Question 16 Marks

Calculate Trade Receivables Turnover Ratio in the following:

Case: Cost of Revenue from Operations or Cost of Goods Sold ₹ 4,50,000; Gross Profit on Sales 20%; Cash Sales 25% of Net Credit Sales, Opening Trade Receivables ₹ 90,000; Closing Trade Receivables ₹ 60,000.

Case: Cost of Revenue from Operations or Cost of Goods Sold ₹ 4,50,000; Gross Profit on Sales 20%; Cash Sales 25% of Net Credit Sales, Opening Trade Receivables ₹ 90,000; Closing Trade Receivables ₹ 60,000.

Answer

View full question & answer→Case:

Let Sales be = x.

$\text{Gross Profit}=\text{x}\times\frac{20}{100}$

$=\frac{20\text{x}}{100}$

Sales = Cost of Goods Sold + Gross Profit

or, $\text{x} = 4,50,000+\frac{20\text{x}}{100}$

or, $\text{x}-\frac{20}{100}=4,50,000$

or, $\text{x}=\frac{4,50,000\times100}{80}$

= 5,62,500

Sales = x ₹ 5,62,500

Let Credit Sales be = a

$\text{Case Sales}=\text{a}\times\frac{25}{100}$

$=\frac{25\text{a}}{100}$

Sales = Case Sales + Credit sales

or, $5,62,500=\frac{25\text{a}}{100}+\text{a}$

or, $\text{a}=\frac{5,62,500\times100}{125}$

= 4,50,000

Credit Sales = a = 4,50,000

Average Trade Receivables $=\frac{\text{Opning Trade Receivable + Closing Trade Receivables}}{2}$

Average Trade Receivables $=\frac{90,000+60,000}{2}$

= 75,000

Trade Receivable Turnover Ratio $=\frac{\text{Net Credit Sales}}{\text{Average Trade Receivables}}$

Trade Receivable Turnover Ratio $=\frac{4,50,000}{75,000}=6\text{ Times}$

Let Sales be = x.

$\text{Gross Profit}=\text{x}\times\frac{20}{100}$

$=\frac{20\text{x}}{100}$

Sales = Cost of Goods Sold + Gross Profit

or, $\text{x} = 4,50,000+\frac{20\text{x}}{100}$

or, $\text{x}-\frac{20}{100}=4,50,000$

or, $\text{x}=\frac{4,50,000\times100}{80}$

= 5,62,500

Sales = x ₹ 5,62,500

Let Credit Sales be = a

$\text{Case Sales}=\text{a}\times\frac{25}{100}$

$=\frac{25\text{a}}{100}$

Sales = Case Sales + Credit sales

or, $5,62,500=\frac{25\text{a}}{100}+\text{a}$

or, $\text{a}=\frac{5,62,500\times100}{125}$

= 4,50,000

Credit Sales = a = 4,50,000

Average Trade Receivables $=\frac{\text{Opning Trade Receivable + Closing Trade Receivables}}{2}$

Average Trade Receivables $=\frac{90,000+60,000}{2}$

= 75,000

Trade Receivable Turnover Ratio $=\frac{\text{Net Credit Sales}}{\text{Average Trade Receivables}}$

