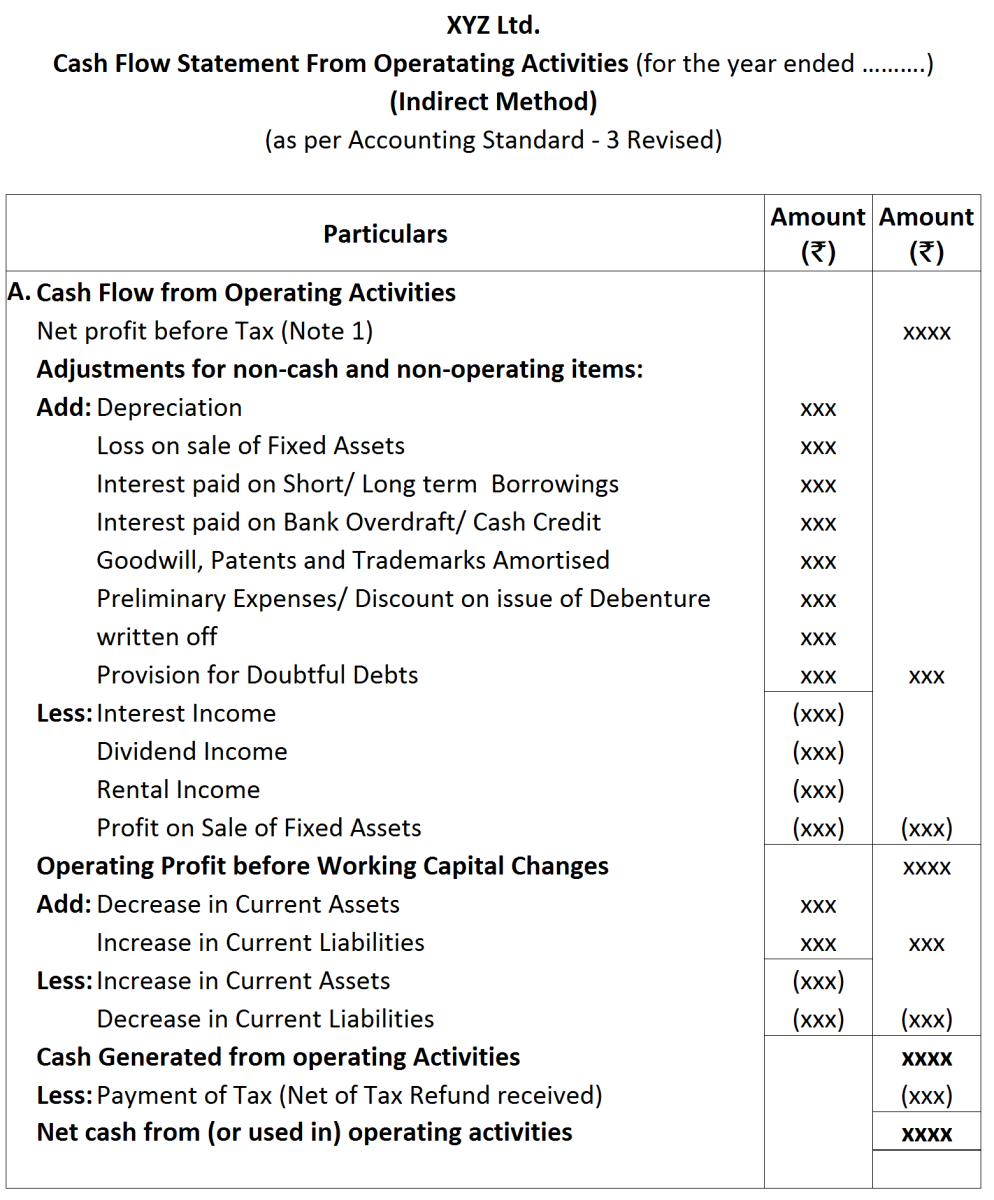

Question

Describe “Indirect” method of ascertaining Cash Flow from operating activities.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

Cost of Revenue

|

₹

|

|

From Operation (Cost of Goods Sold).

|

52,000

|

|

Operating Expenses.

|

18,000

|

| Revenue from Operation | |

| Gross Sales. | 88,000 |

| Sales Return. | 8,000 |