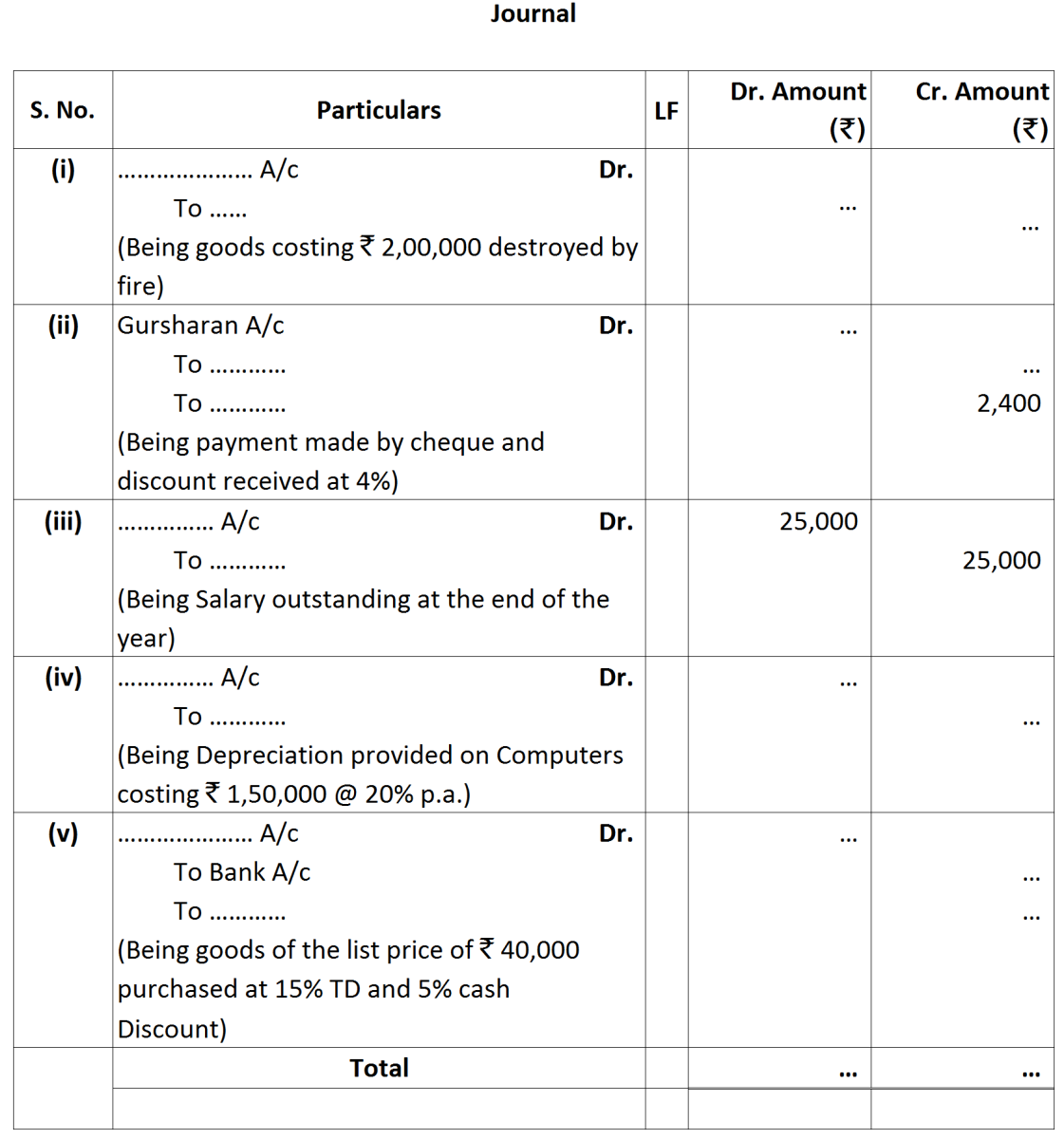

Question

What are the rules of posting in the Ledger?