Trade Receivable Turnover Ratio $=\frac{4,50,000}{75,000}=6\text{ Times}$

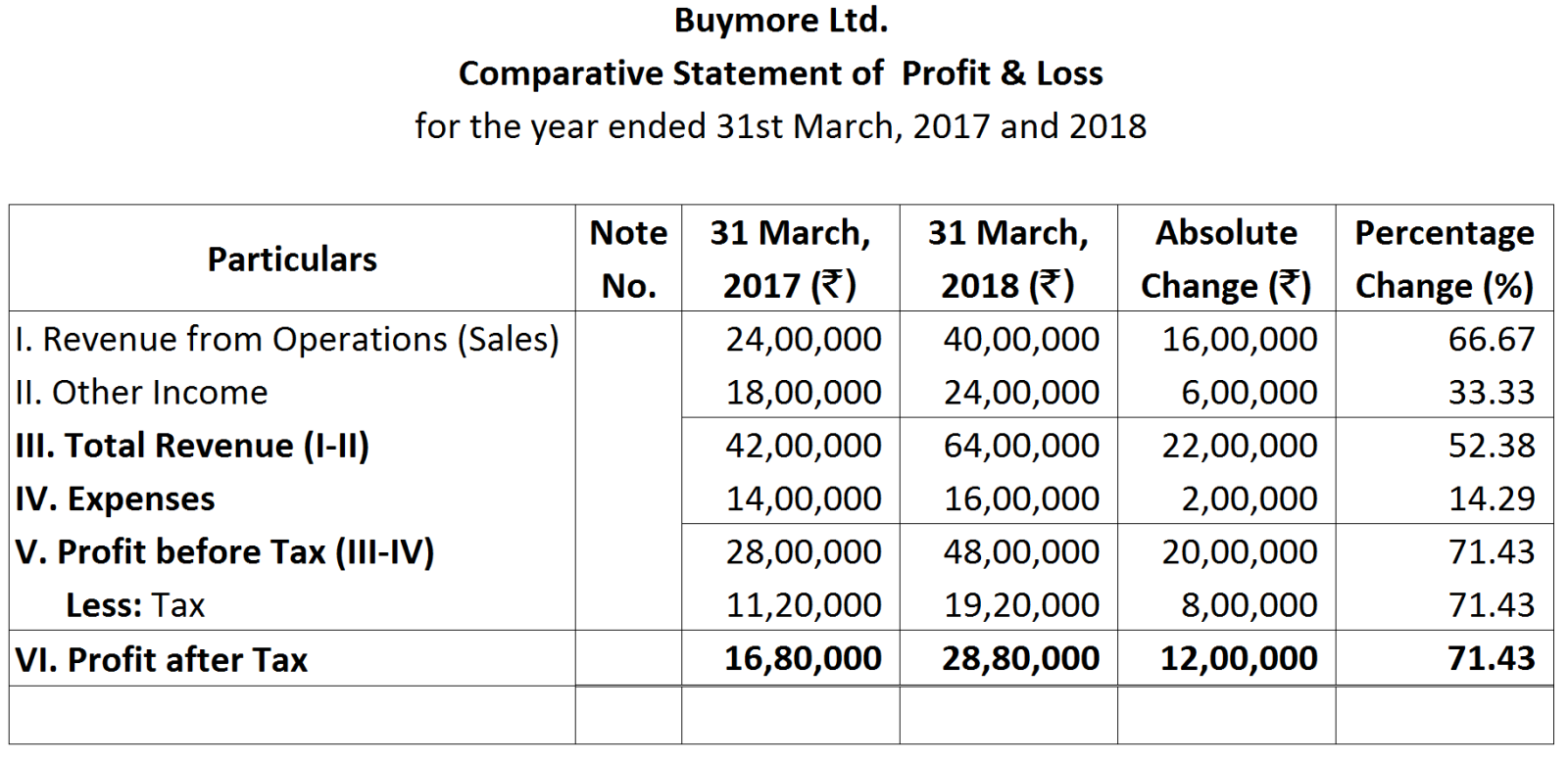

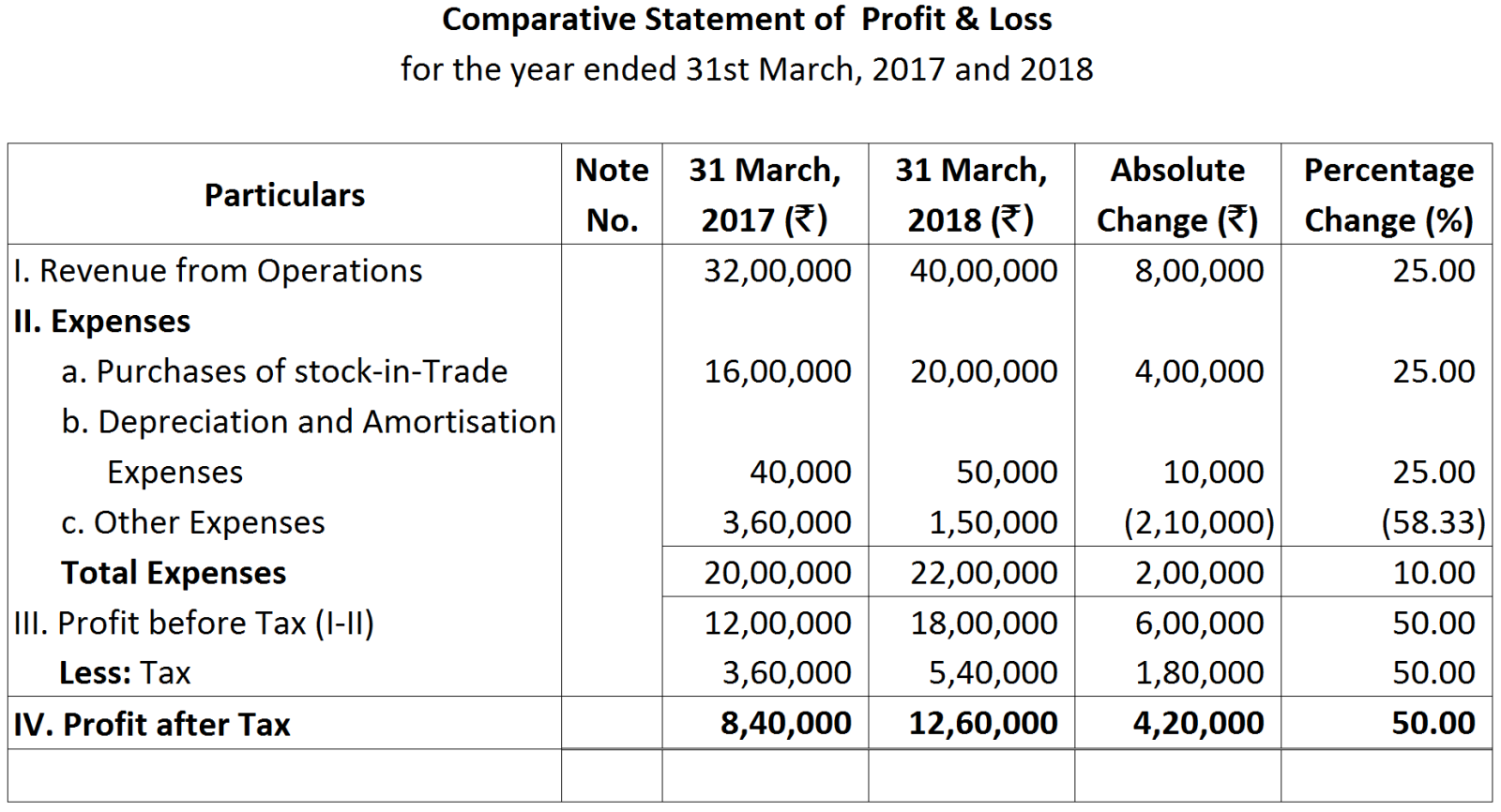

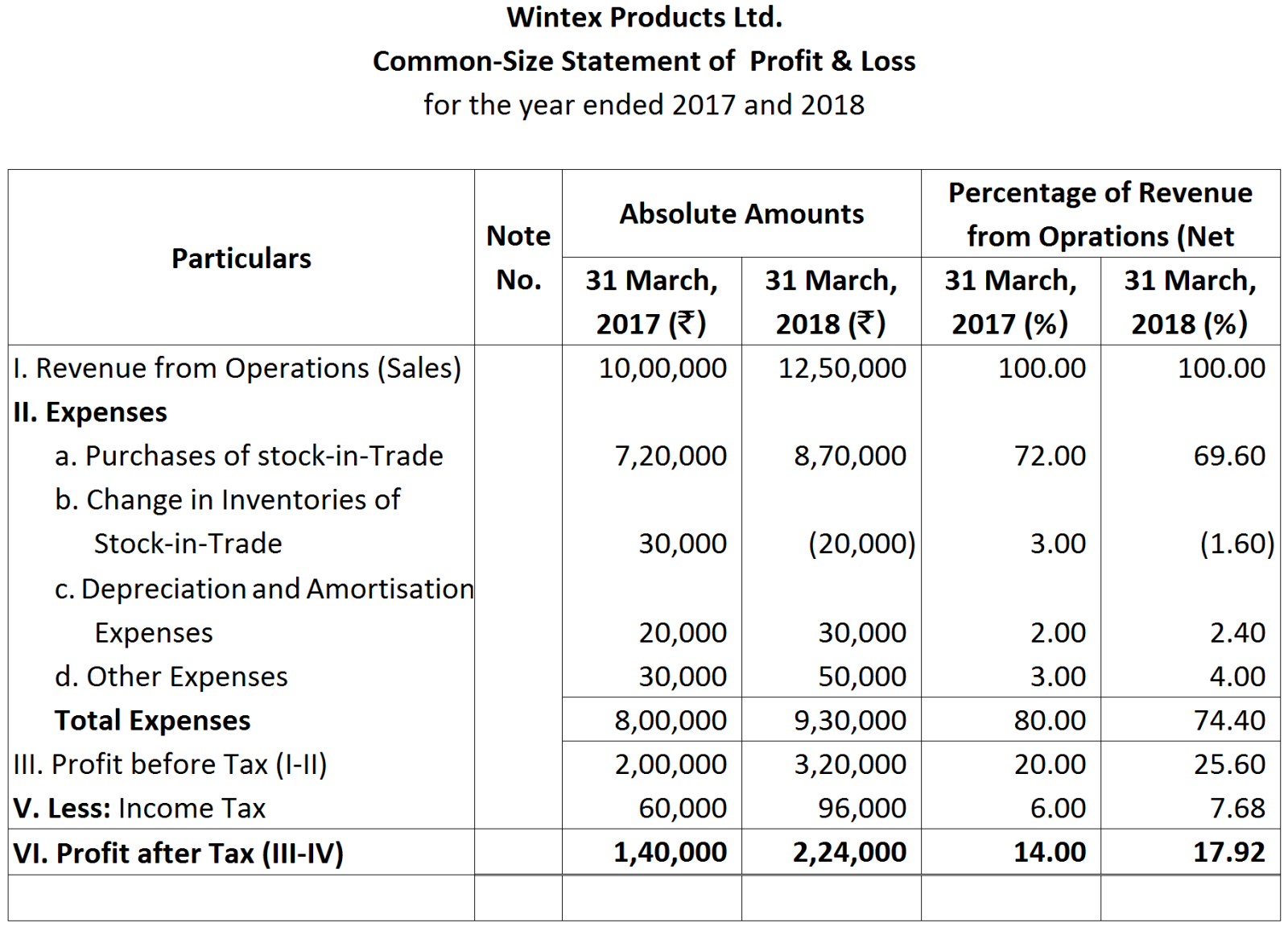

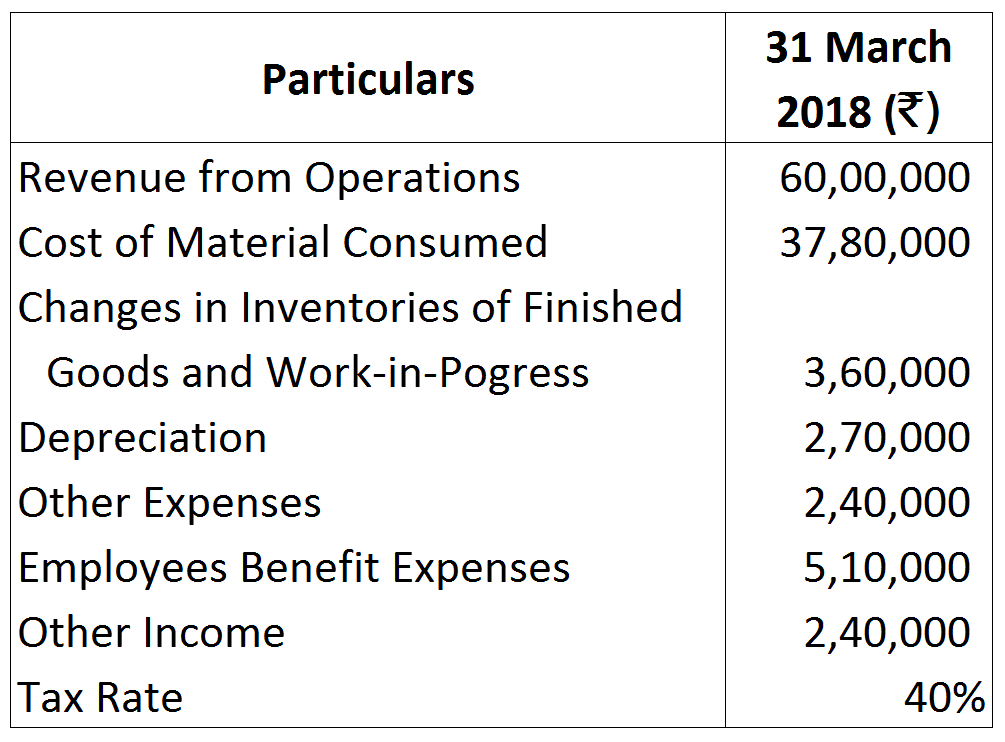

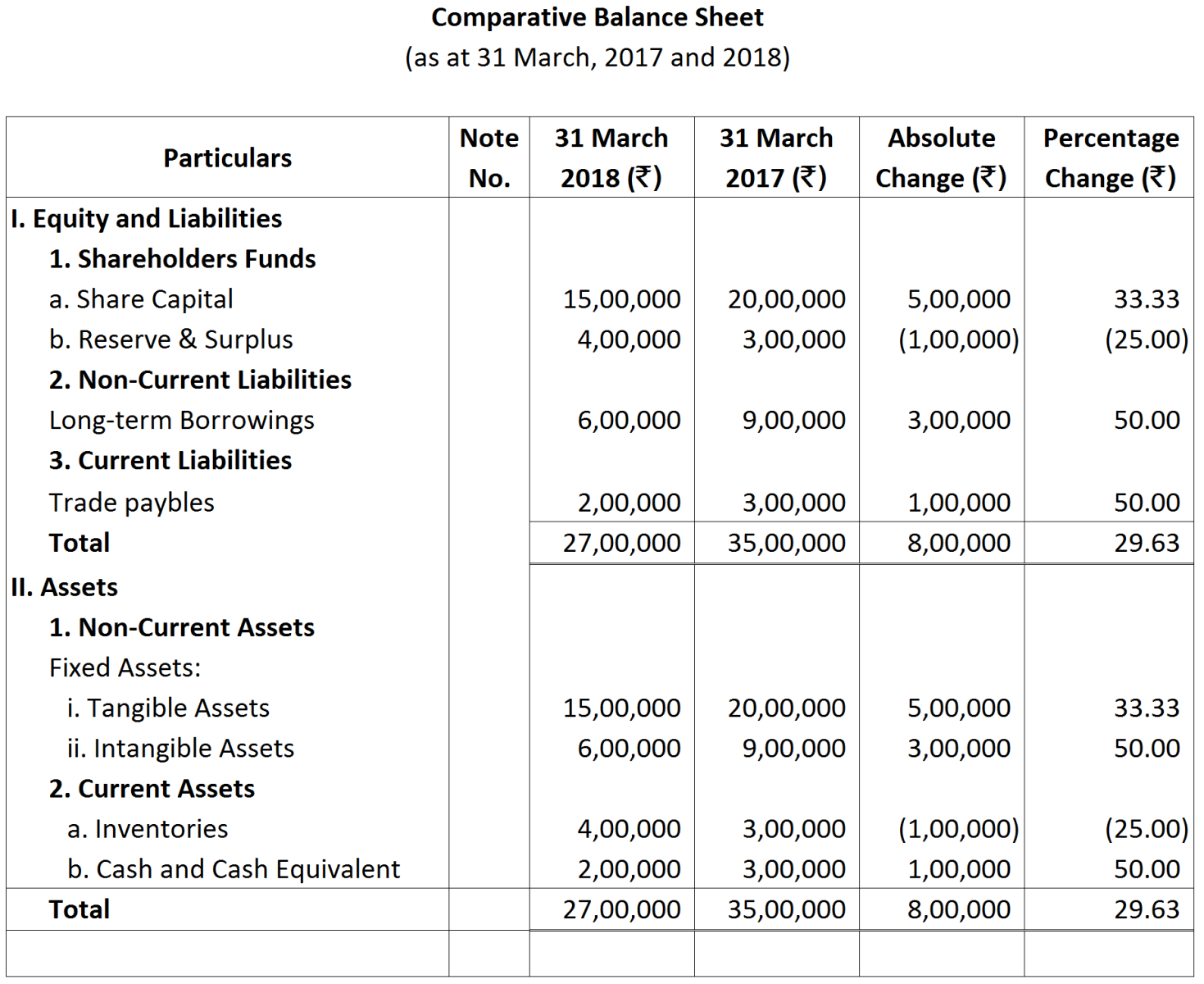

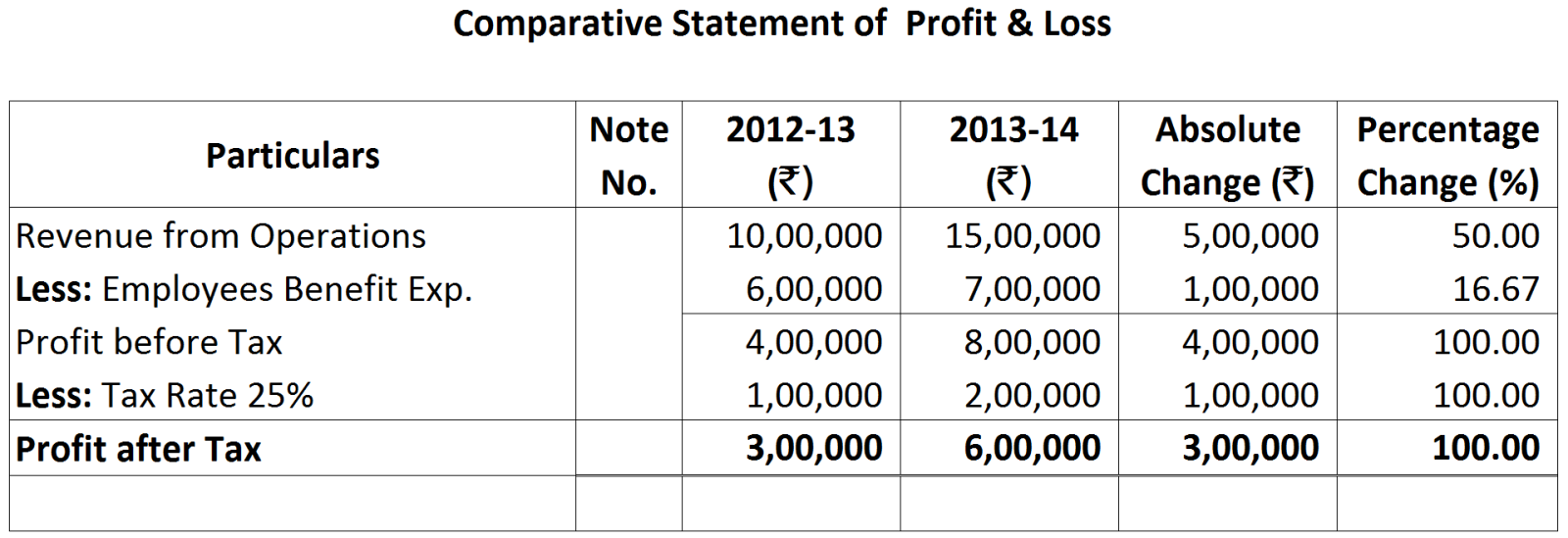

From the above Comparative Statement of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Net Profit ratio.

From the above Comparative Statement of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Net Profit ratio. From the above Comparative Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Operating ratio.

From the above Comparative Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Operating ratio. From the above, Compute Operating Ratio.

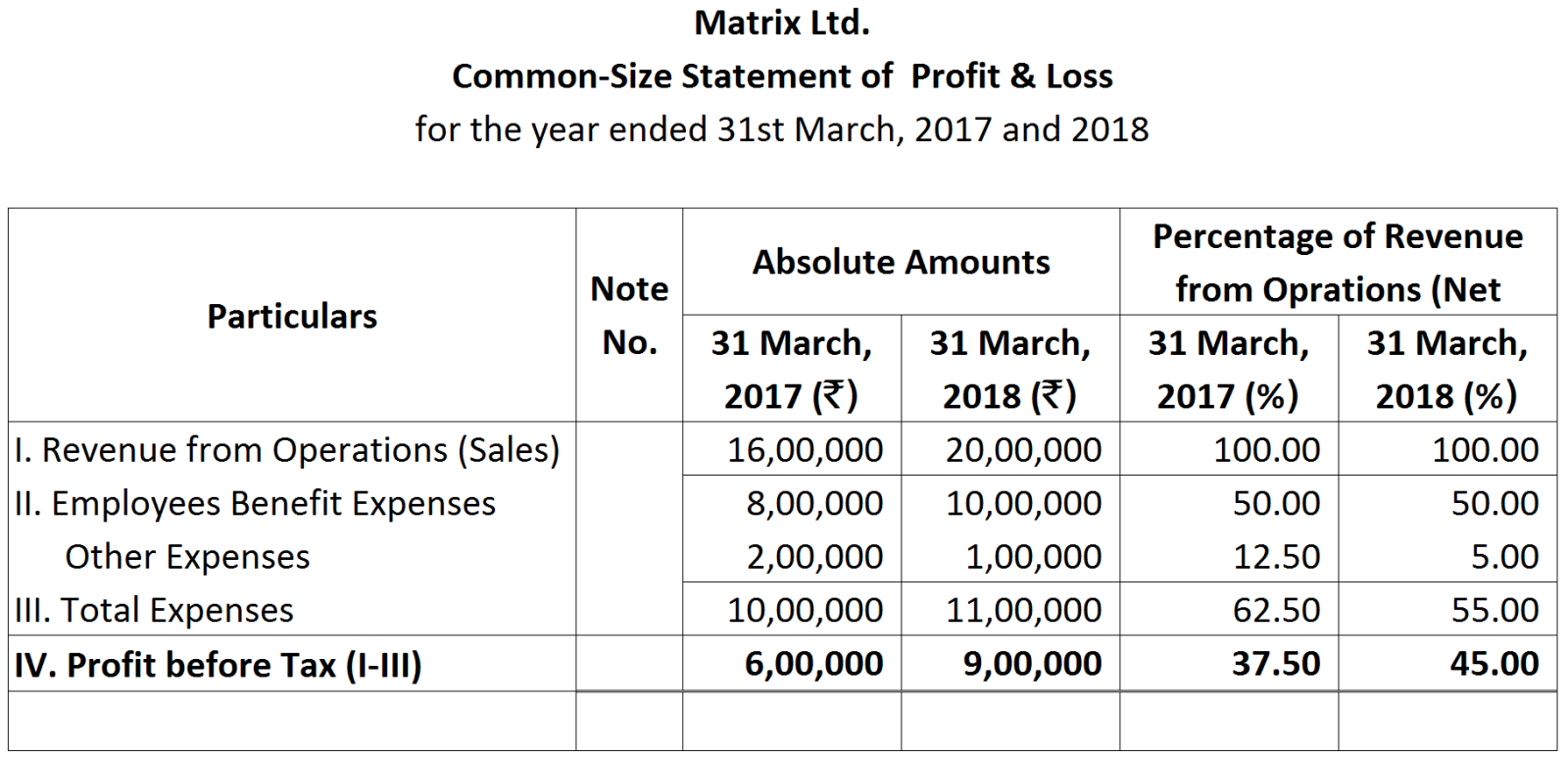

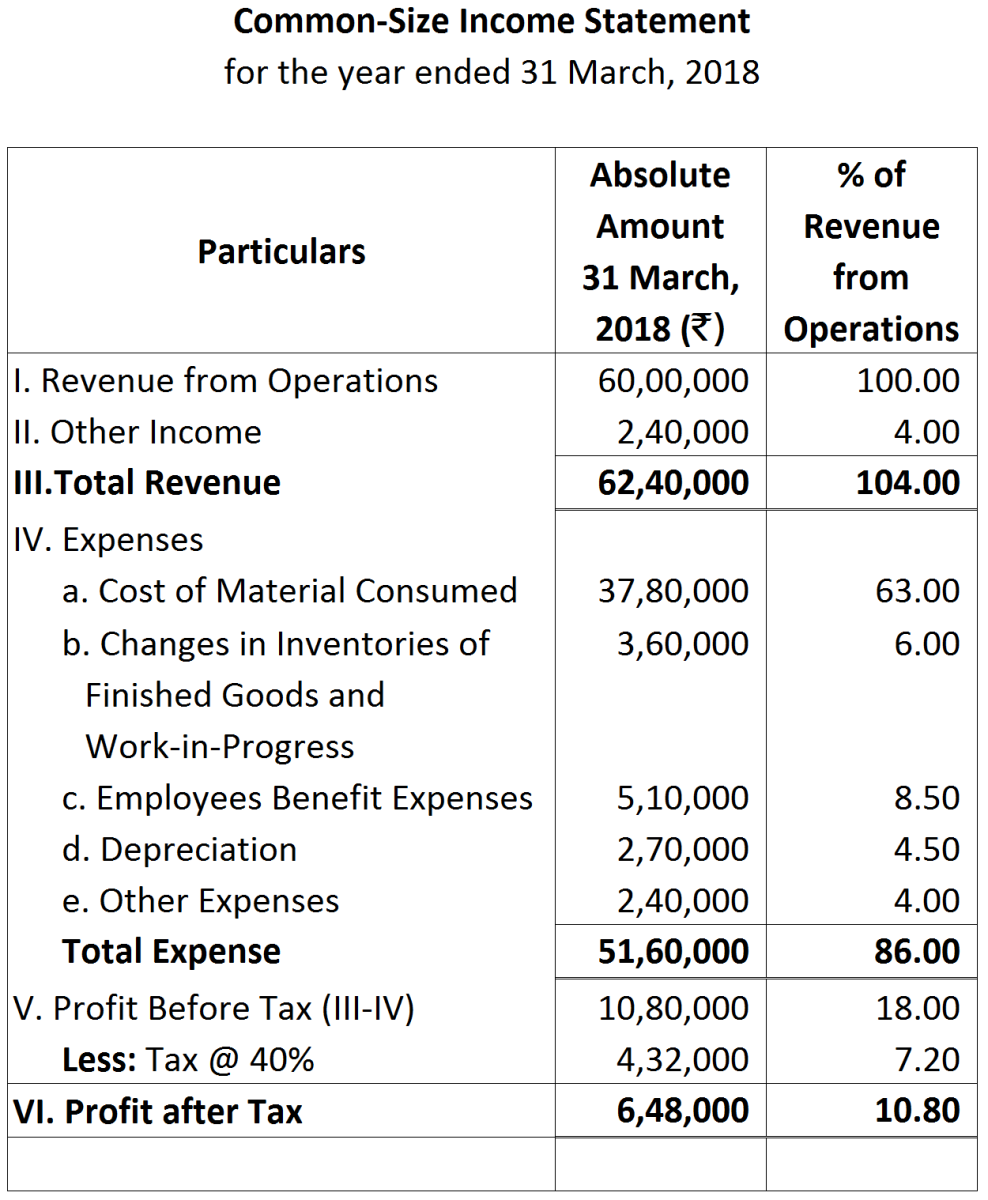

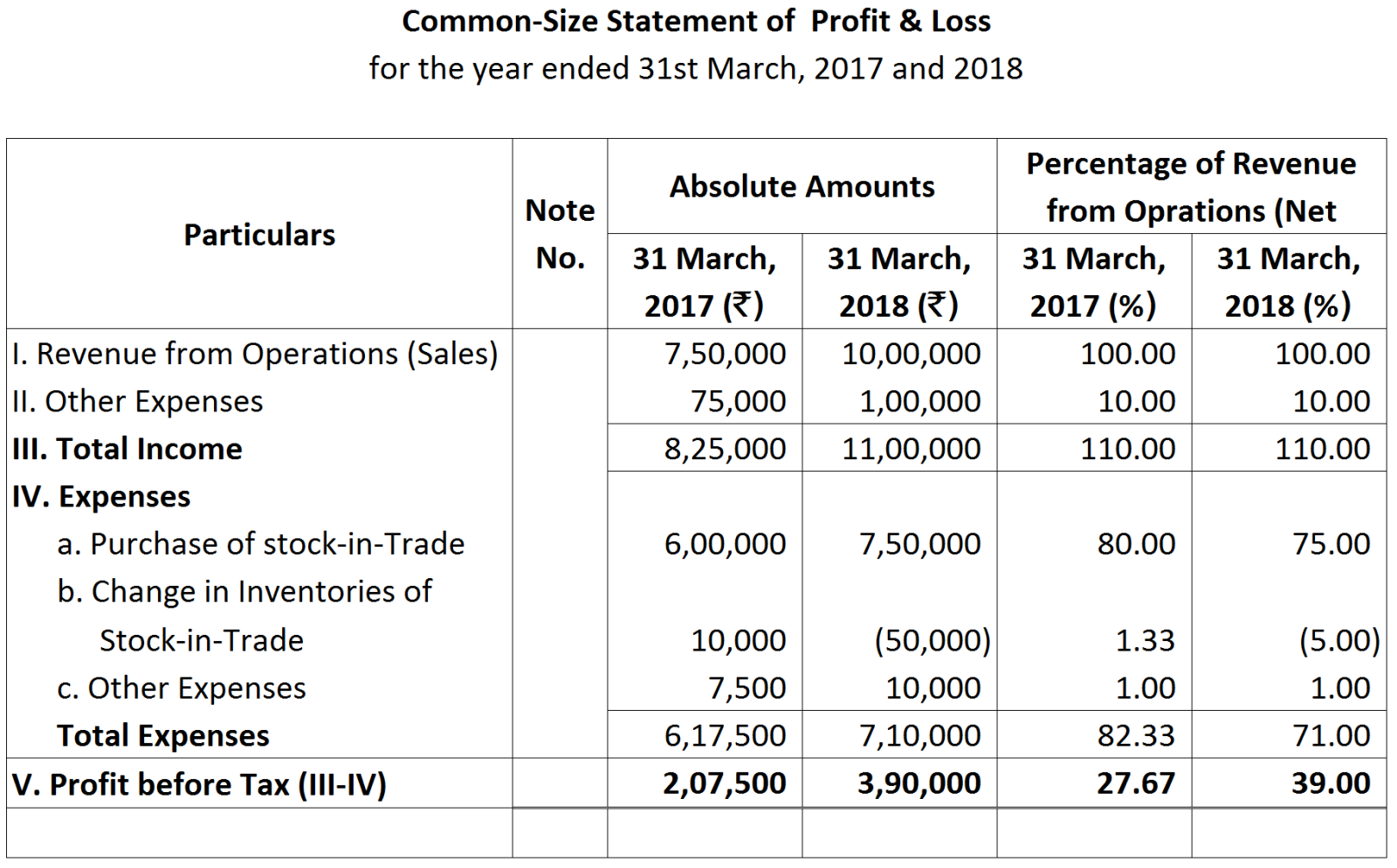

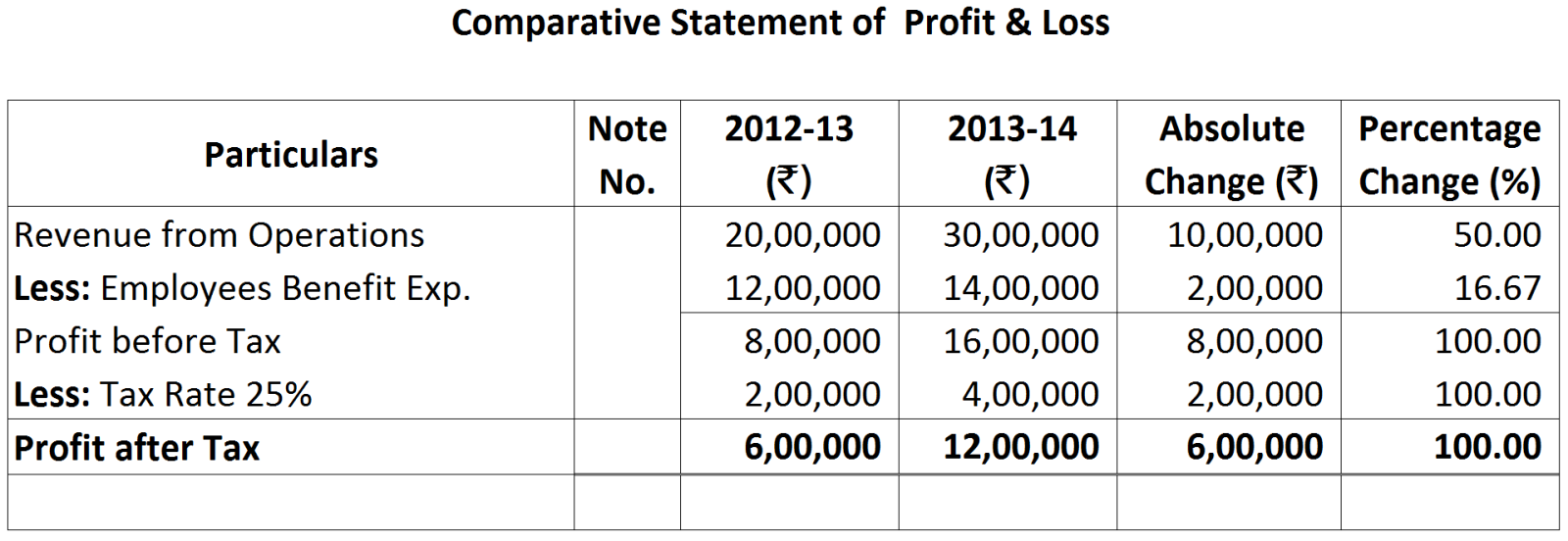

From the above, Compute Operating Ratio. From the above Common-size Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Gross Profit ratio.

From the above Common-size Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Gross Profit ratio.

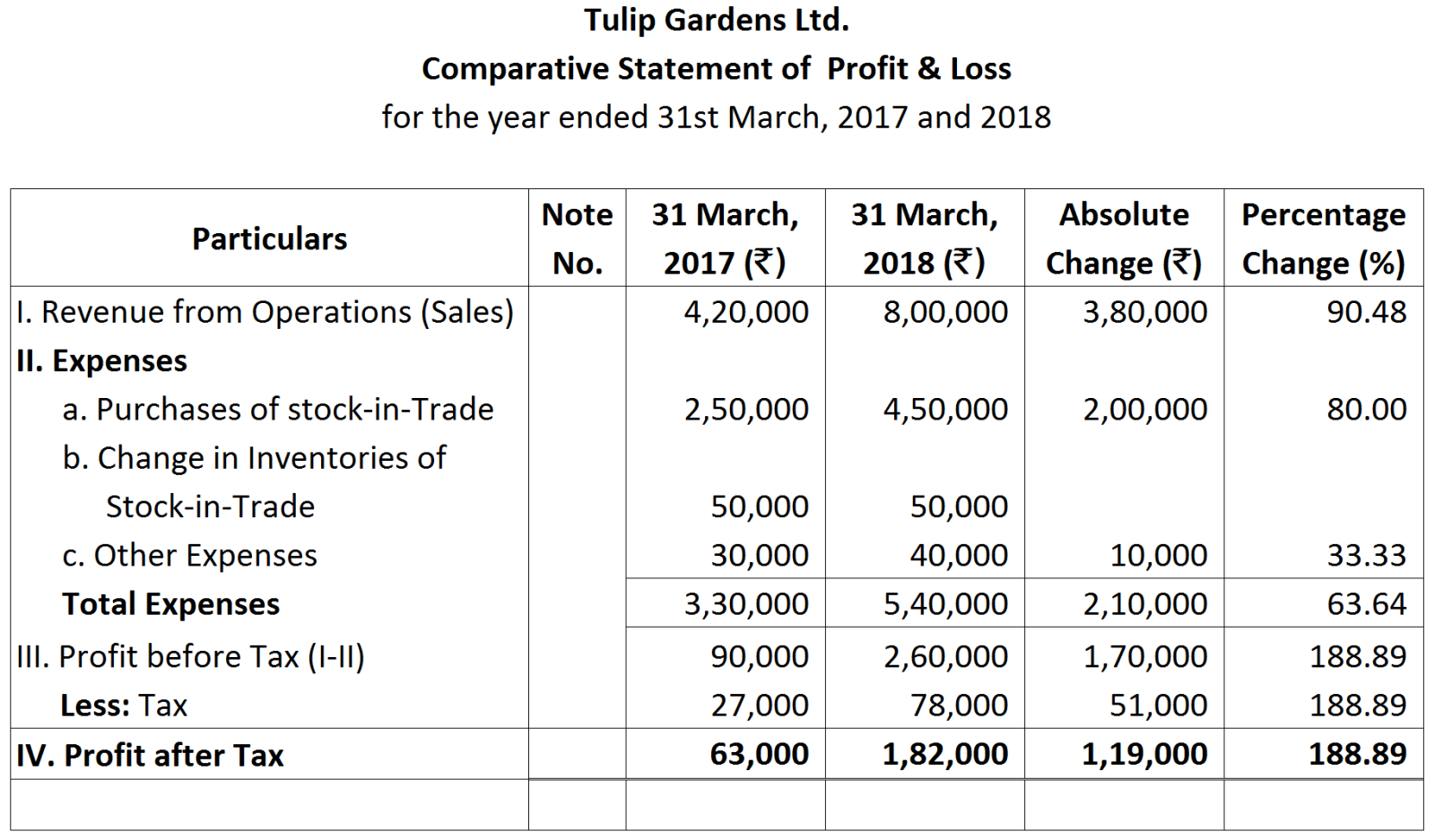

From the above Comparative Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Gross Profit ratio.

