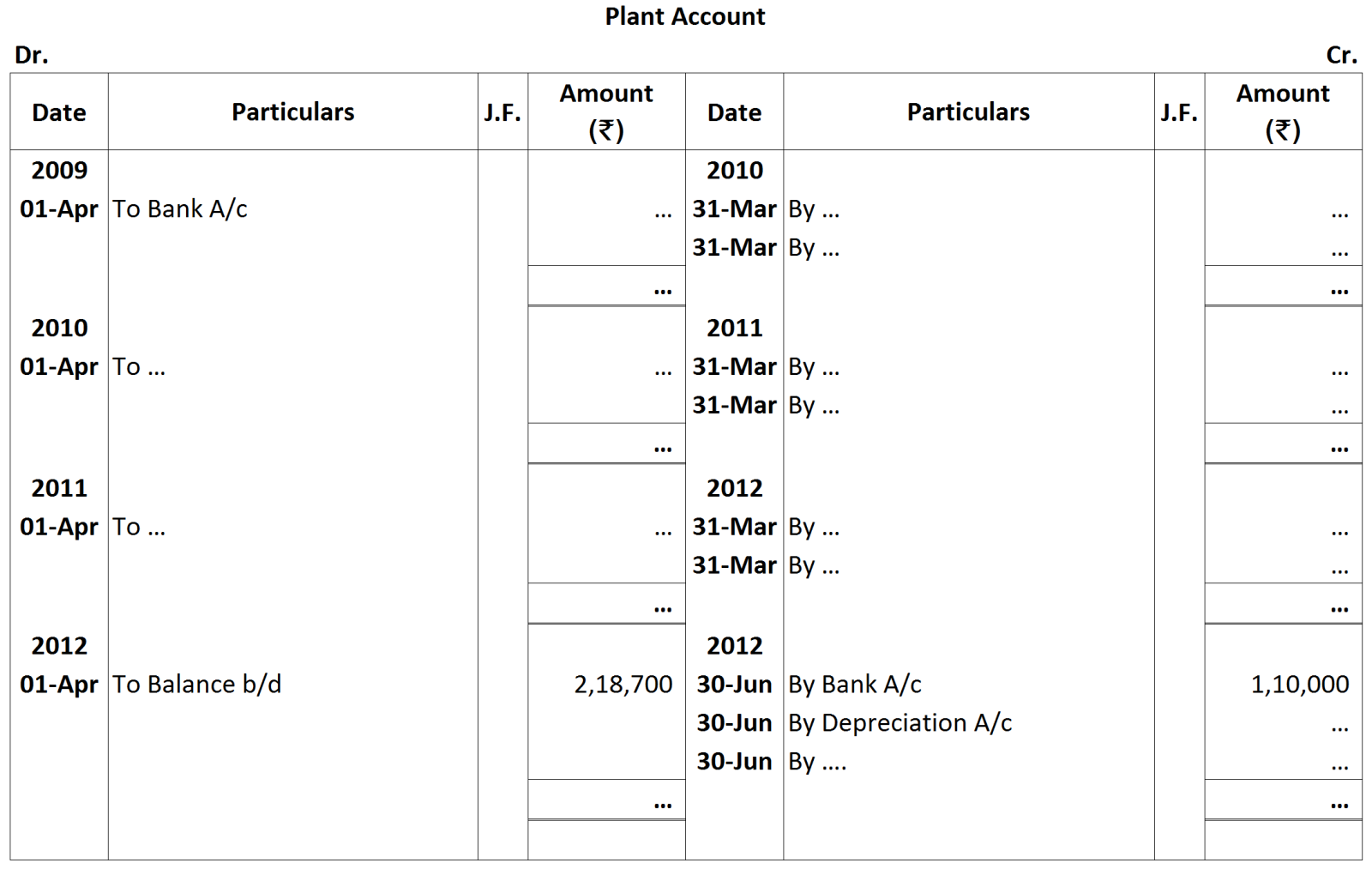

Question

Mohit has the following transactions, prepare accounting equation:

(Ans: Cash ₹ 1,32,500 + Goods ₹ 32,500 + Furniture ₹ 10,000 = ₹ 1,75,000; Liabilition = Capital ₹ 1,75,000)

|

a.

|

Business started with cash

|

₹ 1,75,000

|

|

b.

|

Purchased goods from Rohit

|

₹ 50,000

|

|

c.

|

Sales goods on credit to Manish (Costing ₹ 17,500)

|

₹ 20,000

|

|

d.

|

Purchased furniture for office use

|

₹ 10,000

|

|

e.

|

Cash paid to Rohit in full settlement

|

₹ 48,500

|

|

f.

|

Cash received from Manish

|

₹ 20,000

|

|

g.

|

Rent paid

|

₹ 1,000

|

|

h.

|

Cash withdrew for personal use

|

₹ 3,000

|