Question

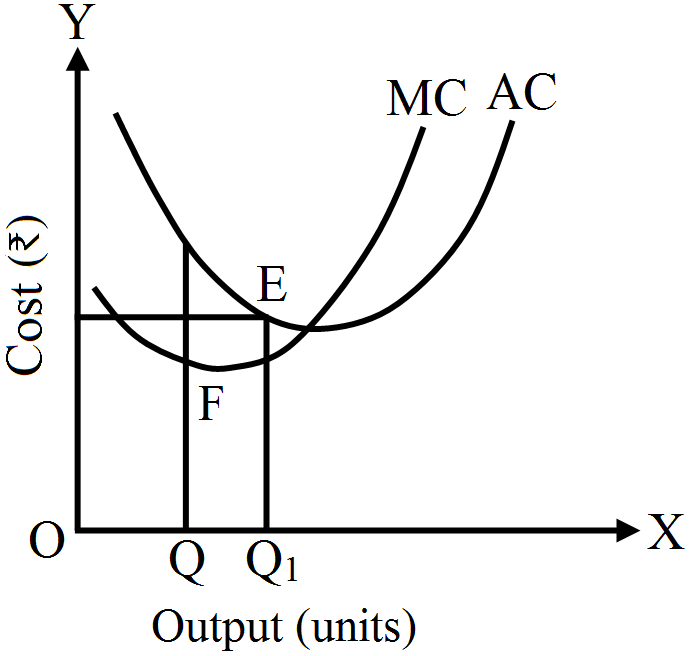

Explain the relationship between Marginal Cost and Average Cost using diagram.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

Total Output

(Units)

|

Total Cost (Rs)

|

|

0

|

120

|

|

1

|

180

|

|

2

|

200

|

|

3

|

210

|

|

4

|

230

|

|

5

|

270

|

|

6

|

360

|