Question 16 Marks

Journalise the following transactions in the books of Ashok:

- Received ₹ 11,700 from Hari Krishan in full settlement of his account for ₹ 12,000.

- Received ₹ 11,700 from Shyam on his account for ₹ 12,000.

- Received a first and final dividend of 70 paise in the rupee from the official receiver of Rajagopal who owed us ₹ 7,000.

- Paid ₹ 2,880 to A.K. Mandal in full settlement of his account for ₹ 3,000.

- Paid ₹ 2,880 to S.K. Gupta on his account for ₹ 3,000.

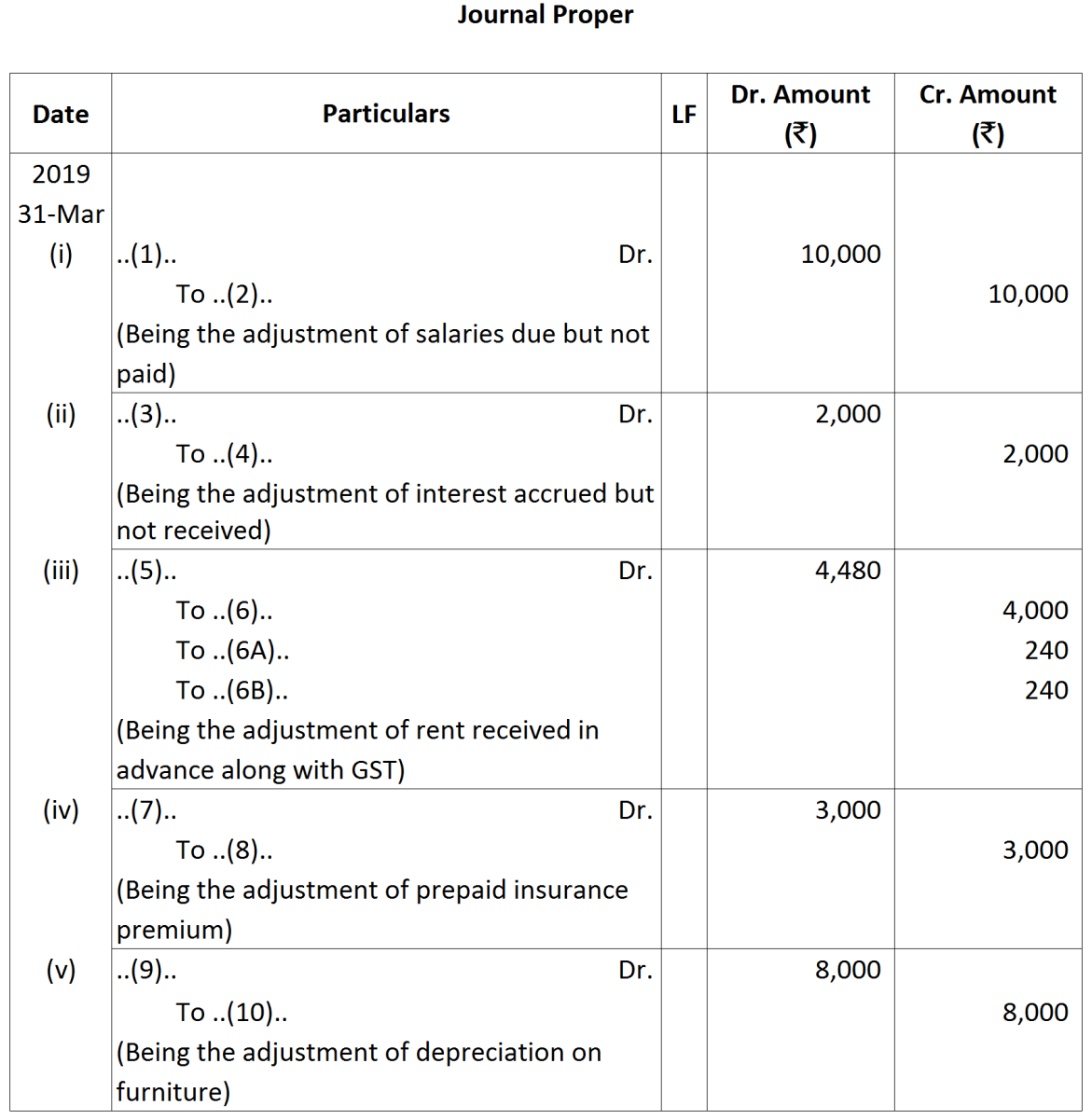

Working Note:

Working Note:

Working Notes:

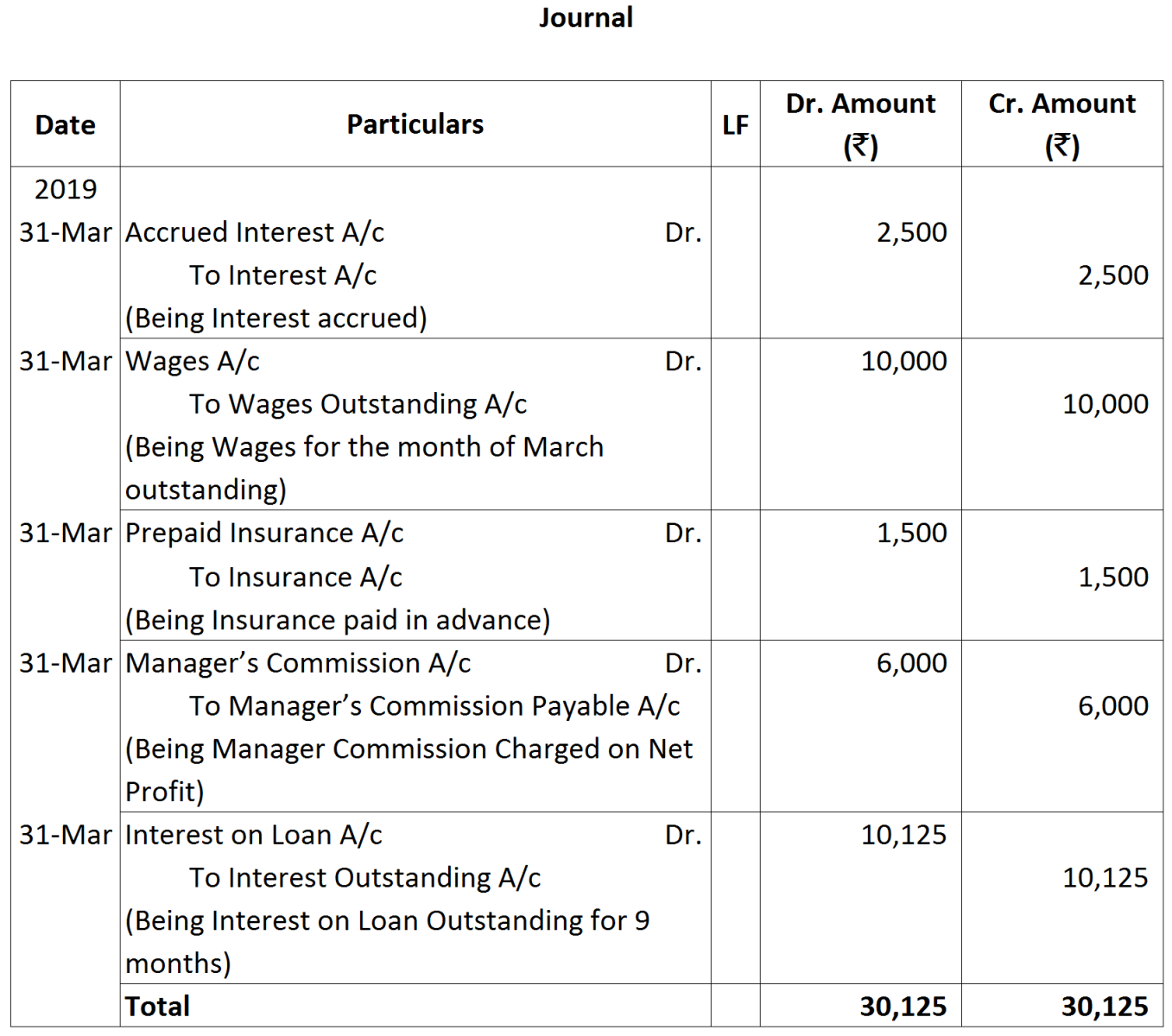

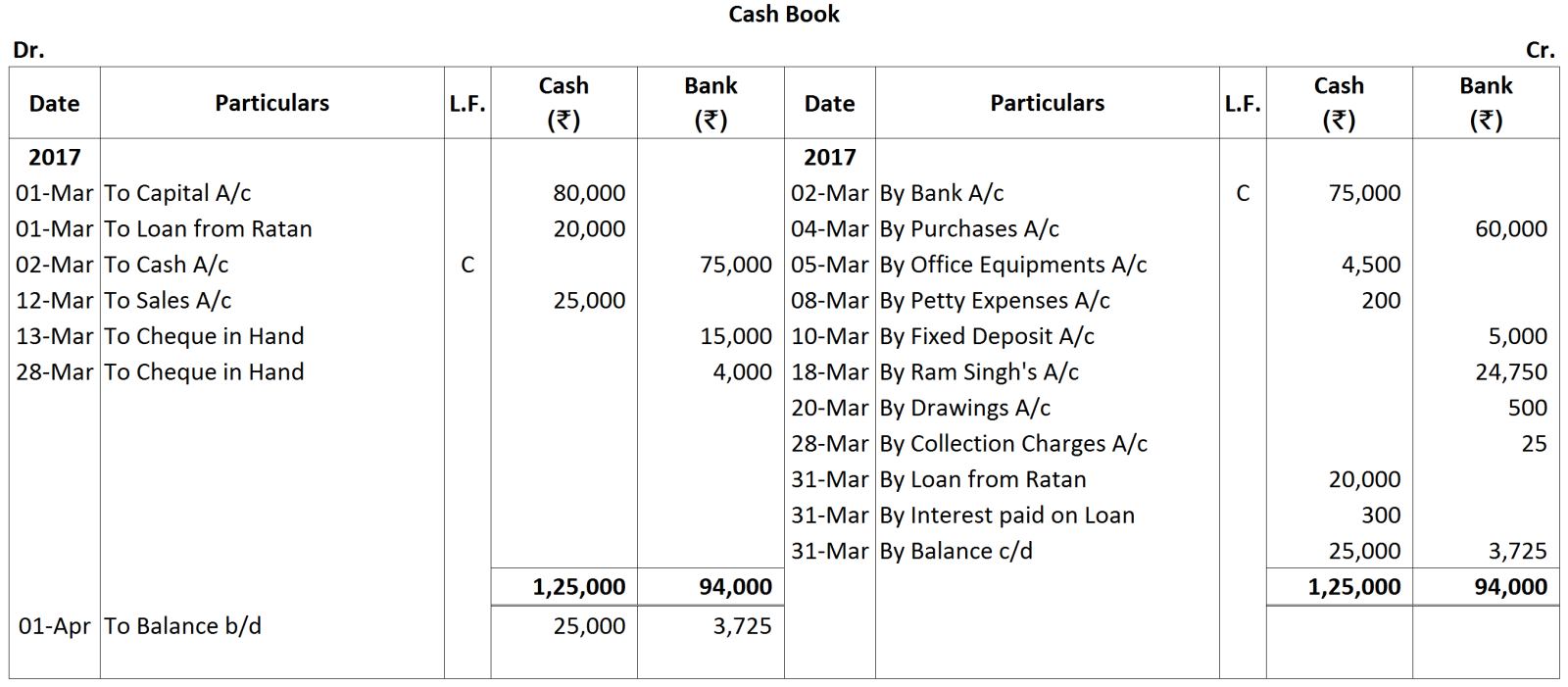

Working Notes: WN 2: Calculation of Interest on Loan, $\text{Interest on Loan}=20,000\times\frac{18}{100}\times\frac{1}{2}=₹\ 300$

WN 2: Calculation of Interest on Loan, $\text{Interest on Loan}=20,000\times\frac{18}{100}\times\frac{1}{2}=₹\ 300$

Working Note:

Working Note:

Working Note:

Working Note: