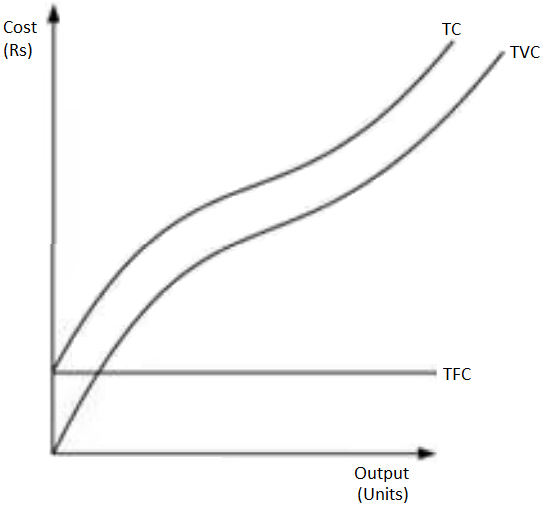

Total Fixed Cost: This refers to the costs incurred by a firm in order to acquire the fixed factors for production like cost of machinery, buildings, depreciation, etc. In short run, fixed factors cannot vary and accordingly the fixed cost remains the same through all output levels. These are also called overhead costs.

Total Variable Cost: This refers to the costs incurred by a firm on variable inputs for production. As we increase quantities of variable inputs, accordingly the variable cost also goes up. It is also called 'Prime cost' or 'Direct cost' and includes expenses like - wages of labour, fuel expenses, etc.

Total Cost (TC): The sum of total fixed cost and total variable cost is called the total cost.

Total cost = Total fixed cost + Total variable cost

TC = TFC + TVC

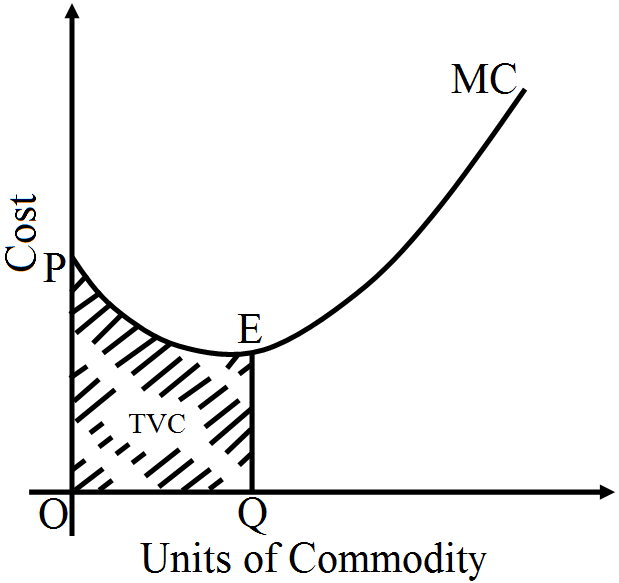

Relationship between TC, TFC, and TVC

Relationship between TC, TFC, and TVC:

- TFC curve remains constant throughout all the levels of output as fixed factor is constant in short run.

- TVC rises as the output is increased by employing more and more of labour units. Till point Z, TVC rises at a decreasing rate, and so the TC curve also follows the same pattern.

- The difference between TC and TVC is equivalent to TFC.

- After point Z, TVC rises at an increasing rate and therefore TC also rises at an increasing rate.

- Both TVC and TFC is derived from TC i.e. TC = TVC + TFC.