From the above Comparative Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Gross Profit ratio.

Net Profit Ratio $\frac{\text{Net Profit After Tax}}{\text{Revenue from Operation}}\times100$

Net Profit Ratio $\frac{\text{Net Profit After Tax}}{\text{Revenue from Operation}}\times100$

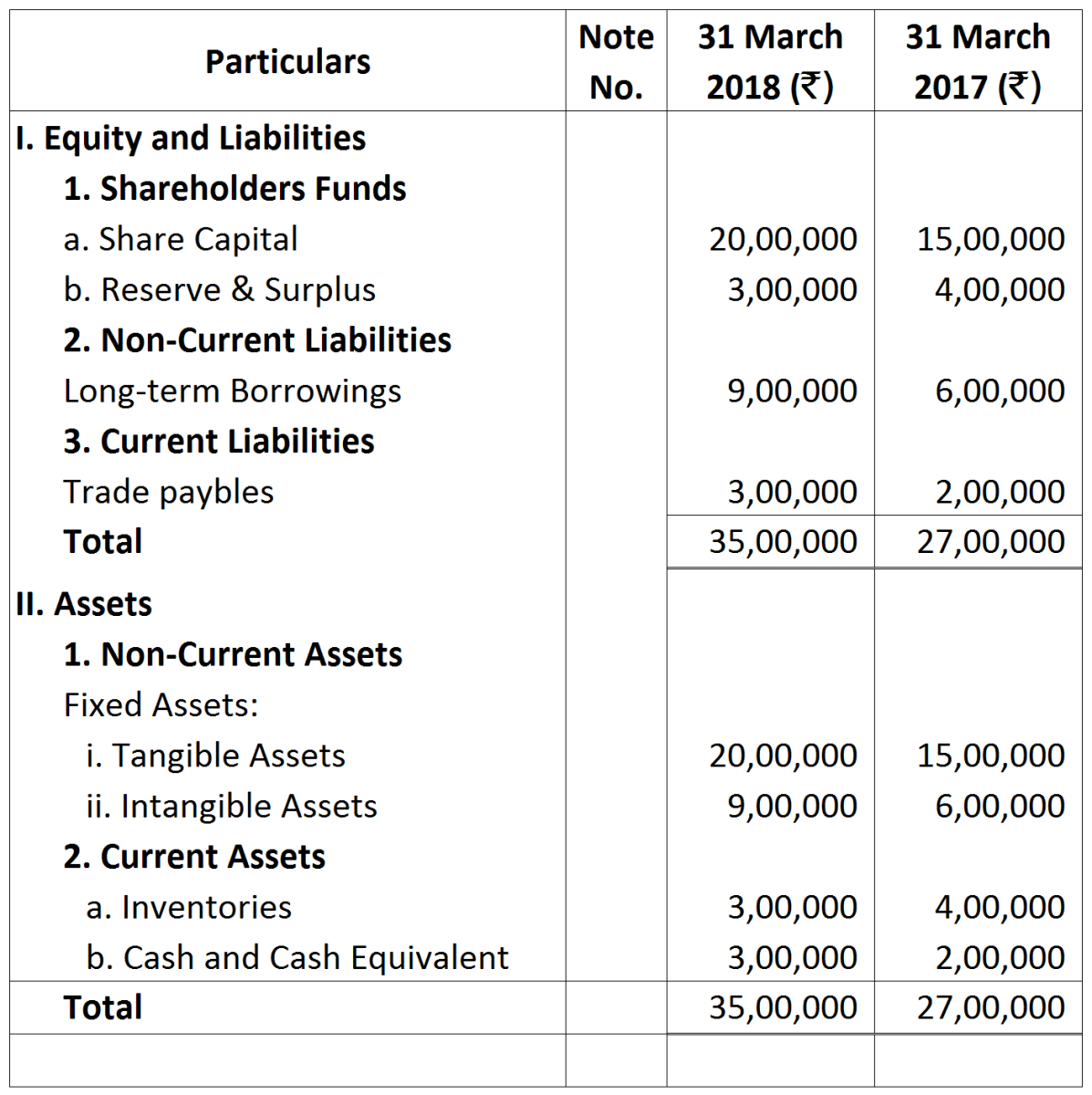

Debt to Equity Ratio $=\frac{\text{Long-term Debts}}{\text{Shareholders' Funds}}$

Debt to Equity Ratio $=\frac{\text{Long-term Debts}}{\text{Shareholders' Funds}}$ From the above, Compute Operating Ratio.