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

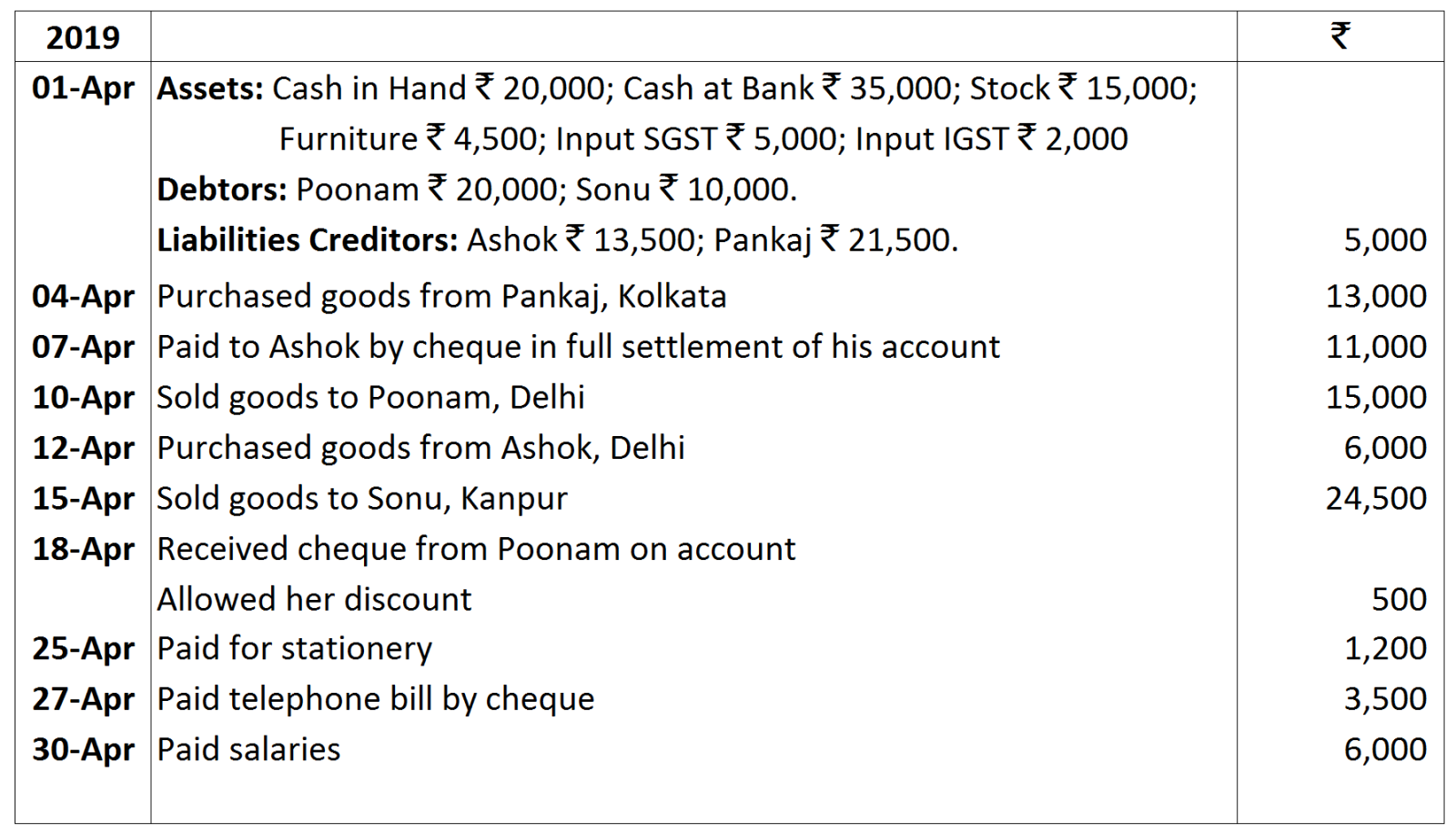

2019

|

|

₹

|

|

March $1$

|

Cash in Hand

|

$2,20,000$ |

| Cash at Bank | $60,000$ | |

| March $3$ | Deposited in Bank | $80,000$ |

| March $4$ | Goods purchased and issued a cheque for the same | $34,000$ |

| March $7$ | Cash Purchases | $16,000$ |

| March $8$ | Paid Commission by cheque | $12,000$ |

|

March $9$

|

Withdrew from bank for personal use

|

$2,500$

|

|

March $12$

|

Received from Ved in full settlement of his account of $₹\ 6,000,$ half of the amount was deposited into bank on the same day

