Question

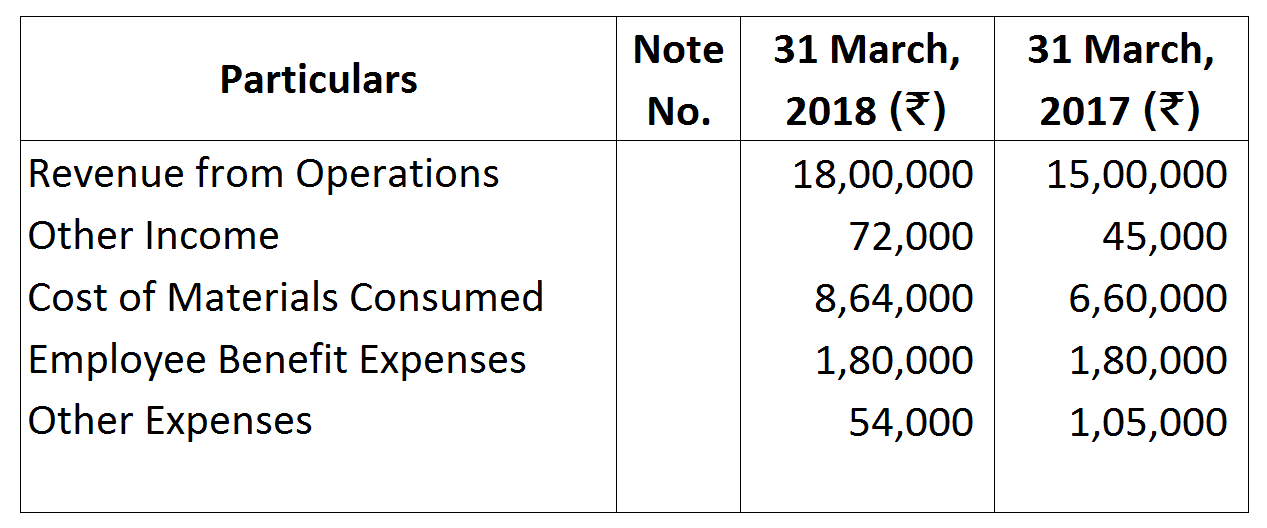

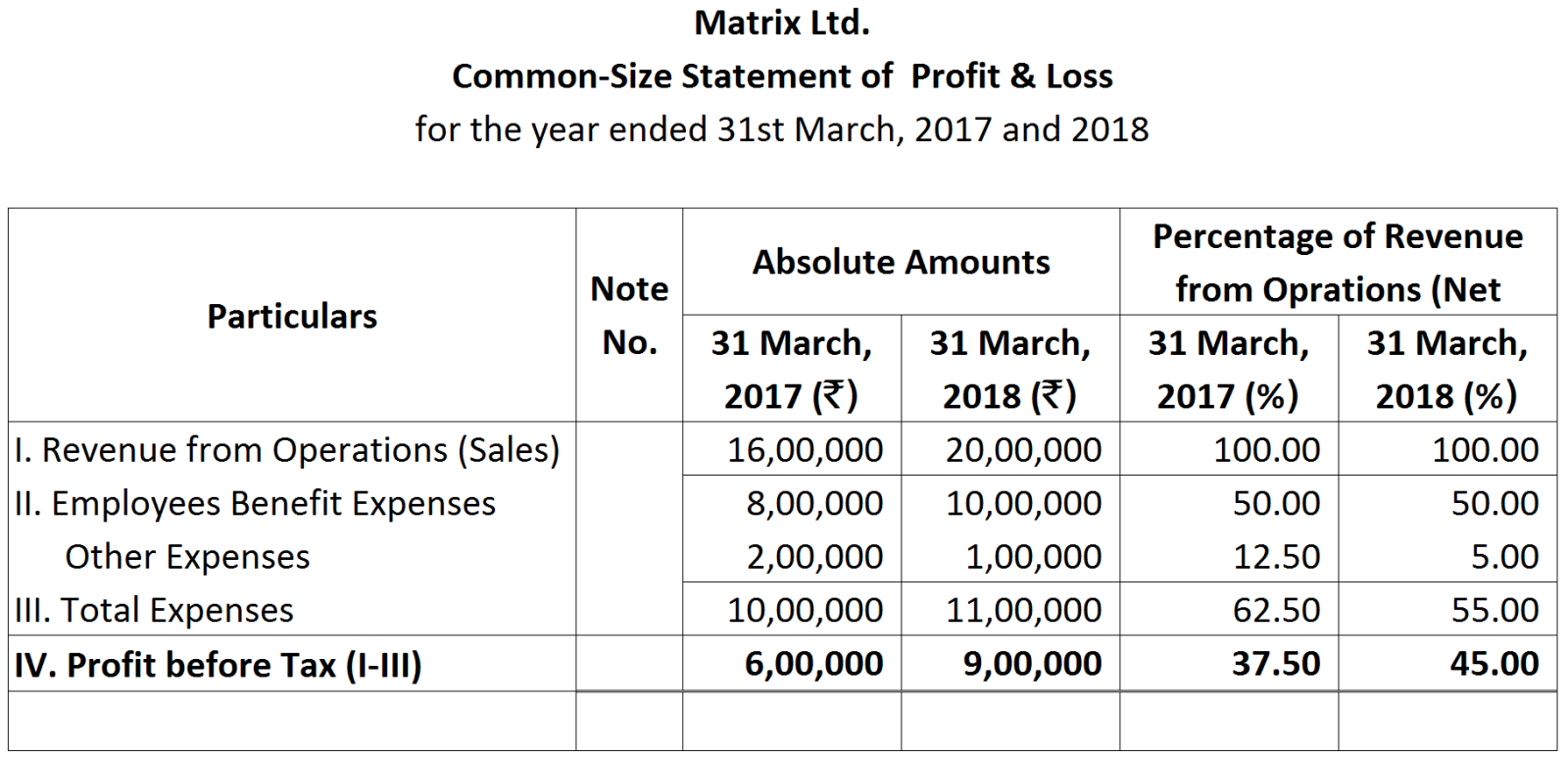

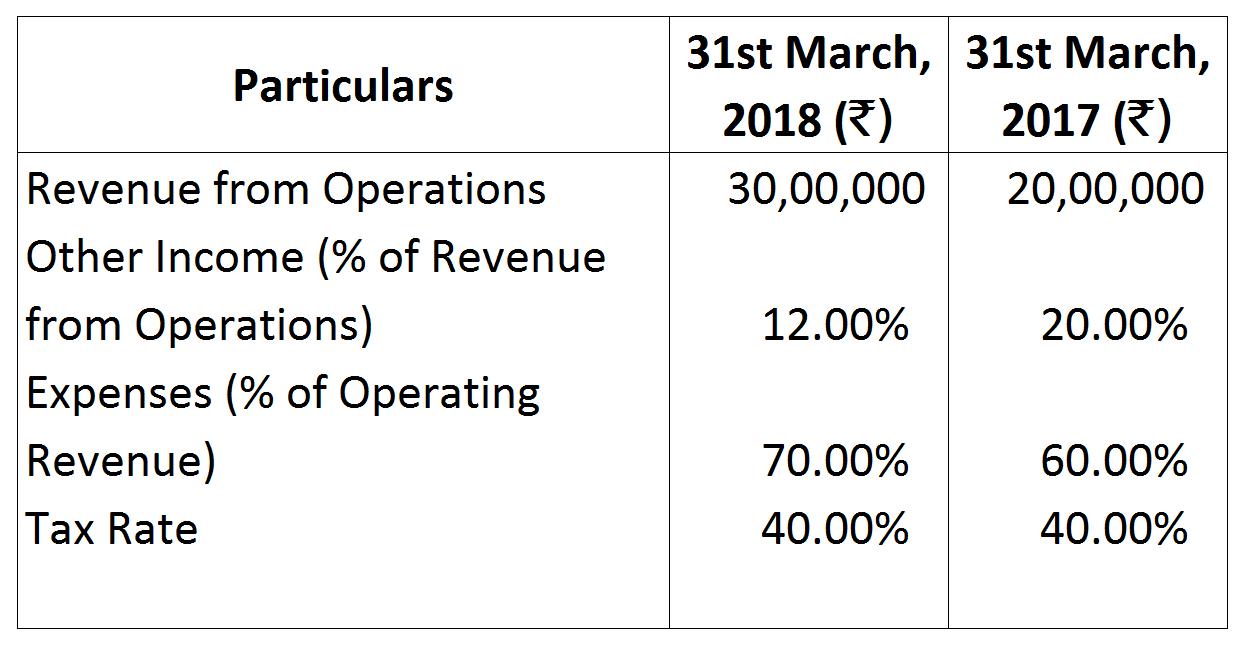

From the above, Compute Operating Ratio.From the above, Compute Operating Ratio.

From the above, Compute Operating Ratio.From the above, Compute Operating Ratio.| Operating Ratio | 31st March, 2017 | 31st March, 2018 |

| $\frac{\text{Operating Cost}}{\text{Revenue from Operation}}\times100$ | $=\frac{₹\ 10,00,000}{₹\ 16,00,000}\times100=62.50\%$ | $=\frac{₹\ 11,00,000}{₹\ 20,00,000}\times100=55\%$ |

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

Calculate Cash flow from operating activities.

Calculate Cash flow from operating activities. Note: Proposed Dividend ₹ 25,000 is shown as contigent liability in Notes to Accounts.

Note: Proposed Dividend ₹ 25,000 is shown as contigent liability in Notes to Accounts.| On Application | - | ₹ 3 per share, |

| On Allotment | - | ₹ 5 per share |

| On First and Final call | - | Balance |

| On Application | ₹ 25 |

| On Allotment | ₹ 25 |

| On First and Final Call | The balance amount |