From the above, Compute Operating Ratio.

Proprietary Ratio $=\frac{\text{Shareholders' Funds}}{\text{Total Assets}}$

Proprietary Ratio $=\frac{\text{Shareholders' Funds}}{\text{Total Assets}}$

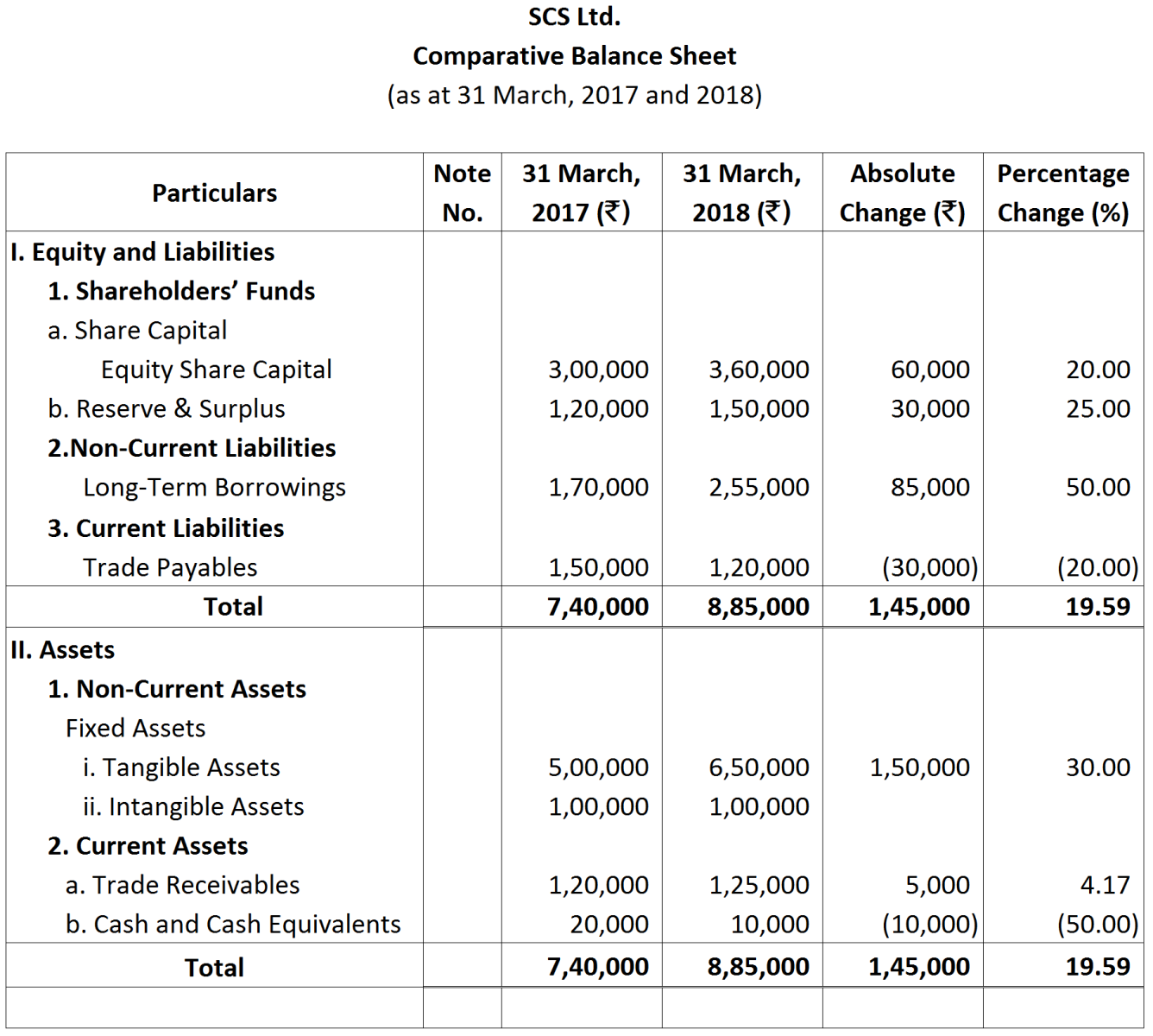

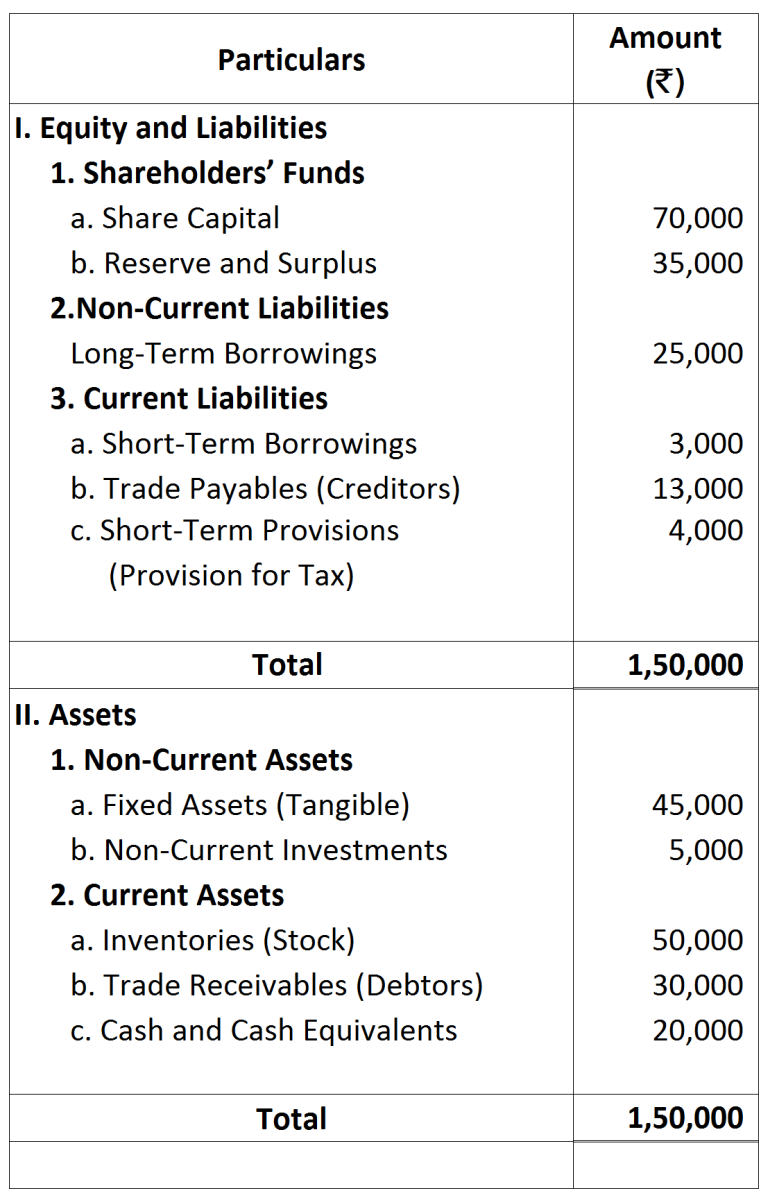

