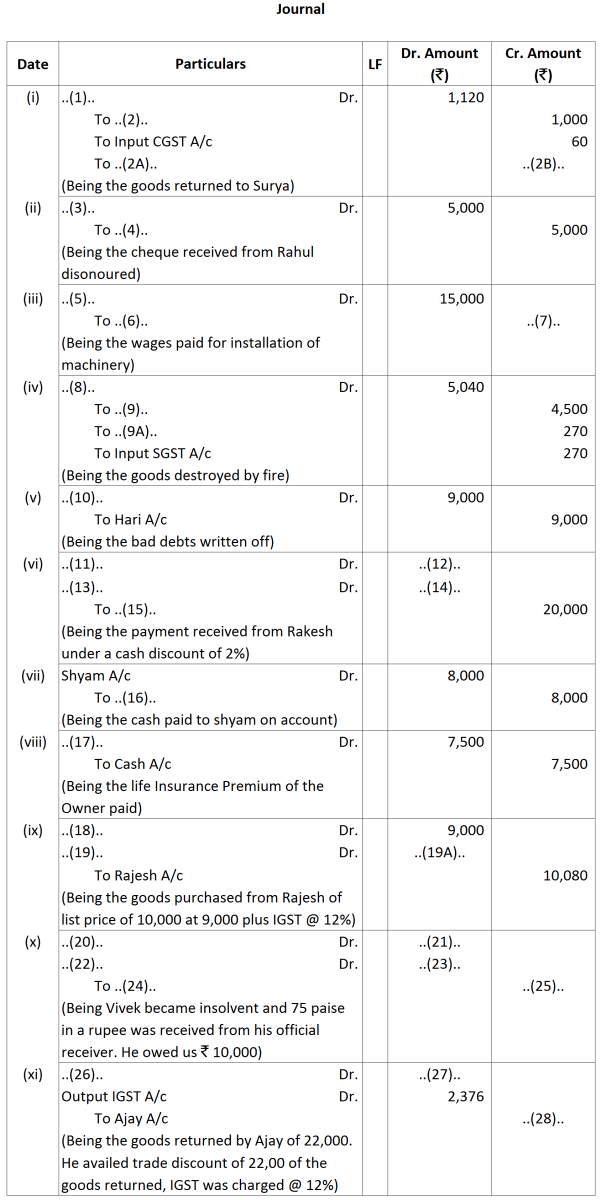

Question

Fill in the missing values on the basis of narration:

Get the step-by-step solution for this question inside the Vidyadip app.

Get the answer in the appGenerate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

2017

|

|

(₹)

|

|

Feb. 1

|

Received from cashier ₹ 9,250, the amount required to make up the amount of the 'imprest' viz.

|

10,000

|

|

Feb. 3

|

Chowkidar's Wages

|

500

|

|

Pencils, Pens etc.

|

250

|

|

|

Feb. 5

|

Bus fare to workmen sent to customer's premises

|

600

|

|

Feb. 7

|

Paid for wages

|

200

|

|

Feb. 10

|

Postage

|

800

|

|

Feb. 12

|

Three Wheeler's charges for manager's trip to the city

|

100

|

|

Feb. 12

|

Wages to casual labourer

|

850

|

|

Feb. 14

|

Repair of furniture

|

300

|

|

Feb. 14

|

Repair of scooter

|

400

|

|

Feb. 18

|

Taxi fare to assistant manager

|

750

|

|

Feb. 20

|

Refreshment to Customers

|

450

|

|

Feb. 22

|

Paid for cartage

|

1,500

|

|

Feb. 25

|

Locks purchased

|

1,200

|

|

Feb. 25

|

Conveyance

|

250

|

|

Feb. 26

|

Paid for writing pads and registers

|

900

|

|

Feb. 28

|

Courier Charges

|

550 |

|

2019

|

|

₹

|

||

|

Jan. 1

|

Commenced business with cash

|

50,000

|

||

|

Jan. 2

|

Opened Bank Account and deposited cash in bank

|

20,000

|

||

|

|

Purchased goods in cash of ₹ 5,000 plus CGST and SGST @ 6% each

|

5,000

|

||

|

Jan. 4

|

Paid wages

|

500

|

||

|

Jan. 6

|

Cash sales of ₹ 2,000 plus CGST and SGST @ 6% each

|

2,000

|

||

|

|

Purchased goods for ₹ 10,000 plus CGST and SGST @ 6% each for cash

|

|

||

|

Jan. 10

|

Sold goods of ₹ 4,000 plus CGST and SGST @ 6% each and payment received by cheque which is deposited in Bank, allowed cash discount of ₹ 400

|

|

||

|

|

Received from Amit

|

5,900

|

||

|

|

Allowed him discount

|

100

|

||

|

Jan. 15

|

Paid to Bhaskar

|

2,800

|

||

|

|

Received discount

|

200

|

||

|

Jan. 18

|

Purchased goods from Kanchan, Delhi of ₹ 10,000 plus IGST @ 12%

|

|

||

|

Jan. 20

|

Goods were destroyed during transportation, Transport Company settled the claim for ₹ 10,000 in full

|

|

||

|

Jan. 27

|

Received cheque from the transport company

|

10,000

|

||

|

Jan. 28

|

Withdrew for office use

|

5,000

|

||

|

|

|

₹

|

|

1.

|

Charge depreciation on Machinery

|

20,000

|

|

2.

|

Salary due to Office Clerks

|

1,00,000

|

|

3.

|

Received cash for Bad-Debts written off last year

|

5,000

|

|

4.

|

Purchased goods from Ashok & Co. for ₹ 50,000 at 20% Trade Discount. Half the payment was made in cash.

|

|

|

5.

|

Issued cheque to Ashok & Co. in full settlement

|

19,500

|

|

6.

|

Paid Life Insurance Premium by cheque

|

6,000

|

|

7.

|

Proprietor used goods for household purposes

|

20,000

|

|

8.

|

Goods given free to a hospital out of business

|

10,000

|