Question 13 Marks

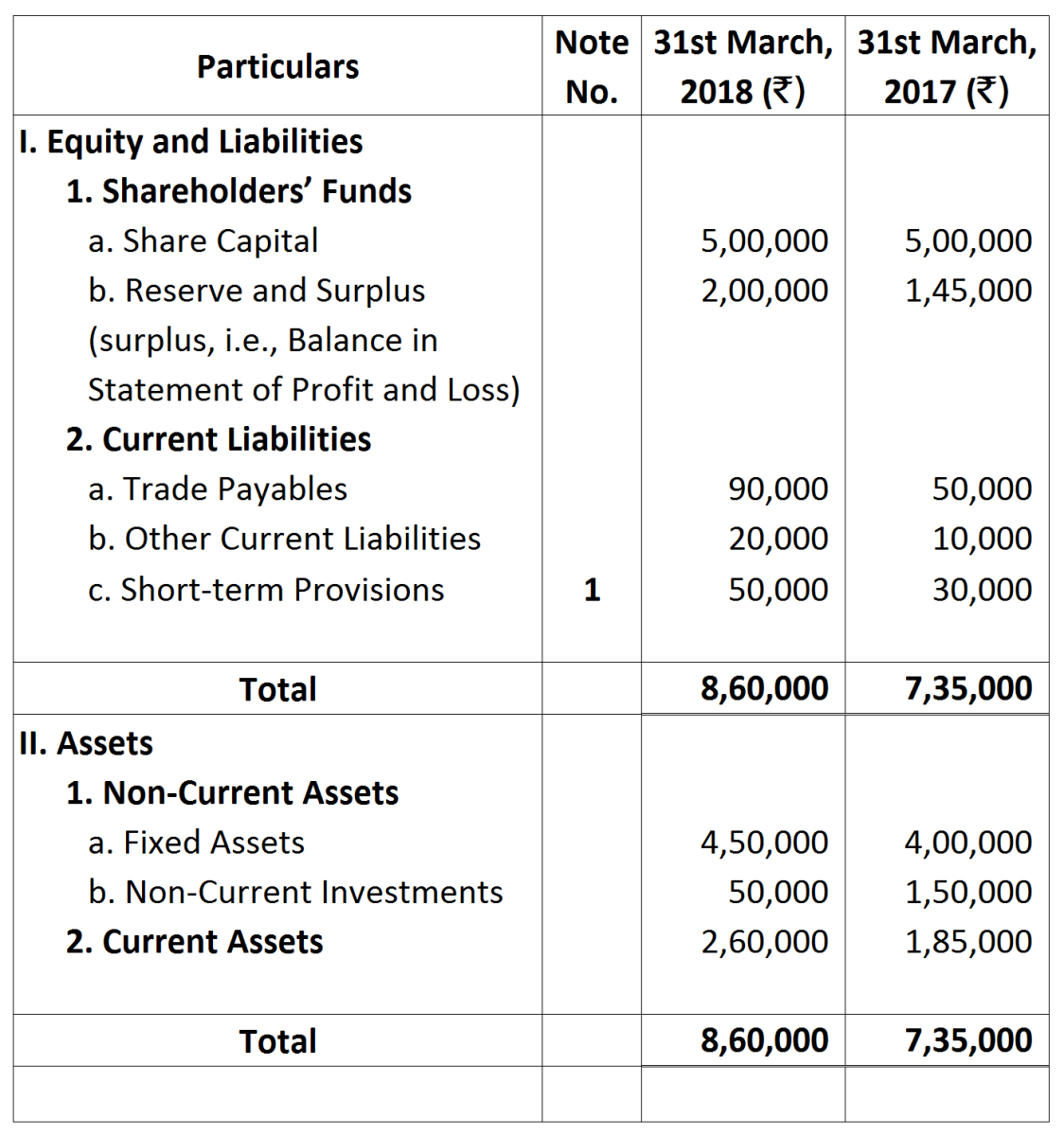

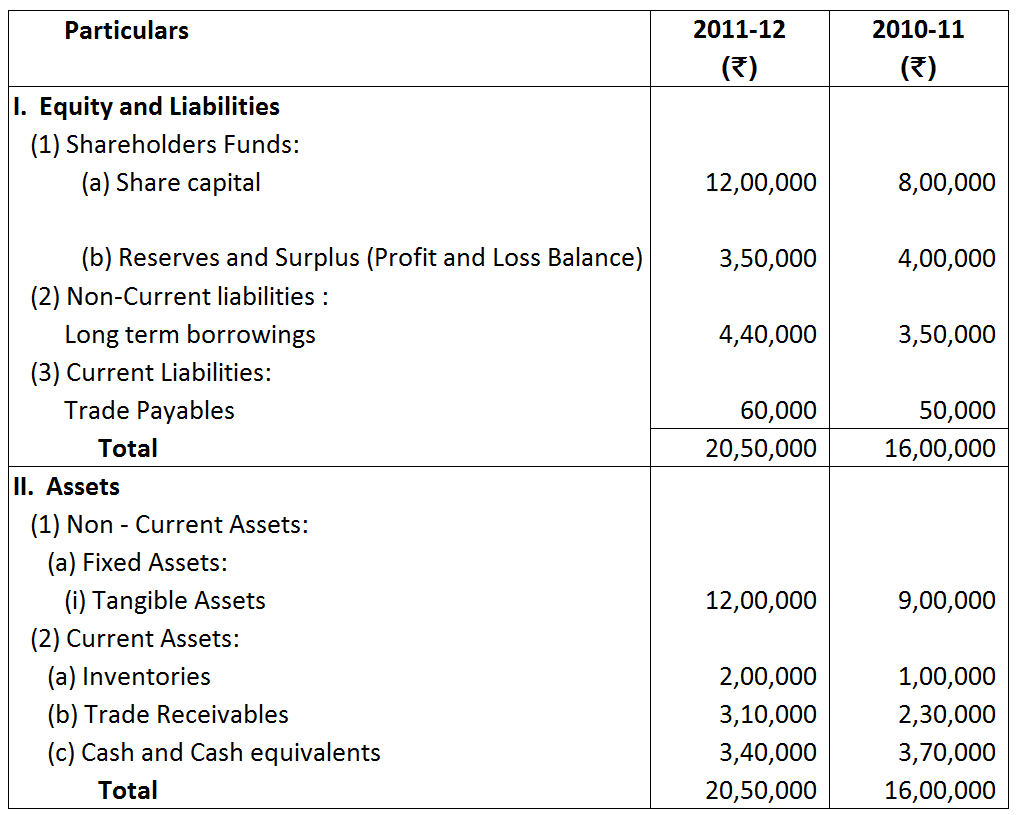

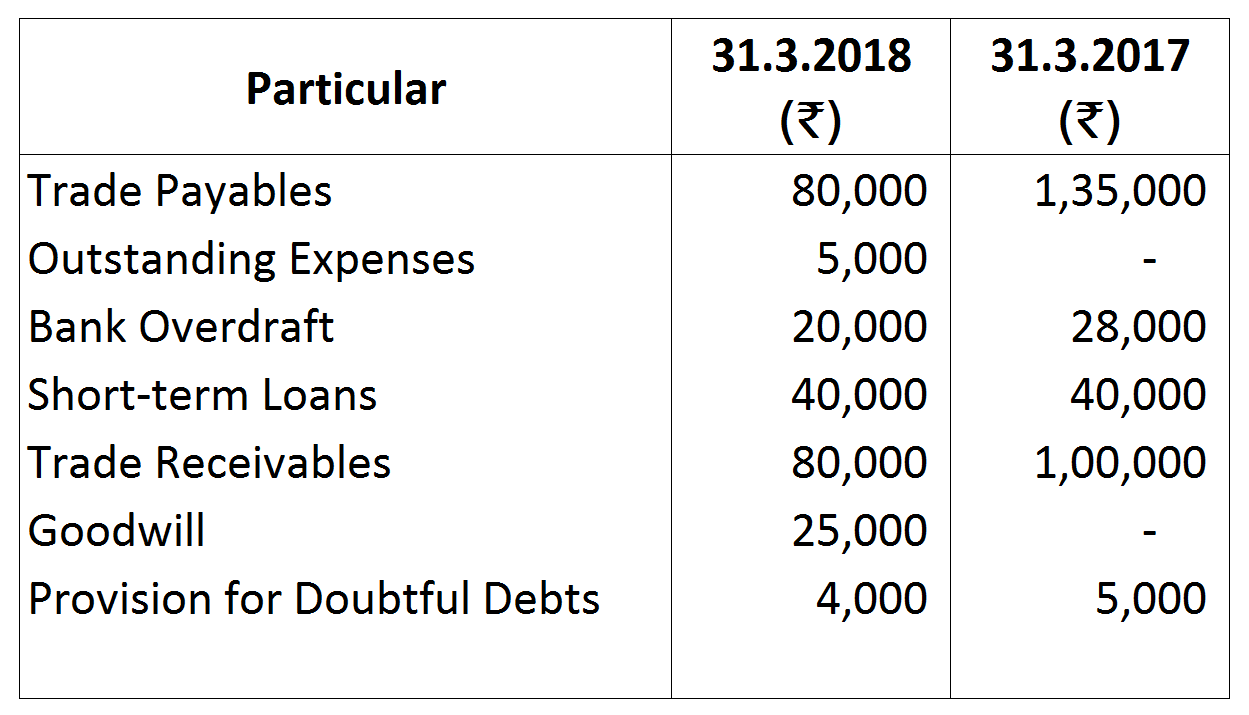

Following are the Balance Sheets of Krishtec ltd. for the year ended $31^{st}$ March $2011$ and $2012$:

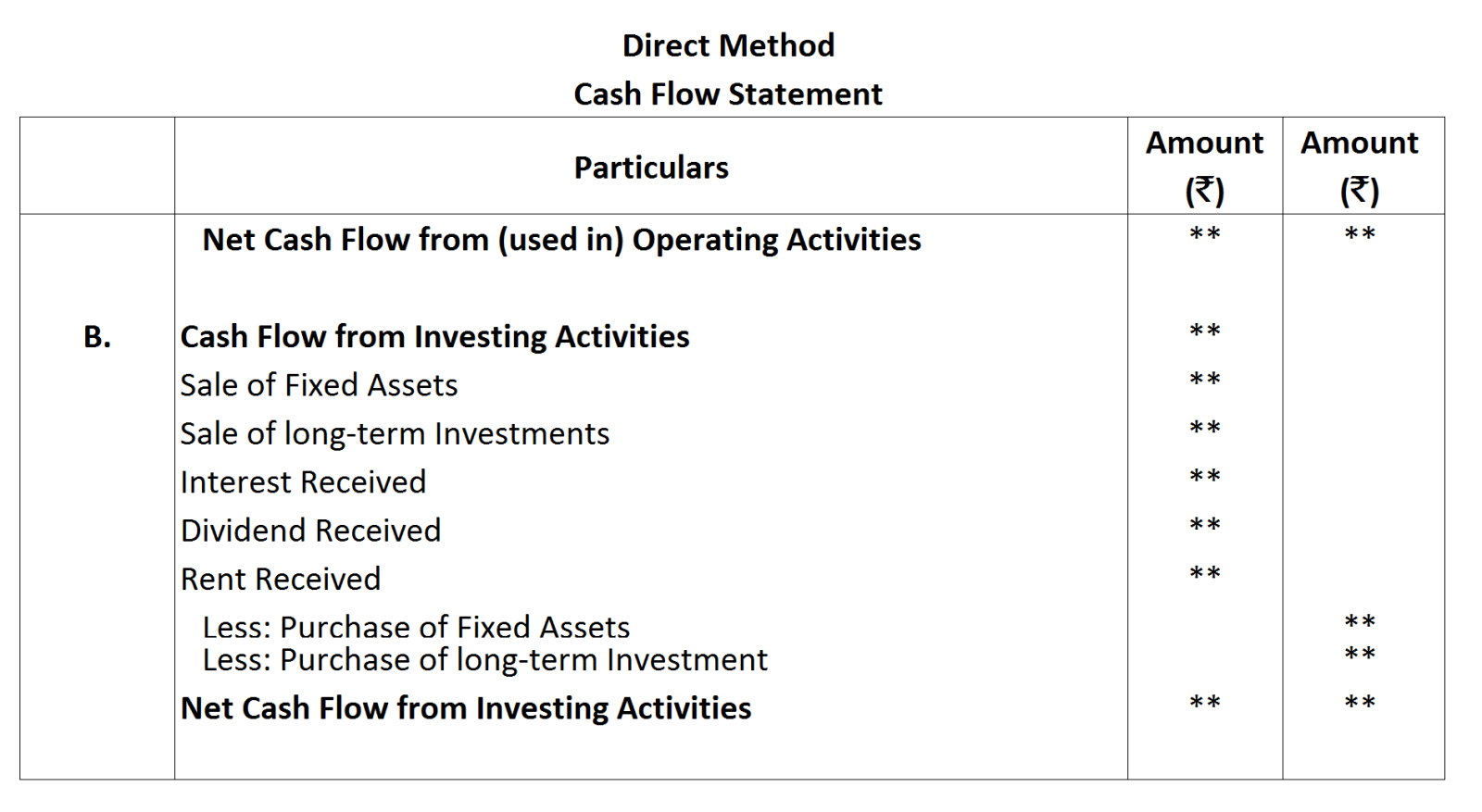

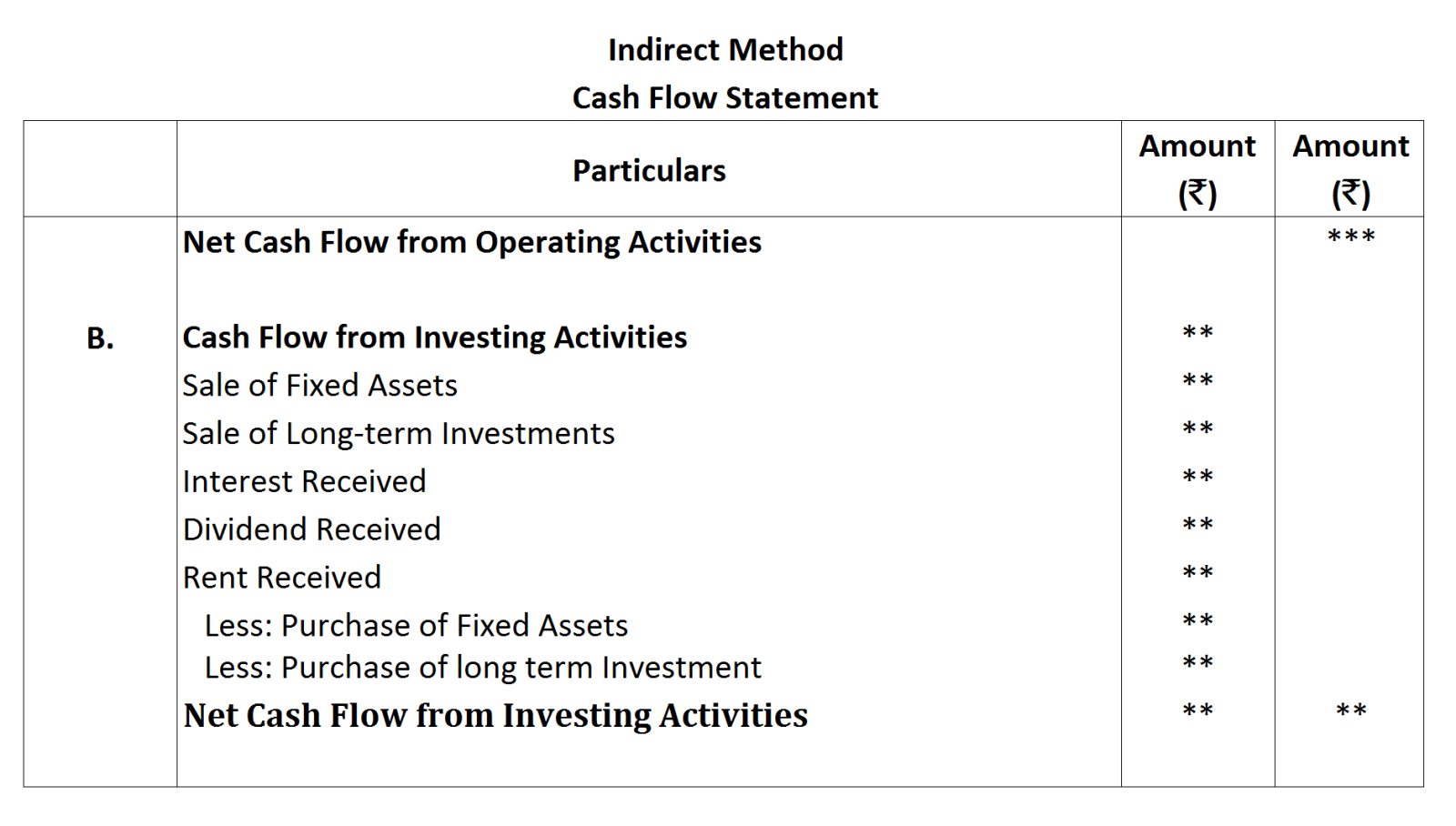

Prepare a Cash Flow Statement after taking into account the following adjustments:

View full question & answer→Prepare a Cash Flow Statement after taking into account the following adjustments:

- "The company paid interest ₹ $36,000$ on its long term borrowings.

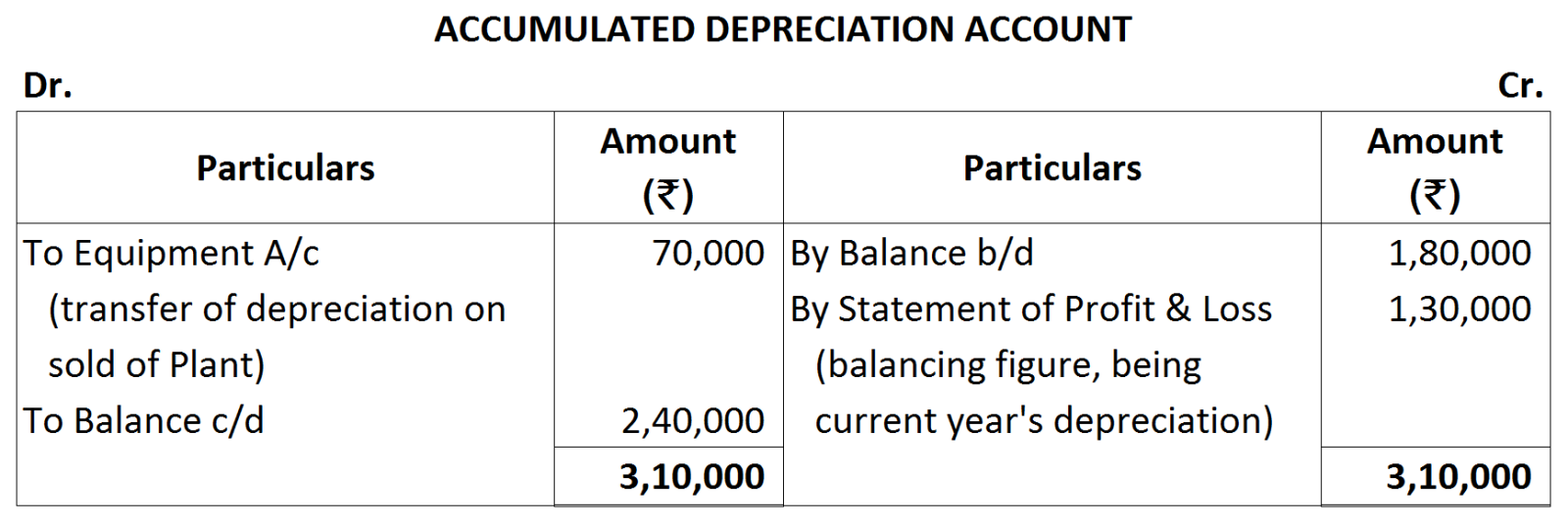

- Depredation charged on tangible fixed assets was ₹ $1,20,000$.