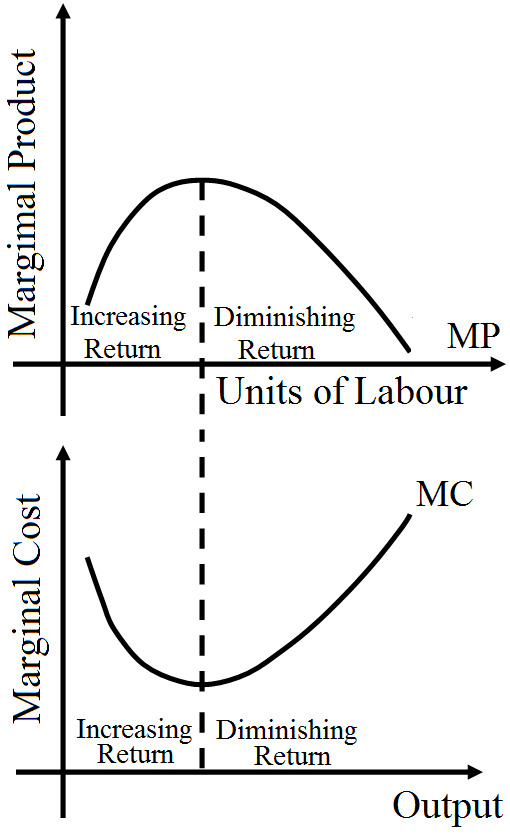

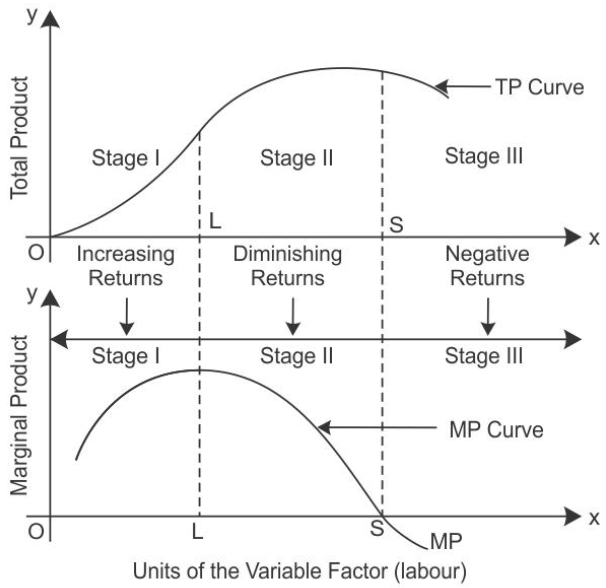

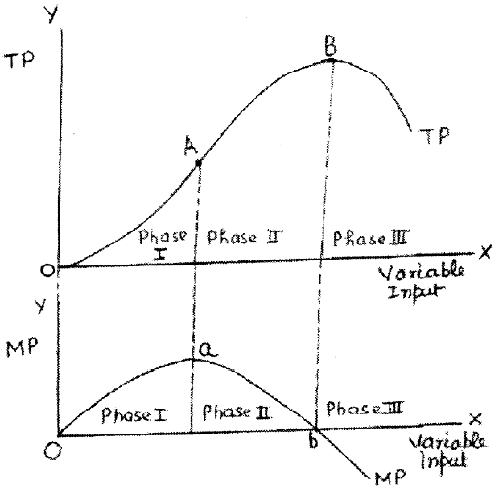

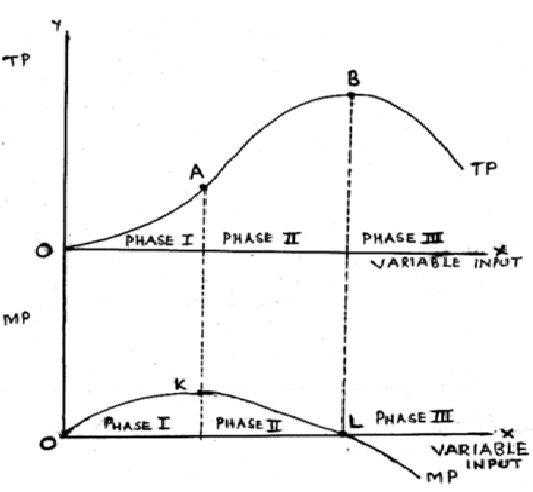

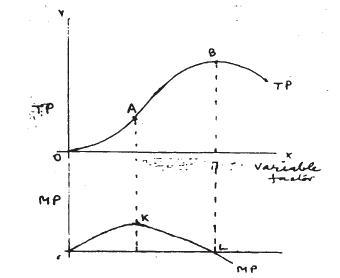

According to the Law of Variable Proportions, when only one input is increased while others are held unchanged, MP and TP change in the following manner:

According to the Law of Variable Proportions, when only one input is increased while others are held unchanged, MP and TP change in the following manner:

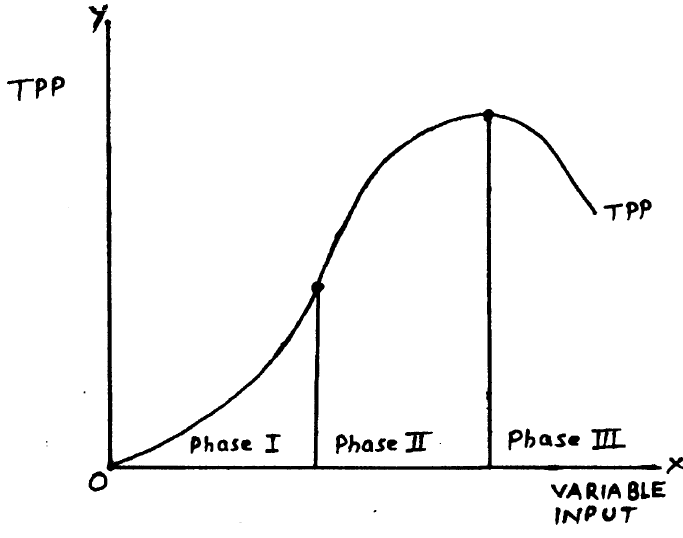

Statement of three phases of law of variable proportion in terms of total physical product using the diagram.

Statement of three phases of law of variable proportion in terms of total physical product using the diagram. Relationship among MC, AVC & AC:

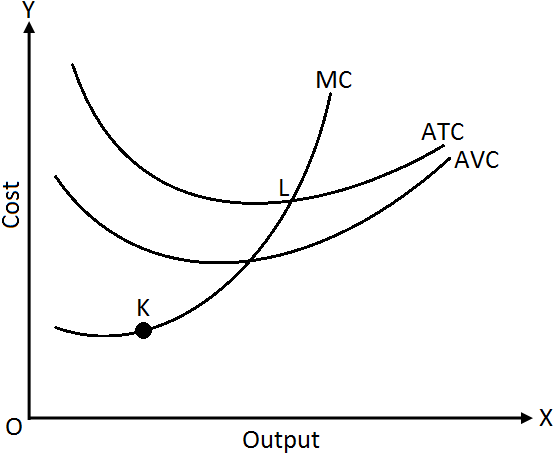

Relationship among MC, AVC & AC: