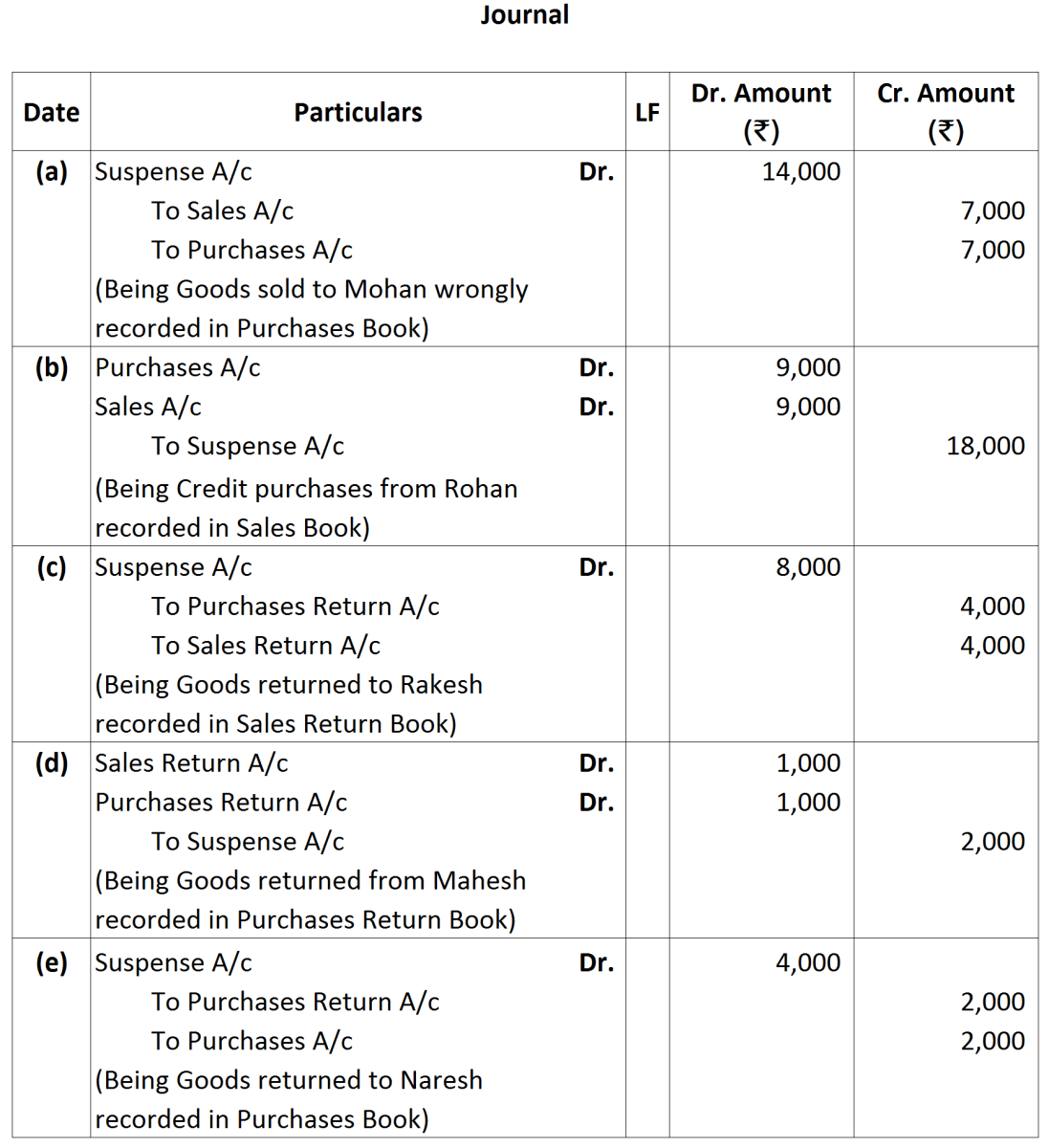

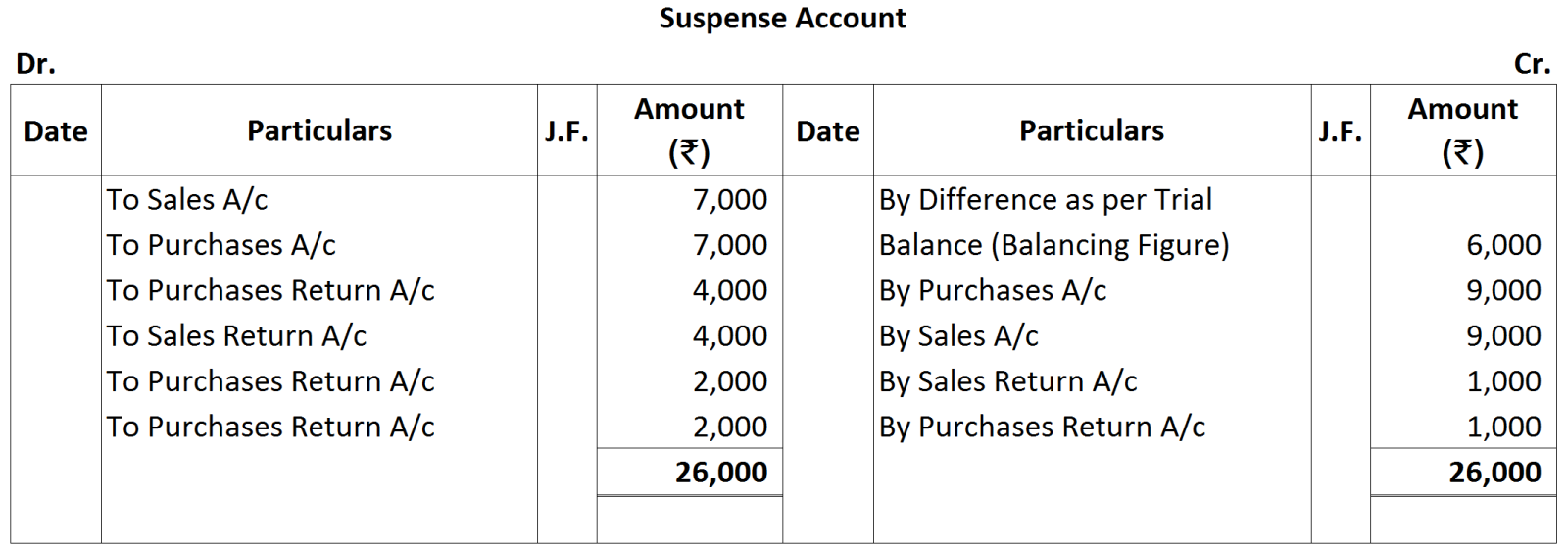

Question

Rectify the following errors assuming that Suspense Account was opened. Ascertain the difference in Trial Balance.

- Credit sales to Mohan ₹ 7,000 were recorded in Purchase Book. However, Mohan's Account was correctly debited.

- Credit purchases from Rohan ₹ 9,000 were recorded in Sales Book. However, Rohan's Account was correctly credited.

- Goods returned to Rakesh ₹ 4,000 were recorded in Sale Returns Book. However, Rakesh's Account was correctly debited.

- Goods returned from Mahesh ₹ 1,000 were recorded through Purchase Returns Book. However, Mahesh's Account was correctly credited.

- Goods returned to Naresh ₹ 2,000 were recorded through Purchases Book. However, Naresh's Account was correctly debited.