Question 12 Marks

Differentiate between normal profit and supernormal profit under a Perfectly Competitive market.

Answer

View full question & answer→Normal Profit : It is the minimum level of profit required to keep a firm in operation in the long run. It occurs when Total Revenue (TR) is equal to Total Cost (TC) or Price (P) equals Average Cost (AC). In economics, normal profit is considered a part of implicit costs.

Supernormal Profit : It is any profit earned over and above the normal profit. It occurs when Total Revenue (TR) is greater than Total Cost (TC) or Price (P) is greater than Average Cost ( AC). This usually happens in the short run under perfect competition.

Supernormal Profit : It is any profit earned over and above the normal profit. It occurs when Total Revenue (TR) is greater than Total Cost (TC) or Price (P) is greater than Average Cost ( AC). This usually happens in the short run under perfect competition.

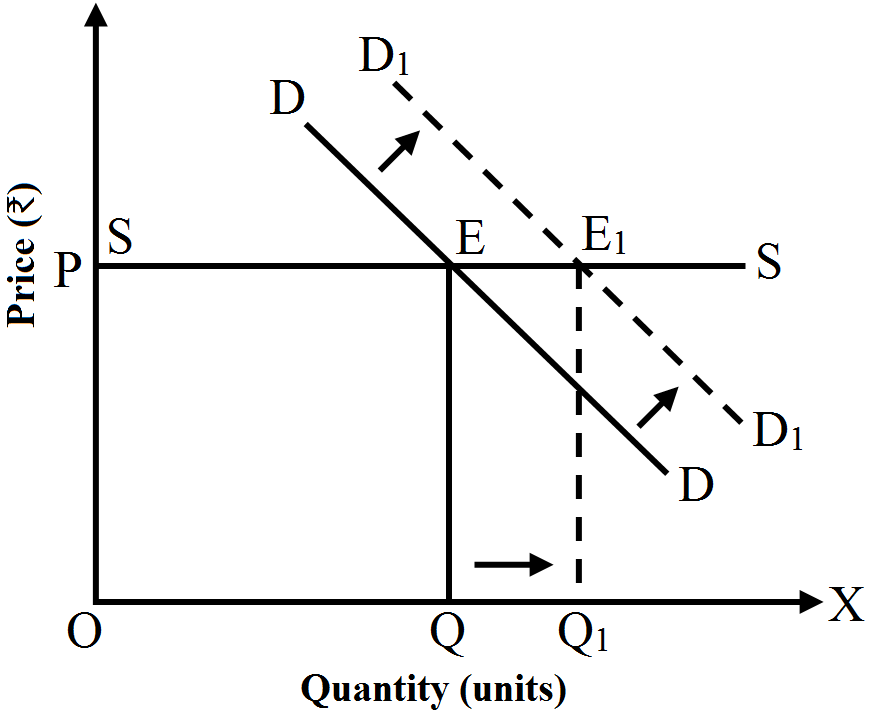

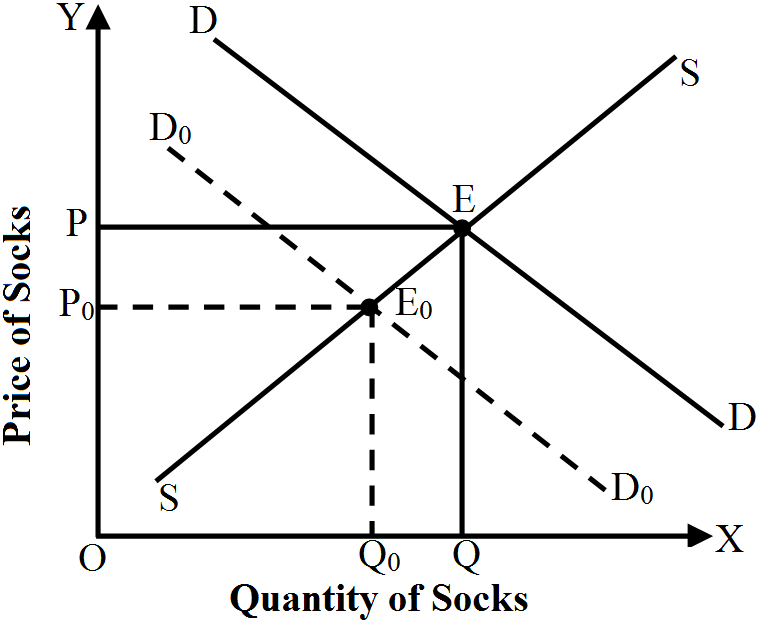

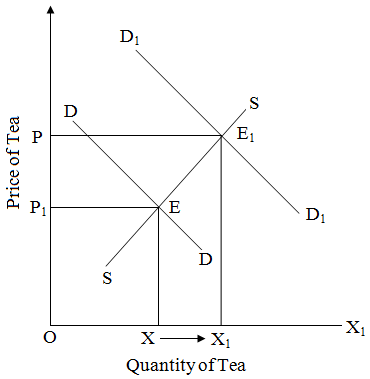

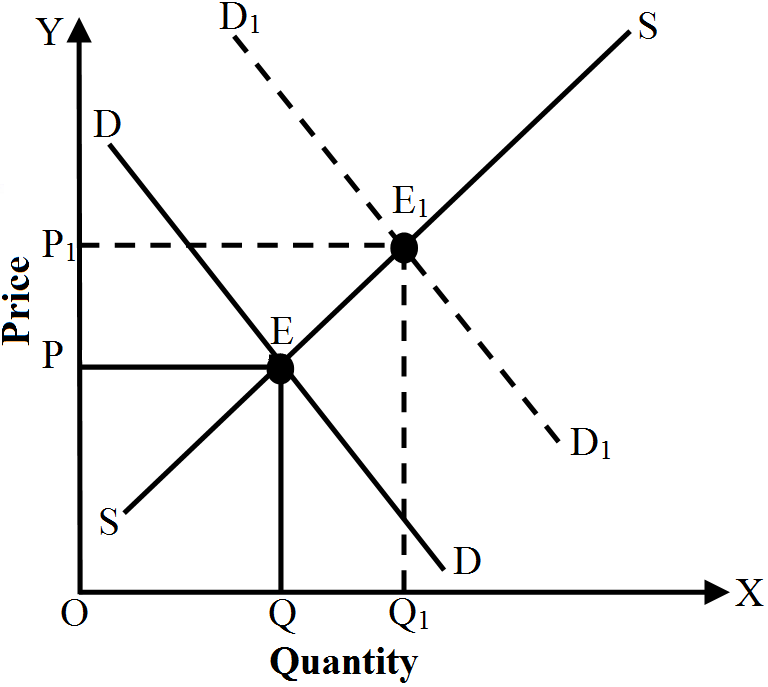

It is clear from the diagram that as a result of decrease in demand, the demand curve will shift leftwards. The equilibrium price falls from OP to OP0 and the equilibrium quantity also falls from OQ to OQ0.

It is clear from the diagram that as a result of decrease in demand, the demand curve will shift leftwards. The equilibrium price falls from OP to OP0 and the equilibrium quantity also falls from OQ to OQ0.

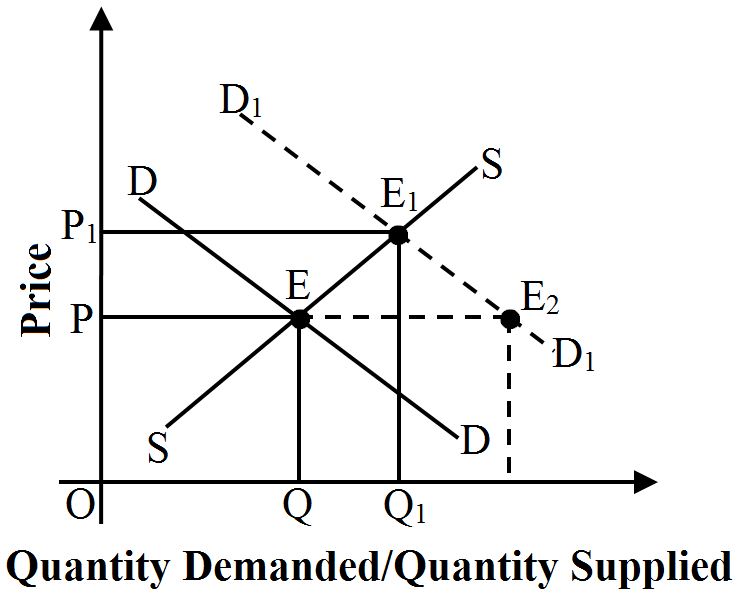

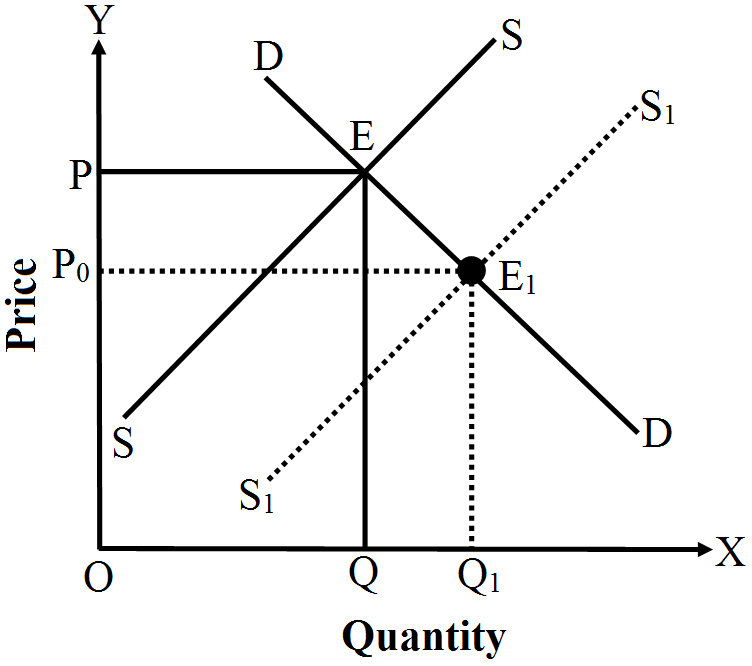

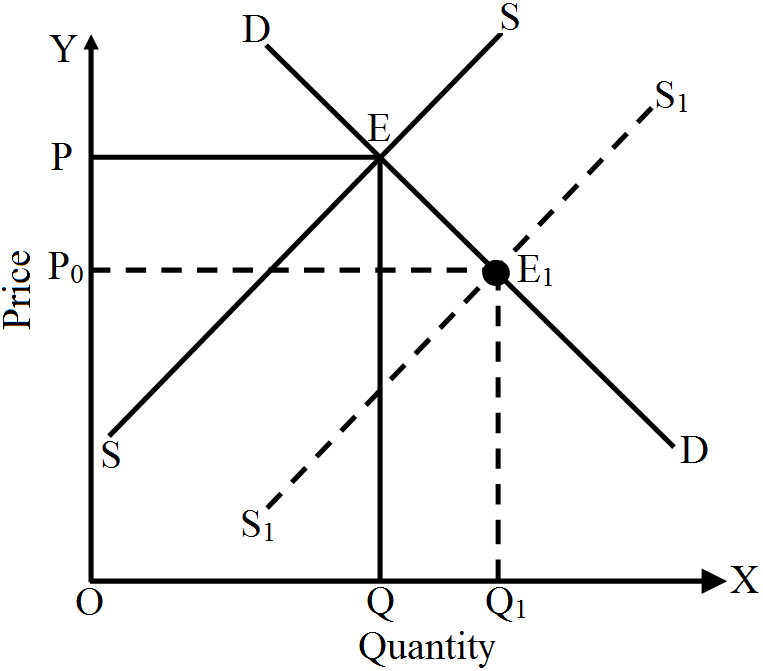

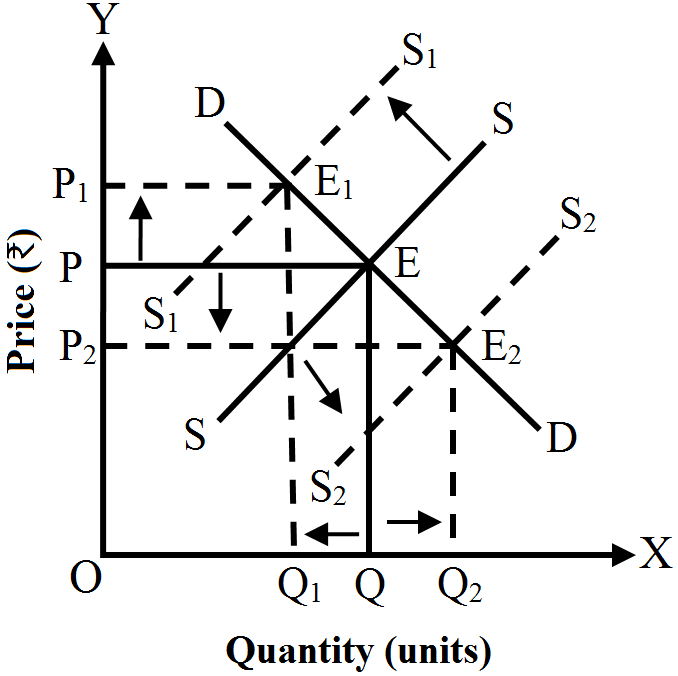

DD is initial demand curve, SS is initial supply curve, OP is initial equilibrium price, OQ is initial equilibrium quantity. Due to increase in supply, supply curve shifts to the right shown by S2S2 and equilibrium price falls to OP2. With a fall in supply, shown by S1S1 equilibrium price rises to OP1.

DD is initial demand curve, SS is initial supply curve, OP is initial equilibrium price, OQ is initial equilibrium quantity. Due to increase in supply, supply curve shifts to the right shown by S2S2 and equilibrium price falls to OP2. With a fall in supply, shown by S1S1 equilibrium price rises to OP1.