|

|

|

March $16$

|

Interest collected by Bank

|

$14,000$

|

|

March $20$

|

Cash Sales

|

$42,000$

|

|

March $22$

|

Salaries paid

|

$40,000$ |

| March $22$ | Goods sold to Mona & Co. | $36,000$ |

| March $23$ | Received cheque from Mona & Co. after discount of $₹\ 300$ | $35,000$ |

| March $26$ | Deposited the cheque received from Mona & Co. into Bank |

|

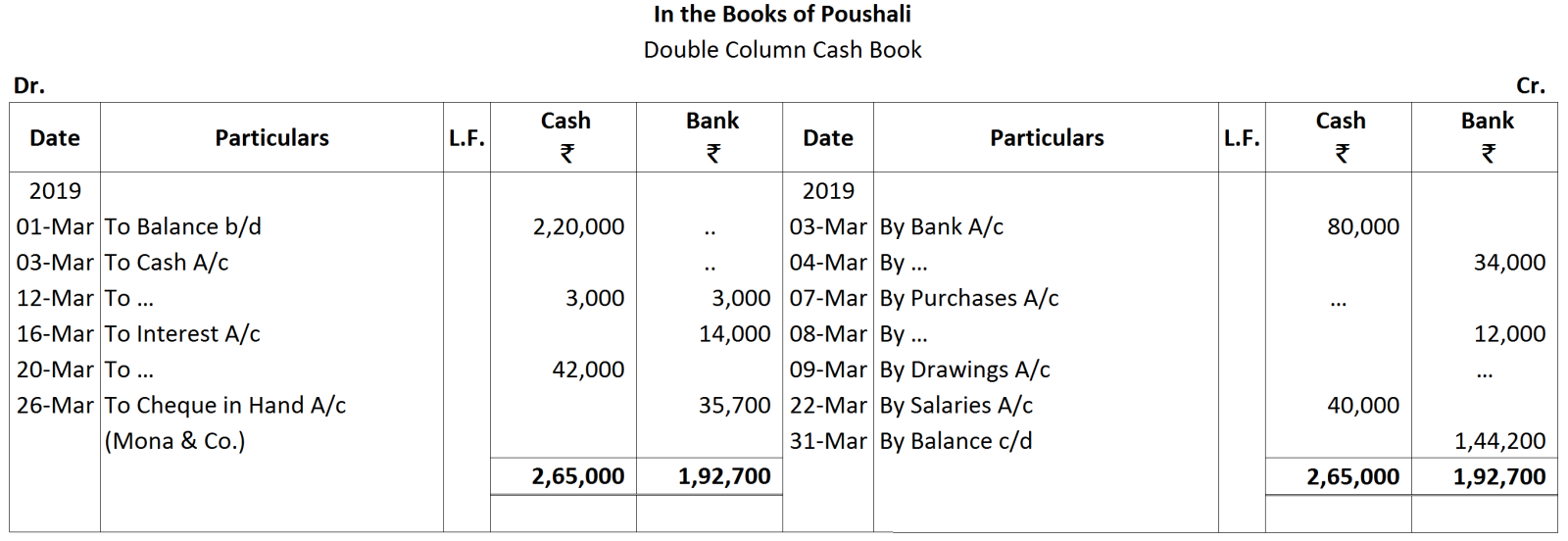

2016

|

|

(₹)