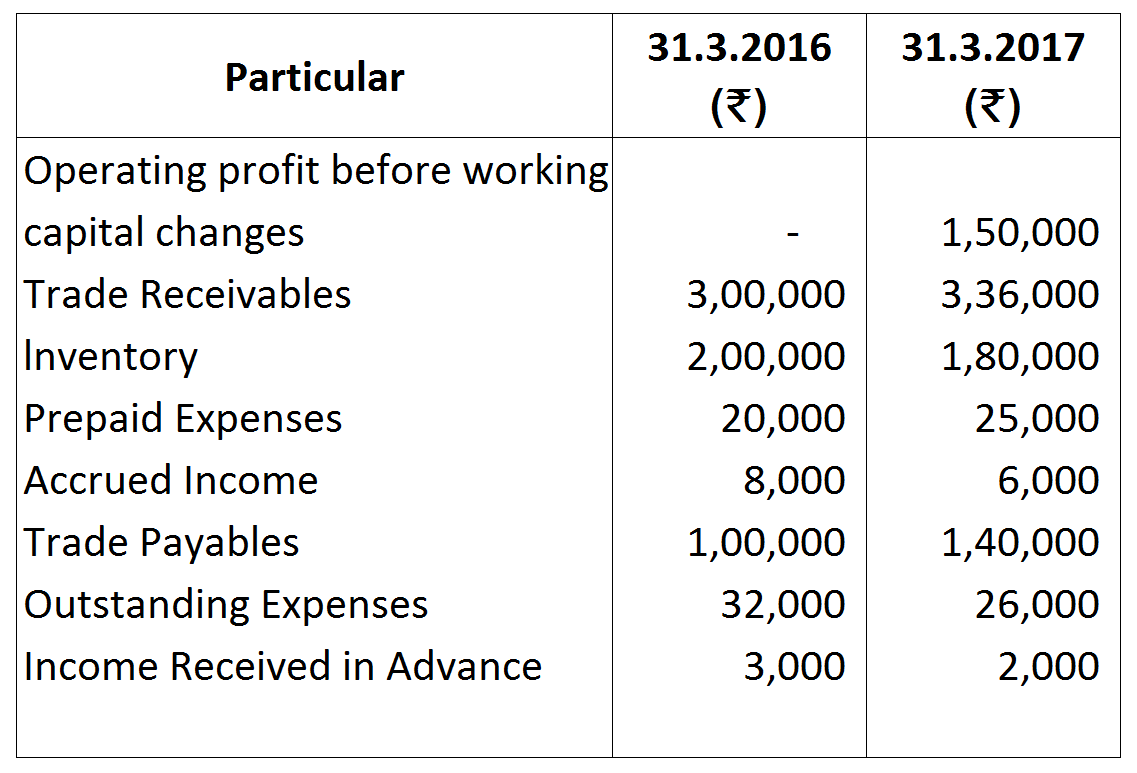

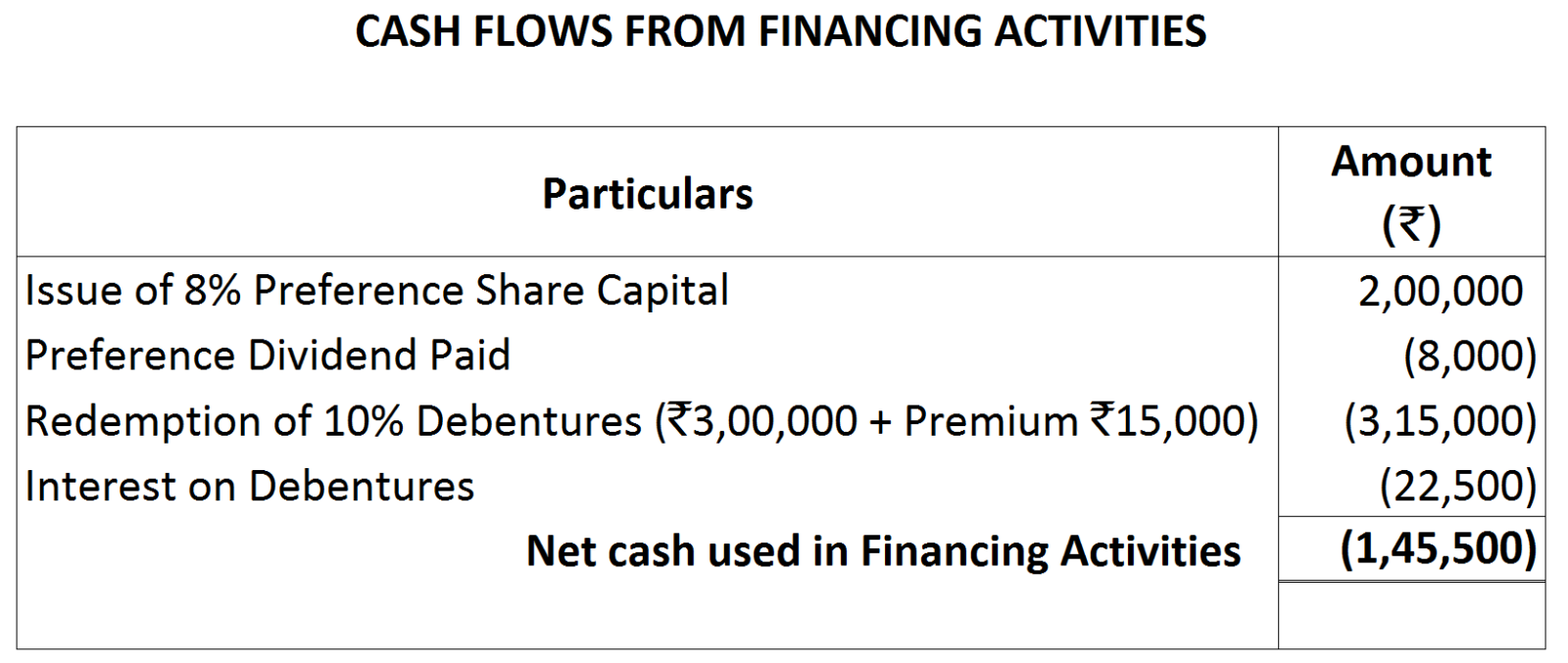

Working Note:

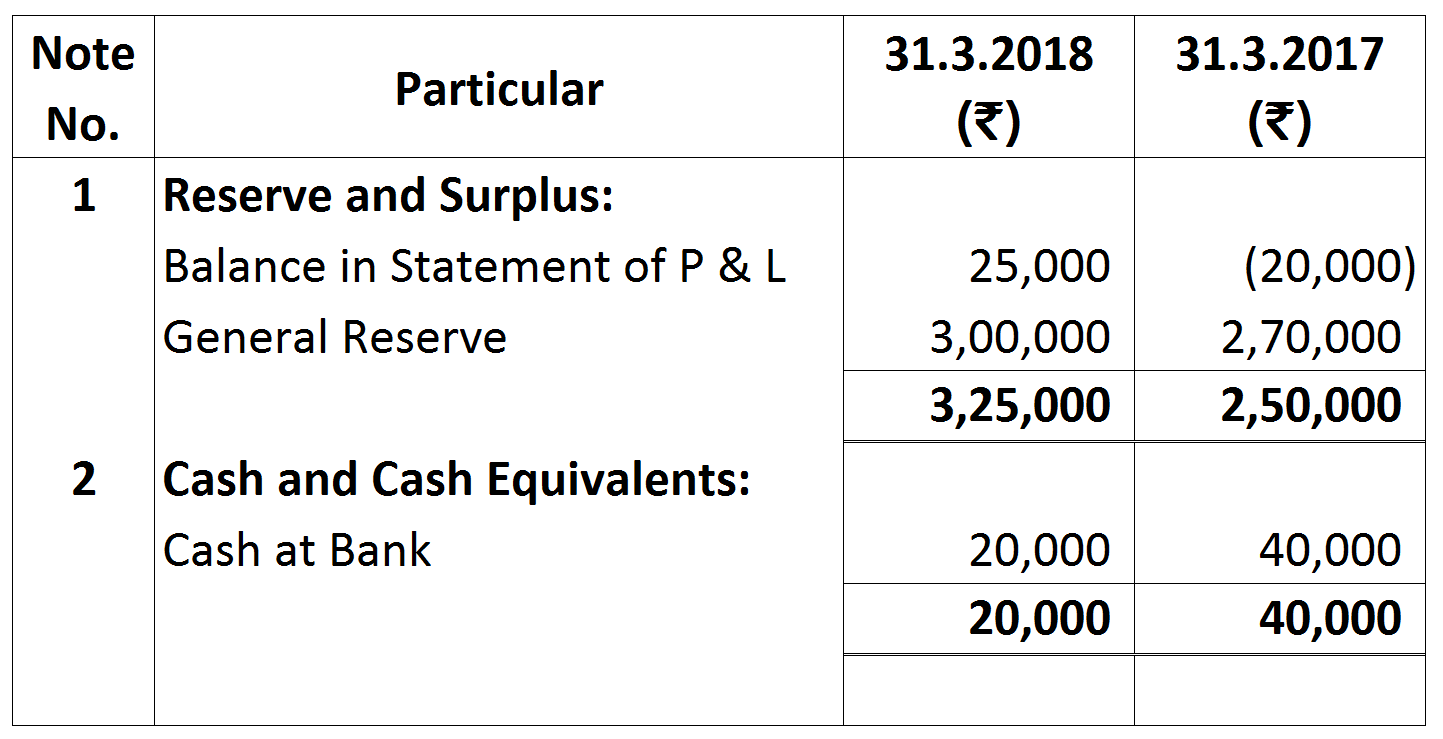

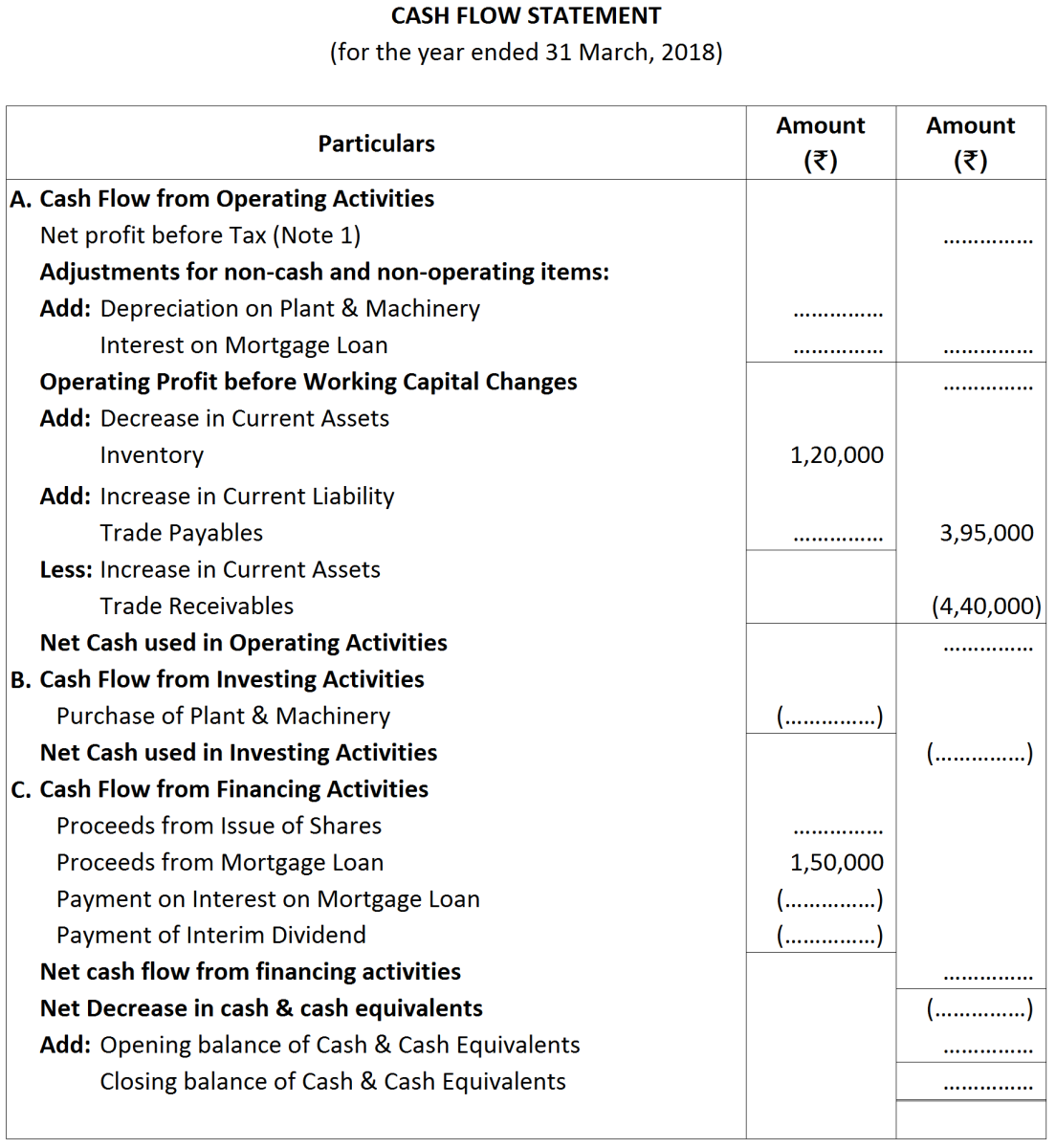

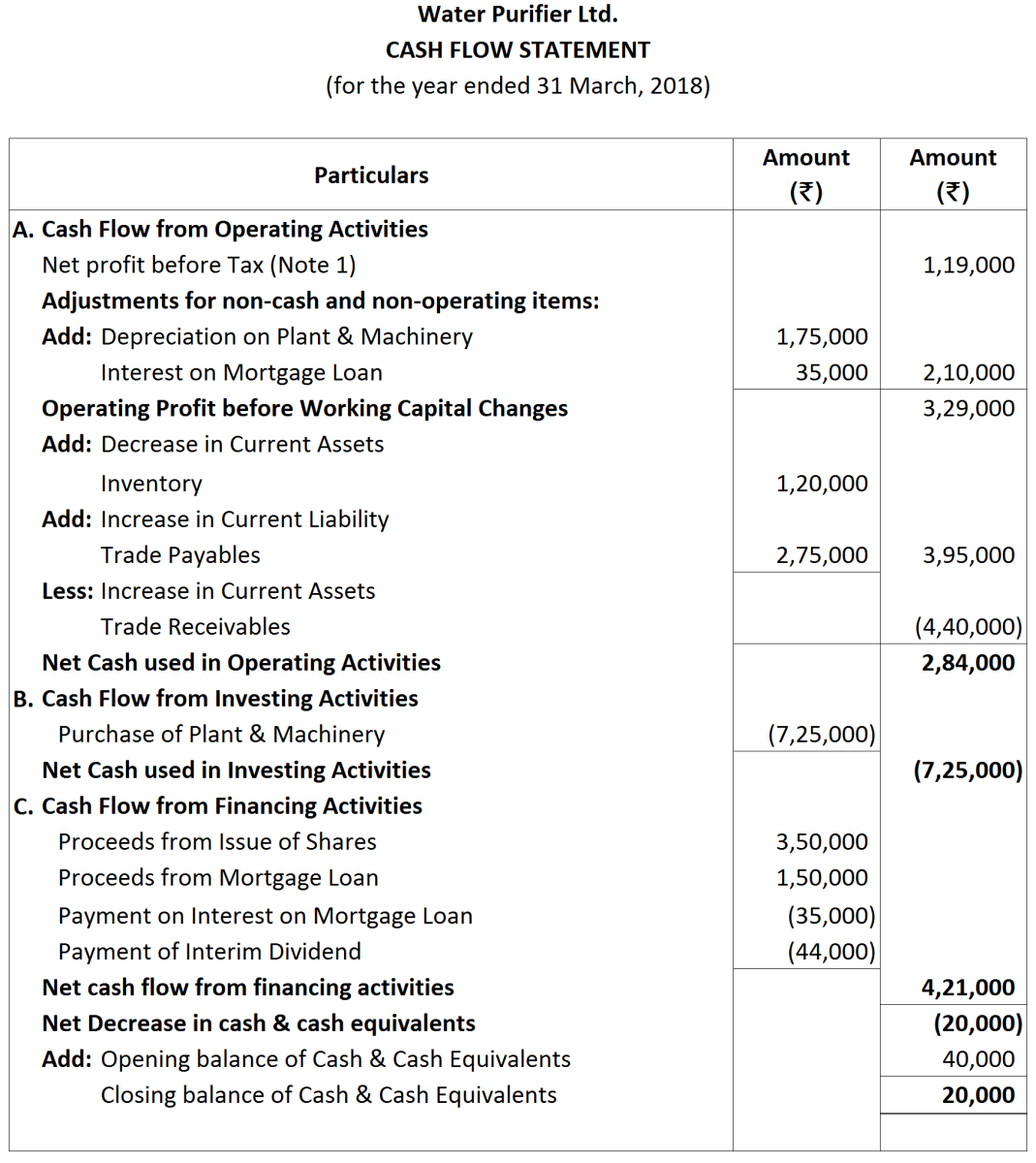

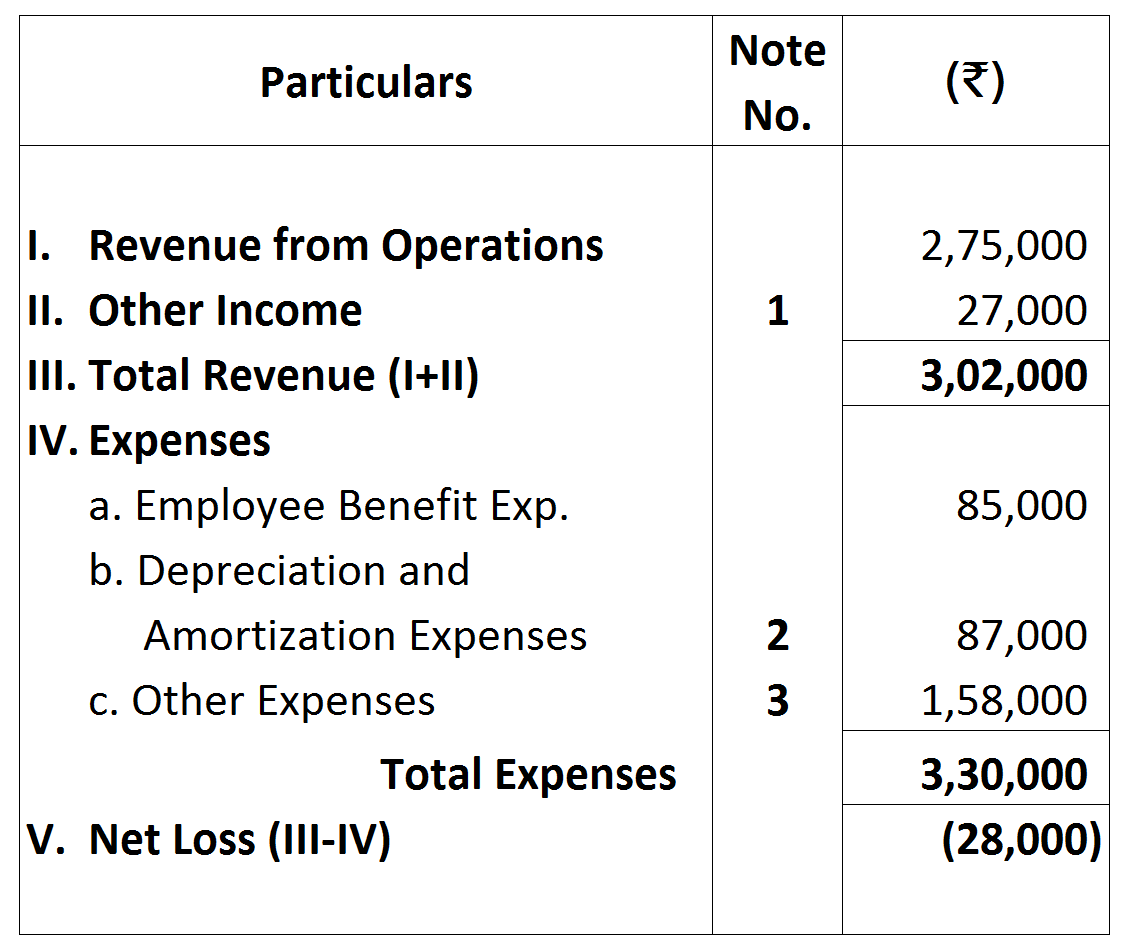

Working Note: * Net Cash Flow from financing activities ₹ 4,21,000 is the balancing figure of Cash Flow Statment.

* Net Cash Flow from financing activities ₹ 4,21,000 is the balancing figure of Cash Flow Statment.

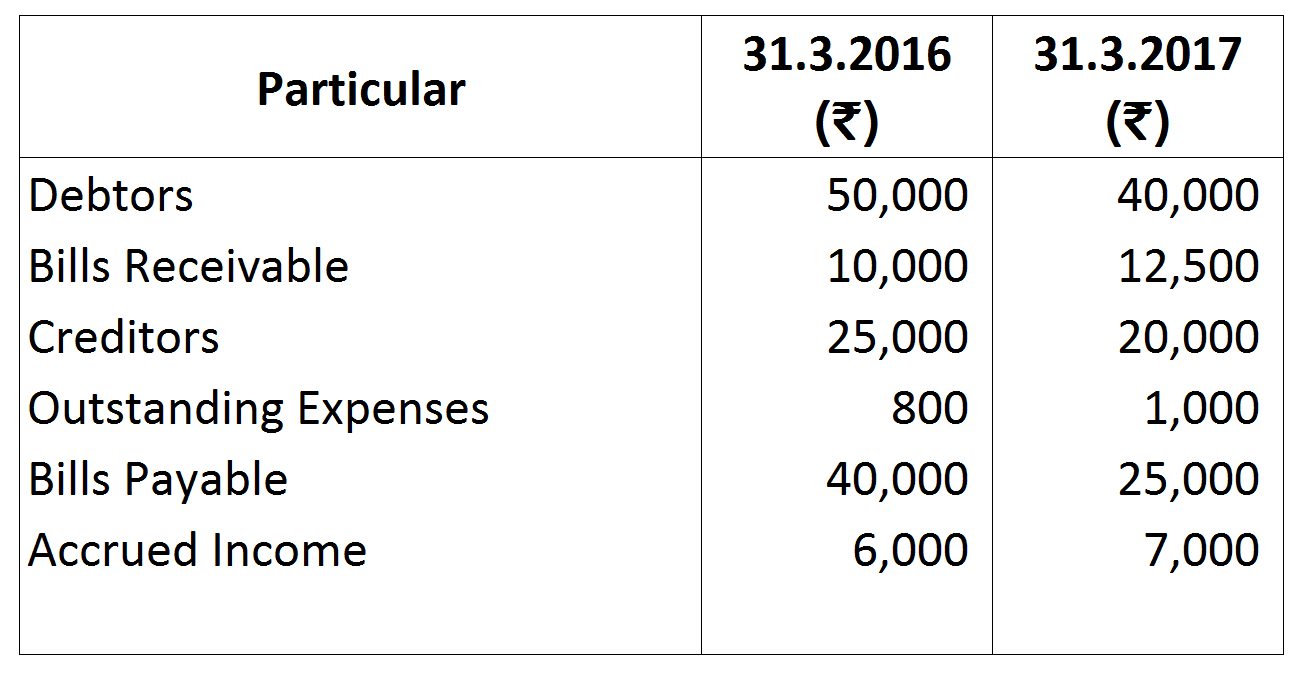

Note:

Note:

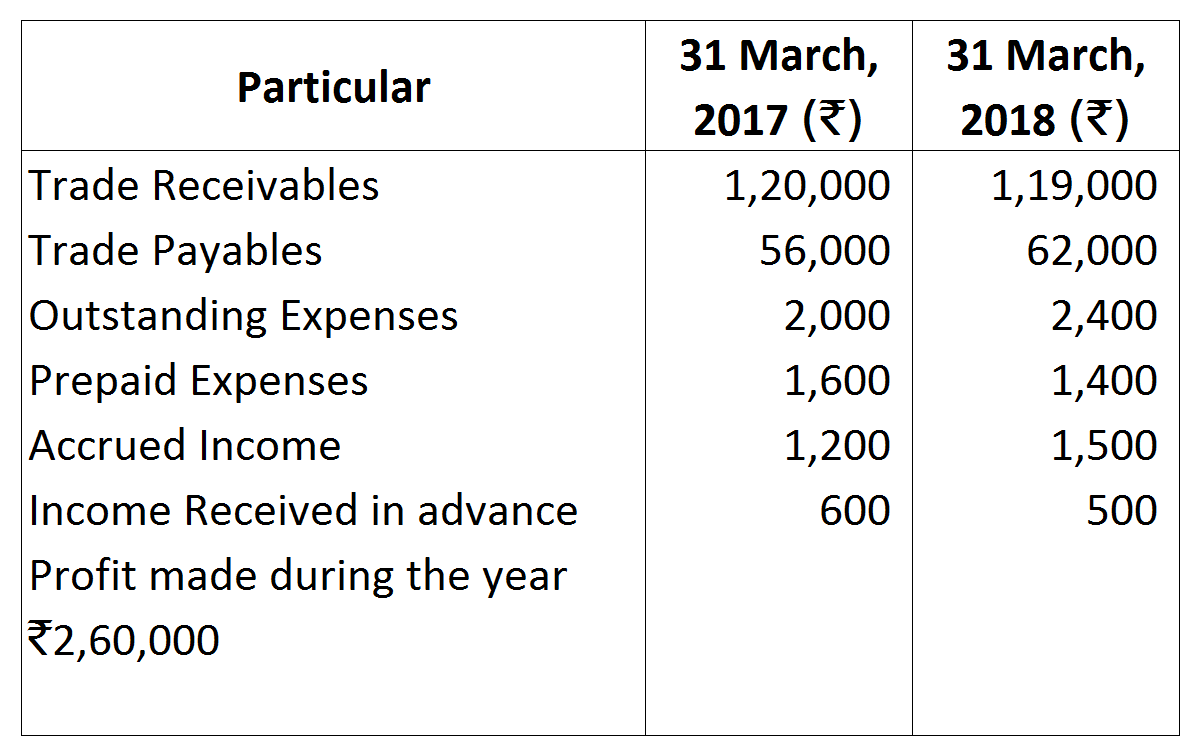

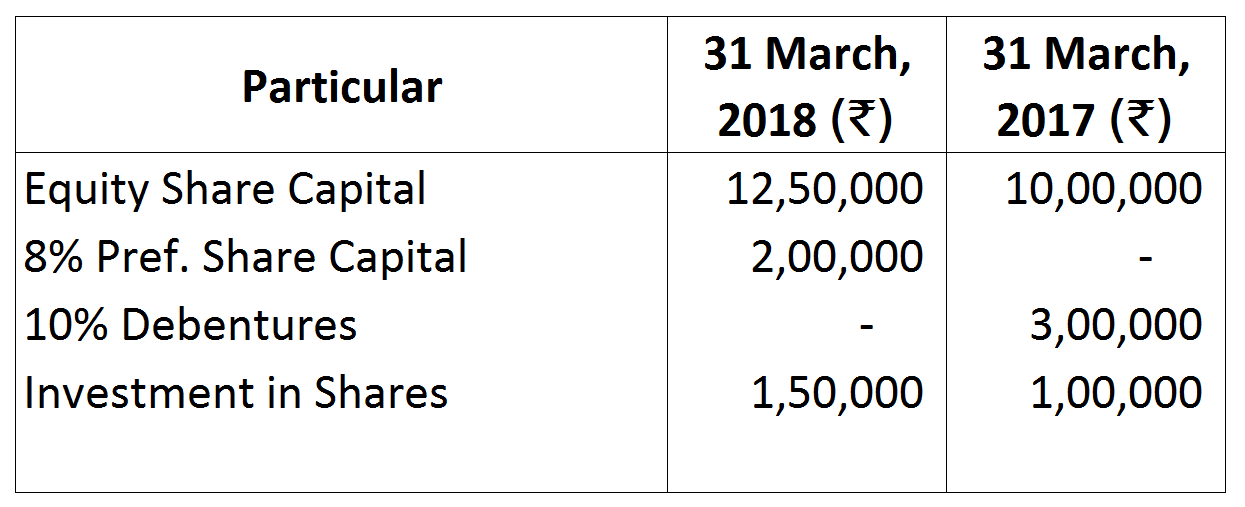

Note: Short-term Loan will be treated as financing activity.