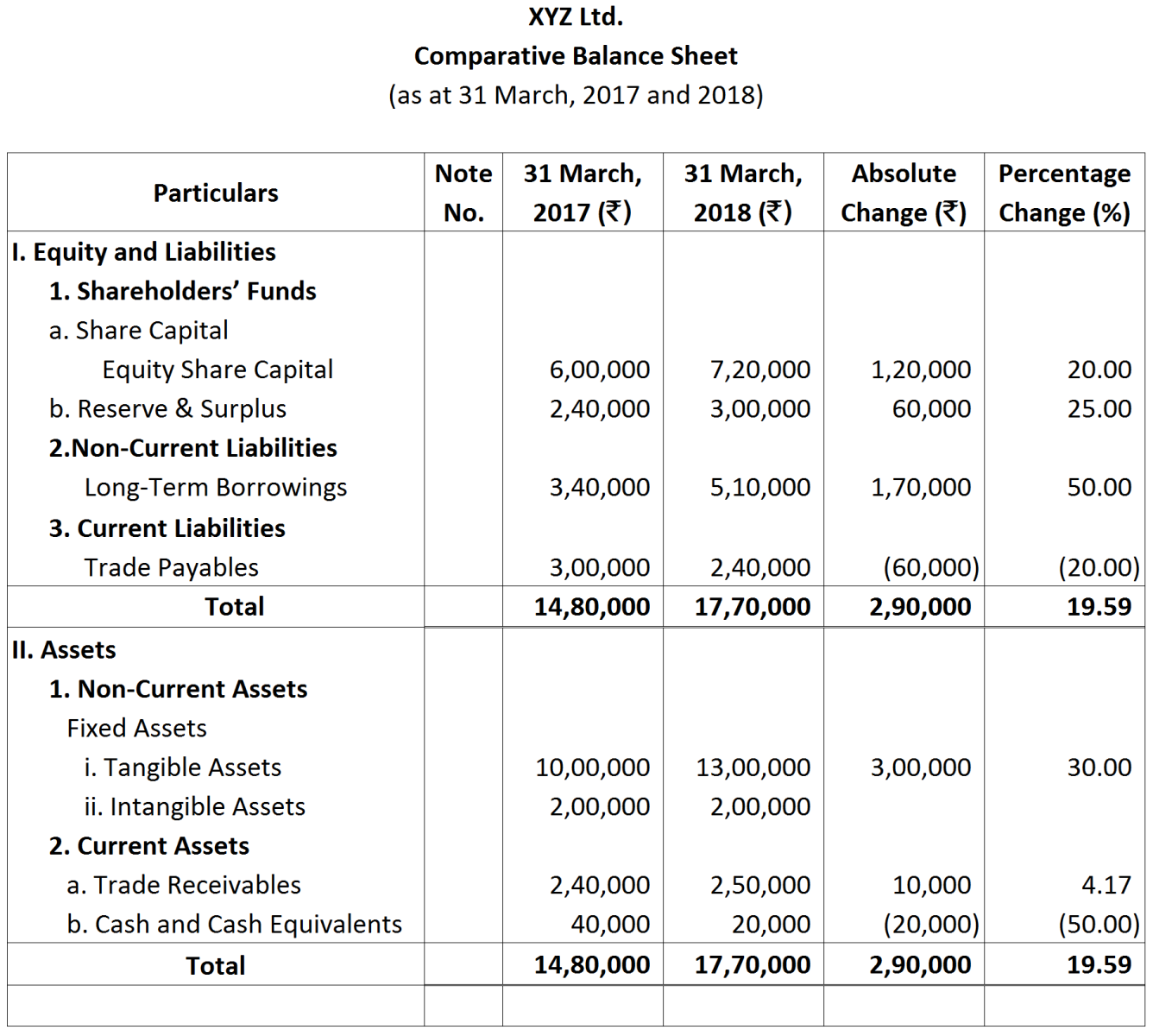

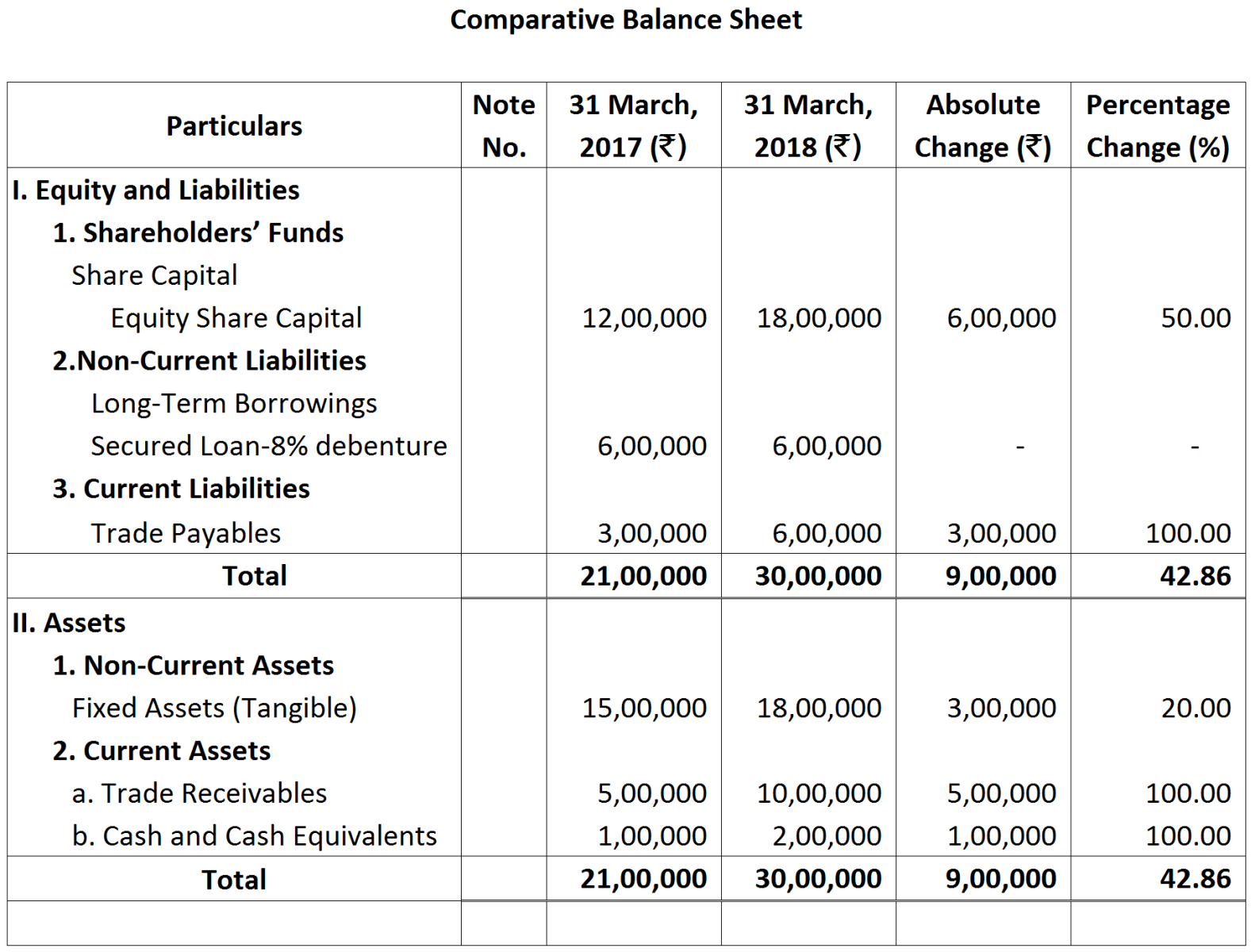

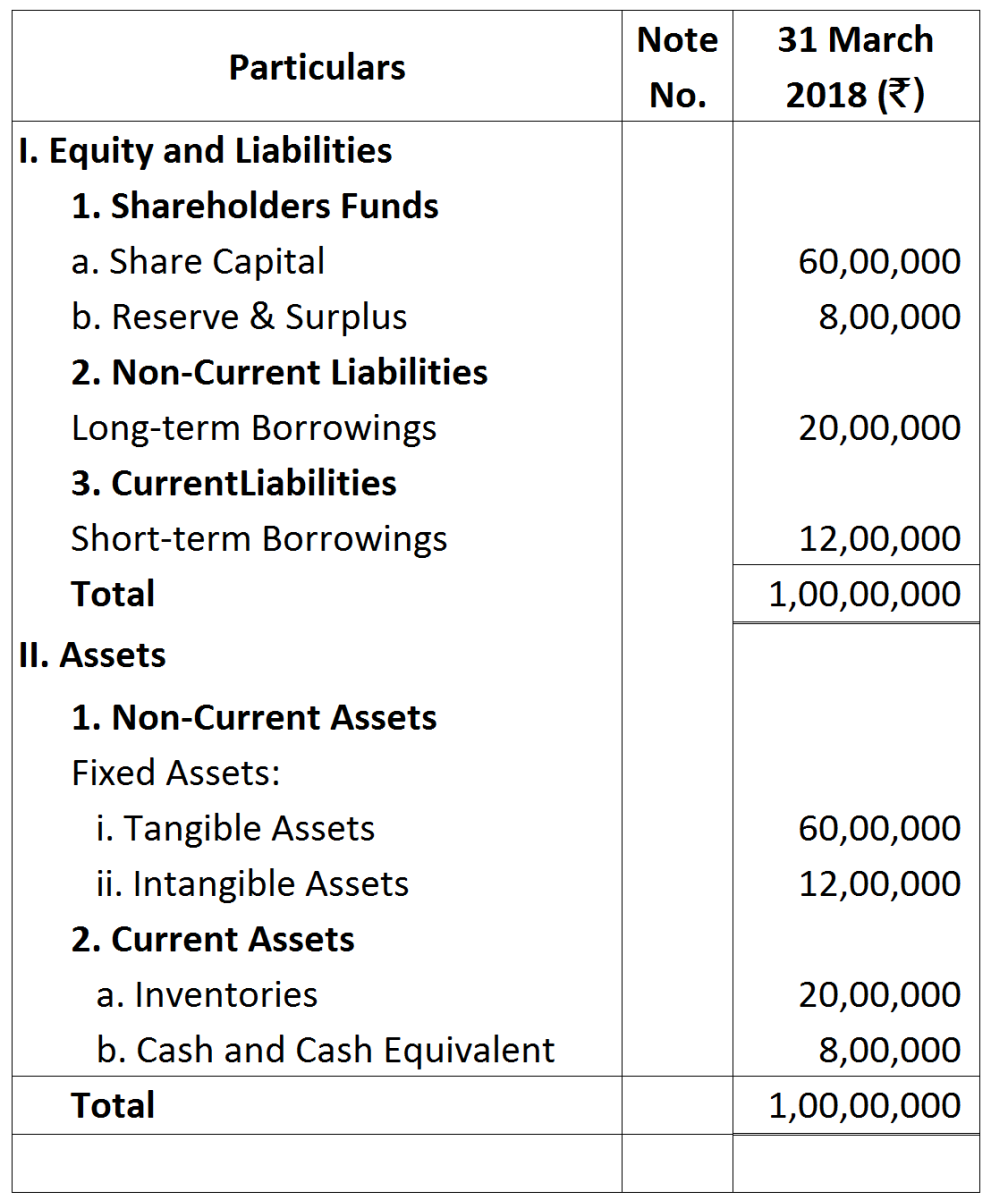

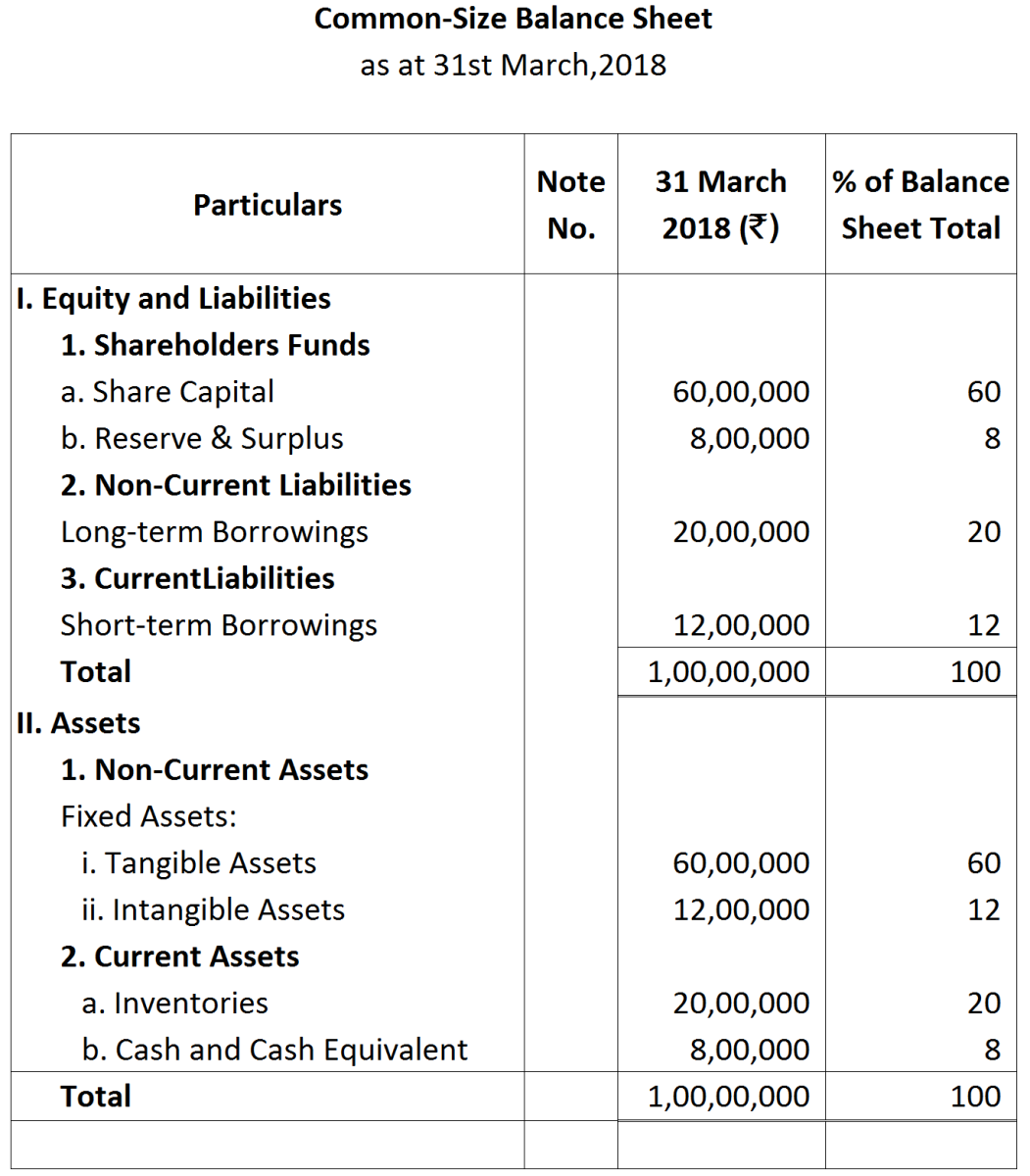

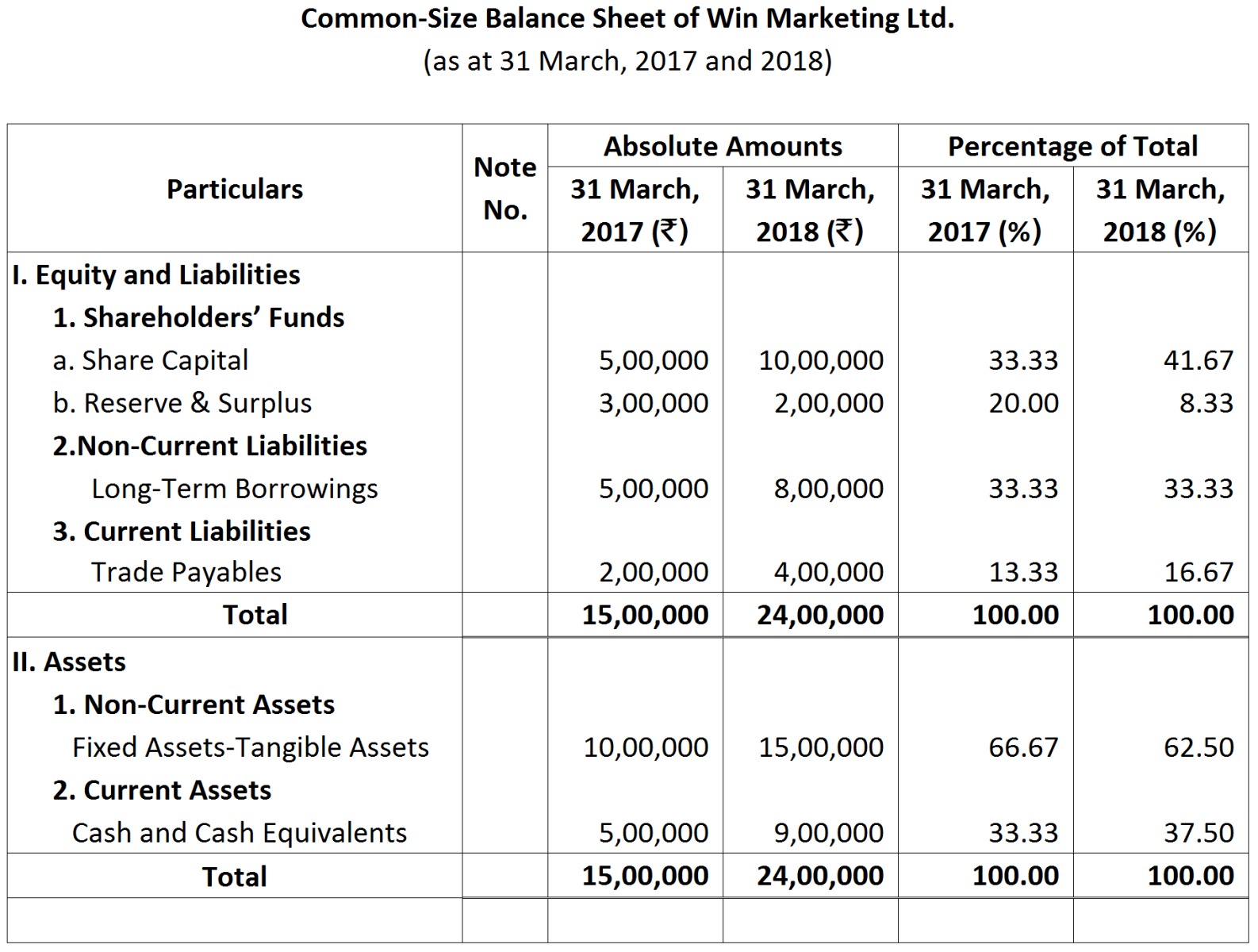

From the above Common-size Balance Sheet as at 31st March, 2018, compute current Ratio, Quick Ratio, Total Assets to Debt Ratio, and Dept to Equity Ratio.

From the above Common-size Balance Sheet as at 31st March, 2018, compute current Ratio, Quick Ratio, Total Assets to Debt Ratio, and Dept to Equity Ratio.