|

|

April 2

|

Taxi fare

|

750

|

|

April 3

|

Refreshments

|

450

|

|

April 5

|

Registered postal charges

|

200

|

|

April 5

|

Wages

|

700

|

|

April 8

|

Auto fare

|

200

|

|

April 9

|

Courier charges

|

150

|

|

April 12

|

Postal Stamps

|

600

|

|

April 14

|

Eraser/ Sharpeners/ Pencils

|

400

|

|

April 17

|

Speed Post charges

|

200

|

|

April 20

|

Cartage

|

600

|

|

April 20

|

Computer Stationery

|

500

|

|

April 22

|

Wages

|

300

|

|

April 24

|

Bus fare

|

600

|

|

April 25

|

Office Sanitation

|

800

|

|

April 26

|

Refreshments

|

750

|

|

April 28

|

Loading Charges

|

300

|

|

April 30

|

Photostatting Charges

|

200

|

|

April 30

|

Wages

|

800

|

|

|

|

₹

|

|

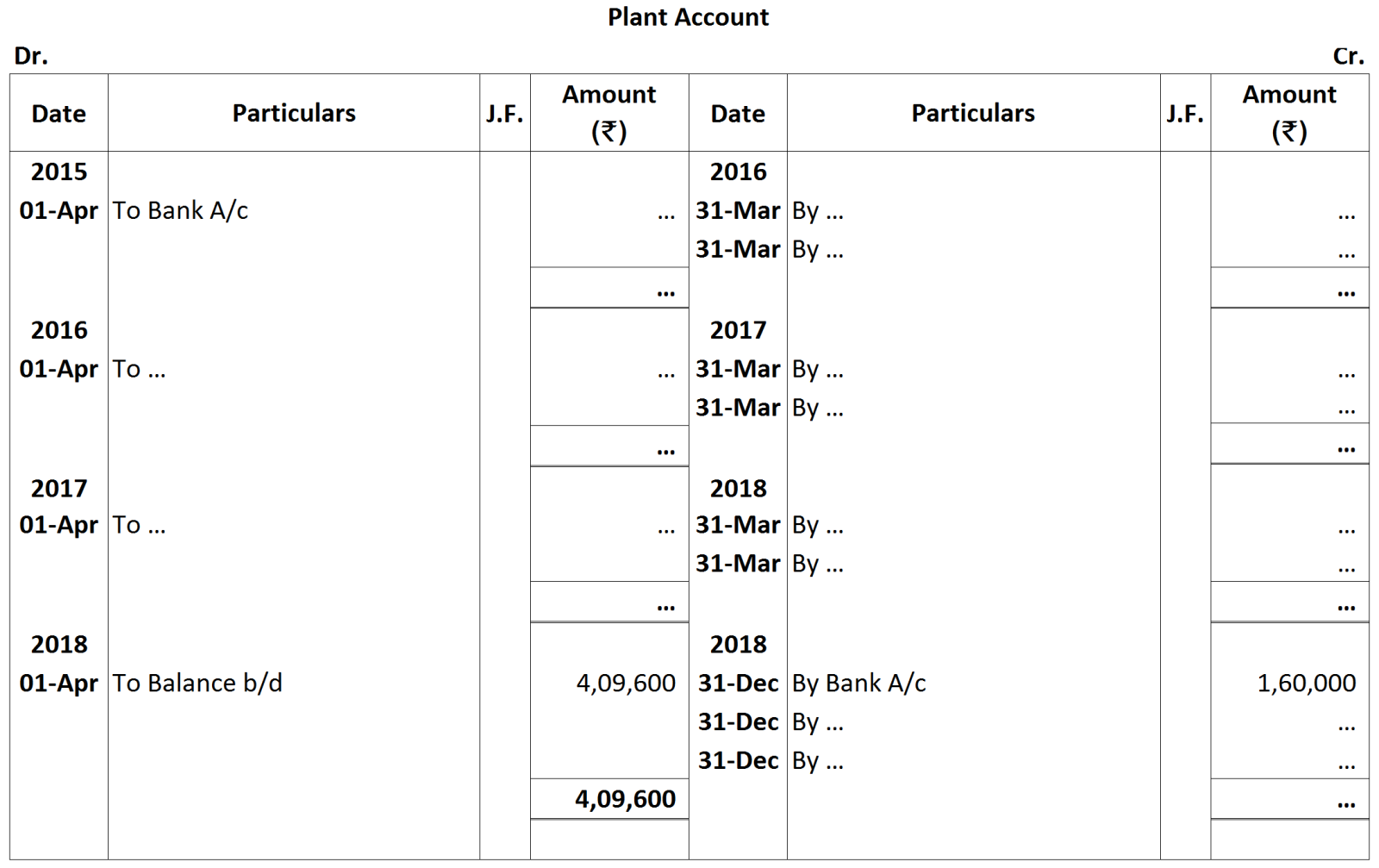

1st April, 2017

|

Machinery A/c

|

20,00,000

|

|

|

Provision for Depreciation A/c

|

8,00,000

|