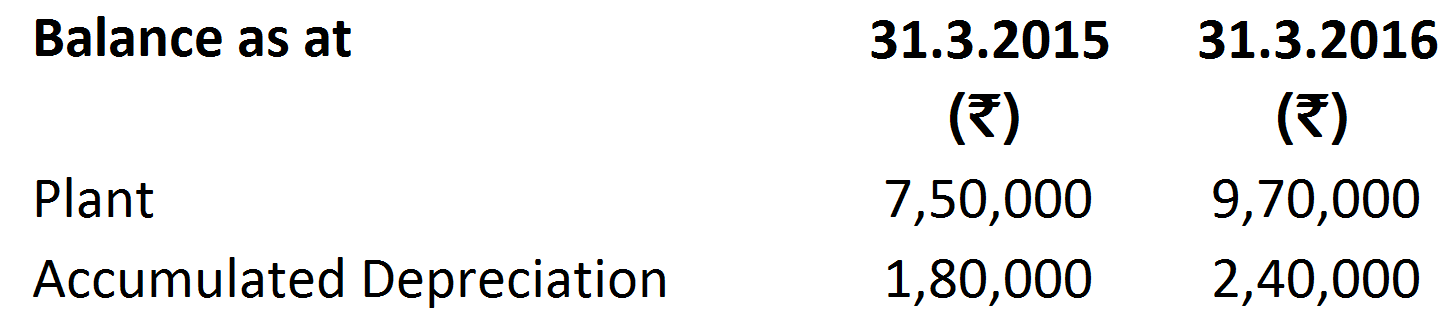

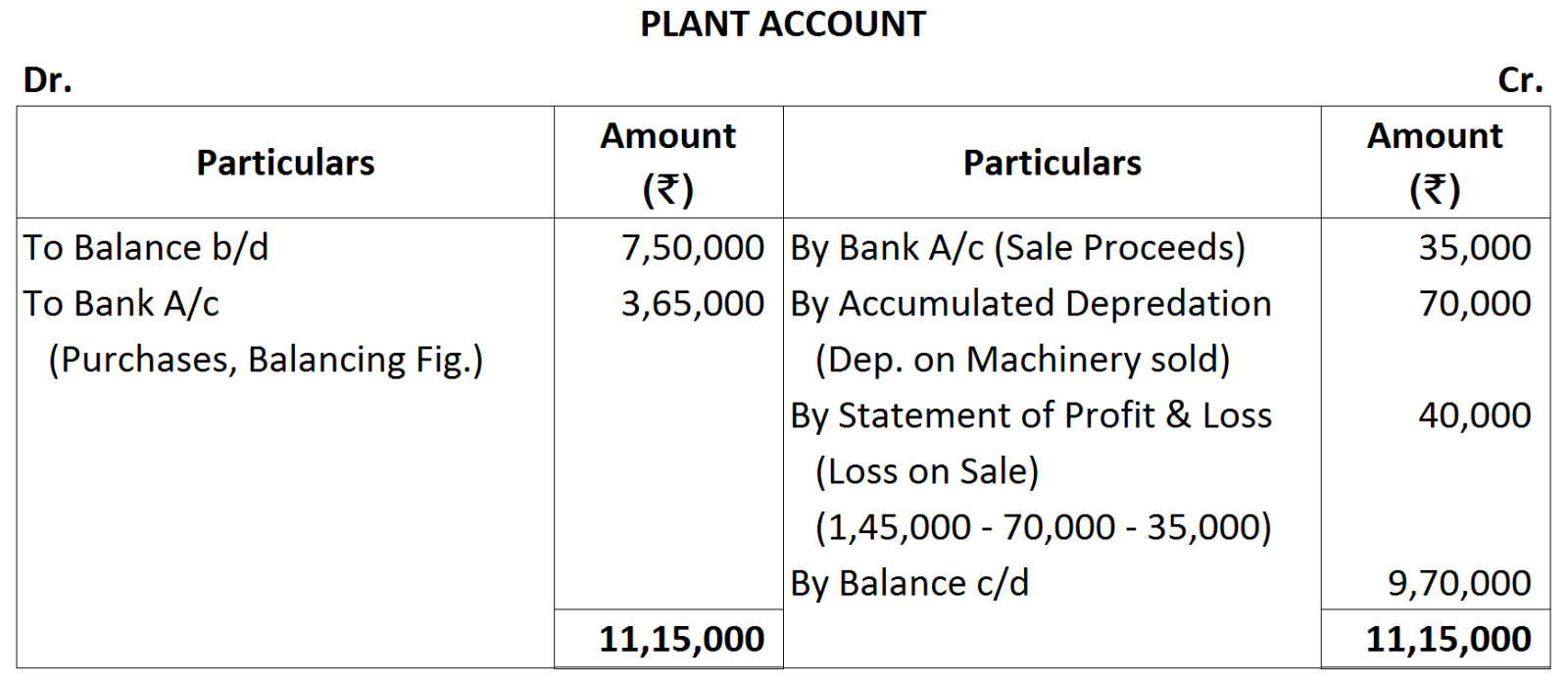

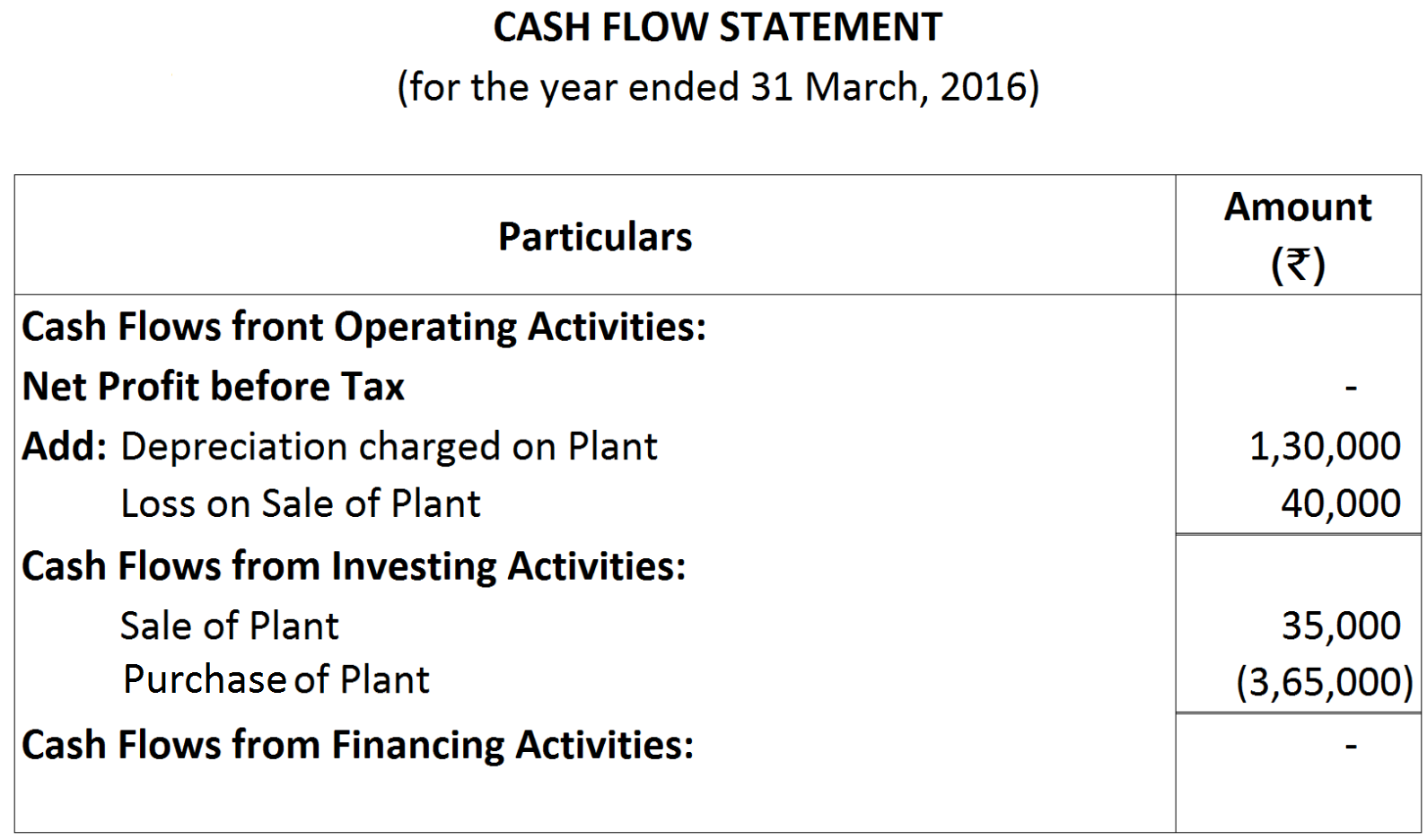

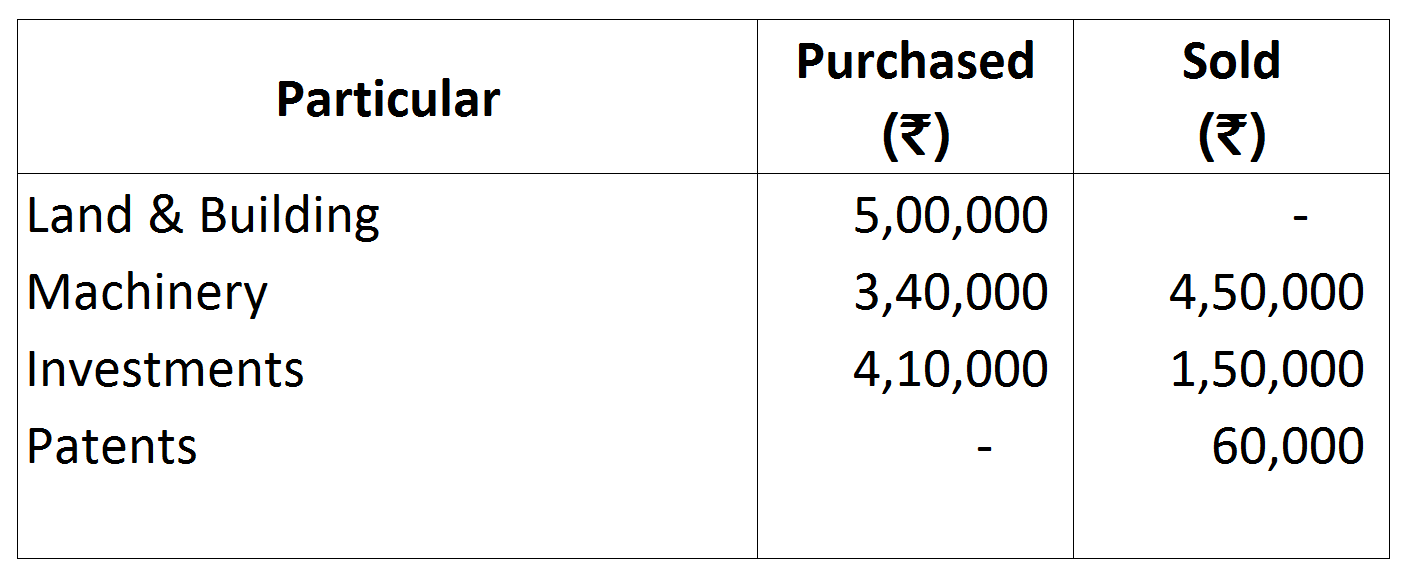

Note: Short-term Loan will be treated as financing activity. Additional Information:Plant costing ₹ 1,45,000; accumulated depreciation thereon ₹ 70,000, was sold for ₹ 35,000.

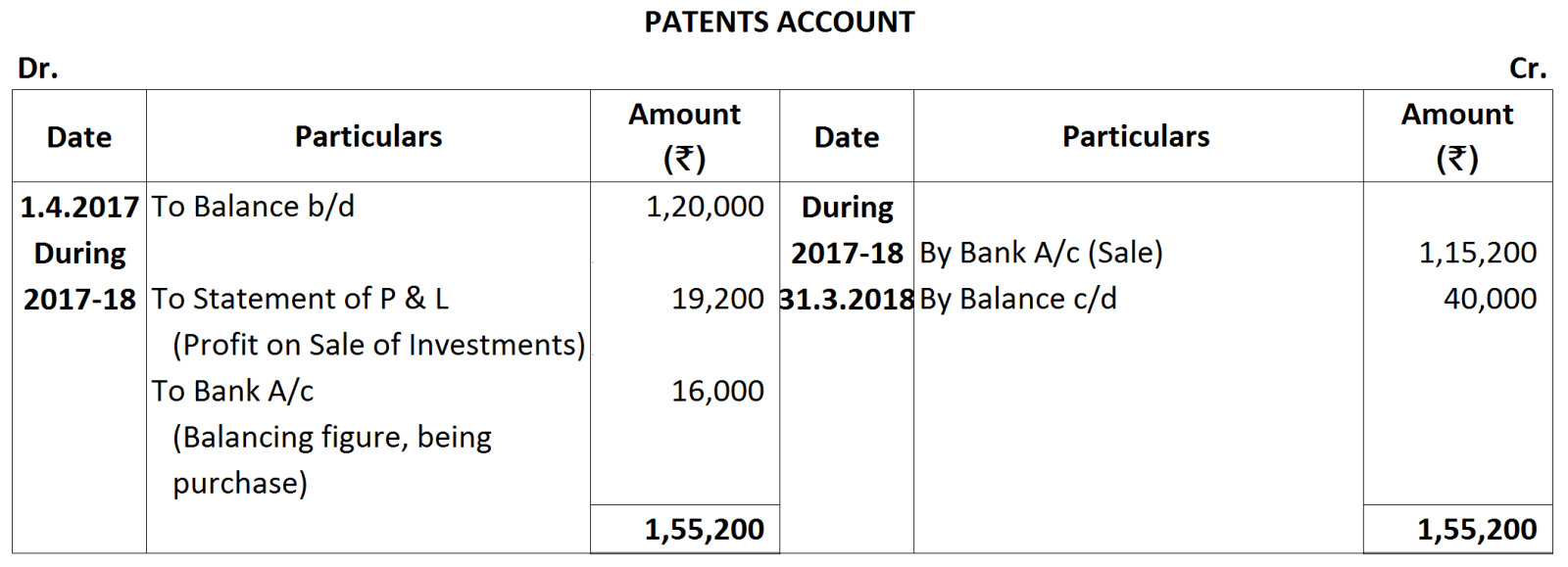

Additional Information:Plant costing ₹ 1,45,000; accumulated depreciation thereon ₹ 70,000, was sold for ₹ 35,000.

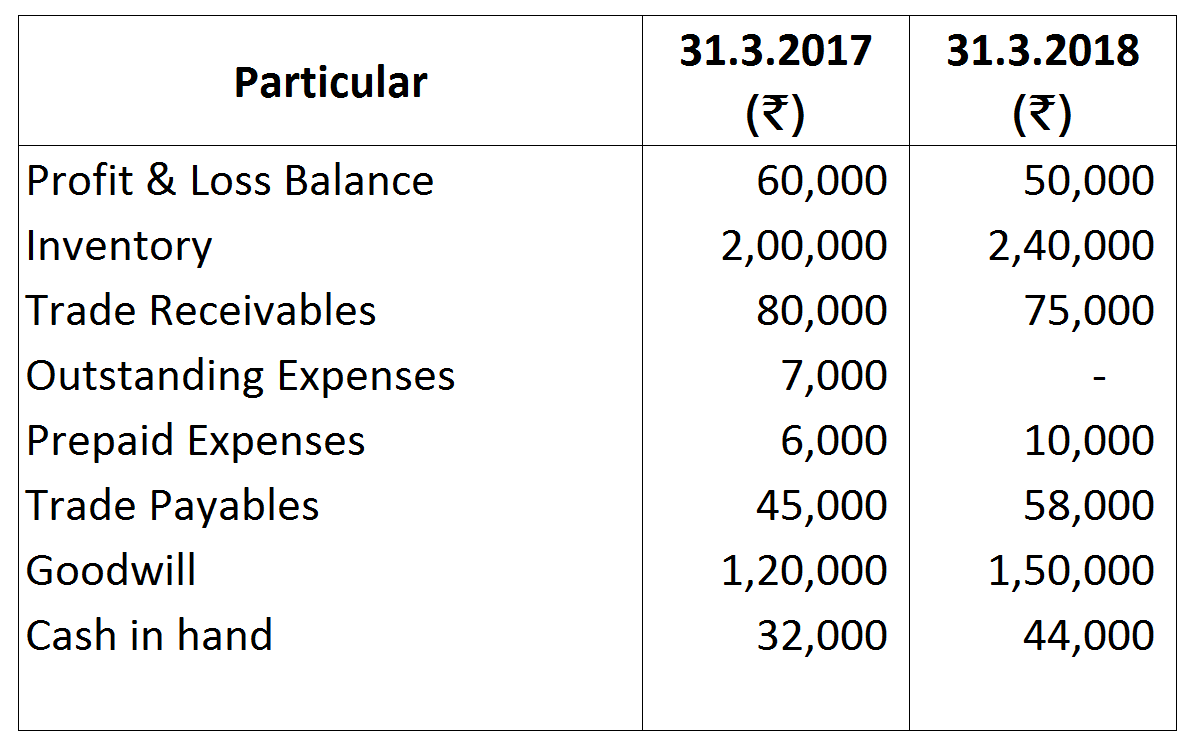

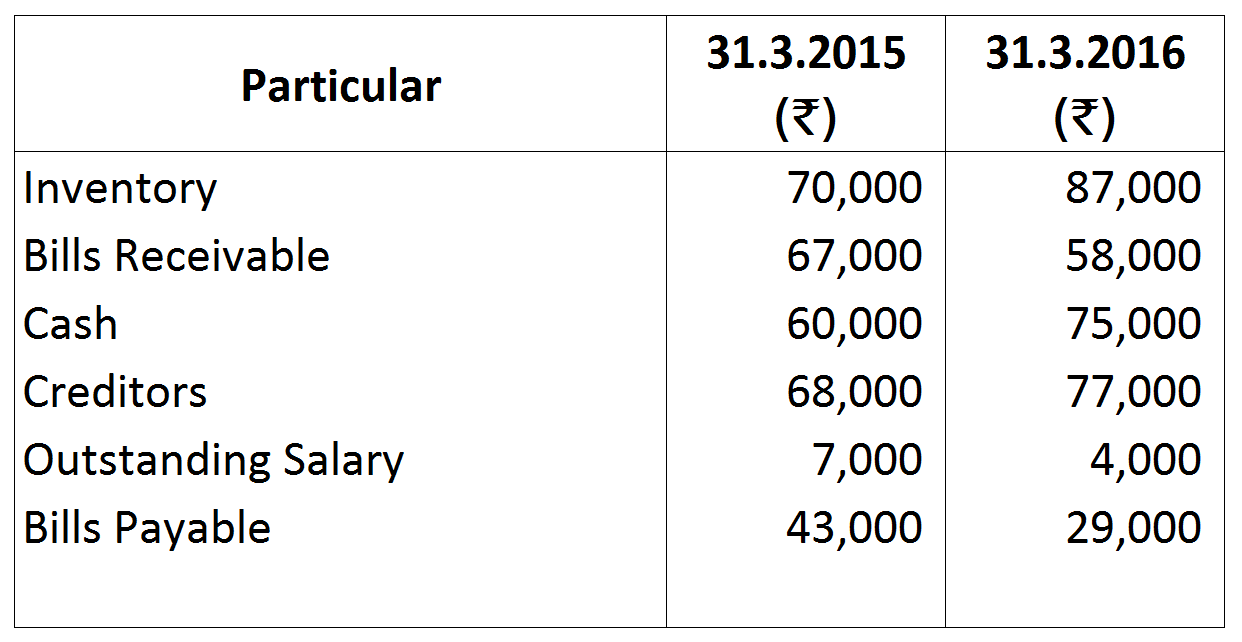

Hint: Goodwill will be treated as purchase of Goodwill. Hence, it will not affect Cash from operating activities.

Hint: Goodwill will be treated as purchase of Goodwill. Hence, it will not affect Cash from operating activities.

