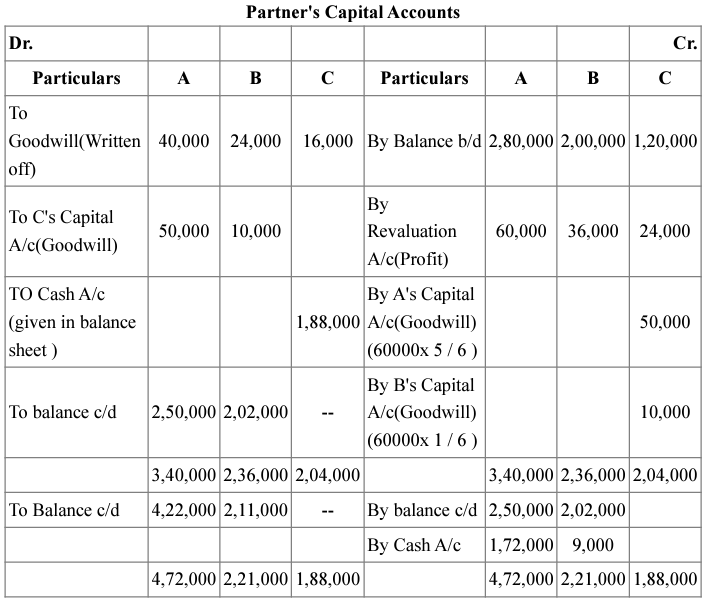

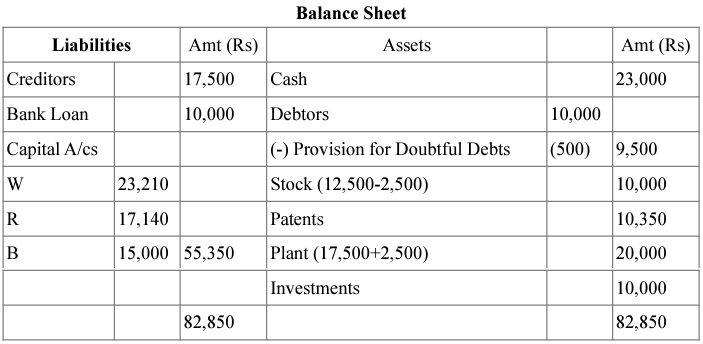

Anita, Gaurav and Sonu were partners in a firm sharing profits and losses in proportion to their capitals. Their Balance Sheet as at 31

st March, 2019 was as follows:

| Balance Sheet of Anita, Gaurav and Sonu as at 31st March, 2019 |

| Liabilities | Amount (₹) | Assets | Amount (₹) |

| Capitals: | | Land and Building | 5,00,000 |

| Anita | 2,00,000 | | Investments | 1,20,000 |

| Gaurav | 2,00,000 | | Debtors | 1,50,000 | |

| Sonu | 1,00,000 | 5,00,000 | Less: Provision for doubtful debts | 10,000 | 1,40,000 |

| Investment Fluctuation Fund | 40,000 | Stock | 1,00,000 |

| General Reserve | 30,000 | Cash at Bank | 1,70,000 |

| Creditors | 4,60,000 | | |

| | 10,30,000 | | 10,30,000 |

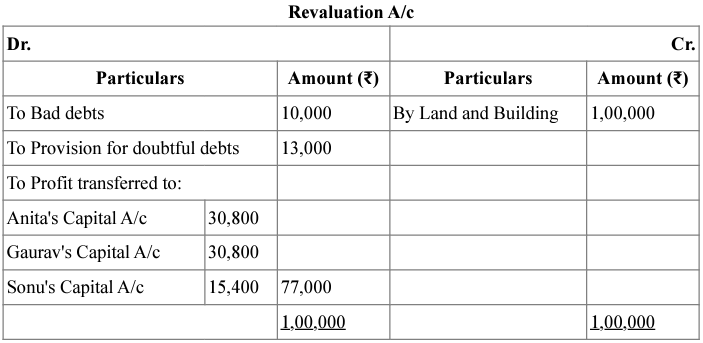

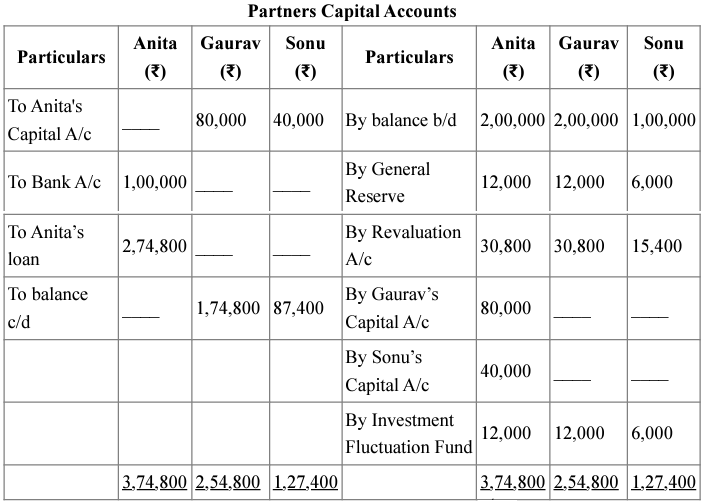

On the above date, Anita retired from the firm and the remaining partners decided to carry on the business. It was agreed to revalue the assets and reassess the liabilities as follows:

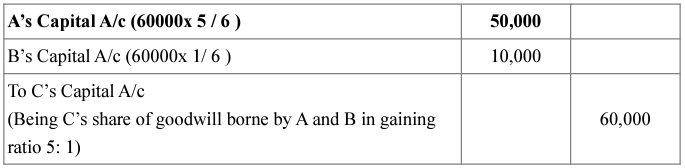

i. Goodwill of the firm was valued at ₹ 3,00,000 and Anita's share of goodwill was adjusted in the capital accounts of the remaining partners, Gaurav and Sonu

ii. Land and Building was to be brought up to 120% of its book value.

iii. Bad debts amounted to ₹ 20,000. A provision for doubtful debts was to be maintained at 10% on debtors.

iv. Market value of investments was ₹ 1,10,000.

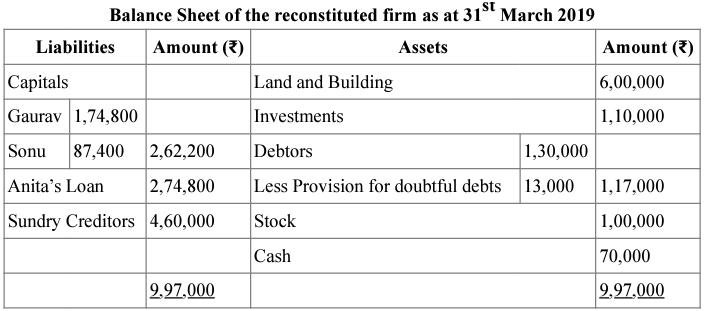

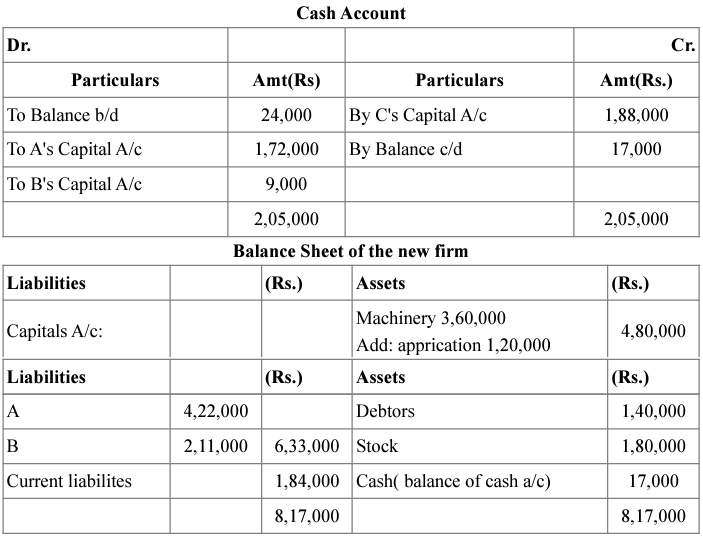

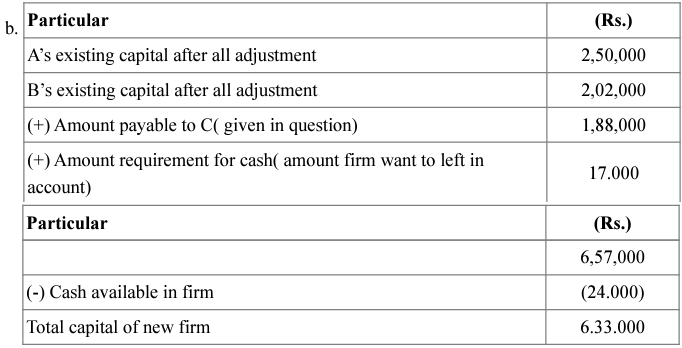

v. ₹ 1,00,000 was paid immediately by cheque to Anita out of the amount due and the balance was to be transferred to her loan account which was to be paid in two equal annual instalments along with interest @ 10% p.a

Prepare the Revaluation Account, Partners' Capital Accounts and the Balance Sheet of the reconstituted firm on Anita's retirement.