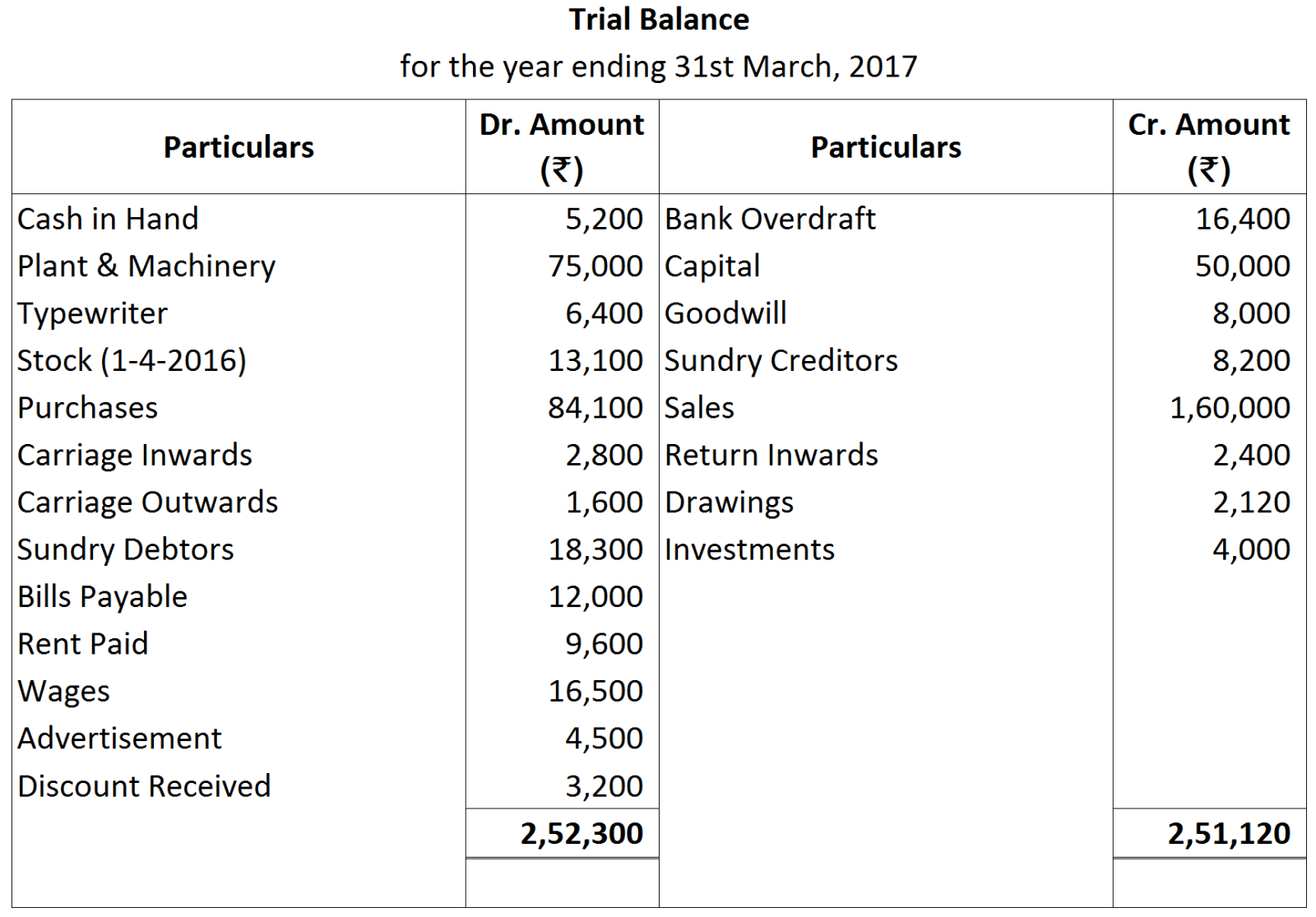

Question

Explain briefly any five advantages of accounting.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

1.

|

Purchased goods from Karunakaran of Chennai for ₹ 1,00,000.

(IGST @18%) |

|

2.

|

Sold goods to Ganeshan of Bengaluru for ₹ 1,50,000.

(CGST @ 6% and SGST @ 6%) |

|

3.

|

Sold goods to S. Nair of Kerala for ₹ 2,60,000.

(IGST @18%) |

|

4.

|

Purchased a Machinery for ₹ 80,000 from Surya Ltd. against cheque.

(CGST @ 9% and SGST @ 9%) |

|

5.

|

Paid rent ₹ 30,000 by cheque.

(CGST @ 6% and SGST @ 6%) |

|

6.

|

Purchased goods from Ram Mohan Rai of Bengaluru for ₹ 2,00,000.

(CGST @ 6% and SGST @ 6%) |

|

7.

|

Paid insurance premium ₹ 10,000 by cheque.

(CGST @ 9% and SGST @ 9%) |

|

8.

|

Received commission ₹ 20,000 by cheque which is deposited into bank.

(CGST @ 9% and SGST @ 9%) |

|

9.

|

Payment made of balance amount of GST.

|

| Date | Amount (₹) |

| Jan. 01, 2017 | 20,000 |

| Jan. 08, 2017 | 25,000 |

| Jan. 10, 2017 | 10,000 |

| Jan. 15, 2017 | 40,000 |

|

2017

|

|

|

March 1

|

Sold to Chandra Light House

|

| 50 Tubelights @ ₹ 60 each Less: 20% | |

| 20 Heaters @ ₹120 each Less: 25% | |

|

March 5

|

Purchased from Charat Ram Electric Co.

|

|

March 10

|

25 Table Fans @ ₹ 600 each |

| 20 Ceiling Fans @ ₹800 each | |

|

Chaudhary & Sons purchased from us

80 Dozen Bulbs @ ₹ 90 per Dozen

|

|

|

March 12

|

Purchased from Ram Lal & Sons one Typewriter for ₹ 6,000 on credit, for office use.

|

|

March 16

|

Sri Ram & Sons sold to us:

|

| 10 Electric Irons @ ₹ 180 each less: 10% | |

|

March 20

|

Chandra Light House returned

|

|

March 22

|

5 Tubelights sold on March 1. |

|

Sold goods to Jai Bhagwan & Co. for cash ₹ 10,000.

|

|

|

March 25

|

Returned to Sri Ram & Sons 2 Electric Irons purchased on March 16.

|

|

2018

|

|

|

March 1

|

Mahesh Chandra of Bihar purchased goods for ₹ 1,00,000 from Sunil Soren of Jharkhand and sold the same to Deepak Patnaik of Odisha for ₹ 1,50,000.

|

|

March 5

|

Deepak Patnaik sold goods to Suresh Yadav of Odisha for ₹ 1,80,000.

|

|

March 10

|

Suresh Yadav sold goods to Ravi Chakravarti of West Bengal for ₹ 2,50,000.

|

|

March 14

|

Ravi Chakravarti sold goods costing ₹ 2,50,000 to Sanjay Diwedi of West Bengal at a profit of 40% on cost.

|