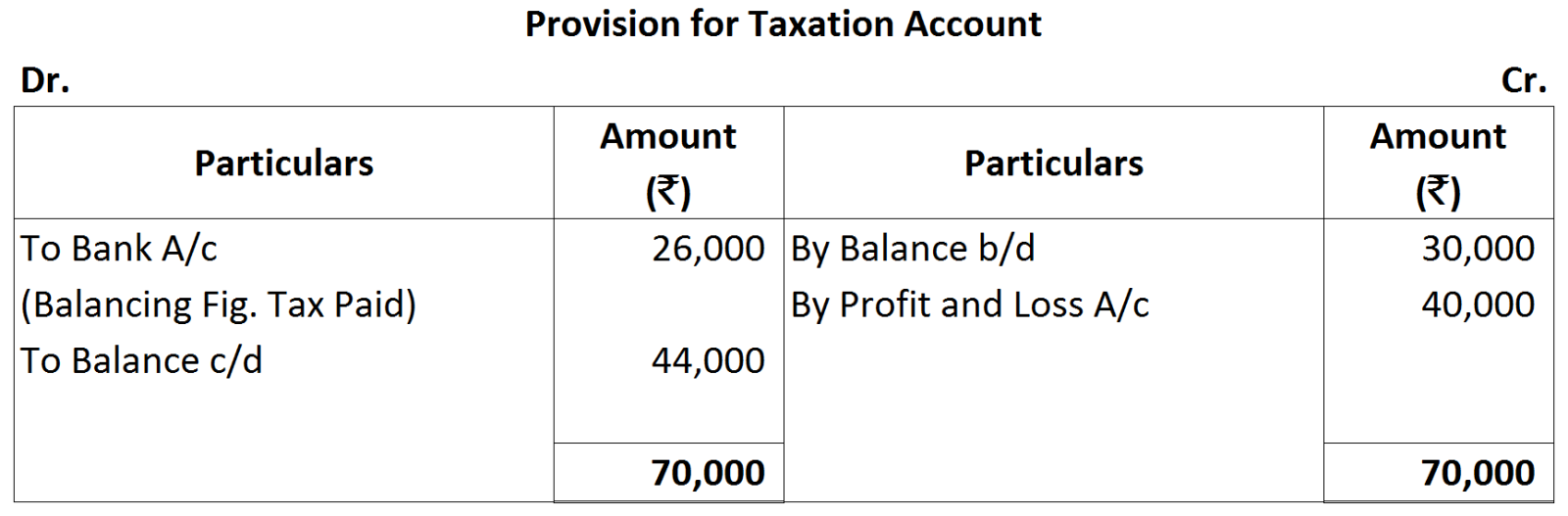

Working Notes:

Working Notes:

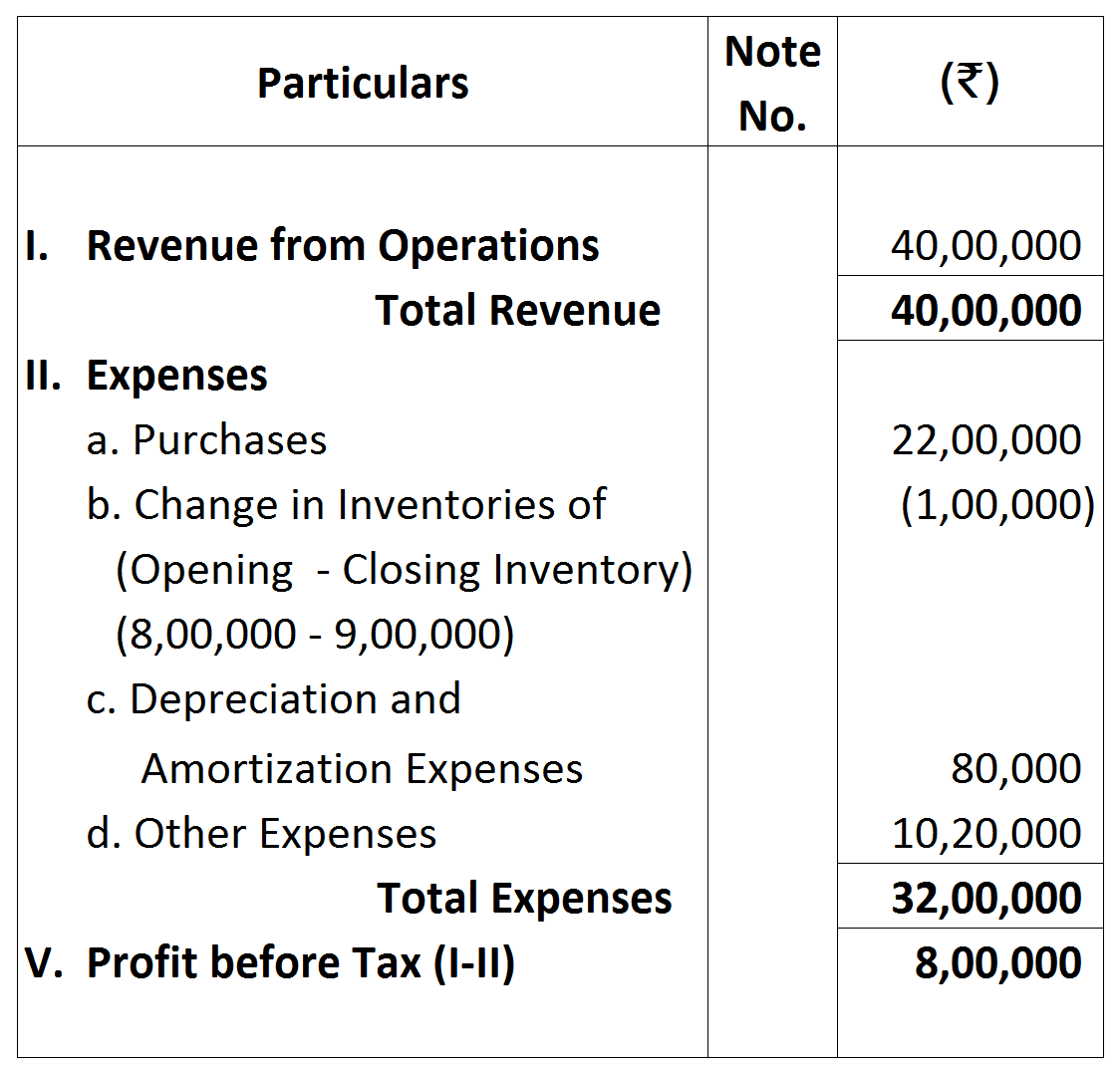

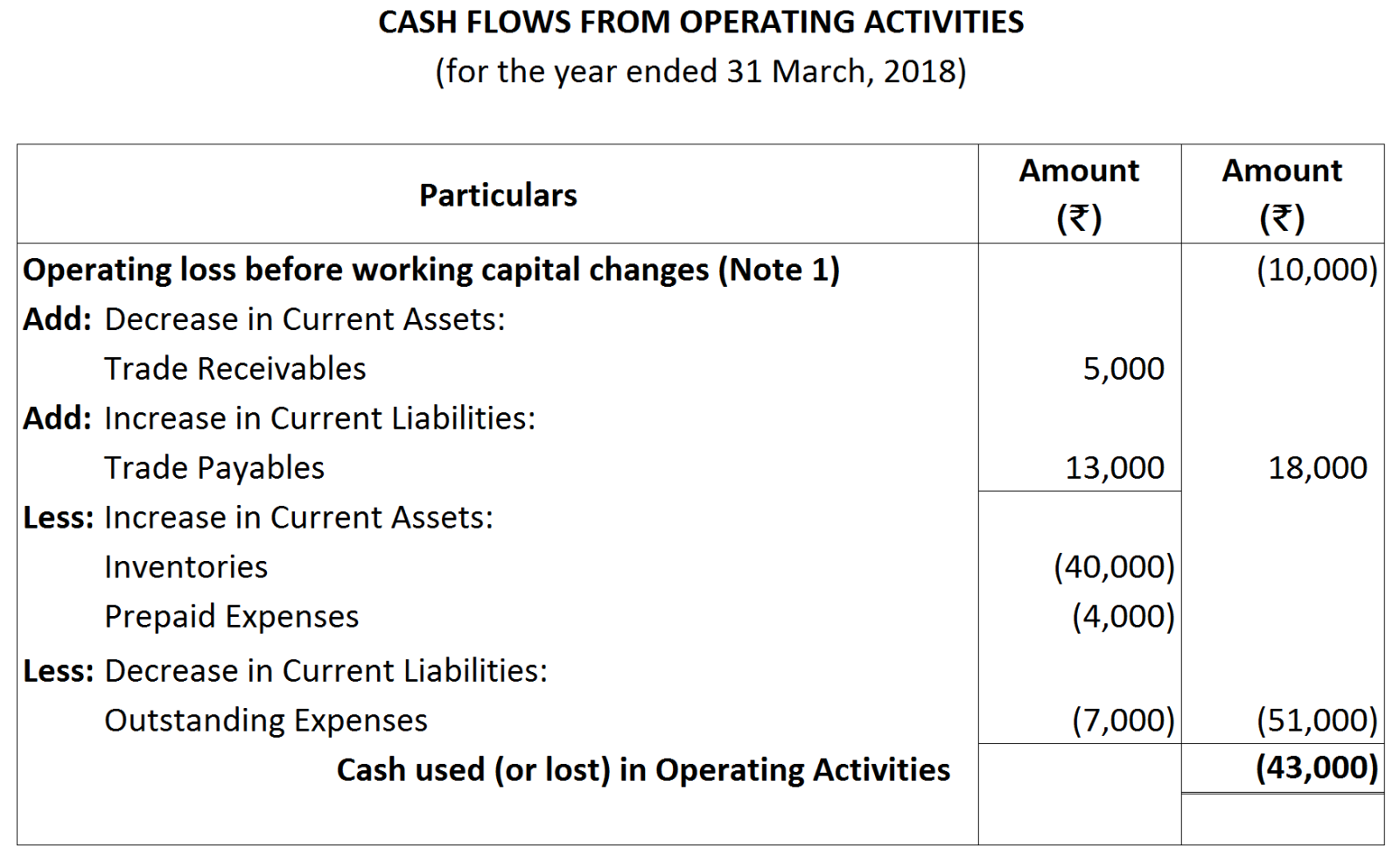

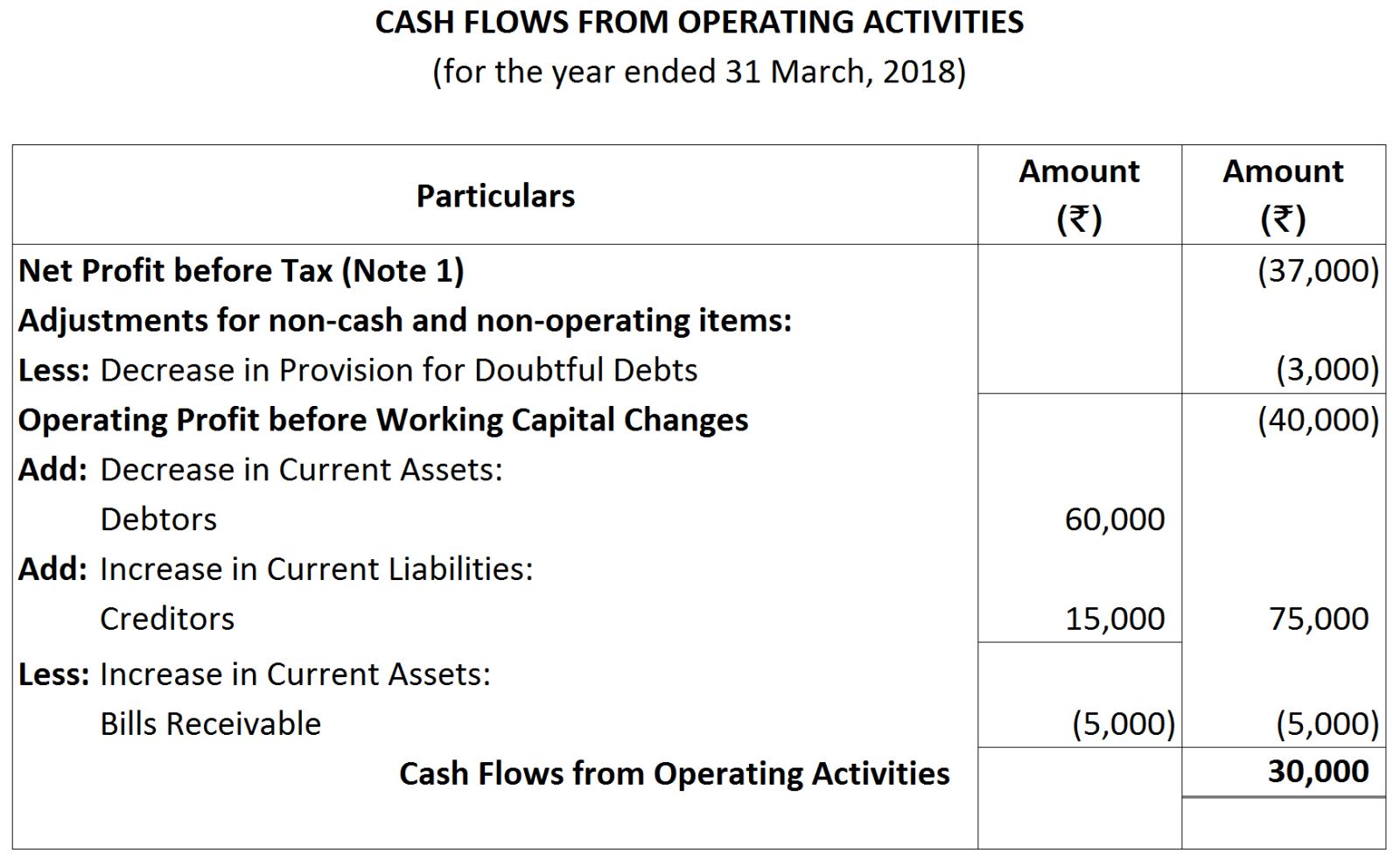

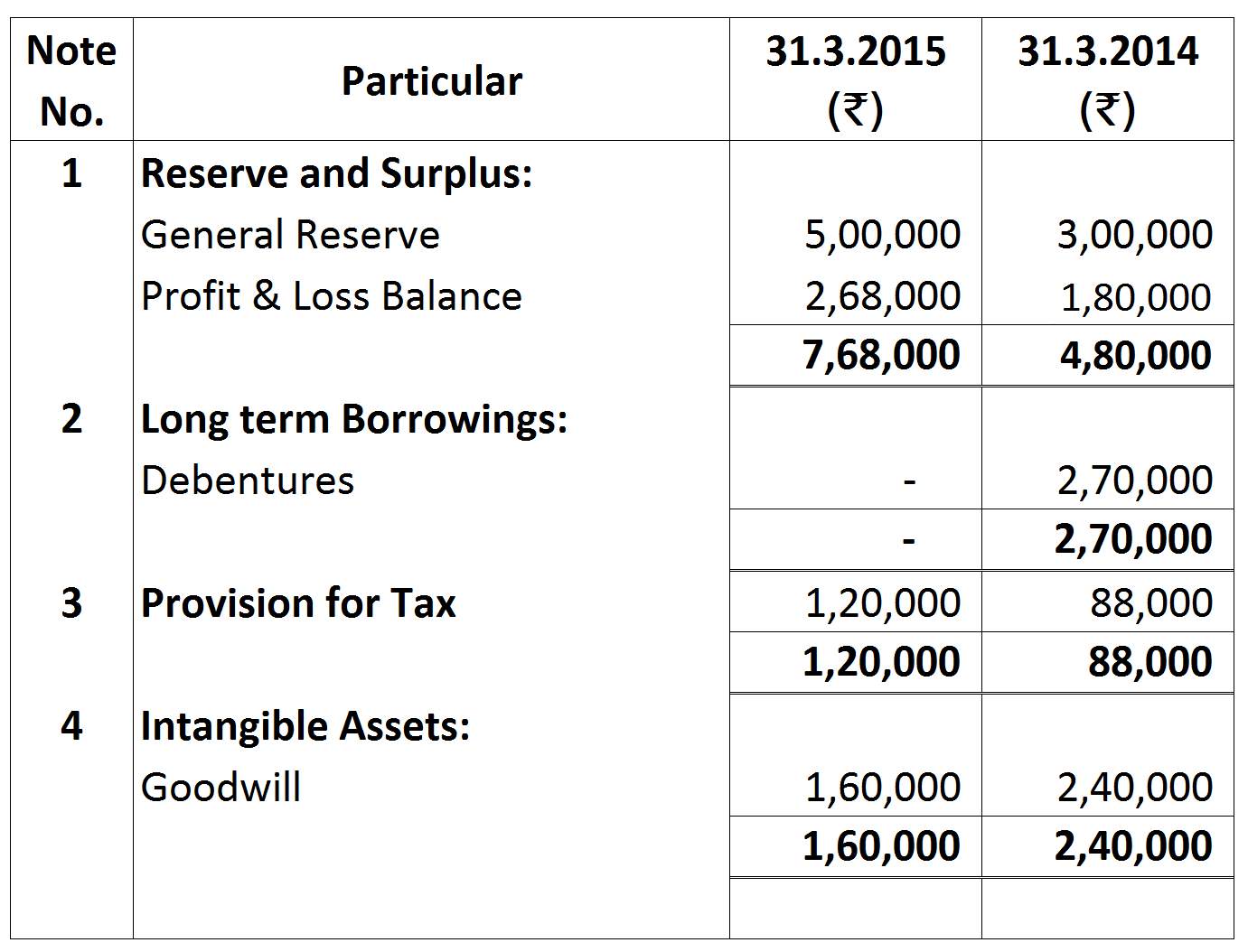

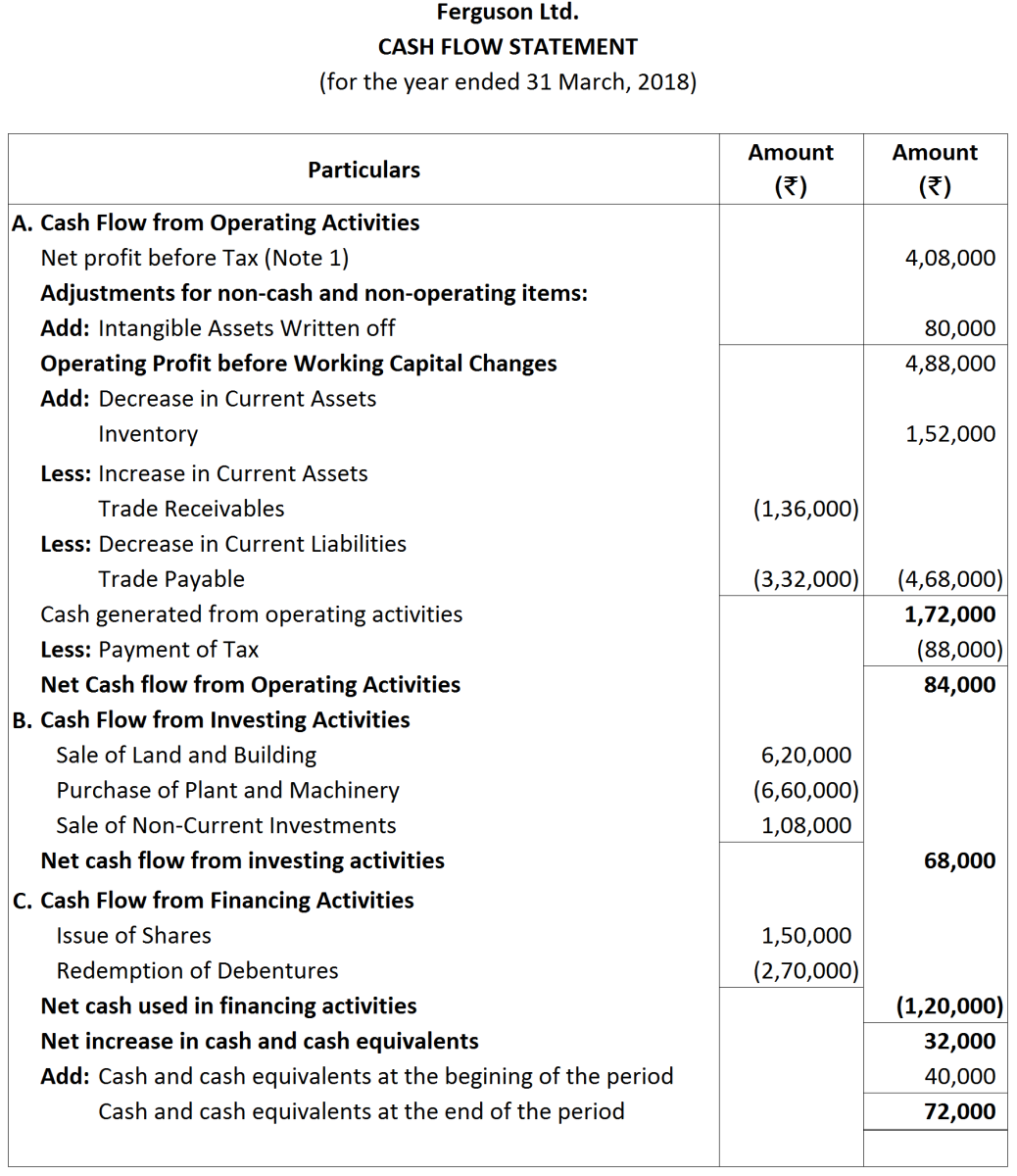

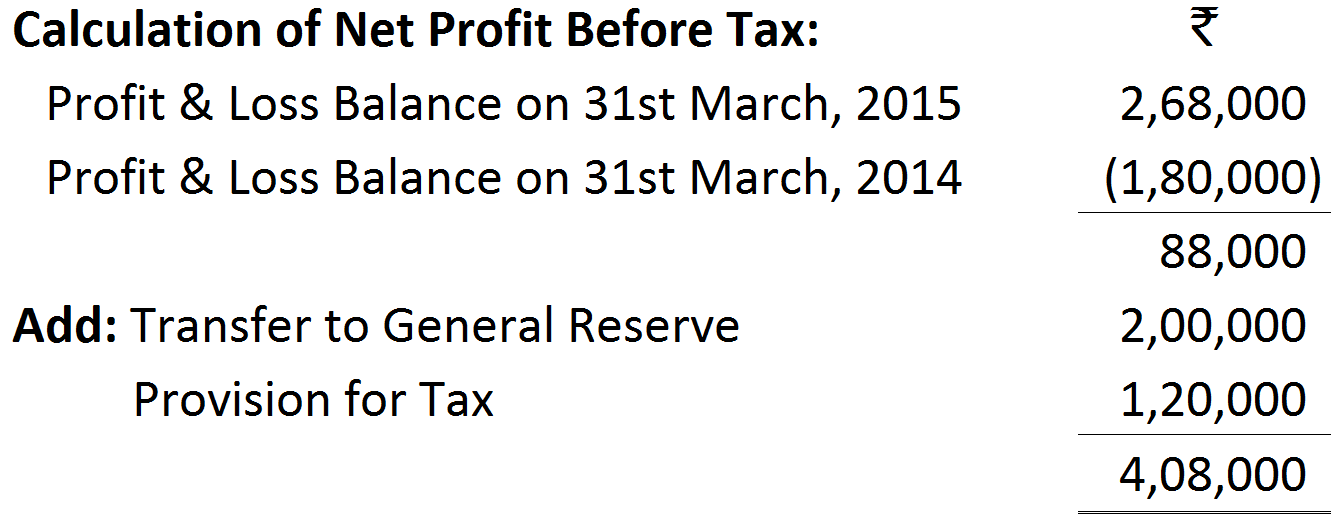

Net Profit before Tax ₹ 4,08,000; Cash Flow from Operating Activities ₹ 84,000; Cash Flow from Investing Activities ₹ 68,000; Cash used in Financing Activities ₹ 1,20,000.

Net Profit before Tax ₹ 4,08,000; Cash Flow from Operating Activities ₹ 84,000; Cash Flow from Investing Activities ₹ 68,000; Cash used in Financing Activities ₹ 1,20,000.